Technical Textiles Market Size, Share Global Analysis Report, 2026-2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Technical Textiles Market Summary

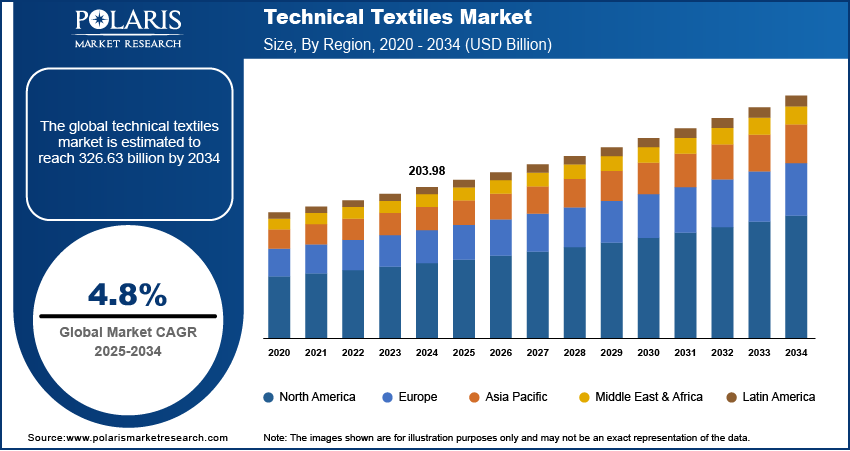

The global technical textiles market size was valued at USD 213.69 billion in 2025. It is expected to grow from USD 223.86 billion in 2026 to USD 326.55 billion by 2034, at a CAGR of 4.83% from 2026 to 2034. The market growth is primarily driven by increasing demand for high-performance materials, growing awareness of safety and stringent regulations, and advancements in material science and manufacturing technologies.

Market Statistics

Key Takeaways

- North America is projected to witness the highest CAGR of 4.30% during the projection period. The market is driven by strong demand across automotive and industrial sectors.

- Asia Pacific led the global market with a 43.3% revenue share in 2025. Rapid industrialization and urbanization are driving the regional market growth.

- The indutech segment is projected to grow at a 5.32% CAGR due to increased demand for technical textiles designed for specialized industrial applications.

- The 3D weaving segment dominated the market with a 13.0% share in 2025 due to its ability to generate intricate and highly integrated three-dimensional structures.

- The nanofibers segment is projected to witness the fastest growth at a 8.10% CAGR. This is due to their growing usage in smart textiles.

*Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The augmentation of automotive industry pushed by surging vehicle demand is driving the need for technical textiles.

- Geotextiles are growingly utilized in construction and infrastructure projects which are used in enhancing soil robustness, drainage, irrigation regulation and road longevity.

- Technical textiles plays a vital role in several sectors such as automotive, construction, healthcare, aerospace, and protective clothing.

- Increased manufacturing prices may act as a restraining factor for the market growth.

What are Technical Tiles?

Technical textiles refer to a specialized category of textiles designed and engineered for specific functionalities, surpassing the conventional role of fabrics primarily for clothing or decoration. Unlike traditional textiles, technical textiles are developed with a purpose-driven approach, incorporating advanced materials and technologies to introduce specific performance characteristics. This diverse category of textiles encompasses a wide range of applications, including geotextiles, medical textiles, agro-textiles, protective clothing, and industrial textiles.

Technical textiles are defined as textile substances and commodities utilized essentially for their technical conduct and operational attributes instead of their attractiveness or ornamental features. This is one of the speediest evolving domains of the textile industry, which is making futuristic, pepped-up fabric designed not just to look captivating but to dispense a notable added value in the context of operationalization. The textile coating procedure is broadly utilized in the making of technical textiles.

The technical textiles market has emerged as a rapidly growing market within the broader textile industry. It plays an important role in various sectors such as automotive, construction, healthcare, aerospace, and protective clothing. The increasing demand for high-performance materials in industries such as automotive and aerospace, where lightweight and durable textiles are crucial, has been a significant driver. Also, the growing awareness of safety and stringent regulations related to workplace safety and environmental protection have propelled the demand for protective clothing and geotextiles. Advancements in material science and manufacturing technologies have enabled the development of innovative technical textiles with properties such as flame resistance, antibacterial capabilities, and smart functionalities, further expanding their applications.

