Japan Medical Plastics Market Demand, Growth Analysis, 2026-2034

REPORT DETAILS

REPORT DETAILS

Market Statistics

Market Overview

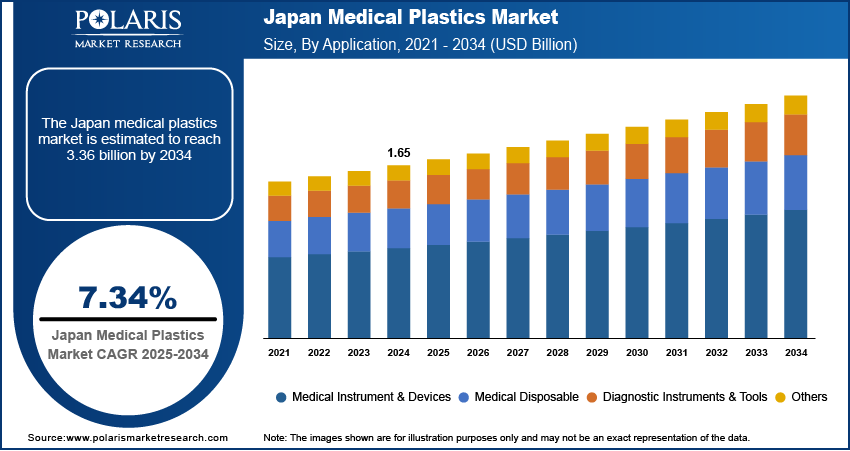

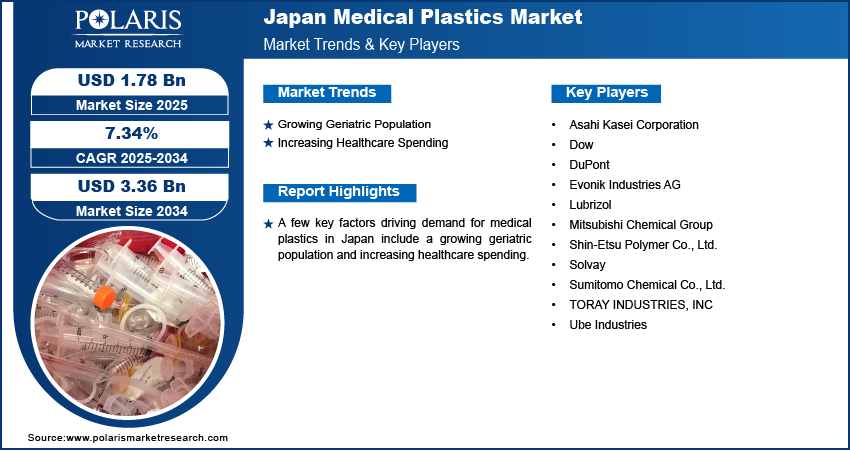

The Japan medical plastics market size was valued at USD 1,776.2 million in 2025, registering a CAGR of 7.3% during 2026–2034. The healthcare materials market is seeing increased demand, fueled in part by an aging population. Strong manufacturing capabilities in high-performance polymers also support this growth.

Key Insights

- Tokyo, Osaka, and Yokohama are key demand hubs in the Japan medical plastics market. Strong healthcare systems and manufacturing bases drive high use of medical devices and plastic materials.

- The thermoplastics segment represented 68.63% of the Japan medical plastics market's revenue in 2025. This is oowing to the biocompatibility of thermoplastics.

- The medical disposables segment is projected to register a CAGR of 7.8% from 2026 to 2034, owing to growing focus on infection control.

Market Statistics

- 2025 Market Size: USD 1,776.2 Million

- 2034 Projected Market Size: USD 3,358.8 Million

- CAGR (2026–2034): 7.3%

Industry Dynamics

- Japan's aging population is fueling a surge in demand for medical plastics. This stems from the reality that older people frequently contend with various health problems and long-term ailments. Consequently, there's a growing need for plastic-based medical devices like syringes, catheters, and implants to aid in managing these conditions.

- The increasing healthcare expenditure is fueling the Japan medical plastics market as it allows healthcare providers to use high-performance plastic-based solutions, including surgical equipment and IV tubes.

- The growing popularity of home healthcare services in the country is expected to create a lucrative market opportunity during the forecast period.

- The presence of major players and growing competition among them creates an entry barrier for new entrants, which hinders market expansion.

