U.S. Autonomous Underwater Vehicle Market Trends Analysis, Growth, 2026-2034

REPORT DETAILS

U.S. Autonomous Underwater Vehicle Market Summary

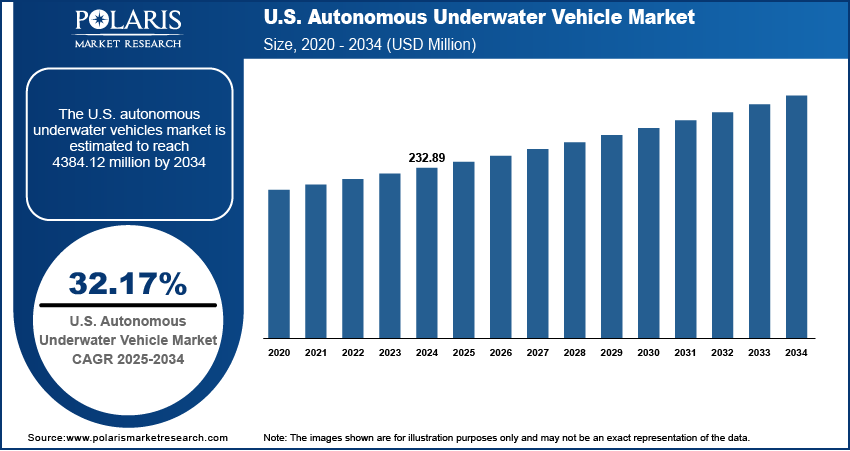

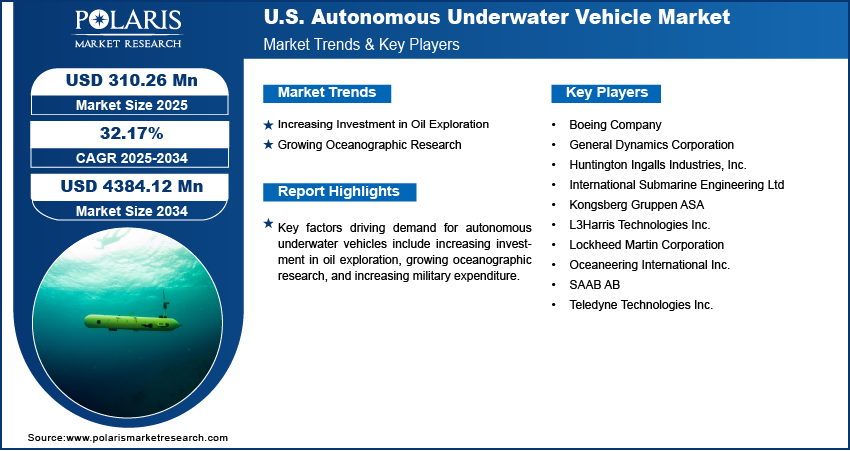

The U.S. autonomous underwater vehicle market size was valued at USD 310.26 million in 2025. The market is projected to grow at a CAGR of 32.17% from 2026 to 2034. Key factors driving demand for autonomous underwater vehicles include increasing investment in oil exploration, growing oceanographic research, and increasing military expenditure.

Market Statistics

Key Takeaways

- The navigation segment accounted for a major revenue share of 41.01% in 2025. This is due to continuous investment by the U.S. Navy in advanced navigational technologies.

- The large segment accounted for a 44.2% revenue share in 2025. This is owing to the ability to operate at greater depths.

- The torpedo segment held the largest revenue share of 38.42% in 2025. The hydrodynamic design of torpedoes allows them to achieve higher speeds and extended ranges.

- The sensors segment accounted for a major revenue share of 35.9% in 2025. Sensors are widely used for studying marine ecosystems and climate change.

- The synthetic aperture sonars segment is expected to grow at a 14.2% CAGR. The rising need for high-resolution imaging for commercial and defense applications contributes to the segment's growth.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations

Industry Dynamics

- The growing investment in oil exploration in the U.S. is boosting demand for autonomous underwater vehicles (AUVs) as energy companies require more efficient and cost-effective machines to survey and map the ocean floor.

- The growing oceanographic research is fueling the need for AUVs, as these vehicles can reach depths and endure conditions that limit human divers or traditional research vessels.

- Increasing need for underwater infrastructure inspection is projected to create a lucrative market opportunity.

- High development and maintenance costs are projected to hamper the demand for autonomous underwater vehicles.

AI Impact on U.S. Autonomous Underwater Vehicle Market

- AI enhances U.S. AUVs with smarter navigation and real-time decision-making, improving mission efficiency.