Key Usage Areas of Technical Textiles

- Geotextiles: These textiles are used in construction and civil engineering applications to reinforce soil, build roads, and control water erosion.

- Medical Textiles: They are used in hospitals, surgeries, or any healthcare facility. They help prevent infections and ensure hygiene in healthcare centers.

- Protective Textiles: They are designed for firefighters, soldiers, and industrial workers to provide protection from heat, hazardous chemicals, and other workplace threats.

- Smart Textiles: Embedded with sensors and electronics for tracking health status, body temperature, or other environmental parameters. These find applications in wearable technology and health care monitoring.

- Industrial Textiles: These are used in conveyor belts, filtration, and reinforcement in the heavy industries sector. They help make operations more efficient and effective.

- Filter Textiles: These are used in air, water, and chemical filtration. They help control pollution.

Market Dynamics

Expansion of Automotive Industry

The automotive industry relies heavily on technical textiles for both safety and comfort. The expansion of the industry, driven by rising vehicle demand, is driving the requirement for technical textiles. According to the International Organization of Motor Vehicle Manufacturers, vehicle sales in 2024 were 82,061,217, showcasing the growth of the industry. These textiles are used in airbags, seat belts, headliners, carpets, insulation, and soundproofing materials. The demand for such specialized materials is growing as global car production rises, especially in developing countries. Technical textiles offer lightweight, durable, and cost-effective solutions, helping manufacturers improve fuel efficiency and meet safety standards. Additionally, the rise in electric vehicles (EVs) and innovations in vehicle interiors are boosting the need for advanced textiles, thereby driving technical textiles market growth.

Rising Demand from Construction Industry

Technical textiles, particularly geotextiles, are increasingly used in construction and infrastructure projects. They help improve soil strength, drainage, erosion control, and road durability. Governments around the world are investing in highways, bridges, railways, and smart cities, all of which require long-lasting and efficient construction materials. According to the US Census Bureau, in the US alone, monthly construction spending in February 2025 was USD 2,195.8 billion. Geotextiles are cost-effective and help extend the life of infrastructure, reducing long-term mainteNanoce costs. Their use also supports sustainable construction practices by improving water management and reducing environmental impact. The need for reliable construction solutions is rising as urbanization and industrialization continue, driving the demand for technical textiles in the infrastructure sector.

Technical Textiles Types

| Type | Description | Applications |

| Woven Technical Textiles | Sturdy, structural textile construction | Car parts, conveyor belts |

| Nonwoven Technical Textiles | Bonded fibers without weaving or knitting | Mask production, cleaning fabrics, filtering materials |

| Knitted Technical Textiles | Elastic textile construction | Sports clothes, medical bandages |

Segment Analysis

Market Assessment by Application

The technical textiles market segmentation, based on end use, includes clothtech, sportech, mobiltech, indutech, hometech, packtech, and others. The indutech segment is expected to witness significant growth with a CAGR of 5.32% during the forecast period due to the increasing demand for specialized textiles designed to cater to industrial applications. Indutech textiles have several applications in a wide range of industries, including manufacturing, construction, and automotive, where their unique properties contribute significantly to enhanced performance and durability. The rising need for advanced materials that can withstand extreme conditions, such as high temperatures, corrosive environments, and mechanical stress, has driven the adoption of Indutech textiles, thereby driving the segmental growth.

Market Evaluation by Technology

The technical textiles market segmentation, based on technology, includes 3D knitting, 3D weaving, thermo-forming, Nano fibers, finishing treatments, and others. The 3D weaving segment dominated the market with 13.0% share in 2025 due to its ability to create complex and highly integrated three-dimensional structures, overcoming traditional textile manufacturing methods. This innovative technique involves interlacing multiple layers of fibers in different directions, providing enhanced strength, durability, and structural enhancement to the final product.

