Fuel Cell Market Growth Statistics and Revenue Projections, 2026-2034

REPORT DETAILS

What is Fuel Cell Market Size?

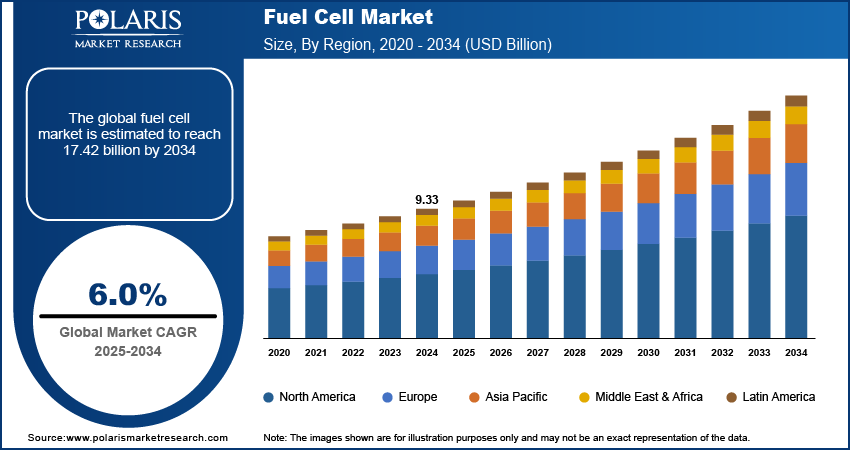

The global fuel cell market size was valued at USD 10.76 billion in 2025 and is anticipated to register a CAGR of 14.8% from 2026 to 2034. The key drivers include increasing demand for clean energy and low-carbon emissions. Government support accelerates fuel cell market growth by providing strong policies and investments. Improvements in technology also enhance the hydrogen fuel cell market, expanding clean energy power generation.

Market Statistics

Key Takeaways

- Asia Pacific dominated the PEM fuel cell market with 32.0% revenue share in 2025, accounting for a revenue of USD X due to rapid adoption and government support.

- Europe is projected to grow at a CAGR of 14.2% during 2026–2034, driven by strong hydrogen investments and emission regulations.

- The balance of plant segment is expected to grow at a CAGR of 13.7% during 2026–2034, supported by advancements in system efficiency components.

- Based on type, the PEM fuel cell market had the largest share of 59.1% in 2025. It has a fast startup time and a high power density, which are quite beneficial in the transportation sector, particularly fuel cell electric vehicles.

- In terms of application, the stationary segment accounted for the largest share of 67.4% in 2025. It is a vital source of clean and reliable power for essential infrastructure such as data centers and hospitals, as well as for combined heat and power systems.

Industry Dynamics

- The imposition of rigorous environmental norms and the challenge to reduce carbon emissions are key fuel cell market drivers. Fuel cells help users achieve net-zero emissions by providing zero-emission power solutions that produce clean electricity tailored for use at the required location.

- Hydrogen economy initiatives, tax credits, and direct hydrogen infrastructure investment significantly reduce entry barriers for fuel cell adoption. These fuel cell government incentives support growth across both transportation and stationary power sectors.

- Advances in technology are also enhancing the efficiency, durability, and economics of fuel cells. Technological advancements are also enabling fuel cells for new applications, such as heavy-duty transport vehicles and power plants. Technological advancements are also helping improve their commercial viability.

- High cost of fuel cells and lack of hydrogen infrastructure slows down market growth.

Source: Polaris Market Research Analysis

AI Impact on Fuel Cell Market

- The fuel cell industry is being revolutionized by Artificial Intelligence (AI) across design, production, optimization, and energy management.

- Engineers use AI to analyze a wide range of fuel cell designs, optimizing electrode designs and fluid dynamics.

- The technology combines electrochemical, thermal, and structural analysis models to provide high-fidelity insights during prototyping.

- AI tools redistribute power across fuel cell stacks to maintain safety and performance.

- AI enhances thermal management, hydrogen storage, and autonomous driving features in fuel cell vehicles (FCVs).

