U.S. Outdoor Power Equipment Market Size, Industry Trends, 2026-2034

REPORT DETAILS

U.S. Outdoor Power Equipment Market Summary

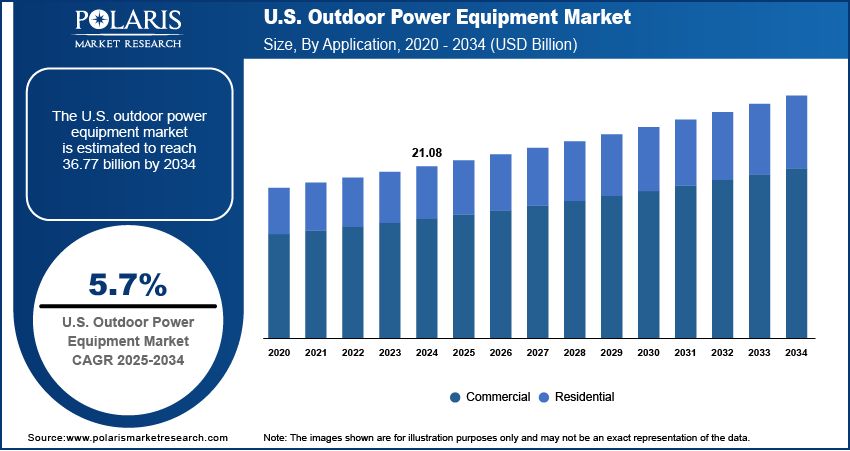

The U.S. outdoor power equipment market size was valued at USD 22.26 billion in 2025. The market is anticipated to register a CAGR of 5.7% from 2026 to 2034. The growth is driven by strong retail and e-commerce presence, and high demand for residential landscaping and lawn care.

Market Statistics

Key Takeaways

- The mowers segment held a market share of 35.49% in 2025 . The segment's strong performance can be attributed to the presence of lawns and to the growing landscaping trend in the U.S.

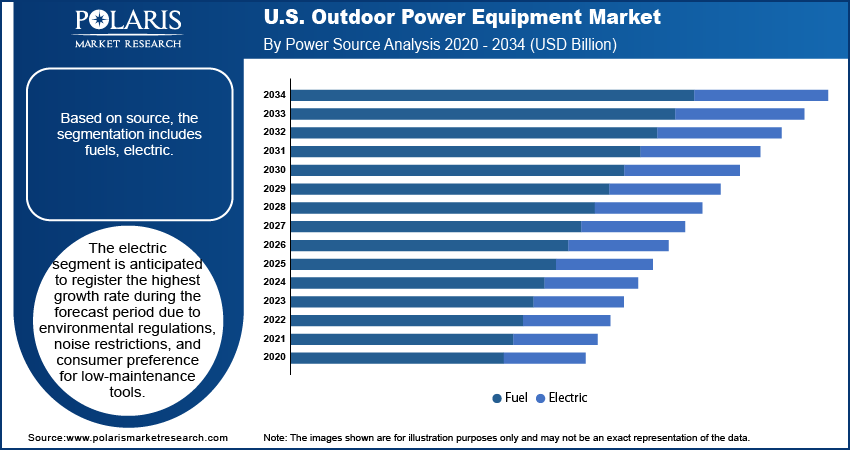

- The electrical category is estimated to record a high CAGR of 6.9% during the forecast period . Increasing environmental concerns and the adoption of eco-friendly tools are driving the segment's growth.

- The residential application segment occupied a dominant market share of 63.92% in 2025 . Increased spending by homeowners on tools like mowers and pressure washers contributed to the dominance of the segment.

- Connection/AI-based products are projected to exhibit a CAGR of 6.4% during the forecast period . Increasing needs for intelligent outdoor equipment will boost the segment's growth..

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Strong retail and e-commerce presence is expected to accelerate the outdoor power equipment industry growth

- High demand for residential landscaping and lawn care is projected to drive the outdoor power equipment demand.