Regional Insights

By region, the study provides the technical textiles market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific dominated the market with 43.3% revenue share in 2025, fueled by rapid industrialization, urban development, and increasing healthcare needs. Countries such as China, Japan, South Korea, and Australia are leading the market with rising investments in infrastructure, automotive production, and medical technology. The region offers low-cost manufacturing and a large workforce, attracting global textile producers. Demand for geotextiles, medical textiles, and industrial fabrics is rising due to ongoing development projects and stricter safety standards. In addition, increasing awareness about hygiene, personal protection, and environmental concerns is supporting the growth of advanced and sustainable technical textiles across the region.

In India, demand for technical textiles is growing rapidly, due to its expanding manufacturing base, rising domestic demand, and supportive government policies. The “Make in India” initiative and special incentives for the textile industry are encouraging investments in technical textile production. Applications in agriculture, construction, healthcare, and transportation are growing rapidly. The demand for technical textiles in India is further driven by a large workforce, increasing infrastructure development, and rising safety awareness in industrial sectors. The growth of e-commerce and rising consumer demand for functional and durable products are further pushing the market growth.

North America is expected to witness 4.30% CAGR during the forecast period, driven by strong demand across automotive, healthcare, defense, and industrial sectors. The region benefits from high R&D investments, leading to innovations in smart textiles, protective clothing, and medical fabrics. Government regulations around worker safety and defense needs have further boosted the use of advanced materials. The US has a well-established manufacturing base and a strong presence of leading textile companies. Additionally, the growing focus on sustainability and eco-friendly production is pushing North American manufacturers to develop more efficient and environmentally responsible technical textile solutions, thereby driving market growth.

Key Players and Competitive Analysis

The market opportunity is constantly evolving, with numerous companies striving to innovate and distinguish themselves. Leading global corporations dominate the market by leveraging extensive research and development, and advanced techniques. These companies pursue strategic initiatives such as mergers and acquisitions, partnerships, and collaborations to enhance their product offerings and expand into new markets.

New companies are impacting the market by introducing innovative products to meet the demand of specific sectors. The competitive trend is amplified by continuous progress in product offerings. A few major players in the market include 3M, Ahlstrom Corporation, DuPont De Nemours & Co., Freudenberg & Co., GSE Environmental Inc., HINDOOSTAN MILLS, Huesker Synthetic GmbH, Johns Manville, Proctor and Gamble, and Royal Ten Cate.

3M Company, originally founded in 1902 as Minnesota Mining and Manufacturing Company, is a diversified technology and science corporation headquartered in St. Paul, Minnesota. The company has operations in over 70 countries and sales in ∼200 countries. 3M business operates in various industries, including industrial, safety, healthcare, and consumer markets. The company’s portfolio features more than 60,000 products categorized into key business segments. The Safety & Industrial segment offers personal protective equipment, adhesives, abrasives, and tapes for industries such as automotive and construction. In the Transportation & Electronics segment, 3M provides solutions for automotive OEMs and electronic components. The Healthcare segment focuses on medical supplies, dental products, and health information systems for hospitals and clinics. Meanwhile, the Consumer segment includes home improvement items, office supplies, and consumer health products. 3M operates manufacturing facilities across various regions, including North America, and significant operations in Asia Pacific, particularly in India and China. The company also maintains a robust presence throughout Europe. 3M offers Nextel ceramic fibers, textiles, fabrics, and yarns designed for manufacturing applications requiring high strength, thermal stability, and durability in demanding industrial environments.

