Ventilators Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Ventilators Market Summary

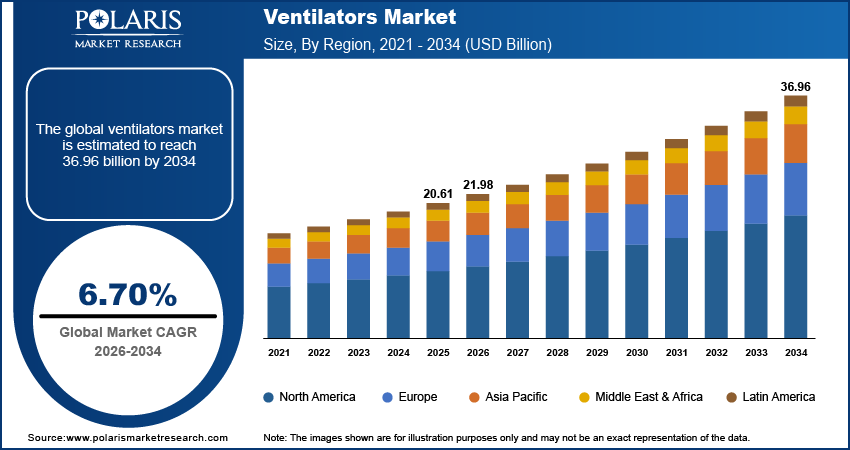

The global ventilators market is estimated around USD 20.61 billion in 2025,?with consistent growth anticipated during 2026–2034. Expansion is supported by rising incidence of ARDS, COPD, asthma, and post-surgical respiratory failure, along with increasing ICU capacity worldwide. The market is projected to grow at a CAGR of 6.70% during the forecast period.

Market Statistics

Key Takeaways

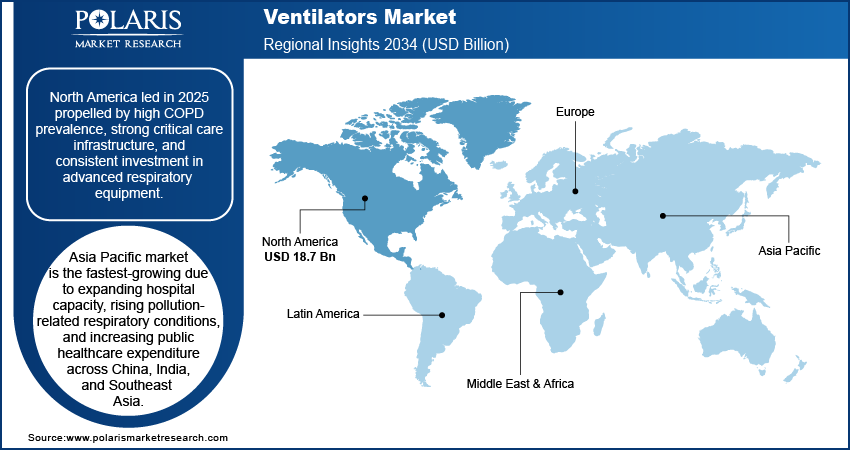

- North America accounted for the largest regional share of around 38.7% in 2025, driven by high prevalence of chronic respiratory diseases, well-established ICU networks, structured reimbursement systems, and advanced emergency response infrastructure.