- Machine learning enables AUVs to adapt to dynamic underwater environments, boosting data collection accuracy.

- AI-driven automation reduces reliance on human operators, lowering operational costs and risks.

- Integration with AI accelerates data processing, enabling rapid analysis for defense, research, and energy sectors.

- Growing AI investment spurs innovation, expanding market demand, and driving competition among U.S. AUV manufacturers.

An autonomous underwater vehicle is a self-operating, unmanned robotic system designed to navigate underwater without direct human control. Equipped with sensors, cameras, sonar systems, and navigation technologies, AUVs conduct tasks such as seabed mapping, environmental monitoring, underwater surveillance, and resource exploration. They play a critical role in scientific research, defense, offshore oil and gas industries, and search-and-rescue missions by reaching depths and terrains that are difficult or unsafe for human divers.

The U.S. Navy uses AUVs for mine detection, surveillance, and undersea warfare, strengthening national security capabilities. In the energy sector, offshore oil and gas companies deploy AUVs for pipeline inspection, subsea infrastructure monitoring, and resource exploration. Scientific institutions also utilize them for oceanographic studies, climate research, and marine biodiversity assessment. Advancements in sensor technologies, artificial intelligence, and battery life are further fueling AUV adoption in the U.S.

Source: Polaris Market Research Analysis

The demand for autonomous underwater vehicles in the U.S. is driven by the growing military expenditure. According to a report by STOCKHOLM INTERNATIONAL PEACE RESEARCH INSTITUTE, military spending by the USA rose by 5.7% in 2024. This accelerated the research and development of more sophisticated and reliable AUV models, which encouraged militaries to adopt them. Moreover, rising military expenditure is propelling defense agencies in the country to modernize their fleets with autonomous underwater vehicles to enhance their maritime surveillance and strengthen underwater warfare capabilities. Therefore, the growing military expenditure in the U.S. is fueling the demand for autonomous underwater vehicles.

Autonomous Underwater Vehicles (AUVs) vs Remotely Operated Vehicles (ROVs)

| Feature | Autonomous Underwater Vehicle (AUV) | Remotely Operated Vehicle (ROV) |

| Control | Completely autonomous operation | Tethered control by operators |

| Mobility | Great maneuverability and mobility | Limited by tethering system |

| Depth Range | Able to operate in deep sea and ultra-deep sea environments | Restricted by tethering system depth limits |

| Cost | Expensive but efficient | Relatively inexpensive but more dependent on operators |

| Uses | Exploration and survey | Repair and maintenance |

Source: Polaris Market Research Analysis

Drivers & Opportunities/Trends

Increasing Investment in Oil Exploration: The growing investment in oil exploration in the U.S. is boosting demand for autonomous underwater vehicles (AUVs) as energy companies require more efficient and cost-effective machines to survey and map the ocean floor. AUVs equip exploration teams with advanced tools for high-resolution seabed imaging, pipeline inspection, and environmental monitoring, which are essential for identifying new oil reserves and assessing drilling sites. The push for deeper and more remote offshore exploration, especially in challenging environments such as the Arctic or ultra-deep waters, is making AUVs crucial, as they operate autonomously for extended periods and collect critical data without human intervention. Moreover, rising oil prices and the need to replace depleting reserves are encouraging companies in the U.S. to invest in advanced underwater technologies, further driving the adoption of AUVs.

Growing Oceanographic Research: Scientists and research institutions involved in oceanographic research are increasingly relying on AUVs to explore deep-sea ecosystems, monitor the impacts of climate change, and study marine biodiversity, as these vehicles can reach depths and endure conditions that limit human divers or traditional research vessels. AUVs equip researchers with advanced sensors and imaging tools, enabling them to gather high-resolution data on ocean currents, temperature, salinity, and underwater geology with greater accuracy and efficiency. The push for more comprehensive and frequent oceanographic studies, fueled by concerns over climate change, ocean acidification, and resource depletion, is further accelerating the adoption of AUVs.

Emerging Trends in Underwater Robotics

Autonomous underwater vehicle (AUV) systems are evolving towards greater efficiency. Swarm technology AUVs are being designed to collaborate to increase the speed and reach of data acquisition. Affordable underwater drones are being introduced to increase access to the technology. The implementation of machine learning and artificial intelligence technologies has assisted in the improvement of the autonomous ability of the robot by facilitating its ability to navigate, adapt, and make decisions. Through the adoption of the modular design approach, modifications can easily be made via different sensor and tool attachments.

