Video Conferencing Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Video Conferencing Market Summery

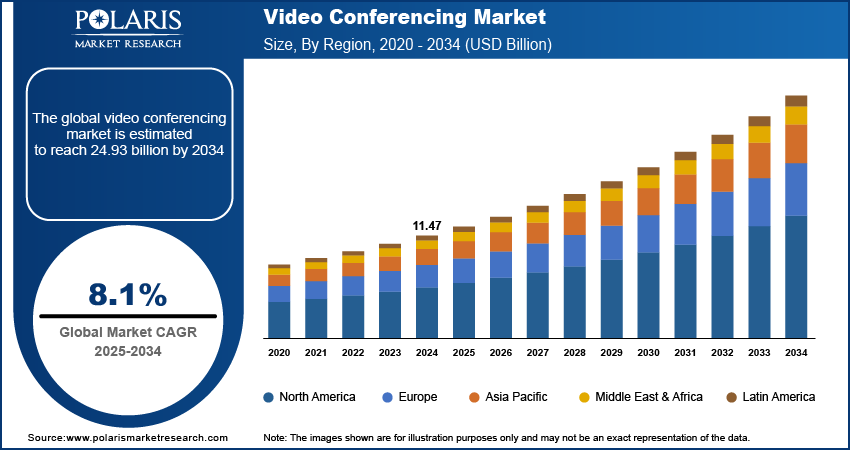

The global video conferencing market size was valued at USD 12.30 billion in 2025, growing at a CAGR of 7.35% from 2026 to 2034. Key factors driving the market demand include sur innovations in video conferencing, rising adoption in the education and telemedicine sectors.

Market Statistics

Key Takeaways

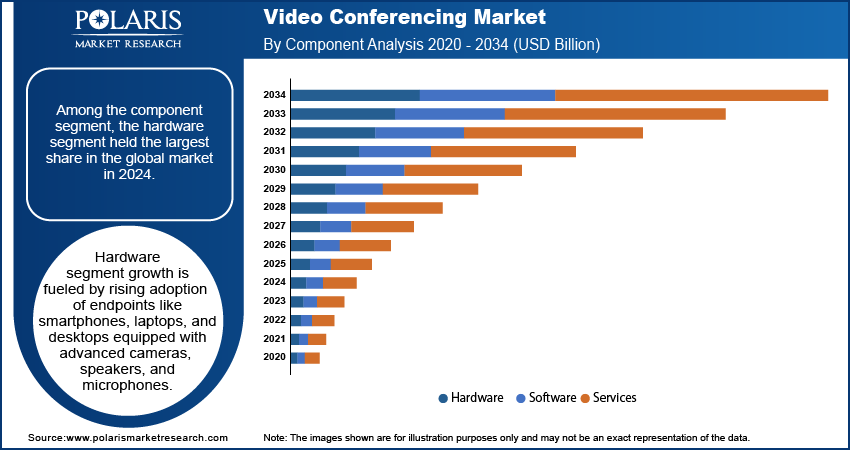

- In 2025, the hardware segment dominated the global market with 48.5% share. The growth is attributed to the rapid development and adoption of smartphones, laptops, and desktops with high-resolution cameras, speakers, and microphones.

- The corporate segment is expected to witness rapid growth of 7.9% during the forecast period. It is driven by the growing cloud-based communication software industry. Also, the rapid development of enterprise collaboration software propels the industry growth.

