1,3 Butadiene (BD) Market Share, Size, Trends, Industry Analysis Report, 2022 - 2030

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

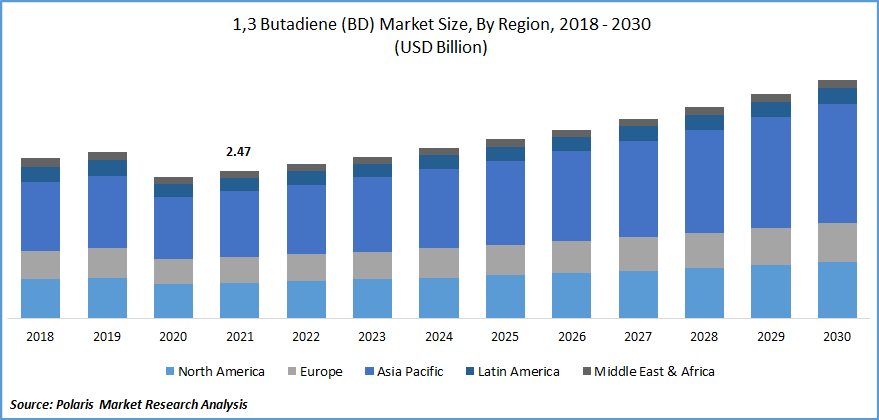

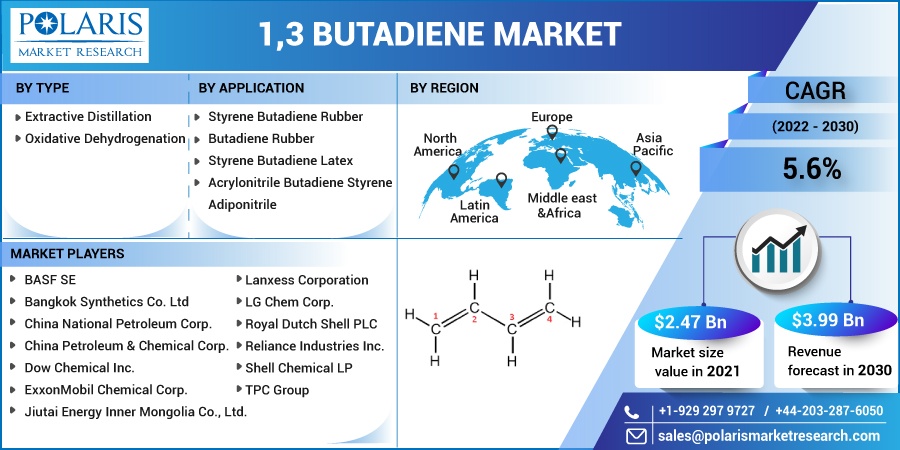

The global 1,3 Butadiene (BD) market was valued at USD 2.47 billion in 2021 and is expected to grow at a CAGR of 5.6% during the forecast period. The major factor which is boosting the market growth is the worldwide automotive industry's projected expansion in the coming years. As per the IBEF, the total amount of passenger vehicles, three-wheelers, and two-wheelers, including quadricycles, produced in April 2022, was 1,874,461.

Know more about this report: Download Sample Report

The rising production of vehicles has led to an increase in the demand for the 1,3 Butadiene (BD) market as it is used in the production of tires. It is mainly employed as an intermediate in the production and a monomer in the production of rubber and plastic, which are utilized in a wide range of commercial and consumer goods, including automobiles, building materials, electronics, protective apparel, containers, and appliance parts.

Butadiene, often referred to as 1,3-butadiene can exist as a gas or a chilled liquid and has a wide range of industrial applications. The 1,3-BD is a by-product of the thermal cracking process used to produce ethylene and olefins. It is classified as a colorless gas that burns easily, reacts strongly, especially with oxygen, and has a light aromatic smell.

In contrast to water, this substance is extremely soluble in alcohol, ether, ethanol, methanol, and benzene. Because it is combustible, 1,3 BD must be handled very carefully and precisely. The main source of 1,3-BD comes from the mixture c4 stream generated in steam crackers; the production and content of the c4 stream depend on the difficulty of the procedure and the feedstocks.