- The rising government initiatives for infrastructure development across the country to make cities greener is likely to pave the demand for the industry.

- High maintenance costs and environmental concerns related to emissions from fuel-powered equipment limits the growth.

AI Impact on the Industry

- AI enhances product development in the outdoor power equipment market by analyzing usage patterns, environmental conditions, and performance data to design more efficient, durable, and user-friendly equipment.

- AI-powered predictive maintenance systems monitor equipment health in real time, enabling early detection of wear and tear, reducing downtime, and extending the life of machines.

- AI-driven customer analytics help manufacturers better understand consumer preferences, seasonal demand patterns, and usage behavior, allowing for more targeted product designs and marketing strategies.

- Integration of AI in manufacturing operations streamlines production workflows, improves quality control, reduces material waste, and optimizes inventory management across outdoor power equipment facilities.

Outdoor power equipment refers to mechanical or motorized tools used for outdoor tasks such as lawn care, gardening, landscaping, and maintenance. Common types include lawn mowers, chainsaws, trimmers, blowers, and snow throwers, which can be powered by gas, electricity, or batteries. These tools are widely used by homeowners, commercial landscapers, and professionals to maintain outdoor spaces efficiently.

Source: Polaris Market Research Analysis

The expanding commercial landscaping sector in the U.S. significantly fuels the demand for outdoor power equipment. Businesses, municipalities, schools, and real estate developers increasingly rely on professional landscaping services to maintain green spaces, public parks, and campuses. This demand drives higher sales of commercial-grade equipment such as ride-on mowers, hedge trimmers, and chainsaws. Furthermore, the need for efficient, durable, and high-performing tools encourages landscaping companies to regularly upgrade their equipment. Moreover, strong growth in commercial real estate and institutional landscaping contracts further fuels the growth.

Government policies promoting environmentally friendly landscaping practices are influencing the outdoor power equipment industry in the U.S. Several states offer rebates and incentives for purchasing electric or low-emission tools, making them more affordable for both residential and commercial users. Additionally, some municipalities have imposed restrictions on noisy, gas-powered equipment, prompting users to upgrade to compliant models. These regulations are driving faster adoption of eco-friendly equipment. Federal funding for green infrastructure and urban beautification projects further creates opportunities for OPE manufacturers and landscaping service providers to meet regulatory and sustainability goals.

Electric vs Gas Outdoor Equipment

| Factor | Electric Outdoor Equipment | Gas Outdoor Equipment |

| Source of Power | Electricity (cords or batteries) | Gasoline-powered internal combustion engine |

| Functioning | For light and medium-level use | Has high efficiency for heavy-duty use |

| Maintenance | Low maintenance since no fuel system | High maintenance due to oiling and servicing of engine |

| Noise | Operates quietly | Noisy operations |

| Environmental Effects | Low emissions, environmentally friendly | Higher emissions, less environmentally friendly |

| Costs | Higher initial cost, but lower running costs | Lower initial cost, but higher operating costs |

| Flexibility | Limited by cords or battery charge | Highly flexible |

Source: Polaris Market Research Analysis

Drivers and Trends

Strong Retail and E-commerce Presence: The U.S. has a highly developed retail and e-commerce infrastructure that makes outdoor power equipment widely accessible to consumers. Major home improvement stores like Home Depot, Lowe’s, and Tractor Supply Co. offer an extensive range of products both in-store and online. Additionally, online marketplaces such as Amazon make it easy for consumers to compare brands, read reviews, and receive fast delivery. This ease of access, combined with seasonal promotions and financing options, encourages more frequent purchases and upgrades. The convenience of online shopping boosts U.S. sales of OPE, thereby fueling the growth.

