Threat Intelligence Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Threat Intelligence Market Summary

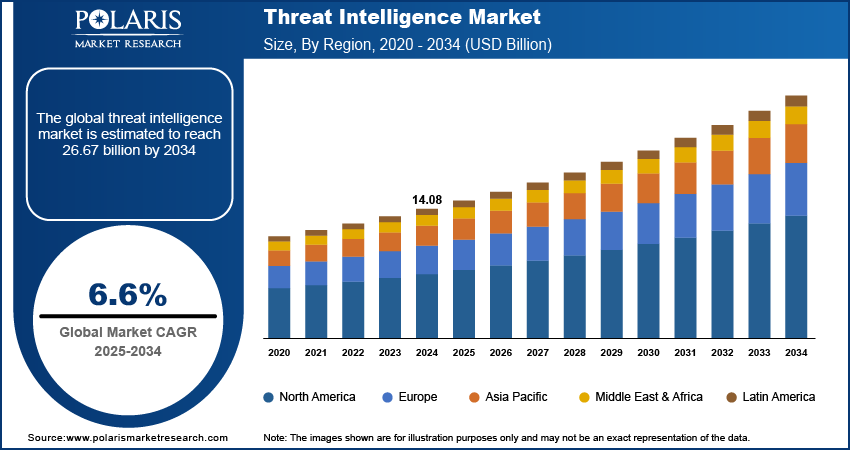

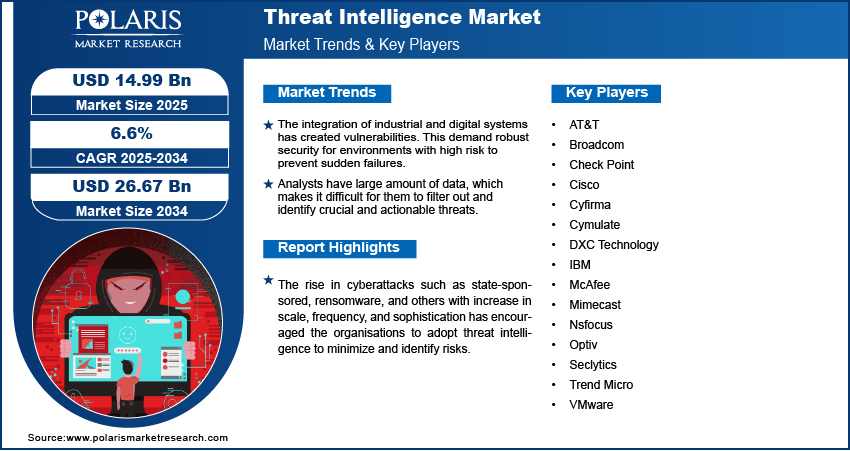

The global threat intelligence market is estimated around USD 14.99 billion in 2025,?with consistent growth anticipated during 2026–2034. Growth is driven by rising cyberattack frequency and increasing enterprise cybersecurity investment. The market is projected to grow at a CAGR of 6.6% during the forecast period.

Market Statistics

Key Takeaways

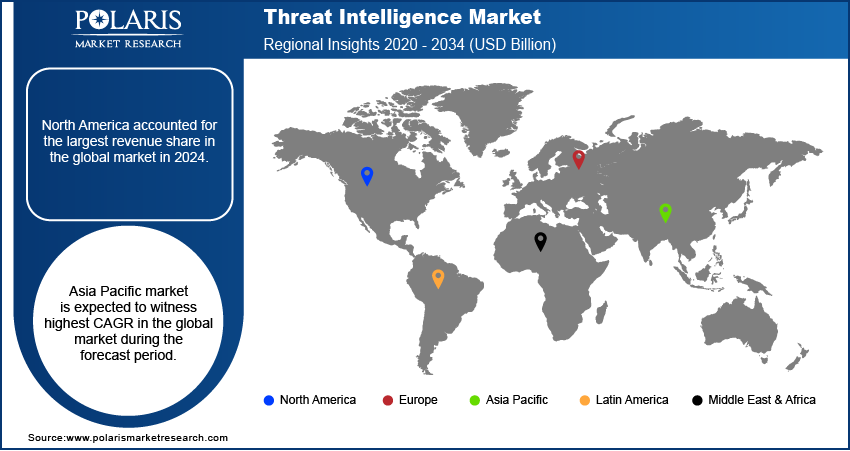

- North America accounted for the largest regional share of around 40.5% in 2025, supported by high ransomware incidence, mature security infrastructure, strong cybersecurity spending, and presence of leading vendors.