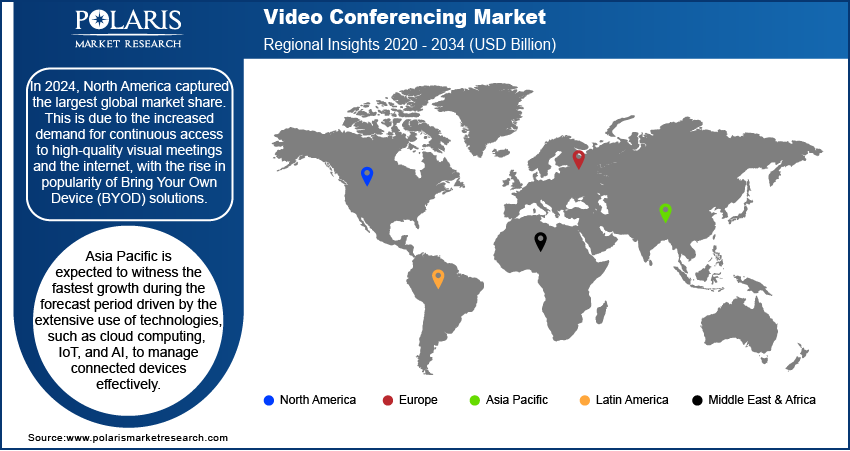

- In 2025, North America captured the largest global market share of 39.68%. This is due to the increased demand for continuous access to high-quality visual meetings and the internet, with the rise in popularity of Bring Your Own Device (BYOD) solutions.

- Asia Pacific is expected to witness the fastest growth rate at 7.1% during the forecast period. The regional market is driven by the extensive use of technologies, such as cloud computing, IoT, and AI, to manage connected devices effectively.

- The service segment is expected to grow at the fastest rate, registering a CAGR of 8.0%, driven by rising demand for cloud and managed services.

- The healthcare segment is expected to hold around 16.5% revenue share in 2025. This is due to increasing use of telemedicine and remote care solutions.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The growing hybrid work video conferencing market has led to an increased demand for video conference tools to support daily collaboration as opposed to in-person meetings.

- The rise in telehealth options for consultations and patient monitoring, offered by healthcare providers, has contributed to demand for video conferencing platforms.

- Owing to the availability of free and freemium video conferencing tools, market players experience video conferencing pricing pressure. This makes profitability and differentiation of core products difficult. Hence, increased competition from free platforms is one of the major market restraints.

- Opportunity for premium services and new revenue streams to offer distinct value beyond a basic video call is done through the integration of AI features, such as meeting summaries and automated transcription.

Impact of AI in Video Conferencing Market

- Dynamic enhancement of audio and video quality, removal of background noise, and adjusting for lighting, AI enhances the professionalism and ease for all participants.

- Intelligent collaboration platforms improve meeting effectiveness and accessibility. They provide real-time transcription, translation, and automatic summarization to capture important discussions and action items.

- AI-powered video conferencing has features like virtual backgrounds, gesture recognition, and automatic framing. AI tools perform back-end tasks, making meetings more seamless and smart.

- Vendors try to monetize these features in various ways to generate alternative revenue streams and reduce customer churn.

To Understand More About this Research: Download Sample Report Source: Polaris Market Research Analysis

What is video conferencing?

The video conferencing industry focuses on platforms and solutions that enable real-time audio-visual communication across geographically dispersed locations. These systems are deployed as core enterprise collaboration tools. They support internal meetings, telehealth consultations, customer engagement, digital classrooms, and government communications. The market has evolved from basic video calling to intelligent, cloud-based collaboration ecosystems, which are integrated with AI-driven automation, security controls, and analytics.

The growing need for operational enterprise communication, along with large-scale investments by several organizations to modernize and simplify communication networks, is driving the global adoption of video conferencing tools. The technology is often considered convenient for business users in several countries as it saves expenses, time, and aggravation regarding business travel. Furthermore, video conferencing is used to conduct routine meetings and job interviews, and assign business deals. These end uses are propelling the enterprise video conferencing market growth.

Industry Dynamics

Growth Drivers

The video conferencing market is growing rapidly worldwide. There is a rising shift in preference for virtual interviews in the recruitment process. Therefore, the use of video conferencing technology has increased to hire candidates with exceptional professional skills. Conferencing enables business organizations to gain insights regarding the aspects, including the ideal meeting length, the optimal number of participants, and more. Enterprises are increasingly standardizing video conferencing platforms as part of unified communication strategies, enabling consistent collaboration across distributed teams, geographies, and time zones.