To Understand More About this Research: Download Sample Report

AI Impact on Japan Medical Plastics Market

- AI-based diagnostics and minimally invasive procedures are increasing demand for medical plastics. These applications need lightweight and durable materials.

- AI is supporting the use of advanced medical polymers. It helps improve material performance and product design.

- AI-driven technologies are increasing demand for smart medical plastics. Materials with antimicrobial coatings are being used more.

- AI is also supporting the shift toward sustainable materials. Demand for biodegradable and recyclable plastics is increasing in healthcare.

Japan continues to leverage engineering thermoplastics such as polyethylene, polypropylene, and polycarbonate for applications ranging from surgical instruments to drug delivery systems.

Japan is a leader in the area of precision polymer engineering. This is helping the growth of the Japan medical plastics market and the Japan healthcare plastics market. Japan has a good healthcare infrastructure and adheres to high-quality and compliant requirements. It also focuses on research and development activities. This is helping the growth of high-quality medical-grade polymers in Japan. The use of smart medical plastics in Japan, such as antimicrobial plastics and biodegradable plastics, is also growing. These polymers are developed to meet the growing demand for medical-grade polymers.

The Japan medical plastics market is also seeing strong demand due to the increasing use of AI-based diagnostics and minimally invasive procedures. These applications need materials that are lightweight, durable, and easy to sterilize. This supports the use of advanced medical polymers across healthcare settings. At the same time, the Japan healthcare plastics market is shifting toward more sustainable options, including biodegradable plastics. Demand for recyclable materials is increasing due to strict environmental rules and rising concerns around medical waste. The use of smart medical plastics, including those with antimicrobial coatings, is also broadening to meet these changing needs.

Industry Dynamics

Growing Geriatric Population

The aging population is a major driver of the Japan medical plastics market. The country has one of the highest shares of elderly individuals globally. This is rising demand for medical devices, implants, and disposable healthcare products.

This trend shows the rising aging population and Japan’s healthcare demand. Age-related conditions such as cardiovascular diseases, orthopedic disorders, and chronic respiratory illnesses are becoming more common. These conditions require constant medical care and the frequent use of healthcare products. As a result, the use of plastic-based medical devices is increasing in both hospitals and home care. As a result, medical plastics demand among the Japan elderly population is growing steadily. Devices such as catheters, syringes, and prosthetics are being used more often. This is supporting overall market growth.

Increasing Healthcare Spending

Healthcare spending in Japan is steadily increasing. Hospitals and healthcare providers are adopting more advanced materials and technologies. Rising healthcare spending on plastics in Japan is increasing the use of advanced medical materials. Providers are investing in high-performance polymers. These materials offer good biocompatibility and durability. They also perform well under repeated sterilization. This makes them suitable for critical medical use. As a result, medical polymer demand in Japan is growing. This includes applications in implantable devices and drug delivery systems. This trend is also supporting innovation and improving material quality.

Rise of Home Healthcare Services

The expansion of home healthcare services is creating new growth opportunities. More patients now use medical devices at home. This is increasing the use of home healthcare plastics in Japan. Single-use items are proving popular as well. This trend is beneficial for the market of disposable medical plastics within Japan. Items such as syringes and tubing are seeing increased usage in home care settings. These products are easy to use and dispose of. Overall, home-based care is increasing the demand for plastic medical products.

Market Restraints – Entry Barriers

New companies face challenges because of established competitors and strict regulatory requirements. The Japan medical plastics market competition is highly consolidated, making it difficult for new companies to gain a foothold.Companies must meet strict quality, safety, and compliance standards before entering the market. This increases both time and cost. These factors act as key entry obstacles in the healthcare plastics market in Japan. New market entrants also face challenges in building strong distribution networks and gaining trust from healthcare providers. In addition, long approval timelines can delay product entry. These obstacles create a barrier for those just starting out, and they also hinder the influx of new participants into the market.

Market Trends & Innovations

Japan's medical plastics market is undergoing a swift transformation, driven by continuous innovation and an increasing emphasis on sustainability. These changes are impacting the primary medical plastics trends in Japan, spanning various healthcare applications.

Smart Polymers & AI Integration

Material innovation is becoming more essential in healthcare. The use of smart polymers in Japan healthcare is increasing in modern medical devices. These materials can adjust to changes like temperature or pressure. This helps improve accuracy in treatments. AI is also being used to improve device performance and monitoring. Overall, these advances are making healthcare solutions more efficient and dependable.