- Asia Pacific is projected to grow at a CAGR of 12.3%, driven by rapid digital transformation, increasing internet penetration, expanding cloud adoption, and rising cyberattack frequency across emerging economies.

- By Component, Platforms segment accounted for the largest share of approximately 61.8% in 2025, driven by demand for centralized dashboards, automated analytics, real-time threat visibility, and seamless security integration.

- By Type, Strategic Intelligence segment accounted for the largest share of around 34.7% in 2025, supported by board-level focus on long-term cyber risk planning, geopolitical threat assessment, and compliance requirements.

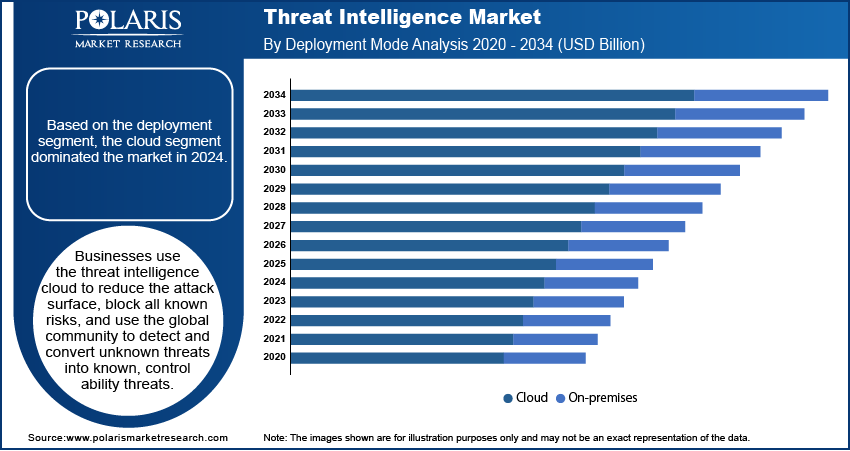

- By Deployment, Cloud-Based segment accounted for the largest share of nearly 64.2% in 2025, driven by scalability, flexible pricing, rapid implementation, and real-time analytics integration across enterprises.

- By Enterprise Size, Large Enterprises segment accounted for the largest share of around 68.9% in 2025, supported by substantial cybersecurity budgets, complex IT infrastructures, and continuous threat monitoring needs.

- By Application, Incident Response segment is projected to grow at a CAGR of 6.8%, driven by increasing demand for faster breach containment, improved investigation accuracy, and intelligence-driven response capabilities.

- By Industry Vertical, BFSI segment accounted for the largest share of approximately 29.8% in 2025, driven by high exposure to financial cybercrime and sustained investment in advanced threat intelligence solutions.

Industry Dynamics

- Rising ransomware and advanced persistent threats expand demand for proactive monitoring.

- Increasing cybersecurity budgets accelerate adoption across the threat intelligence market.

- High implementation and subscription costs restrict adoption among small and mid-sized enterprises.

- AI-driven analytics and automation models create long term opportunities across the cyber threat intelligence industry.

What Is the Threat Intelligence Market?

Threat intelligence refers to the structured collection, validation, and analysis of data related to cyber threats, threat actors, malware campaigns, and system vulnerabilities. The threat intelligence market covers technology platforms, intelligence feeds, analytics engines, and managed services that convert raw threat data into actionable insights. The cyber threat intelligence industry supports enterprises, government agencies, and critical infrastructure operators that require continuous visibility into external risk exposure. Enterprise threat intelligence solutions are designed to improve risk prioritization, incident readiness, and strategic security planning across complex IT environments.