To Understand More About this Research: Download Sample Report Source: Polaris Market Research Analysis

Video conferencing helps organizations to find and analyze better content of the meeting at a faster pace. It also assists in modernizing and simplifying the business process more effectively. Hence, video conferencing is becoming the standard practice and appeals a comparative analysis among meetings in an organization, which, in turn, strengthens the trend for video conferencing in developed and emerging markets.

This accelerating demand for cloud technology on the back of the digital age has insisted enterprises replace to deploy cloud-based solutions by replacing traditional systems of the business management process. Thus, global companies are looking forward to integrating cloud-based video conferencing solutions and services and playing a critical role in changing the dynamics of the video conferencing market during the forecast period.

Segmental Analysis

Component Analysis

Among the component segment, in 2025, the hardware segment dominated the global market with 48.5% share. The market growth of the hardware segment can be attributed to the growing development and acceptance of endpoints, including smartphones, laptops, and desktops fortified with high-resolution cameras, speakers, and microphones. In addition, the rise in adoption of the Internet of Things (IoT), enabling the robust incorporation of hardware with cloud-based software solutions and other key technologies, such as artificial intelligence and facial recognition, are the few factors that boost the market growth.

The service segment is expected to grow at the fastest rate, registering a CAGR of 8.0%. The video conferencing services market growth is driven by the escalating integration of augmented reality and other technologies. Cloud video conferencing services, such as Adobe Connect, LoopUp, and other are enhancing customer experience. Moreover, a significant increase in mobility needs of the remote workforce and workers has been witnessed. It would further complement the market growth of this segment worldwide. Enterprises seek seamless implementation and ongoing optimization of collaboration infrastructure. Thus, service-based offerings, including managed video conferencing services, cloud deployment support, and system integration, are gaining traction.

End Use Analysis

The corporate segment is expected to witness rapid growth of 7.9% during the forecast period in the global market, owing to the rapid development of the cloud-based collaboration and communication software industry, opening new opportunities for new players in the marketplace. Further, the continual growth in the frequency of geographically dispersed teams has promoted the massive utilization of cloud-based platforms to streamline business processes, enhance productivity, and manage projects of all extents, accelerating market growth.

On the flip side, the healthcare segment is expected to pave a high market share in terms of revenue by 2034. It helps healthcare providers in patient care and telemedicine, healthcare administration applications, and medical education to deliver improved patient care by offering them enhanced communication options. Thus, these factors are expected to contribute to the market growth fortune.

To Understand More About this Research: Request Customization Source: Polaris Market Research Analysis

Video Conferencing Use Cases and Business Impact

| Use Case | Where It Is Used | Business Value | Business Value |

| Business Meetings | Internal team meetings, client discussions | Faster decision-making, reduced travel cost | Hybrid work, global teams |

| Remote Work Collaboration | Daily stand-ups, project collaboration | Improves productivity and team coordination | Cloud platforms, distributed workforce |

| Online Classes | Schools, colleges, training programs | Enables remote learning and wider access | E-learning growth, digital adoption |

| Telemedicine Consultations | Doctor-patient interaction, follow-ups | Improves patient access and reduces hospital visits | Telehealth demand, healthcare digitization |

| Virtual Interviews | Hiring and recruitment processes | Saves time and speeds up hiring cycles | Remote hiring trend, global talent access

|

Source: Polaris Market Research Analysis

Regional Analysis

North America Video Conferencing Market Assessment

Geographically, North America captured the largest global market share of 39.68% due to the robust growth and early adoption of advanced technologies and software associated with video conferencing in the region. Additionally, the escalating demand for continuous access to high-quality visual meetings and the internet, coupled with the increasing popularity of Bring Your Own Device (BYOD) solution, is further expanding the market growth at a rapid pace considering the global scenario.