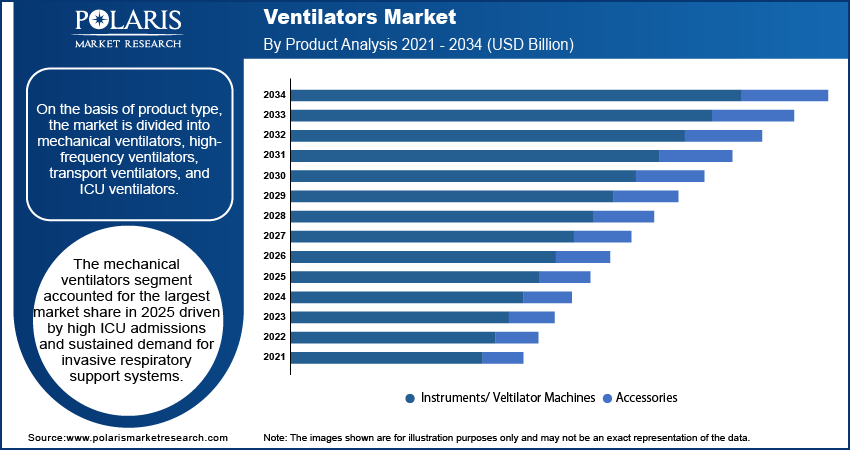

- By Product, Mechanical Ventilators segment accounted for the largest share of approximately 71.5% in 2025, supported by high ICU admissions, demand for invasive respiratory support, and expanding hospital installed base.

- By Interface, Invasive Ventilation segment accounted for the largest share of around 66.2% in 2025, driven by widespread use in respiratory failure management, surgical anesthesia, and controlled airway access in intensive care settings.

- By Mode of Ventilators, Volume-Controlled Ventilation segment accounted for the largest share of nearly 59.4% in 2025, supported by predictable tidal volume delivery, precise respiratory management, and strong adoption across intensive care units.

- By Age Group, Adult segment accounted for the largest share of around 62.8% in 2025, driven by rising ICU admissions, increasing chronic respiratory disorders, and growing post-operative ventilation requirements.

- By End Use, Hospitals segment accounted for the largest share of approximately 68.9% in 2025, supported by expanding ICU infrastructure, rising patient inflow, and strong adoption of advanced respiratory support systems.

Industry Dynamics

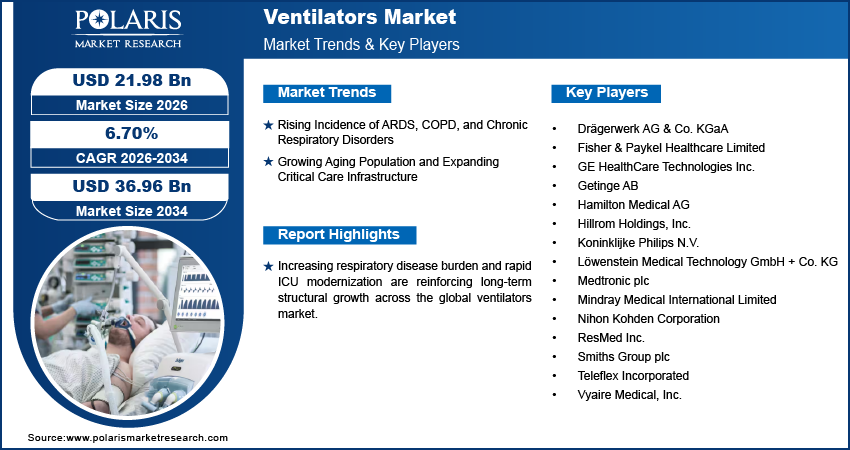

- Rising burden of COPD, ARDS, and chronic respiratory diseases is strengthening demand across ICU and hospital ventilator segments.

- Rapid global aging is increasing long-term ventilatory support requirements in both acute and homecare settings.

- High ICU ventilator costs and regulatory certification requirements create procurement barriers in cost-sensitive healthcare systems.

- AI-enabled ventilators and remote monitoring systems are unlocking long-term intelligent critical care expansion opportunities.

What Are Ventilators?

The ventilators market includes the production and deployment of breathing support machines, forming a defined segment within the respiratory care devices market and broader critical care equipment market. Scope covers ventilator systems only, excluding standalone accessories. The mechanical ventilators market consists of invasive ICU market systems used for intubated patients, along with non-invasive platforms for assisted ventilation. The portable ventilators market caters to emergency and transport requirements, whereas the homecare market caters to long-term respiratory support outside the hospital setting.