High Demand for Residential Landscaping and Lawn Care: A large number of households in the U.S. have private lawns and gardens, driving consistent demand for outdoor power equipment. Suburban expansion and rising interest in home improvement encourage homeowners to invest in tools like lawn mowers, trimmers, and leaf blowers. Additionally, the increasing popularity of DIY landscaping, supported by online tutorials and home improvement shows, motivates consumers to purchase their own equipment. This trend is especially prominent in states with favorable climates for year-round yard maintenance. Consequently, residential usage fuels the demand for U.S. outdoor power equipment.

Technological Advancements in Outdoor Equipment: The outdoor power equipment industry has undergone numerous technological transformations. This trend has seen the emergence of more intelligent, energy-saving, and user-friendly technologies. A growing number of equipment types incorporate navigation powered by artificial intelligence, mostly in the case of robotic lawn mowers, in order to perform their duties automatically with precision and minimal human input. Modern smart sensors enable tracking of the remaining battery or fuel capacity, blade performance, and the general condition of the machines. Users can then optimize their maintenance activities. Advances made in the field of lithium-ion battery technology have led to longer periods of operation and charging time as well as greater durability. Moreover, ergonomics is playing an increasingly prominent role in the design process.

Source: Polaris Market Research Analysis

Segmental Insights

Equipment Analysis

Based on equipment, the segmentation includes mowers, saws, trimmers, edgers, blowers, tillers & cultivators, others. The mowers segment held the largest share of 35.49% in 2025 due to widespread lawn ownership and strong emphasis on home landscaping. The suburban lifestyle, with expansive lawns and outdoor spaces, fuels high demand for push, ride-on, and robotic mowers. Additionally, seasonal changes and HOA regulations in many neighborhoods encourage regular lawn maintenance. Manufacturers cater to diverse user needs by offering battery, gas, and zero-turn models. The growth of the landscaping services sector further supports the commercial mower segment. Moreover, increasing interest in DIY lawn care further fuels the segment growth.

Power Source Analysis

Based on source, the segmentation includes fuels, electric. The electric segment is anticipated to register the highest growth rate of 6.9% during the forecast period due to environmental regulations, noise restrictions, and consumer preference for low-maintenance tools. Cities such as Los Angeles and New York have implemented bans or limitations on gas-powered landscaping equipment, pushing both consumers and professionals toward battery-powered alternatives. Modern electric tools offer powerful performance, fast charging, and portability, making them ideal for residential use. Government incentives and manufacturer-led innovation in battery technology are further boosting adoption. This shift toward cleaner, quieter fuels the segment growth.

Application Analysis

Based on application, the segmentation includes commercial, and residential. The residential segment held the largest share of 63.92% in 2025 as homeowners across the country regularly invest in lawn mowers, trimmers, blowers, and pressure washers to maintain outdoor spaces. Rising homeownership rates and increasing interest in curb appeal and outdoor aesthetics further fuel product demand. The pandemic further sparked a strong DIY trend, with more people spending time at home and engaging in gardening or yard work. Consumers are further drawn to connected tools that simplify maintenance as smart home integration grows, driving the segment growth.

Functionality Analysis

Based on functionality, the segmentation includes conventional products, connection/ai enabled products. The connection/ai enabled products segment is anticipated to register the highest growth rate of CAGR 6.4% during the forecast period as consumers seek convenience, automation, and efficiency. Products such as robotic lawn mowers with app control, smart irrigation systems, and Bluetooth-enabled equipment offer real-time monitoring, automation, and remote operation. Tech-savvy U.S. homeowners appreciate features such as scheduling, battery health updates, and GPS tracking. Additionally, professional landscapers benefit from AI-driven tools that optimize task efficiency and equipment usage. This growing demand for smart, connected tools is supported by widespread internet access and smart home automation adoption, driving expansion in the segment.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