DuPont de Nemours, Inc. (DuPont) is an American multinational chemical company established in 1802 and headquartered in Wilmington, Delaware. Over its long history, the company has transitioned from producing gunpowder to focusing on specialty chemicals and advanced materials. The company’s operations are divided into two main segments: Electronics & Industrial and Water & Protection. The Electronics & Industrial segment provides materials and products for sectors including semiconductors, circuit boards, displays, healthcare, aerospace, and printing. This segment’s offerings include semiconductor manufacturing materials, interconnect films and laminates, as well as industrial polymers and lubricants. The Water & Protection segment focuses on water treatment technologies, personal protective materials, and building solutions. Products in this segment include reverse osmosis membranes under the FilmTec brand, Tyvek building materials, Styrofoam insulation, Corian surfaces, and fibers such as Kevlar and Nomex used in protective clothing. DuPont operates in ∼50 countries and serves customers in over 90 countries. It maintains manufacturing plants, research facilities, and technical centers across North America, Europe, Asia Pacific, and Latin America. Major locations include the US, Belgium, China, and India. DuPont offers high-performance fabrics, fibers, and nonwovens-such as Kevlar, Nomex, and Tyvek, and is designed for protection, durability, and diverse industrial applications, including safety, construction, and transportation.

Key Companies in Technical Textiles Market

- 3M

- Ahlstrom Corporation

- DuPont De Nemours & Co.

- Freudenberg & Co.

- GSE Environmental Inc.

- HINDOOSTAN MILLS

- Huesker Synthetic GmbH

- Johns Manville

- Proctor and Gamble

- Royal Ten Cate

Technical Textiles Industry Developments

-

April 2026: Teijin Frontier revealed the development of a new stretch polyester yarn. The company stated that the yarn offers exceptional compatibility with high-performance polyester materials. (source: teijin-frontier.com)

-

February 2026: Rieter announced the successful completion of the acquisition of Barmag. According to Rieter, the acquisition will help the company become a leading system provider for synthetic and natural fibers. (source: rieter.com)

- March 2025: three innovative test methods for soft ballistic inserts were developed and launched through a collaboration between Hohenstein and DuPont, aiming to enhance comfort, mobility, and performance in protective body armor. (Source: hohenstein.com)

- January 2025: Messe Frankfurt announced that the Dornbirn Global Fiber Congress Asia would be hosted for the first time in India at Techtextil India, positioning the country as a key hub for advanced fiber innovation and sustainable technical textiles. (Source: messefrankfurt.com)

Technical Textiles Market Segmentation

By Technology Outlook (Revenue USD Billion, 2021–2034)

- 3D Knitting

- 3D Weaving

- Thermo-Forming

- Nano Fibers

- Finishing Treatments

- Others

By Application Outlook (Revenue USD Billion, 2021–2034)

- Clothtech

- Sportech

- Mobiltech

- Indutech

- Hometech

- Packtech

- Others

By Regional Outlook (Revenue USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Future of Technical Textiles Market

The technical textiles industry is poised to grow because of the increased need for advanced fabrics in industrial and infrastructural sectors. The rising use of intelligent fabrics that come fitted with electronic components and sensors will lead to higher functionality. Sustainability trends will help eco-friendly fabrics gain more popularity. Moreover, nanotechnology innovations are expected to aid growth in many sectors, such as the healthcare sector and even the military.

Technical Textiles Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 213.68 billion |

| Market Size Value in 2026 | USD 223.86 billion |

| Revenue Forecast by 2034 | USD 326.55 billion |

| CAGR | 4.83% from 2026 to 2034 |

| Base year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, region and segmentation. |

FAQ's

The market size was valued at USD 213.68 billion in 2025 and is projected to grow to USD 326.55 billion by 2034.

The global market is projected to register a CAGR of 4.83% during the forecast period.

Asia Pacific held the largest share of the global market in 2025.

A few key players in the market are 3M, Ahlstrom Corporation, DuPont De Nemours & Co., Freudenberg & Co., GSE Environmental Inc., HINDOOSTAN MILLS, Huesker Synthetic GmbH, Johns Manville, Proctor and Gamble, and Royal Ten Cate.

The 3D weaving segment dominated the market in 2025, due to its ability to create complex and highly integrated three-dimensional structures, overcoming traditional textile manufacturing methods.

The indutech segment is expected to witness significant growth during the forecast period due to the increasing demand for specialized textiles designed to cater to industrial applications.

Download Sample Report of Technical Textiles Market

Please fill out the form to request a customized copy of the research report.