3D Printing in Healthcare

3D printing is securing steady use in healthcare. It helps create personalized implants and medical devices using advanced polymers. These materials provide strength and flexibility. They also allow better design precision. This helps patient-specific treatments. It also reduces production time and material waste. As a result, 3D printing is becoming more common in medical manufacturing.

Sustainability Trends

Sustainability is becoming a key focus. The use of biodegradable plastics in Japan is increasing due to environmental concerns. Healthcare providers are also choosing recyclable materials to reduce waste. Companies are working on eco-friendly material solutions. These efforts support both regulatory needs and long-term sustainability goals.

Segmental Insights

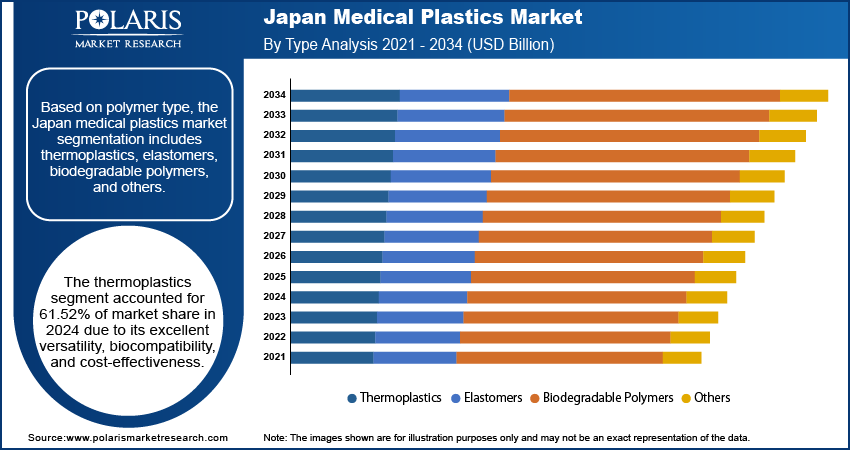

Polymer Type Analysis

Based on polymer type, the segmentation includes thermoplastics, elastomers, biodegradable polymers, and others. Thermoplastics dominated with 62.4% revenue share in 2025 due to versatility and cost-effectiveness. In the thermoplastics Japan medical market, demand stays strong due to wide usage across applications. At the same time, the segment is evolving with the rising use of high-performance materials. Polymers such as PEEK and bio-based plastics are gaining attention. These materials offer better strength, durability, and biocompatibility. This is increasing their use in advanced medical applications. As a result, the role of engineering plastics in healthcare in Japan is also expanding. This shift is gradually reshaping the overall segment.

Application Analysis

In terms of application, the Japan medical plastics market segmentation includes medical instruments & devices, medical disposables, diagnostic instruments & tools, and others. Medical disposables are expected to grow at a CAGR of 7.4% from 2026 to 2034. This growth is supported by the increasing demand for medical disposables in Japan. The demand is being met through hospitals, clinics, and home care. The focus of medical care providers is shifting to hygiene and patient safety. This is resulting in the use of medical disposables in routine medical care. At the same time, stronger infection control plastics in Japan standards are reassuring this shift. Post-pandemic practices have made infection prevention more essential than before. As a result, the use of items such as syringes, gloves, tubing, and diagnostic kits is increasing. These products help reduce contamination and improve safety. Broadly, demand for disposable plastic medical products continues to rise steadily.

Regulatory Landscape

The Japan medical plastics market operates under strict rules set by the Pharmaceutical and Medical Device Act (PMDA). PMDA regulations for medical plastics in Japan ensure product safety and performance. The PMDA reviews how materials are used in healthcare and checks their quality. Manufacturers must follow clear standards for testing, sterilization, and product safety. In addition, compliance with ISO certification standards is required. Japan's plastic safety standards in healthcare play a crucial role in upholding consistent quality and safeguarding patients within the realm of medical applications.

Value Chain Analysis

The value chain includes raw material suppliers, polymer manufacturers, medical device companies, and healthcare providers. Japan's medical plastics value chain can be characterized as well-structured, which ensures a consistent supply chain in the different segments. In addition, the value chain can be considered reliable because the country depends on both domestic production and imports for key supplies.