Additionally, countries such as the U.S and Canada are further estimated to register the largest number of initiatives, and partnership agreements will prolong unified communication (UC) solutions and video conferencing collaboration portfolio to streamline businesses of several sizes across these countries.

Asia Pacific Video Conferencing Market Insights

Asia Pacific is expected to witness the fastest growth rate at 7.1% during the forecast period owing to the extensive usage of technologies, including cloud computing, IoT, and AI to manage connected devices effectively, coupled with the huge proliferation of 4G and 5G networks that present huge opportunities for the acceptance of video conferencing. The growth of this region is further boosted by the digital transformation across the BFSI, IT & Telecom, and education sectors, which has boosted the adoption of remote communication tools. A rise in initiatives for the promotion of digital infrastructure and the startup ecosystem has also created a wide path for market expansion. Moreover, the rise in remote and hybrid work, with the need for cost-effective communication solutions, especially after the pandemic, encouraged organizations to adopt advanced video conference systems into their operations.

To Understand More About this Research: Request Customization Source: Polaris Market Research Analysis

How does the imposition of regulations on data protection and privacy impact the India video conferencing market?

The increasing adoption of e-learning, hybrid work, and telehealth propels the demand for video conferencing in India. Also, government initiatives and the rising penetration of 5G networks boost the adoption of video conferencing platforms in the country. However, the rising use of these platforms leads to the requirements for data privacy, enterprise security compliance, and regulatory compliance. The following table comprises comprehensive information on key regulatory and compliance areas in India.

| Area | Description | Relevance to Video Conferencing |

| Data Protection | India’s DPDP Act 2023 | Ensures personal and corporate data is securely stored and processed |

| Telemedicine Practice Guidelines (MoHFW, India) | Regulations for remote patient consultation and medication | Requires secure end-to-end encrypted platforms for doctor-patient communication Emphasis on ensuring the privacy of patients in video consultation |

| Corporate Security Standards | ISO 27001, SOC 2, NIST frameworks | ISO 27001 imposes the use of an Information Security Management System (ISMS). Ensures enterprise-grade security for internal meetings, board meetings, and sensitive information |

| Sector-specific Compliance | Financial (PCI DSS), Healthcare (HIPAA) | Platforms used in the banking and healthcare sectors must have specialized security certifications. They focus on data protection from fraud and theft. |

Source: Polaris Market Research Analysis

The imposition of such regulations and rules clarifies that companies providing video conferencing products must maintain a balance between innovation and regulatory adherence. Many major global market players, including Cisco Webex, Microsoft Teams, and Zoom, focus on obtaining various certifications to expand their business in India. On the flip side, Indian vendors such as Airmeet, JioMeet, and Zoho Vani, are taking actions to comply with domestic and international regulations. These factors boost the adoption of video conferencing in the country.

Key Players & Competitive Analysis Report

Video conferencing landscape is characterized by intense competition among established players and agile market entrants. Competitive intelligence and strategic assessments identify leading vendor strategies concentrated on innovation, primarily in the area of AI, to improve user experience and automate meetings. A large opportunity for revenue exists in small and medium businesses that are a new segment of the market with specific technology requirements for scalable, cost-efficient solutions. Planned product development is now largely shaped by socioeconomic and geopolitical factors, and supply chain disruption challenges that vendors must consider when regrouping their regional footprint. Performance will depend on vendor's use of expert's foresight of industry change, including hybrid work, that builds sustainable value ecosystems and provides strong competitive positioning with superior products.