To Understand More About this Research: Download Sample Report

Drivers & Opportunities

Incidence of ARDS, COPD, and Asthma: The rising incidence of acute respiratory distress syndrome and chronic respiratory diseases is bolstering the demand in the ARDS ventilators market and COPD ventilator devices market. According to WHO 2024 statistics, COPD is the fourth leading cause of death worldwide, accounting for 3.5 billion deaths in 2021, with nearly 5% of total global deaths, and nearly 90% of premature deaths in low- and middle-income countries. This large disease burden translates into hospitalizations and long-term respiratory support. The rising number of respiratory cases fueled by ICU growth and increasing investment in the healthcare infrastructure are boosting the market growth.

Rising Aging Population Worldwide: Rapidly aging global population is creating increasing vulnerability to respiratory complications boosting the need for ventilatory support. According to United Nations estimates, by the end of the 2070s, the global population aged 65+ is projected to reach 2.2 billion, surpassing the number of children aged 18 and under, while the population aged 80+ is projected to reach 265 billion in the mid-2030s. Aged individuals are more prone to COPD, pneumonia, and post-surgical respiratory failure. The aging population trend creates a robust long-term demand for the ICU facilities and critical care units, thereby creating a robust structural growth trend in the hospital ventilators market.

Restraints & Challenges

High ICU ventilator costs: Modern ICU ventilators are expensive and require high capital outlays. Ventilator pricing analysis shows significant cost variation based on features, automation level, and regulatory approvals. Compliance requirements such as FDA approval for ventilators and CE certification ventilators add development and certification expenses. These variables influence the outcome of cost comparisons for ventilators and are also restrains the adoption of ventilators in emerging markets.

Opportunity

AI-enabled ventilators and smart monitoring systems: The integration of automation and predictive analytics is developing opportunities in the AI -enabled market. Smart ventilator systems employ advanced analytics to optimize ventilation parameters based on real-time patient data. Remote monitoring ventilators facilitate centralized monitoring of multiple ICU beds and step-down units from a single location. Growing Asia Pacific market growth, supported by infrastructure upgrades and technology adoption, strengthens commercial opportunities for intelligent respiratory support systems.

Segmental Insights

This report offers detailed coverage of the market by product type, interface, mode of ventilation, age group, and end user to help readers identify the fastest expanding and most attractive demand segments.

By Product Type

-

Mechanical Ventilators

The mechanical ventilators holds the largest share, driven by high ICU admission rates and critical respiratory care demand. ICU ventilators market adoption remains strong in tertiary hospitals where invasive respiratory support is essential. High-frequency ventilators demand supports specialized neonatal and ARDS treatment settings. Installed base expansion in public and private hospitals sustains steady revenue generation.

-

Transport Ventilators

The transport ventilators market is growing rapidly with increasing demands for emergency response and patient transfer between facilities. Portable, battery-powered, and advanced monitoring capabilities enhance adoption in ambulances and critical care transport vehicles. The market is driven by growing investments in emergency medical infrastructure.

By Interface

-

Invasive Ventilators

The invasive ventilators market represents the largest share propelled by the widespread use of these devices in critical respiratory failure and surgical anesthetic care. These devices are common in intensive care settings where controlled airway access is required. The demand is strong in advanced care facilities.

-

BiPAP Ventilators

The BiPAP drives growth in the non-invasive market. The increasing incidence of COPD and sleep-related breathing disorders is a key factor in driving the adoption of these devices. Compared to the CPAP systems, BiPAP ventilators provide dual pressure levels, which enhance patient comfort and adherence in chronic respiratory diseases.

By Mode of Ventilation

-

Volume-Controlled Ventilation

Volume-controlled ventilation registered the largest market share due to the predictable delivery of tidal volumes in critical care. It is most commonly used in ICUs, where there is a need for precise control of ventilation.

-

Combined-mode ventilation

Combined-mode ventilation is growing at a rapid rate fueled by the need for flexibility between the pressure-controlled ventilation market and volume-controlled environments. The parameters of these modes are automatically changed according to the response of a patient.