Source: Polaris Market Research Analysis

Segmental Insights

Technology Analysis

Based on technology, the segmentation includes collision avoidance, navigation, communication, imagery, and propulsion. The navigation segment accounted for a major revenue share of 41.01% in 2025 due to continuous investment by the U.S. navy in advanced navigational technologies for deep-sea reconnaissance. Accurate navigation ensured the successful completion of seabed mapping, mine countermeasure operations, and scientific exploration, where even minor errors could compromise mission objectives. The growing use of advanced inertial navigation systems (INS), Doppler velocity logs (DVL), and acoustic positioning technologies significantly boosted demand. Oil and gas companies also adopted high-precision navigation to conduct pipeline inspections and monitor subsea infrastructure, further strengthening the segment’s dominance.

The collision avoidance segment is projected to grow at a rapid pace in the coming years, owing to the rising offshore energy activities, coupled with the growing use of autonomous vehicles for deep-sea mining and undersea cable inspections. Advances in sonar-based sensing, machine learning integration, and autonomous decision-making software make modern collision avoidance technologies more reliable and adaptive. Defense agencies are also emphasizing survivability in contested waters, pushing for vehicles equipped with robust collision avoidance systems.

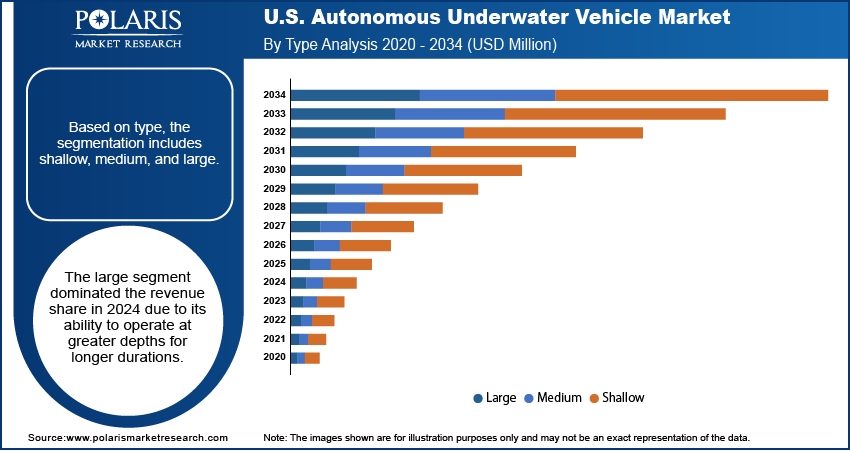

Type Analysis

Based on type, the segmentation includes shallow, medium, and large. The large segment dominated the revenue share of 44.2% in 2025 due to its ability to operate at greater depths for longer durations. Large autonomous vehicles carried advanced payloads, including high-resolution sonars and synthetic aperture imaging systems, which enabled them to perform long-endurance operations in strategic waters. The U.S. Navy’s focus on expanding undersea dominance and strengthening maritime security drove substantial investments in large vehicles with advanced navigation, propulsion, and communication technologies. Moreover, research institutions and energy companies favored these vehicles for deep-ocean exploration and subsea infrastructure inspection, further enhancing their adoption.

Shape Analysis

In terms of shape, the segmentation includes torpedo, laminar flow body, streamlined rectangular style, and multi-hull. The torpedo segment held the largest revenue share of 38.42% in 2025 due to its hydrodynamic design, which enabled it to achieve higher speeds, extended ranges, and superior maneuverability in deep and shallow waters. Defense operators favored this shape for missions such as anti-submarine warfare training, mine countermeasure operations, and long-endurance reconnaissance due to its proven efficiency and reliability. Research organizations and commercial users also relied on torpedo designs for seabed mapping and environmental monitoring. The shape’s compatibility with advanced propulsion systems and diverse payloads further strengthened its adoption, making it the most widely deployed configuration across defense, scientific, and industrial applications.

Payload Analysis

Based on payload, the segmentation includes sensors, cameras, synthetic aperture sonars, echo sounders, acoustic doppler current profilers, and others. The sensors segment accounted for a major revenue share of 35.9% in 2025 due to their ability to study marine ecosystems and climate change. Advanced sensors, including inertial measurement units, pressure sensors, and magnetometers, enabled autonomous underwater vehicles to gather critical data in real time, ensuring accurate positioning and reliable performance in challenging underwater environments. The U.S. Navy invested heavily in sensor-integrated vehicles to improve mine detection, seabed mapping, and intelligence-gathering capabilities, while energy companies deployed them for subsea infrastructure inspection and leak detection.