Some of the Major Players operating the global market include:

- Amazon Web Services, Inc.,

- AURA Presence,

- Avaya Inc.,

- Barco NV,

- BlueJeans Network, Inc,

- Cisco Systems, Inc.,

- Fuze, Inc.,

- Google, Haivision, Inc.,

- HighFive, Inc.,

- Huawei Technologies Co. Ltd.,

- Kaltura, Inc.,

- Kollective Technology, Inc.,

- Lifesize, Inc.,

- Logitech International S.A.,

- LogMeIn, Inc.,

- Microsoft Corporation,

- Pexip, AS,

- Plantronics, Inc.,

- Qumu Corporation,

- Sonic Foundry, Inc.,

- StarLeaf Inc.,

- Vidyo, Inc.,

- Zoom Video Communications, Inc.

How Enterprises Evaluate Video Conferencing Platforms?

Enterprises evaluate video conferencing platforms through a structured mix of technical, commercial, and strategic criteria aligned with long-term digital collaboration goals. In the enterprise video conferencing market, security and compliance are top priorities. It fuels the demand for secure video conferencing solutions with end-to-end encryption, identity management, and role-based access controls. The solutions must have certifications such as ISO 27001, SOC 2, HIPAA, or GDPR readiness. Scalability and reliability are assessed based on concurrent user capacity, global latency, uptime SLAs, and performance consistency across geographies. Enterprises also evaluate the depth of integration with existing IT ecosystems, including unified communications, calendar tools, CRM, and workflow platforms. A total cost of ownership (TCO) analysis compares licensing models, infrastructure requirements, and long-term operational costs. Finally, vendor roadmap, AI-enabled features, and enterprise-grade support influence platform selection.

Pricing Structure and Total Cost of Ownership (TCO)

The video conferencing market uses subscription-based SaaS pricing models. Companies offering video conferencing tools usually charge based on the number of users or hosts. They offer monthly or annual plans. Vendors provide tiered pricing that ranges from free plans with limited features to enterprise packages that include enhanced security, compliance, analytics, and integrations. Large organizations often negotiate custom contracts. Additional costs for enterprise collaboration can come from webinars, cloud storage, telephony, or AI features.

Total cost of ownership (TCO) goes beyond license fees. It also includes costs for implementation, hardware for conference rooms, network bandwidth upgrades, training, and ongoing IT management. Moving to the cloud shifts expenses to operating costs through subscriptions. It helps avoid large capital expenses for hardware. However, on-premise or private cloud video conferencing solutions require higher initial spending but offer more control over data and compliance. As hybrid work becomes standard, companies are increasingly seeking solutions based on multi-year TCO, scalability, and operational efficiency instead of just the upfront pricing.

Video Conferencing Pricing Models: Cloud-Based Vs. On-Premise

| TCO Parameter | Cloud-Based Video Conferencing | On-Premise Video Conferencing |

| Upfront Cost | Low to moderate. Subscription-based. Minimal initial investments. | High. Requires server infrastructure, licenses, networking, and room systems |

| Licensing Model | Recurring OPEX (per-user/per-host SaaS subscriptions) | One-time perpetual licenses plus annual maintenance |

| Deployment Time | Rapid deployment and scalability | Longer deployment and configuration cycles |

| Hardware Requirement | Limited to endpoints and meeting rooms | Extensive on-site servers, storage, and networking hardware |

| Maintenance & Upgrades | Included in subscription; vendor-managed | Internal IT staff, energy costs, additional IT and upgrade costs |

| Security & Compliance | Shared responsibility; vendor certifications | Full internal control, preferred for regulated sectors |

| Long-Term TCO | Higher over time due to recurring fees | Lower for large, stable user bases |

| Scalability Costs | Pay-per-use, elastic for variable meetings | Fixed infrastructure, costly to expand |

| Hidden Expenses | Data transfer fees, potential vendor lock-in | Downtime, cooling, compliance hardware |

Source: Polaris Market Research Analysis

Pricing competition in the video conferencing industry is moving from basic meeting licenses to value-based differences. This trend is influenced by different features like AI integration, security, interoperability, and ecosystem integration. Hybrid work is becoming a permanent part of many organizations. As a result, companies assess platforms based on long-term total cost of ownership, scalability, and operational efficiency, not just upfront pricing.