What are Fuel Cells?

Fuel cells generate electricity using hydrogen as fuel. They convert chemical energy into electrical energy through a reaction between hydrogen and oxygen. This process produces electricity, heat, and water as a byproduct. Fuel cells have benefits like zero emissions, higher efficiency, and can be used in transport and power generation applications.

The clean energy market is based on the use and production of fuel-conversion devices, such as converting hydrogen to electricity. This market is significant in the shift from fossil fuels. It is used in the energy and transportation sectors as well as in portable technology.

The growing need for efficient power backup solutions is driving demand for fuel cells in this industry. Backup systems require a large number of fuel cells because they will be used continuously, without frequent refueling or long recharge times. Therefore, they could be very effective in critical applications for data centres or telecommunications. Another factor is that interest in off-grid power solutions is growing rapidly in remote areas and developing countries. This fuel cell provides clean, reliable power in areas without an electrical grid.

One factor driving the fuel cell market is the emphasis on sustainable energy consumption. Fuel cells are at the forefront of this new chapter in the history of energy production, producing electricity with minimal emissions, thereby helping the world meet its ambition to contain climate change, not to mention improving air quality. For instance, they are in actual use in medical equipment and healthcare facilities; therefore, they can provide a clean source of electricity in areas that need it most.

Drivers and Trends

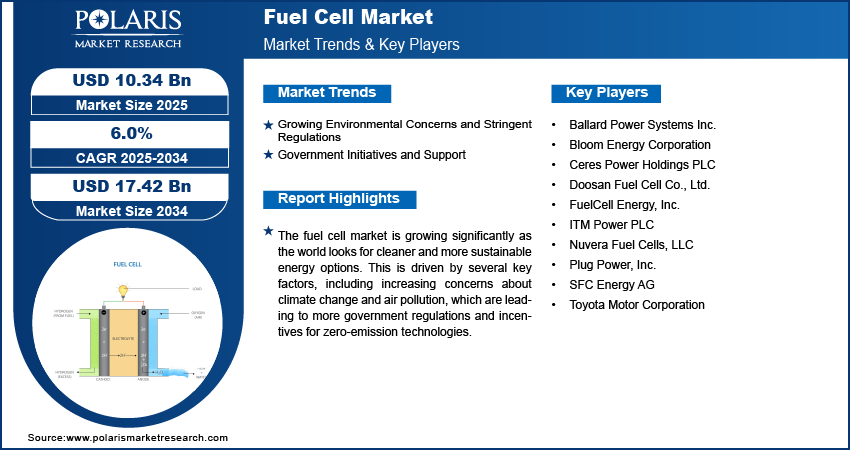

Growing Environmental Concerns and Stringent Regulations

The increasing need to reduce carbon emissions and the transition to clean energy sources are driving adoption. Fuel cells use hydrogen to produce electricity and release only water, highlighting their strong fuel cell environmental benefits. Fuel cells can be applied in both transportation and power technologies. Fuel cells are increasingly being used in the development of clean transport and renewable energy sources. They benefit from fuel cells being more durable and offering a longer driving range than batteries. Climate change mitigation requirements are pushing the government to develop the hydrogen economy initiatives.

The International Energy Agency reports that more than 85% of global car sales are affected by fuel economy and CO2 regulations. The EU's CO2 regulations have had a major influence on the surge in electric vehicle sales. In the USA, CO2 regulations, as observed by the Department of Energy, show that if a car is made 10% lighter, its fuel economy could increase by 6% to 8%.

Government Initiatives and Support

Government support through policies is also contributing to the growth. Many nations are developing strategies to advance the hydrogen economy. This involves developing the infrastructure required for the generation, storage, and transport of hydrogen. This government support includes investment in R&D in the fuel cell industry. This aims at overcoming the initial cost barriers associated with fuel cell power.

India’s National Green Hydrogen Mission, with a significant budget, enables pilot applications of green hydrogen as a transport fuel in buses and trucks powered by fuel cells. In the US, the Inflation Reduction Act provides tax incentives to increase investment in hydrogen production and distribution. Such government interventions are essential to forging a healthy future for this technology's development.

