U.S. Analytical Instrumentation Market Emerging Trends and Key Innovations, 2025-2034

REPORT DETAILS

REPORT DETAILS

Market Statistics

What is U.S. analytical instrumentation market size?

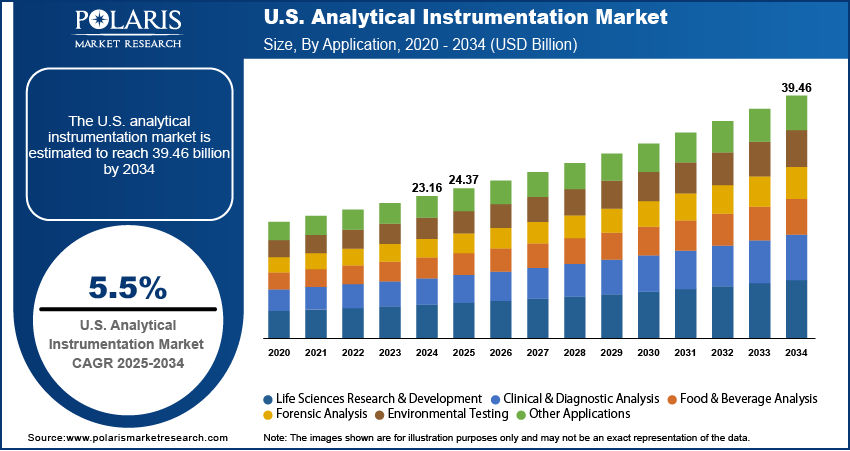

The global U.S. analytical instrumentation market size was valued at USD 23.16 billion in 2024, growing at a CAGR of 5.5% from 2025 to 2034. Rising adoption of analytical instruments across pharma, biotech, and healthcare labs and focus on precision diagnostics and personalized medicine drives the market.

Key Insights

- The spectroscopy instruments segment dominated the U.S. analytical instrumentation market in 2024.

- Hospitals and diagnostic laboratories to grow fastest due to rising demand for precision and automated diagnostics.

Industry Dynamics

- Increasing pharma and biotech research fuels adoption of advanced instruments.

- Rising precision diagnostics require increase healthcare analytical instrument usage.

- Integration of AI and automation with analytical instruments opens new possibilities for manufacturers.

- High expense and maintenance cost restrict adoption among smaller laboratories.

Market Statistics

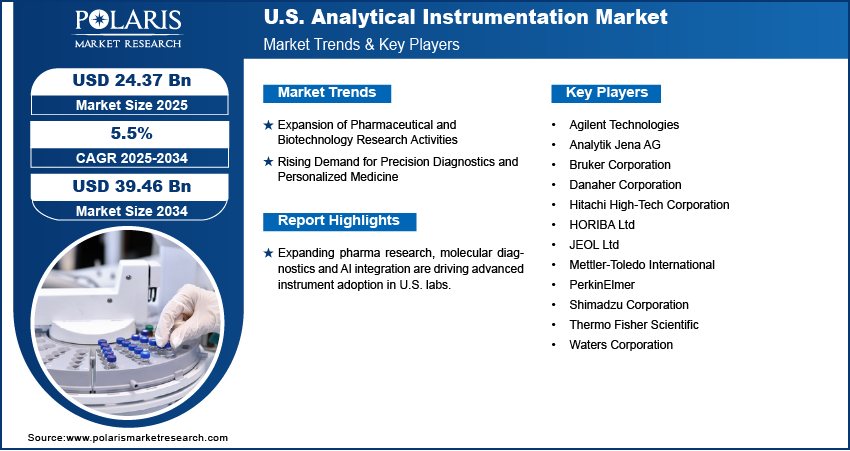

- 2024 Market Size: USD 23.16 Billion

- 2034 Projected Market Size: USD 39.46 Billion

- CAGR (2025–2034): 5.5%

The U.S. market of analytical instrumentation involves a broad variety of equipment including spectrometers, chromatographs, analyzers, and microscopes employed for qualitative as well as quantitative analysis in the field of pharmaceutical, biotechnology, environmental, and industrial sectors. These instruments facilitate exact measurement, material characterization, and quality control in laboratory and process settings.

Growing pharmaceutical research, biotechnology manufacturing expansion and increasing emphasis on precision diagnostics are driving demand for advanced analytical systems across the country. For example, in March 2023, Waters launched Next-Generation Alliance iS HPLC system to add to its range of analytical instruments by combining intelligent diagnostics and touchscreen interface to reduce lab errors by as much as 40%.