The U.S. outdoor power equipment market is highly competitive, driven by innovation, brand legacy, and expanding consumer demand. Key players like Deere & Company, The Toro Company, STIHL Group, Husqvarna, and Honda dominate the landscape with wide product portfolios and strong distribution networks. These brands continuously invest in advanced features such as battery powered engines, smart connectivity, and ergonomic designs to meet evolving consumer preferences. Companies like Stanley Black & Decker, Makita Corp, and Techtronic Industries focus on cordless and electric tools, catering to the growing demand for eco-friendly and low-noise solutions. Briggs & Stratton, MTD Holdings Inc., and Ariens Company strengthen their presence through reliability and affordability in the residential and commercial segments. Additionally, brands such as Excel Industries, Robert Bosch, and Yamabiko Corp contribute to innovation in specialized segments. The competitive environment pushes continuous R&D, strategic partnerships, and new product launches across both residential and professional landscaping markets

Key Players

- KO KOBER GROUP

- Andreas Stihl AG & Company KG

- Ariens Company

- Briggs & Stratton

- CHEVRON (China) Trading Co., Ltd.

- Deere & Company

- Excel Industries, Inc.

- HONDA

- Husqvarna

- Makita Corp

- MTD Holdings Inc.

- Robert Bosch

- Stanley Black & Decker

- STIHL Group

- Techtronic Industries

- The Toro Company (US)

- Yamabiko Corp

Future Outlook

The U.S. outdoor power equipment market will continue to grow steadily, driven by the growing demand for electrical and smart devices. The growing demand for residential landscaping services is also driving the expansion of the market. Technological advancements, such as automation and artificial intelligence, are having a significant impact on enhancing the performance of these devices. Increasing e-commerce trends and heightened environmental concerns are resulting in the sustainability of these devices and the use of battery-powered equipment.

Industry Developments

-

January 2026: NexLawn and MOVA highlighted three new product categories at CES 2026. These include the EvoLife smart power tools series, intelligent robotic lawn mowers, and a 60V Intelligent Cordless Garden Tools lineup. (source: prnewswire.com)

-

January 2026: Bosch Power Tools announced new OPE additions to its 18V line. The newly launched products include pole chainsaws, the GKE18V-40 16-inch chainsaw, and the GRT18V-40 string trimmer. According to Bosch Power Tools, the new tools are powered by its 18V platform. (source: bosch-press.com)

U.S. Outdoor Power Equipment Market Segmentation

By Equipment Outlook (Revenue – USD Billion, 2021–2034)

- Mowers

- Saws

- Trimmers

- Edgers

- Blowers

- Backpack Blowers

- Handheld Blowers

- Tillers & Cultivators

- Others

By Power Source Outlook (Revenue – USD Billion, 2021–2034)

- Fuel

- Electric

By Application Outlook (Revenue – USD Billion, 2021–2034)

- Commercial

- Residential

By Functionality Outlook (Revenue – USD Billion, 2021–2034)

- Conventional Products

- Connection/AI Enabled Products

U.S. Outdoor Power Equipment Market Report Scope:

| Report Attributes | Details |

| Market Size in 2025 | USD 22.26 billion |

| Market Size in 2026 | USD 23.46 billion |

| Revenue Forecast by 2034 | USD 36.77 billion |

| CAGR | 5.7% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Insights |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to segmentation. |

Source: Polaris Market Research Analysis

U.S. Outdoor Power Equipment Market FAQ's

The market size was valued at USD 22.26 billion in 2025 and is projected to grow to USD 36.77 billion by 2034.

The market is projected to register a CAGR of 5.7% during the forecast period.

A few key players in the market include AL-KO KOBER GROUP, Andreas Stihl AG & Company KG, Ariens Company, Briggs & Stratton, CHEVRON (China) Trading Co., Ltd., Deere & Company, Excel Industries, Inc., HONDA, Husqvarna, Makita Corp, MTD Holdings Inc., Robert Bosch, Stanley Black & Decker, STIHL Group, Techtronic Industries, The Toro Company (US), and Yamabiko Corp.

The Mower segment accounted for the largest share of 35.49% in 2025.

The electric is expected to witness the fastest growth rate of CAGR 6.9% during the forecast period.

Download Sample Report of U.S. Outdoor Power Equipment Market

Please fill out the form to request a customized copy of the research report.