Market Challenges

Limitations of Cost, Storage, and Technology: Cost and infrastructure issues plagued the fuel cell market. Hydrogen storage challenges make transport and refueling complex and expensive. There is an ongoing fuel cell vs battery comparison, as batteries often have superior charging networks. Fuel cells still rely on expensive materials with limited supply chains. This slows adoption despite the ongoing growth in interest in clean energy.

Performance and Adoption Comparison: Fuel Cells vs Batteries

| Metric | Fuel Cell | Battery | Notes |

| Energy Density | High (more energy per kg) | Lower | Fuel cells store more energy in less weight, which is useful for long-range vehicles. |

| Refueling/Recharging Time | Fast (3–10 minutes) | Slow (30 min to several hours) | Fuel cells offer faster refueling than battery charging. |

| Operating Range | Long | Short to medium | Vehicles with fuel cells can travel longer distances per refuel. |

| Infrastructure Availability | Limited hydrogen stations | Widespread charging stations | Battery systems are easier to adopt in most regions today. |

| Maintenance | Moderate, fewer moving parts | Low to moderate | Both require maintenance, but fuel cells can be sensitive to fuel quality. |

| Environmental Impact | Zero emissions at use | Zero emissions at use, but production emissions vary | Both are clean during operation; battery production can have higher upstream emissions. |

| Cost | High initial cost, fuel cost variable | Lower cost, electricity cost is stable | Fuel cells still cost more upfront, but may be better for heavy-duty or long-range use. |

| Weight & Space Efficiency | Lighter for the same energy | Heavier for the same energy | Batteries add significant weight for long-range applications. |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Segmental Insights

Type Analysis

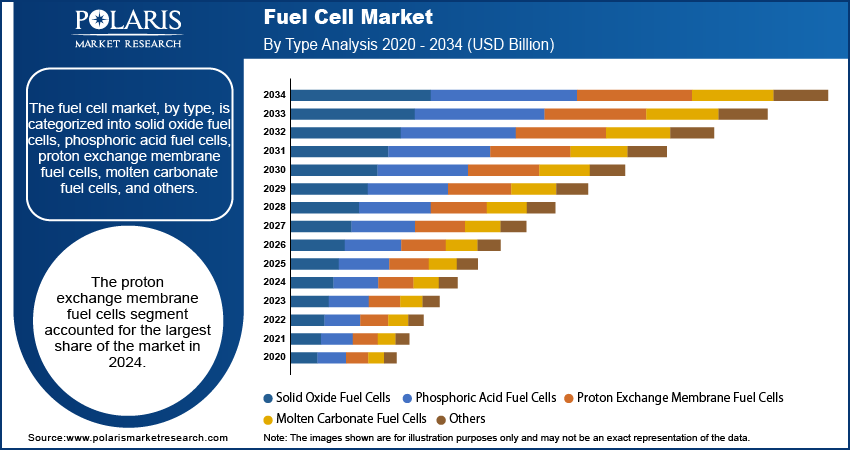

Based on type, the segmentation includes solid oxide fuel cells, phosphoric acid fuel cells, proton exchange membrane fuel cells, molten carbonate fuel cells, and others. The PEM fuel cell market had the largest share of 59.1% in 2025. PEM fuel cells are commercially preferred because they can work at relatively low temperatures, start up quickly, and react fast. Relatively compact and high-power-density, these are vital for fuel cell transportation applications such as cars, buses, and heavy-duty trucks. The increasing demand for zero-emission vehicles and the significant investments by car manufacturers in hydrogen mobility have lately favored their adoption. Having already proven their technology, with improved performance and ongoing cost reductions, PEM fuel cells remain the leading choice for mass-market mobility solutions.