It comprises software platforms that collect data from open-source intelligence, dark web monitoring, technical indicators, and proprietary research networks. The platforms use analytics, automation, and risk scoring in context to help security teams. The threat intelligence services comprise managed intelligence operations, customized reporting, and advisory services that help organizations with limited capabilities in-house. Intelligence feeds offer real-time indicators of compromise and threat actor profiles for use in enterprise security systems.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The threat intelligence solution differs from SIEM, SOAR, XDR, and MDR solutions based on the primary goal. SIEM and XDR solutions target log collection and event correlation in internal environments. SOAR concentrates on workflow automation and response orchestration. MDR delivers outsourced detection and response services. On the other hand, the cyber threat intelligence is centered on the monitoring of external threats, tracking of adversaries, and predictive risk analysis. This creates a gap where the threat intelligence platforms and enterprise threat intelligence solutions act as strategic enablers of proactive cybersecurity measures rather than being incident response solutions.

Drivers & Opportunities

Rising ransomware and advanced persistent threats: The number of ransomware attacks and cyber campaigns is also rising. As per the IBM 2026 X-Force Threat Index report, ransomware and extortion groups grew 49% year-over-year as the ecosystem became more fragmented, with public victim numbers up 12%, while vulnerability exploits led the way in attacks at 40% of X-Force's 2025 incidents. Furthermore, targeted attacks also increased in critical infrastructure, BFSI, healthcare, and government sectors. The financial impact of these attacks is also rising for enterprises. The growing demand for threat intelligence due to rising cyberattacks is a major driving factor for the threat intelligence market.

Rise in cybersecurity expenditure and regulatory pressure: The amount of budget being allocated by enterprises for advanced cybersecurity solutions is rising. Boards and risk committees are giving importance to external threat visibility and early risk detection. Regulatory compliance threat intelligence requirements under data protection and critical infrastructure laws are strengthening procurement decisions. This effect of the increased cybersecurity spending supports the growth of the cyber threat intelligence and enterprise threat intelligence solutions market.

Restraints & Challenges

High implementation and subscription costs: The implementation of intelligent platforms requires integration with the existing security infrastructure, thereby resulting in high initial investment costs. The subscription model for high-end intelligence feeds and services incurs high operational costs. Small and medium-sized businesses are challenged by budget and resource constraints. Budget and resource constraints are some of the factors that restrict the use of threat intelligence platforms.

Opportunity

AI integration and real-time analytics adoption: AI in the threat intelligence market is improving automated threat detection and faster risk assessment. The real-time threat analytics market solutions provide security analysts with the capability to detect new attack patterns with higher accuracy. In February 2026, VAST Data and CrowdStrike formed a strategic partnership at VAST Forward 2026 to combine VAST Data's data governance capabilities with CrowdStrike's Falcon threat protection for end-to-end AI security from data ingestion to inference. The threat intelligence automation market is growing with machine learning-based data enrichment and prioritization. This technology-focused development supports scalable growth across the global threat intelligence market.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the threat intelligence market by component, type, deployment, enterprise size, application, and industry vertical to help readers identify the fastest expanding and most attractive demand segments.

By Component

-

Platforms

Platforms accounted for the highest revenue share in 2025 within the threat intelligence platforms market. Strong demand for centralized dashboards, automated analytics, and integration with existing security systems supported adoption. Companies are likely to have integrated platforms that can give real-time visibility into threats and risk scores in context. Subscription-based pricing models create recurring revenue streams for large enterprise customers.

-

Services

The services segment is expected to register the fastest growth due to an increase in demand for managed intelligence and advisory support. Organizations have not had the expertise in-house to interpret complex threat data. Managed monitoring and tailored reporting services increase efficiency. This is a positive factor for growth in the threat intelligence services market.

By Type

-

Strategic

Strategic intelligence led the market in 2025 due to the boardroom focus on long-term cyber risk planning. Enterprises need macro-level threat analysis to inform security investments and policy choices. This market supports executive reporting and geopolitical risk analysis. However, demand is still high in the regulated sectors.

-

Operational

Operational intelligence is projected to grow at the fastest CAGR during the forecast period, driven by increasing need for real-time threat investigation. The increasing number of cyber events drives the demand in the security operations centers. The ability to perform continuous monitoring helps drive the market.

By Deployment

-

Cloud-based

Cloud deployment model had the largest market share in 2025 due to scalability and flexible pricing models. Enterprises are looking for faster deployment cycles and remote access. Cloud integration enables real-time data updates and analytics processing. The model is widely adopted by large and medium-sized enterprises.