However, high equipment costs with complex maintenance procedures along with lack of skilled personnel continue to impede wider usage of analytical instruments in small labs. Convergence of AI-powered automation, cloud-stored data management, and transportable analytical solutions offers new chances for digital transformation and operational efficiency enhancement in U.S. laboratories and testing stations.

Drivers & Opportunities

Which are the factors driving U.S. analytical instrumentation market growth?

Expansion of Pharmaceutical and Biotechnology Research Activities: Growing pharmaceutical and biotechnology research activities are fueling demand for advanced analytical equipment to support drug discovery services, formulation analysis and quality control. For instance, in October 2025, Waters Corporation launched the Xevo CDMS, a charge-detection mass spectrometer enabling rapid, precise measurement of large biomolecules for next-generation biotherapeutics.

Rising Demand for Precision Diagnostics and Personalized Medicine: Growing demand for accurate diagnostics and personalized medicine is enhancing the utilization of analytical equipment in health care testing labs. Increasing focus on early disease detection and patient-specific treatment methods is stimulating the application of advanced molecular and biochemical analysis platforms for precise biomarker identification and diagnostic verification in clinical laboratories.

Segmental Insights

Product Analysis

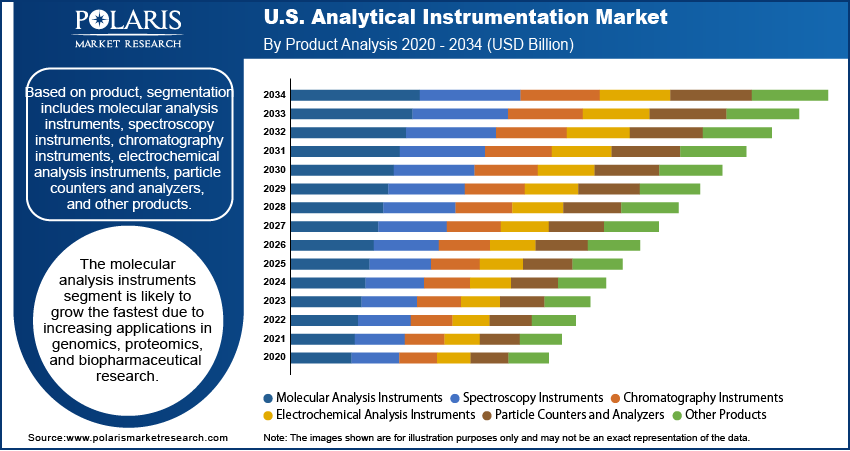

By component, the market is divided into molecular analysis instruments, spectroscopy instruments, chromatography instruments, electrochemical analysis instruments, particle counters and analyzers, and other products. The spectroscopy instruments segment dominated the U.S. analytical instrumentation market in 2024 due to its extensive scope of applications across chemical analysis, life sciences, and material testing.

The molecular analysis instruments projected to develop at the highest CAGR over the forecast period, fueled by increasing applications in genomics, proteomics, and precision diagnostics. In addition, increasing R&D spending in biopharmaceutical development is enhancing the adoption of advanced molecular instruments.

Technology Analysis

Based on construction type, the market is segmented into polymerase chain reaction, spectroscopy, microscopy, chromatography, flow cytometry, sequencing, microarray, and others. Chromatography led the construction type segment in 2024, due to its pivotal position in drug quality analysis and compound differentiation.

The sequencing segment is expected to grow at the highest CAGR as a result of growing genomic studies and personal medicine initiatives. Moreover, the incorporation of next-generation sequencing platforms in the diagnostic pipeline is enhancing demand in research and clinical applications.

Application Analysis

Based on application, the market is segmented into life sciences research & development, clinical & diagnostic analysis, food & beverage analysis, forensic analysis, environmental testing, and other applications. Life sciences research & development segment led the market during 2024 with increasing investment in biopharmaceutical studies, molecular biology, and drug discovery, due to robust funding from private as well as government institutions.

The clinical & diagnostic analysis segment is projected to witness the highest CAGR, driven by increasing adoption of molecular diagnostics and biomarker testing. In addition, increasing healthcare infrastructure and emphasis on disease identification at early stages are boosting analytical instrument usage in clinical laboratories.