The solid oxide fuel cells market is projected to experience the sharpest growth rate during the forecast period. SOFCs are more efficient than other technologies in stationary fuel cell systems and in combined heat and power generation for industrial purposes. In addition, SOFCs can be powered by a wide range of fuels, including synthetic natural gas, biogas, and hydrogen. Due to their high operating temperature, these cells can better utilize heat, thereby increasing their efficiency. These characteristics make SOFCs highly suitable for distributed power generation and other uses.

Application Analysis

Based on the application, the segmentation includes stationary, transportation, and portable. The stationary segment had the highest revenue share of 67.4% in the market in 2024. Such systems serve as backup power sources for critical applications such as data centers, hospitals, and telecommunications systems. Moreover, these systems act as the primary power source in combined heat and power plants. These plants boast efficiency and can be applied in both commercial and industrial settings. Additionally, these systems are noiseless and environmentally clean, making them the best substitutes for diesel generators in major cities with tight environmental regulations.

The transportation sector is also projected to witness the highest growth rate in the future years. This is due to the rise in the adoption of hydrogen-emission-free vehicles and the government's increased support for the development of hydrogen infrastructure. The demand for fuel cells is also rising in transportation applications such as buses, trucks, trains, and even ships, due to their quick refueling and longer driving distances, which battery-driven vehicles cannot match. As a result, the use of fuel cells in transportation is also rising, driven by the growing number of fueling stations and lower hydrogen costs.

Fuel Cell Applications and Real-World Examples

| Application Area | Fuel Cell Use | Real-world Examples |

| Transportation | Used for zero-emission mobility with fast refueling and long range | Hydrogen buses, fuel cell trucks, fuel cell cars |

| Stationary Power | Provides continuous and reliable power supply | Backup power for hospitals, telecom towers, industrial power systems |

| Data Centers | Used for clean and uninterrupted power supply | Fuel cell backup systems for data centers and critical IT infrastructure |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Regional Analysis

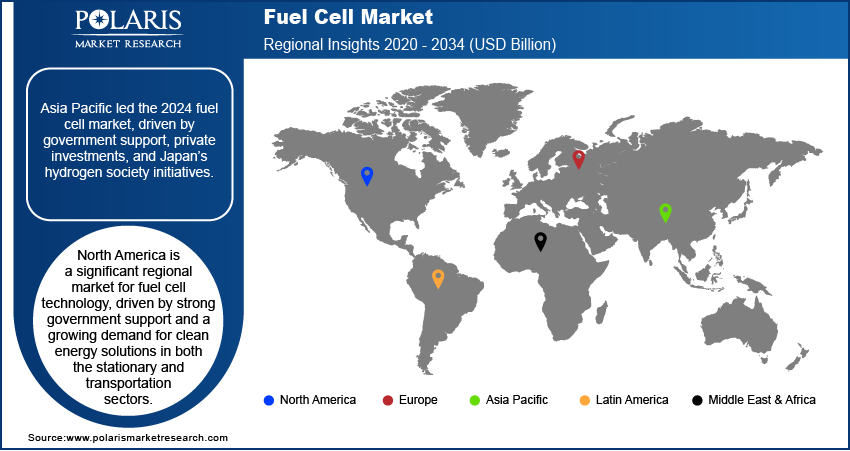

The Asia Pacific fuel cell market was the largest with a revenue share of 35.0% in 2025. The aggressive hydrogen strategy, presence of key OEMs, and earlier commercialization of fuel cell vehicles are the key drivers. The government support and investments are contributing to the innovation and adoption process. The region emphasizes energy security and mitigating air pollution, hence increasing the hydrogen infrastructure development. Key players are investing in both stationary and transportation markets; as a result, fuel cell vehicles are becoming more widely available to the public. This enhances the presence of the hydrogen fuel cell market in the region as well.

Japan Fuel Cell Market Overview

Japan is one of the major players in the development of fuel cell technology. The Japan fuel cell industry is characterized by Japanese leadership in converting vehicles to fuel cell vehicles and in establishing hydrogen refueling station infrastructure. Japan’s Hydrogen Society is at the forefront globally in the use of hydrogen in dwellings, transportation, and industrial applications. Japanese government support for residential fuel cells and for the broader use of fuel cells has made Japan one of the major bases for the development of fuel cell systems.