Furthermore, market safety and regulatory issues are anticipated to arise from exposure-related health problems. Regulating agencies have created tight criteria to maintain safety standards in sectors due to health concerns. The market has changed its focus to creating bio-based 1,3 BD substitutes to address these issues.

One of the compounds listed as carcinogenic by the Environmental Protection Agency (EPA) is 1,3-BD. The material can irritate the eyes, throat, lungs, and nasal passages, among other things, and increase the risk of leukemia and even cardiovascular disorders. This is anticipated to somewhat reduce the usage of 1,3 BD shortly. However, 1,3 BD's carcinogenic properties and other acute and chronic damages brought on by its fumes could constrain the market.

COVID-19 harmed the market. The construction of new buildings and car manufacturing facilities were temporarily put on hold due to the ongoing pandemic scenario. As a result, the demand for 1,3-BD declined, which adversely affected the production of styrene-butadiene and polybutadiene polymers, which are principally used in tires, construction crack fillers, and concrete additives, respectively. The 1,3 butadiene market has grown as a result of the current scenario, which has seen an increase in the use of rubber gloves made of nitrile latex.

Know more about this report: Download Sample Report

Industry Dynamics

Growth Drivers

The market demand for 1,3-BD also rises as a result of the desire to conserve resources and cut fuel costs, creating lucrative prospects for market participants. Demand for BD in resin is anticipated to rise as consumer product production preferences increase. The major players are adopting strategies to launch consumer products based on the BD, boosting the market growth over the forecast period.

For instance, in April 2022, Dynasol Group constructed a new solution styrene-butadiene rubber (SSBR) manufacturing line. The project adds 20 kilotonnes per year (ktpa) with the ability to increase to 25 ktpa of SSBR at the plant. A 10ktpa network capacity for the JV's present styrene butadiene-copolymer (SBC) facility in Altamira, Mexico, is also part of the planned expansion. Both in North America and Europe, Dynasol reported that demand for their SSBRs and SBCs are rising in industries like EVs, semiconductors, consumer products, asphalt alteration, and compounding.

Further, the increasing expansion capacity by the major players is also boosting the market growth over the forecast period. For instance, in May 2019, Jiutai Energy officially completed on-specification polymers manufacturing at its newest methanol-to-olefins (MTO) unit. Currently working at 60–70% capacity and will reach full capacity in a month. To make 280,000 t/yr of polyolefin and 320,000 t/yr of polypropylene, the MTO unit can manufacture 280,000 t/yr of ethanol and 320,000 t/yr of polypropylene.

Report Segmentation

The market is primarily segmented based on type, application, and region.

| By Type | By Application | By Region |

|

|

|

Know more about this report: Download Sample Report

The Styrene Butadiene Rubber (SBR) Segment is Expected to Witness the Fastest Growth

Synthetic rubber is created from 1,3-BD, and SBR is the main component mixed with rubber from natural sources to create tires. These rubber polymers' physical and chemical characteristics give tires performance-improving elements, including rolling resistance, wear, and traction. Natural rubber is typically replaced directly by SBR rubber in industrial settings. Excellent abrasion resistance, crack endurance, and aging properties are only a few of its benefits.

Additionally, styrene-butadiene has strong water and compression set resistance. SBR, a synthetic copolymer, was first created to take the role of natural rubber in tires. Styrene and BD are used to make SBR. It now makes up 90% of the rubber consumed worldwide, together with natural rubber. SBR is frequently employed in situations involving water, hydraulic fluids, or alcohol. This means, for instance, that SBR can be found in tires, tubes, compressors, and conveyor belt covers.

SB Latex Accounted for the Highest Market Share in 2021

A typical kind of emulsified polymer utilized in various commercial and industrial uses is styrene-butadiene (SB) latex. SB latex is regarded as a polymerization because it is created by two different kinds of monomers, styrene, and butadiene. 1,3-BD is a consequence of the manufacture of ethylene, while styrene is created when benzene and ethylene combine.