The synthetic aperture sonars segment is expected to grow at a robust pace of CAGR 14.2% during the forecast period, owing to the rising need for high-resolution imaging for both defense and commercial applications. These systems provide detailed seabed maps and object classification capabilities that conventional sonar technologies cannot match, making them crucial for mine countermeasure operations, undersea reconnaissance, and environmental assessments. Offshore industries are increasingly adopting synthetic aperture sonars to support pipeline inspections, subsea construction monitoring, and resource exploration due to their ability to deliver precise images in turbid waters. Defense agencies are also prioritizing these payloads for missions in contested maritime zones where accuracy and clarity of data directly impact mission success.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The U.S. autonomous underwater vehicle (AUV) market features a competitive landscape dominated by major defense and aerospace contractors alongside specialized marine technology firms. Key players include Boeing, General Dynamics, and Lockheed Martin, which leverage their defense expertise to develop advanced AUVs for military applications. L3Harris Technologies and Teledyne Technologies contribute through the use of sophisticated sensors and integrated systems. Oceaneering International and Huntington Ingalls focus on subsea operations and naval integration, respectively. International Submarine Engineering Ltd. brings niche expertise in unmanned submersibles. Kongsberg Gruppen and SAAB AB maintain a strong presence in the U.S. market through partnerships and technology exports. Competition is driven by innovation in endurance, autonomy, and sensor capabilities, with growing demand from defense, offshore energy, and scientific research sectors shaping strategic developments across the industry.

Major companies operating in the U.S. autonomous underwater vehicle industry include Boeing Company; General Dynamics Corporation; Huntington Ingalls Industries, Inc.; International Submarine Engineering Ltd; Kongsberg Gruppen ASA; L3Harris Technologies Inc.; Lockheed Martin Corporation; Oceaneering International Inc.; SAAB AB; and Teledyne Technologies Inc.

Key Companies

- Boeing Company

- General Dynamics Corporation

- Huntington Ingalls Industries, Inc.

- International Submarine Engineering Ltd

- Kongsberg Gruppen ASA

- L3Harris Technologies Inc.

- Lockheed Martin Corporation

- Oceaneering International Inc.

- SAAB AB

- Teledyne Technologies Inc.

Industry Developments

March 2026: Anduril announced that the Defense Innovation Unit (DIU) and the U.S. Navy selected the company for the XL-AUV program. According to Anduril, the selection was done through IU’S competitive Commercial Solutions Opening after the completion of the longest XL-AUV demonstration conducted to date. (source: helsing.ai)

October 2025: Helsing announced the acquisition of Blue Ocean, a specialist in AUVs. According to Helsing, the acquisition will involve the integration of Blue Ocean’s manufacturing and hardware capabilities with Helsing’s AI. It is aimed at enhancing Helsing’s Maritime Defence Programme. (source: anduril.com).

U.S. Autonomous Underwater Vehicle Market Segmentation

By Technology Outlook (Revenue, USD Million, 2021–2034)

- Collision Avoidance

- Navigation

- Communication

- Imagery

- Propulsion

By Type Outlook (Revenue, USD Million, 2021–2034)

- Shallow

- Medium

- Large

By Shape Outlook (Revenue, USD Million, 2021–2034)

- Torpedo

- Laminar Flow Body

- Streamlined Rectangular Style

- Multi-hull

By Payload Outlook (Revenue, USD Million, 2021–2034)

- Sensors

- Cameras

- Synthetic Aperture Sonars

- Echo Sounders

- Acoustic Doppler Current Profilers

- Others

By Application Outlook (Revenue, USD Million, 2021–2034)

- Army & Defense

- Petroleum & Gas

- Environmental Security & Tracking

- Oceanography

- Archeology & Exploration

- Search & Rescue Activities

U.S. Autonomous Underwater Vehicle Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 310.26 Million |

| Market Size in 2026 | USD 391.36 Million |

| Revenue Forecast by 2034 | USD 4384.12 Million |

| CAGR | 32.17% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

U.S. Autonomous Underwater Vehicle Market FAQ's

The market size was valued at USD 310.26 million in 2025 and is projected to grow to USD 4384.12 million by 2034.

The market is projected to register a CAGR of 32.17% during the forecast period.

A few of the key players in the market are Boeing Company; General Dynamics Corporation; Huntington Ingalls Industries, Inc.; International Submarine Engineering Ltd; Kongsberg Gruppen ASA; L3Harris Technologies Inc.; Lockheed Martin Corporation; Oceaneering International Inc.; SAAB AB; and Teledyne Technologies Inc.

The large segment dominated the market with revenue share of 44.2% in 2025.

The synthetic aperture sonars segment is projected to witness the fastest growth rate of CAGR 14.2% during the forecast period.

Download Sample Report of U.S. Autonomous Underwater Vehicle Market

Please fill out the form to request a customized copy of the research report.