North America Fuel Cell Market Trends

The market in North America is expected to witness growth with a CAGR of 13.6%, driven by strong government support and a growing demand for clean energy solutions in both the stationary and transportation sectors. The region has seen considerable investment in hydrogen infrastructure and research and development, particularly in the U.S. and Canada. The firms are also aggressively seeking collaborations to develop fuel cell systems for commercial and industrial use. The collaborative development and government support are thus aiding the rapid development of this technology.

U.S. Fuel Cell Market Insights

The U.S. is leading among North America countries in its focus on developing and using fuel cell technology. Public support and spending are essential for the growth of hydrogen and fuel cell technology. Fuel cells have also garnered interest in the transportation industry, especially in the truck and bus sector, as states aim to achieve zero-emission transportation.

Their successful sectors and efforts to lower carbon emissions have ensured that fuel cells are promoted through various means.

Europe Fuel Cell Market Outlook

The European market is expanding rapidly due to its firm commitment to reducing carbon emissions and its well-developed hydrogen strategy. The European Union, along with government support, enables the entire hydrogen value chain, from production to fueling infrastructure. Fuel cells are used in transport such as buses, trucks, and trains.

Germany is a significant player in Europe’s fuel cell industry, with ambitious plans and considerable government support for hydrogen and fuel cells. Germany has focused significantly on building a network of hydrogen refueling stations and on projects for long-range heavy-duty fuel cells. Germany’s industrial infrastructure, along with its efforts in renewable energy, makes it a leading adopter of fuel cells in generation and transportation.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

The market's competitive landscape has been influenced by both mature and new companies. Key players in this market include Plug Power, Inc.; Ballard Power Systems, Inc.; FuelCell Energy, Inc.; Bloom Energy; and Doosan Fuel Cell Co., Ltd. These companies have been developing new technologies to remain ahead of the competition. These are designed to improve efficiency, extend lifetime, and minimize costs. These include collaboration for a comprehensive hydrogen infrastructure solution and a comprehensive solution set. The market leaders are focusing more on stationary power, hydrogen transportation, and heavy-duty transportation solutions. Innovation is driving the market with a focus on developing more powerful and affordable fuel cell solutions. This emphasizes the importance of fuel cell market players in influencing the fuel cell competitive landscape.

A few prominent companies include Plug Power, Inc.; Ballard Power Systems, Inc.; FuelCell Energy, Inc.; Doosan Fuel Cell, Co., Ltd.; Bloom Energy; Ceres Power Holdings PLC; ITM Power PLC; SFC Energy AG; Nuvera Fuel Cells, LLC; and Toyota Motor Corporation.

Key Players

- Ballard Power Systems Inc.

- Bloom Energy Corporation

- Ceres Power Holdings PLC

- Doosan Fuel Cell Co., Ltd.

- FuelCell Energy, Inc.

- ITM Power PLC

- Nuvera Fuel Cells, LLC

- Plug Power, Inc.

- SFC Energy AG

- Toyota Motor Corporation

Fuel Cell Industry Developments

- January 2026: General Motors Co. and Honda Motor Co. Ltd. decided to end their fuel cell joint venture in Michigan by year-end. GM is shifting its investment focus toward battery-electric vehicle platforms. Source: (Source: https://global.honda)

- In November 2025: Doosan Fuel Cell signed a USD 96.4 billion, 20-year agreement with KEPCO to supply hydrogen-based power. The deal supports South Korea’s hydrogen economy, with Doosan delivering and maintaining fuel cell power systems, ensuring stable long-term revenues and advancing sustainable energy growth. (Source: doosan.com)

- In November 2025: S-Fuelcell unveiled the GFOS platform, a modular fuel cell solution designed for AI data centers. The system initially runs on natural gas while remaining hydrogen-ready for future conversion, helping address grid capacity constraints and providing reliable, scalable power. (Source: inuverse.co.kr)