Paper coverings and goods with transparency, gloss, and luminosity, such as coated canvas and white chipboard, and data capture paper like pneumatically paper and infrared paper used in brochures, periodicals, and promotional flyers, are made with styrene-butadiene latex (SB latex). Also, in the back coats of tufted carpets, SB latex is employed. For adhesives, SB latex is a well-liked option in some industries, such as flooring.

For instance, the polymer can be found as the backing for tufted carpets. The tufts are held in place by the rear coating, which also resists water, improving stability and minimizing edge fraying. The backing coatings attach the pile fibers, keep the spikes in position, and promote security and resistance to shearing or feather loss along the carpet's cut edges.

The Demand in North America is Expected to Witness Significant Growth

Due to its dominant automotive sector and the presence of major producers' manufacturing facilities there, North America will hold a market share in the global market. The US has made significant investments in R&D and increased manufacturing capacity as a result of its desire for self-sufficiency.

Additionally, the demand for the 1,3 Butadiene (BD) market has decreased in East Asia due to a temporary shortage in the vehicle industry, but it is predicted to rise profitably over the coming years. Additionally, due to unanticipated shutdowns and the relocation of significant producers to the East Asia region, the demand for the 1,3 Butadiene (BD) market in Europe has been steadily increasing. The Middle East and Latin America only make up a tiny fraction of the global market for 1,3 BD.

The rapid growth in the market demand for the tire and other secondary applications characterizes the 1,3 BD industry in Europe, Asia-Pacific, and North America. By 2025, it is anticipated that China will be producing 704 million tires annually, including 527 million passenger vehicle tires, 20,000 extra-large industrial tires, 29 million truck tires, and 54,000 airplane tires, among others. By 2025, China will also produce 420 million bicycle tires and 120.7 million motorbike tires yearly.

This has a significant role in driving 1,3 BD market demand in the nation over the anticipated timeframe. As a result of the expansion of important end-use sectors, including building & construction, automotive, and consumer goods in this area, Asia Pacific is also anticipated to have the quickest growth rate among the regions for 1,3 BD; China has been noted as the leading producer. As a result, consumption of 1,3 BD has increased not only in China but also in other Asia Pacific nations like Japan, Indonesia, India, and others.

Competitive Insight

Some of the major players operating in the global 1,3 Butadiene (BD) market include BASF SE, Bangkok Synthetics Co. Ltd, China National Petroleum Corporation, China Petroleum & Chemical Corporation, Dow Chemical Inc., ExxonMobil Chemical Corp., Jiutai Energy Inner Mongolia Co., Ltd., Lanxess Corporation, LG Chem Corp., Royal Dutch Shell PLC, Reliance Industries Inc., Shell Chemical LP, and TPC Group.

Recent Developments

In February 2022, Lummus Technology's Green Circles business and Synthos S.A. revealed that they have accomplished a significant milestone in the advancement of cutting-edge bio-butadiene technology. The bio-butadiene technology is now ready for use and the businesses have decided to begin the project's engineering and development phase.

1,3 Butadiene (BD) Market Report Scope

| Report Attributes | Details |

| Market size value in 2021 | USD 2.47 billion |

| Revenue forecast in 2030 | USD 3.99 billion |

| CAGR | 5.6% from 2022 - 2030 |

| Base year | 2021 |

| Historical data | 2018 - 2020 |

| Forecast period | 2022 - 2030 |

| Quantitative units | Revenue in USD billion and CAGR from 2022 to 2030 |

| Segments Covered | By Type, By Application, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key Companies | BASF SE, Bangkok Synthetics Co. Ltd, China National Petroleum Corporation, China Petroleum & Chemical Corporation, Dow Chemical Inc., ExxonMobil Chemical Corp., Jiutai Energy Inner Mongolia Co., Ltd., Lanxess Corporation, LG Chem Corp., Royal Dutch Shell PLC, Reliance Industries Inc., Shell Chemical LP, and TPC Group |

Download Sample Report of 1,3 Butadiene (BD) Market Share, Size, Trends, Industry Analysis Report, 2022 - 2030

Please fill out the form to request a customized copy of the research report.