-

Hybrid

The hybrid model is anticipated to register the highest growth rate during the forecast period due to the requirement for a balance between control over compliance and flexibility. Businesses are combining cloud analytics with on-premise storage of data.

By Enterprise Size

-

Large enterprises

Large enterprises led the market in 2025 due to increased cybersecurity spending and complex infrastructures. Advanced analytics adoption is limited to large enterprises. Continuous threat monitoring strengthens segment revenue share.

-

SME

SMEs are projected to grow at the fastest CAGR during the forecast period, driven by rising ransomware exposure and awareness initiatives. Managed service models improve accessibility for smaller organizations. Subscription pricing supports steady adoption growth.

Source: Polaris Market Research Analysis

By Application

-

Incident response

Incident response led the market in 2025, as breach events continue to rise. Organizations are interested in quicker containment and better accuracy in investigations. Intelligence integration improves response effectiveness.

-

Threat hunting

Threat hunting is expected to register the highest CAGR through the forecast period, as organizations adopt active cybersecurity measures. Organizations are interested in early detection of stealthy network threats. Increasing attack complexity fuels segment growth.

By Industry Vertical

-

BFSI

BFSI led the market in 2025, as organizations are highly vulnerable to financial cybercrime. Ongoing fraud monitoring remains a key priority. Spending on intelligence solutions continues to drive the segment.

-

Healthcare

The healthcare industry is expected to witness the highest CAGR over the forecast period due to the increasing number of ransomware attacks on patient data. The use of digital healthcare solutions expands the network attack surface. Compliance with regulations enhances the adoption of threat intelligence.

Regional Analysis

North America Market Assessment

North America threat intelligence market dominated in 2025, driven by high incidence of ransomware attacks and strong cybersecurity spending across the US and Canada. According to the 2025 Homeland Threat Assessment Report, there were more than 5,600 public ransomware attacks globally in 2024, including over 2,600+ victims in the US and 105 in New Jersey alone, and the critical manufacturing, finance, IT, and government sectors are likely to remain the top targets in 2025. Industry data indicates that the US accounts for a significant share of global ransomware incidents, with critical infrastructure and BFSI sectors reporting sustained attack volumes. Mature security operations infrastructure and presence of leading vendors support revenue concentration across the cyber threat intelligence industry.

Asia Pacific Threat Intelligence Market Insights

Asia Pacific threat intelligence market is expanding at the fastest pace due to rapid digital transformation and increasing cyberattack frequency across China, India, Japan, and South Korea. According to the World Economic Forum, the ASEAN region is the fastest-growing internet market globally, with 125,000 new users every day, and the digital economy is expected to contribute an additional USD 1 trillion to the region's GDP over the next decade. Additionally, internet penetration and cloud adoption in the region continue to increase, thereby increasing the attack surface.

Europe Threat Intelligence Market Overview

Europe had the second-largest market share in the threat intelligence market, due to the strict data protection regulations and the growing number of cross-border cyber events. The number of GDPR violation reports filed with European data protection authorities rose 22% to a record 443 per day in 2025, according to the study by DLA Piper, due to digital growth and cyber threats, although the amount of fines remained stable at about USD 1.32 billion, pushing the total amount of fines to USD 7.81 billion. In addition, the regulatory requirements for GDPR and the NIS2 directive raise the need for continuous threat intelligence monitoring and reporting.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The threat intelligence market has moderate levels of consolidation, with major cybersecurity vendors dominating the market share. Competition is driven by data accuracy, global threat research capability, and platform integration strength. Companies invest in AI-driven analytics and automation to strengthen differentiation. Strategic partnerships and growth of in-house intelligence feeds help in long-term positioning in the cyber threat intelligence market.

Key players in the threat intelligence industry include CrowdStrike Holdings Inc., Palo Alto Networks Inc., Recorded Future Inc., Google Cloud, Cisco Systems Inc., IBM Corporation, Check Point Software Technologies Ltd., Fortinet Inc., Trend Micro Inc, Anomali Inc., Flashpoint Intelligence Inc., ThreatConnect Inc., and others.