- September 2025: Ballard introduced the FCmove-SC fuel cell at Busworld 2025. Ballard stated that the fuel cell is designed for city transit buses. It offers improved performance and can be easily integrated into vehicles. (Source: ballard.com)

- July 2025: Plug Power announced a new multi-year strategic supply agreement with a major industrial gas company. This deal extends their current partnership through 2030. (Source: plugpower.com)

- March 2025: Doosan Fuel Cell, with KHNP, Airrane, and KECC, developed Korea’s first carbon capture technology for hydrogen fuel cells, redesigning systems and deploying membrane capture at Yeosu Gwangyang Port, with pilots completed by January 2025. (Source: doosanfuelcell.com)

- February 2025: Bloom Energy expanded its Frankfurt modular fuel cell facility to accelerate production of prefabricated medium- and high-voltage electrical houses for rapid deployment in industrial, utility, and renewable energy projects worldwide. (Source: bloomenergy.com)

Fuel Cell Market Segmentation

By Type Outlook (Revenue – USD Billion; Volume, Units; 2021–2034)

- Solid Oxide Fuel Cells

- Phosphoric Acid Fuel Cells

- Proton Exchange Membrane Fuel Cells

- Molten Carbonate Fuel Cells

- Others

By Application Outlook (Revenue – USD Billion; Volume, Units; 2021–2034)

- Stationary

- Transportation

- Portable

By Size (Revenue – USD Billion; Volume, Units; 2021–2034)

- Small-scale (Up to 200 kW)

- Large-scale (Above 200 kW)

By Fuel (Revenue – USD Billion; Volume, Units; 2021–2034)

- Hydrogen

- Methanol

- Ammonia

- Others

By Component (Revenue – USD Billion; Volume, Units; 2021–2034)

- Stack

- Balance of Plant

By End User (Revenue – USD Billion; Volume, Units; 2021–2034)

- Residential

- Commercial & Industrial

- Transportation

- Data Centers

- Military & Defense

- Utilities & Government/Municipal Institutes

By Regional Outlook (Revenue – USD Billion; Volume, Units; 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indnesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Probiotics Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 10.76 Billion |

| Market Size in 2026 | USD 12.34 Billion |

| Revenue Forecast by 2034 | USD 37.22 Billion |

| CAGR | 14.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Fuel Cell Market FAQ's

The global fuel cell market was valued at USD 10.76 billion in 2025. The market is projected to grow from 2026 to 2034 with a CAGR of 14.8% and reach USD 37.22 billion by 2034. The major factors fueling this market are an increasing focus on clean energy, low-carbon technologies, government subsidies, and improvements in hydrogen fuel cell and clean energy technologies.

PEM fuel cells held the largest market share in 2024. These operate at low temperatures, hence allowing their quick start-up, which is ideal for commercial use. Their technology is more advanced, and their costs are falling; hence, they are well-suited for use in fuel cell cars, buses, and trucks.

The stationary segment held the dominant market share in 2024. These fuel cells deliver clean, constant power to mission-critical facilities, including data centers, hospitals, and office spaces. They are in high demand because they operate silently and produce no emissions.

The market is dominated by Asia Pacific in 2024. This is due to the aggressive plans pursued by Asia Pacific governments, coupled with OEM involvement and the earlier commercialization of FCEVs. The Asia Pacific region is currently at the center of the hydrogen fuel cell market.

The fuel cell market is driven by clean energy demand, stringent emissions regulations, and net-zero goals. Government incentives and further investment in hydrogen infrastructure also accelerate the adoption across the transport and stationary power sectors.

A clean energy conversion device that uses hydrogen to produce electricity, releasing only water as a byproduct, used across energy, transportation, and portable technology sectors to replace fossil fuels.

Stringent environmental regulations and net-zero emission goals accelerating adoption, and growing government hydrogen economy initiatives including tax credits and infrastructure investments significantly reducing entry barriers across transportation and stationary power sectors.

Download Sample Report of Fuel Cell Market

Please fill out the form to request a customized copy of the research report.