Industry Developments

- January 2026: AONMeetings, based in Des Moines, started operations in India to offer secure communication tools to small businesses, families, healthcare providers, schools, and legal experts at affordable prices. Founded in 2020, it has a 4.9-star rating on G2 and supports over 1,000 businesses in the U.S. market. (Source: business-standard.com)

- July 2025: Owl Labs began operations in India, launching the Meeting Owl 3, now BIS certified. This device improves hybrid meetings with its 360° camera, microphone, and speaker, providing a better experience for both remote and in-person users. (Source: businesswire.com)

- June 2025: HP Inc. collaborated with Google Beam, an AI-powered, true-to-life 3D video communications solution. The solution is designed to transform the future of workplace communications by combining 3D imaging, natural eye contact, spatial audio, and adaptive lighting into an elegant solution for small meeting spaces. (Source: hp.com)

- March 2024: Zoom Workplace unveiled an AI-powered collaboration platform to reimagine teamwork. According to Zoom, this technology ensures a seamless AI deployed workforce in an economical way. Also, it provides a seamless way for colleagues and customers to connect and achieve their daily objectives more productively. (Source: zoom.com)

- March 2024: Microsoft and Oracle expanded their partnership to satisfy global demand for Oracle Database@Azure worldwide. For Microsoft, this merger with Oracle will make the migration of workloads streamlined and also empower business innovation. (Source: microsoft.com)

Future of Video Conferencing Market

The market will grow due to rising demand for digital communication and remote collaboration. Meetings with features like auto summaries and smart scheduling will become common. Real-time translation will improve communication in regions. Immersive tools like AR and VR meetings will expand use cases. Hybrid work will continue to drive adoption in organizations. Overall, the market is expected to observe steady growth in the coming years

Video Conferencing Market Segmentation

By Component Outlook (Revenue, USD Billion, 2021–2034)

- Hardware

- Software

- Service

By Deployment Type Outlook (Revenue, USD Billion, 2021–2034)

- On-Premise

- Cloud

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Consumer

- Enterprise

By End Use Outlook (Revenue, USD Billion, 2021–2034)

- Corporate

- Education

- Healthcare

- Government & Defense

- BFSI

- Media & Entertainment

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- France

- Germany

- UK

- Italy

- Spain

- Netherlands

- Austria

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Malaysia

- South Korea

- Indonesia

- Rest of Asia Pacific

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- UAE

- Saudi Arabia

- Israel

- South Africa

- Rest of Middle East & Africa

Video Conferencing Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 12.30 Billion |

| Market Size in 2026 | USD13.19 Billion |

| Revenue Forecast by 2034 | USD 23.28 Billion |

| CAGR | 7.35% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The global video conferencing market was valued at USD 12.30 billion in 2025, driven by rising preference for remote work.

A few of the key growth drivers are the growing adoption of remote work, increasing demand for cloud-based collaboration, and reducing expenditure on travel. Also, the rising integration of AI and other technologies into video conferencing platforms would boost the industry growth in the coming years.

In 2025, North America captured the largest global market share of 39.68%.

The market is projected to register a CAGR of 7.35% during 2026–2034. It is expected to reach USD 23.28 billion by 2034, fueled by digital transformation trends.

IT & Telecom, Healthcare, Education, and BFSI sectors lead adoption due to heavy investments in digital communication tools and rising requirements for remote collaboration.

In 2025, the hardware segment dominated the global market with 48.5% share. Hardware segment growth is driven by the growing development and adoption of endpoints, including smartphones, laptops, and desktops, equipped with high-resolution cameras, speakers, and microphones.

It saves time and travel cost. It improves communication and collaboration. It supports remote work, online learning, and healthcare services.

Common platforms include Zoom, Microsoft Teams, Google Meet, and Cisco Webex. These are used for meetings, classes, and business communication.

Download Sample Report of Video Conferencing Market

Please fill out the form to request a customized copy of the research report.