Vendor Capability Matrix and Benchmarking

The vendor capability matrix compares and contrasts the major players in the threat intelligence market based on intelligence scope, automation level, and integration capabilities. The analysis is performed on five major vendors with strong market presence and research infrastructure.

| Company | Breadth vs Depth | Automation Maturity | Integration Capabilities | Benchmark Position |

| CrowdStrike Holdings Inc. | Strong global coverage with deep endpoint intelligence expertise | High AI-driven automation within Falcon platform | Strong integration with cloud-native and XDR ecosystems | Leader |

| Palo Alto Networks Inc. | Broad intelligence coverage across network, cloud, and endpoint | Advanced automation integrated within Cortex platform | Extensive integration across enterprise security stack | Leader |

| IBM Corporation | Broad industry coverage with strong consulting depth | Moderate to high automation within QRadar ecosystem | Strong integration with enterprise IT and SIEM systems | Strong Contender |

| Cisco Systems Inc. | Wide threat telemetry across network infrastructure | Moderate automation with analytics-driven detection | Deep integration within network and hybrid environments | Strong Contender |

| Check Point Software Technologies Ltd. | Strong network-focused intelligence depth | Moderate automation across unified security architecture | Integrated within firewall and gateway ecosystems | Established Player |

Source: Polaris Market Research Analysis

Key Players

- Anomali Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems Inc.

- CrowdStrike Holdings Inc.

- Flashpoint Intelligence Inc.

- Fortinet Inc.

- Google Cloud

- IBM Corporation

- Palo Alto Networks Inc.

- Recorded Future Inc.

- ThreatConnect Inc.

- Trend Micro Inc.

Industry Developments

- February 2026: Palo Alto Networks has launched Unit 42 Managed XSIAM 2.0 (MSIAM), an AI-driven SOC service that combines 24/7 elite expert monitoring with the industry's most comprehensive 250-hour breach response guarantee to enhance cyber resilience and close the gap between attack speed and defense.

- January 2026: Check Point launched AI-driven Exposure Management, unifying threat intelligence, dark web insights, attack surface visibility, and automated remediation across 75+ security controls to prioritize and close remediation gaps against AI-era cyber threats.

- September 2025: CrowdStrike introduced Threat AI, the first agentic threat intelligence solution on the Falcon platform, allowing AI agents to reason, hunt, and respond to threats throughout the entire attack chain.

Threat Intelligence Market Segmentation

By Component Outlook (Revenue, USD Billion, 2021-2034)

- Platforms

- Services

By Type Outlook (Revenue, USD Billion, 2021-2034)

- Strategic

- Tactical

- Operational

- Technical

By Deployment Outlook (Revenue, USD Billion, 2021-2034)

- Cloud-Based

- On-Premise

- Hybrid

By Enterprise Size Outlook (Revenue, USD Billion, 2021-2034)

- SME

- Large enterprise

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Incident response

- Threat hunting

- Fraud detection

- Security information management

By Industry Vertical Outlook (Revenue, USD Billion, 2021-2034)

- BFSI

- Healthcare

- Government & Defense

- IT & Telecom

- Energy & Utilities

- Retail

- Manufacturing

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Threat Intelligence Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 14.99 Billion |

| Market Size in 2026 | USD 15.96 Billion |

| Revenue Forecast by 2034 | USD 26.57 Billion |

| CAGR | 6.6% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Threat Intelligence Market FAQ's

• The global market size was valued at USD 14.99 billion in 2025 and is projected to grow to USD 26.57 billion by 2034.

• North America dominates due to high ransomware incidence, strong cybersecurity spending and early adoption of advanced enterprise threat intelligence solutions.

• Major applications include incident response, threat hunting, fraud detection, and security information management.

• A few of the key players in the market are CrowdStrike Holdings Inc., Palo Alto Networks Inc., Recorded Future Inc., Google Cloud, Cisco Systems Inc., IBM Corporation, Check Point Software Technologies Ltd., Fortinet Inc., Trend Micro Inc, Anomali Inc., Flashpoint Intelligence Inc., ThreatConnect Inc., and others.

• The market is fueled by the growing number of cyberattacks against enterprises and critical infrastructure, as well as the rising allocation of cybersecurity budgets.

Download Sample Report of Threat Intelligence Market

Please fill out the form to request a customized copy of the research report.