By Age Group

-

Adult Critical Care Ventilators

Adult critical care ventilators held the largest market share fueled by the increasing ICU admissions among adults. Chronic respiratory disorders and post-operative requirements drive the market.

-

Neonatal Ventilators

Neonatal is dominating the market in 2025. Increasing preterm births and advancements in neonatal ICUs are driving the growth. Precision control and lung-protective ventilation techniques fuel the demand for specialized equipment.

By End User

-

Hospital Ventilators

The hospital held the largest revenue share driven by the critical care infrastructure. Rising patient flow and ICU capacity expansions continue to drive the demand. Hospitals are the major adopters of advanced invasive equipment.

-

Homecare Ventilators

Homecare ventilators is expanding rapidly due to rising chronic respiratory conditions and preference for long-term home-based therapy. Portable and non-invasive systems support this transition.

Regional Analysis

North America Ventilators Market Assessment

North America market registered leading position in the market due to the rising number of patients suffering from chronic respiratory diseases in the region. According to the American Lung Association, in 2023, 11.1 billion adults in the U.S. suffered from COPD, which imposed an estimated economic burden of USD 50 billion per year. This created a constant clinical demand for invasive and non-invasive ventilation. The availability of well-organized ICUs, reimbursement structures, and emergency response systems further fueled the demand for advanced ventilators in tertiary care centers and ambulatory critical care centers.

Asia Pacific Ventilators Market Insight

Asia Pacific region demonstrated accelerated growth, driven by the rapid expansion of hospitals and ICUs in countries such as China, India, and Southeast Asia. Healthcare investment programs initiated by governments helped raise the number of equipment purchases. According to the Economic Survey 2024-25, the public healthcare spending in India was forecasted to be 1.9% of GDP in FY26. The rising number of respiratory diseases caused by air pollution and smoking-related lung diseases also boosted the demand for ventilator equipment.

Europe Ventilators Market Overview

Europe’s market advanced under strong public healthcare systems and coordinated emergency preparedness strategies. Structured ICU networks across Germany, France, Italy, and the UK supported stable procurement of advanced respiratory support systems. Government initiatives to promote the resilience of the healthcare sector and emergency preparedness further fueled investment in critical care infrastructure. The growing geriatric population and prevalence of chronic respiratory diseases-maintained demand in the hospital and long-term care setting.

Middle East Ventilators Market Assessment

Middle East market is expanding driven by ongoing development of advanced healthcare facilities and specialty hospitals, especially in the GCC countries. The government’s healthcare diversification strategy further fueled the purchase of advanced ICU equipment, such as high-performance ventilators. The increasing incidence of respiratory diseases due to environmental exposure and lifestyle factors maintained the market growth.

Heat Map Analysis

| Region | Market Position | Growth Momentum | Regulatory Strength | Recycling Infrastructure | Secondary Lead Production Base |

| North America | Dominant | High | Very High | Low–Medium | Medium |

| Asia Pacific | High | Very High | Medium | Low | Medium–High |

| Europe | High | Medium | Very High | Medium | Medium |

| Middle East | Emerging | High | Medium | Low | Low |

Technology, Innovation & Investment Insights

-

AI & Automation in Ventilation

Use of automated respiratory support systems is on the rise, with closed-loop modes dynamically adjusting pressure, volume, and oxygen. AI-based waveform analysis enhances patient-ventilator asynchrony detection and minimizes manual adjustments in ICUs.

-

IoT Integration

IoT-enabled ventilators allow for connectivity with hospital EMR systems and monitoring systems. This enhances data integrity, device management, and predictive maintenance for ventilators.

-

Remote Monitoring

Cloud-enabled ICU ventilators facilitate centralized monitoring, remote alarm management, and software updates. In homecare environments, connectivity improves patient compliance and long-term respiratory care.

-

Investment Outlook

Investment in ventilators is now moving towards intelligent, software-based platforms and portable ventilators. Analysis of the ventilator supply chain indicates increasing attention to component localization and digital inventory management to mitigate operational risk and scalability.