End User Analysis

Based on end user, the market is segmented into pharmaceutical & biotechnology industry, research and academic institutes, hospitals & diagnostic laboratories, environmental testing laboratories, food & beverage companies, chemical & petrochemical industries, and other end users. The pharmaceutical & biotechnology industry segment accounted for the highest market share in 2024, driven by rigorous analytical requirements in drug discovery, quality control, and bioprocessing.

The hospitals & diagnostic laboratories segment is anticipated to register the highest CAGR, driven by increasing volumes of diagnostic testing and precision medicine programs. Furthermore, automated analytical platforms are driving better accuracy and efficiency in clinical testing activities.

Key Players & Competitive Analysis

The U.S. market for analytical instrumentation is competitive, with manufacturers and integrators focusing on developing smart, IoT-enabled, and automated solutions to expand detection accuracy and response efficacy. In addition, partnerships between global OEMs and local contractors are accelerating technology adoption across large infrastructure and industrial projects.

Who are the major players in U.S. analytical instrumentation market?

Some of the major firms in the U.S. analytical instrumentation sector are Thermo Fisher Scientific, Agilent Technologies, PerkinElmer, Shimadzu Corporation, Bruker Corporation, Waters Corporation, Danaher Corporation, Mettler-Toledo International, HORIBA Ltd, Analytik Jena AG, Hitachi High-Tech Corporation, and JEOL Ltd.

Key Players

- Agilent Technologies

- Analytik Jena AG

- Bruker Corporation

- Danaher Corporation

- Hitachi High-Tech Corporation

- HORIBA Ltd

- JEOL Ltd

- Mettler-Toledo International

- PerkinElmer

- Shimadzu Corporation

- Thermo Fisher Scientific

- Waters Corporation

U.S. Analytical Instrumentation Industry Developments

September 2025: Oxford Instruments strengthened its analytical instrumentation portfolio with the WITec 360 confocal Raman microscope, featuring the Hexalight spectrometer to characterize materials faster and with greater accuracy.

March 2025: Advanced Instruments reported the acquisition and merger with Nova Biomedical to enhance its analytical instrumentation portfolio in the biopharmaceutical and clinical markets.

October 2024: Agilent Technologies introduced the InfinityLab III LC Series to enhance its analytical instrumentation portfolio through enhanced automation and better liquid chromatography performance.

U.S. Analytical Instrumentation Market Segmentation

By Product Outlook (Revenue, USD Billion, 2020–2034)

- Molecular Analysis Instruments

- Spectroscopy Instruments

- Chromatography Instruments

- Electrochemical Analysis Instruments

- Particle Counters and Analyzers

- Other Products

By Technology Outlook (Revenue, USD Billion, 2020–2034)

- Polymerase Chain Reaction

- Spectroscopy

- Microscopy

- Chromatography

- Flow Cytometry

- Sequencing

- Microarray

- Others

By Application Outlook (Revenue, USD Billion, 2020–2034)

- Life Sciences Research & Development

- Clinical & Diagnostic Analysis

- Food & Beverage Analysis

- Forensic Analysis

- Environmental Testing

- Other Applications

By End User Outlook (Revenue, USD Billion, 2020–2034)

- Pharmaceutical & Biotechnology Industry

- Research and Academic Institutes

- Hospitals & Diagnostic Laboratories

- Environmental Testing Laboratories

- Food & Beverage Companies

- Chemical & Petrochemical Industries

- Other End Users

U.S. Analytical Instrumentation Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 23.16 Billion |

| Market Size in 2025 | USD 24.37 Billion |

| Revenue Forecast by 2034 | USD 39.46 Billion |

| CAGR | 5.5% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 23.16 billion in 2024 and is projected to grow to USD 39.46 billion by 2034.

The global market is projected to register a CAGR of 5.5% during the forecast period.

A few of the key players in the market are Thermo Fisher Scientific, Agilent Technologies, PerkinElmer, Shimadzu Corporation, Bruker Corporation, Waters Corporation, Danaher Corporation, Mettler-Toledo International, HORIBA Ltd, Analytik Jena AG, Hitachi High-Tech Corporation, and JEOL Ltd.

The spectroscopy instruments segment dominated the market in 2024 due to its widespread use in chemical, pharmaceutical, and life sciences analysis.

The hospitals & diagnostic laboratories segment is projected to grow fastest due to rising demand for precision diagnostics and automated testing solutions.

Download Sample Report of U.S. Analytical Instrumentation Market

Please fill out the form to request a customized copy of the research report.