Key Players & Competitive Analysis Report

Market has a moderately consolidated market structure, which is dominated by global critical care device manufacturers and respiratory technology experts in the ICU, transport, and non-invasive ventilation markets. The level of competitiveness is driven by the reliability of products, software integration, sophistication of ventilation modes, and adherence to the latest clinical requirements. Large-scale global players use their worldwide distribution channels, existing ICU equipment infrastructure, and comprehensive monitoring solutions to enhance market share in the market based on company strategies. Mid-scale and niche players compete based on innovation in portable devices, high-flow therapy platforms, and home-care respiratory solutions.

Key companies shaping the global market include Drägerwerk AG & Co. KGaA, Fisher & Paykel Healthcare Limited, GE HealthCare Technologies Inc., Getinge AB, Hamilton Medical AG, Hillrom Holdings, Inc., Koninklijke Philips N.V., Löwenstein Medical Technology GmbH + Co. KG, Medtronic plc, Mindray Medical International Limited, Nihon Kohden Corporation, ResMed Inc., Smiths Group plc, Teleflex Incorporated, and Vyaire Medical, Inc.

Key Players

- Drägerwerk AG & Co. KGaA

- Fisher & Paykel Healthcare Limited

- GE HealthCare Technologies Inc.

- Getinge AB

- Hamilton Medical AG

- Hillrom Holdings, Inc.

- Koninklijke Philips N.V.

- Löwenstein Medical Technology GmbH + Co. KG

- Medtronic plc

- Mindray Medical International Limited

- Nihon Kohden Corporation

- ResMed Inc.

- Smiths Group plc

- Teleflex Incorporated

- Vyaire Medical, Inc.

Industry Developments

- July 2024: Air Liquide Medical Systems launched Monnal TEO, a new resuscitation ventilator designed for emergency and critical care settings. The introduction expanded offerings in Ventilators by delivering advanced respiratory support with improved usability and clinical performance.

Market Segmentation

By Product Type Outlook (Revenue, USD Billion, 2021-2034)

- Mechanical ventilators

- High-frequency ventilators

- Transport ventilators

- ICU ventilators

By Interface Outlook (Revenue, USD Billion, 2021-2034)

- Invasive ventilators

- Non-invasive ventilators

- CPAP ventilators

- BiPAP ventilators

By Mode of Ventilation Outlook (Revenue, USD Billion, 2021-2034)

- Volume-controlled ventilation

- Pressure-controlled ventilation

- Combined-mode ventilation

By Age Group Outlook (Revenue, USD Billion, 2021-2034)

- Adult ventilators

- Pediatric ventilators

- Neonatal ventilators

By End User Outlook (Revenue, USD Billion, 2021-2034)

- Hospitals

- Ambulatory surgical centers

- Homecare

- Emergency medical services

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 20.61 Billion |

| Market Size in 2026 | USD 21.98 Billion |

| Revenue Forecast by 2034 | USD 36.96 Billion |

| CAGR | 6.70% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

Hospitals are the largest end-users, followed by home care, emergency transport services, and specialty care facilities.

Key companies include Drägerwerk AG & Co. KGaA, Fisher & Paykel Healthcare Limited, GE HealthCare Technologies Inc., Getinge AB, Hamilton Medical AG, Koninklijke Philips N.V., Medtronic plc, Mindray Medical International Limited, Nihon Kohden Corporation, ResMed Inc., Smiths Group plc, Teleflex Incorporated, and Vyaire Medical, Inc.

North America led the market due to the high incidence of chronic respiratory diseases, well-developed ICU infrastructure, and organized reimbursement structures.

The global market size was valued at USD 20.61 billion in 2025 and is projected to grow to USD 36.96 billion by 2034.

Market is driven by rising incidence of respiratory diseases, development of ICU capacity, growing geriatric population, and advances in AI-enabled and connected ventilation solutions.

Download Sample Report of Ventilators Market

Please fill out the form to request a customized copy of the research report.