Pricing Analysis

Pricing is shaped by raw material costs, process challenges, and regulatory standards. The medical plastics pricing in Japan reflects these factors across different product types. Fluctuations in input costs can directly affect final pricing. In addition, the cost of polymer in healthcare in Japan varies. It is based on material quality and performance. High-performance plastics usually come at a higher cost due to their high strength, toughness, and biocompatibility.

Regional Insights

Some of the major demand hubs are Tokyo, Osaka, and Yokohama. These cities are major regional demand drivers for Japan medical plastics market. They have excellent healthcare infrastructures and a high number of hospitals and clinics. This increases the use of medical devices and plastic materials. The Tokyo healthcare plastics market is a key center due to advanced facilities and strong research activity. Osaka and Yokohama also contribute with well-established manufacturing bases. They help production and distribution through strong supply networks. These regions also have a skilled workforce. Continuous investments in healthcare infrastructure are further supporting demand. Growing patient needs and better access to care are adding to this trend. Overall, these cities remain important for market growth and development.

Key Players & Competitive Analysis

The Japan medical plastics market is highly competitive. Mitsubishi Chemical Group, Shin-Etsu Polymer, Sumitomo Chemical, Asahi Kasei, and Toray Industries are at the forefront. These Japanese medical plastics companies are recognized for their deep material knowledge and robust research programs. Their emphasis on product quality, safety, and adherence to stringent regulatory requirements allows them to stay competitive.

At the same time, global players like DuPont, Dow, Evonik, Arkema, Solvay, and Lubrizol are also active. Japan's healthcare plastics sector is a competitive arena, with major players vying for dominance through cutting-edge materials and strategic alliances. Numerous companies are actively pursuing growth, fueled by collaborations and the introduction of novel products. This dynamic is promoting increased innovation within the market.

A distinct trend is emerging: a move towards more sustainable materials. Businesses are exploring plastics that can be recycled or are derived from biological sources. Concurrently, the demand for lightweight, durable materials in modern medical devices continues to expand. This sector is highly competitive, fueled by a commitment to innovation and ongoing growth.

Key Companies

- Asahi Kasei Corporation

- Arkema

- Dow

- DuPont

- Evonik Industries AG

- Lubrizol

- Mitsubishi Chemical Group

- Shin-Etsu Polymer Co., Ltd.

- Solvay

- Sumitomo Chemical Co., Ltd.

- TORAY INDUSTRIES, INC

- Ube Industries

Japan Medical Plastics Industry Developments

- In November 2025, SK Capital Partners completed the acquisition of LISI Group’s medical division and set up Precera Medical. The step is aimed at building a stronger presence in specialty medical materials and healthcare components.

- In July 2025, Biomerics acquired Dependable Plastics and launched its Interventional Medical Plastics Division (IMP). This move adds to its capabilities in advanced plastics manufacturing for robotic and interventional medical devices.

Japan Medical Plastics Market Segmentation

By Polymer Type Outlook (Revenue, USD Million, 2021–2034)

- Thermoplastics

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polyethylene (PE)

- Polycarbonate (PC)

- Polyurethane

- Acrylonitrile Butadiene Styrene (ABS)

- Others

- Elastomers

- Biodegradable Polymers

- Others

By Application Outlook (Revenue, USD Million, 2021–2034)

- Medical Instruments & Devices

- Medical Disposables

- Diagnostic Instruments & Tools

- Others

By Manufacturing Outlook (Revenue, USD Million, 2021–2034)

- Extrusion Tubing

- Injection Molding

- Compression Molding

- Others

Future Outlook

The market is expected to grow steadily. Growth is driven by innovation, an aging population, and sustainability efforts. The Japan medical plastics forecast 2034 shows continued expansion across healthcare uses. Demand will rise with better access to care and higher medical needs. The focus of future healthcare materials in Japan will be on advanced and high-performance polymers.

AI and robotics are also being used more in healthcare. These technological advancements are boosting both precision and productivity. Cutting-edge materials are contributing to safer and more effective products. Overall, the market will keep changing, prioritizing innovation and sustained expansion.

Japan Medical Plastics Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 1,776.2 million |

| Market Size in 2026 | USD 1,906.2 million |

| Revenue forecast by 2034 | USD 3,358.8 million |

| CAGR | 7.3% from 2026-2034 |

| Base Year | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Quantitative Units | Revenue in USD million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segment Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The market was valued at USD 1,776.2 million in 2025. It is expected to reach USD 3,358.8 million by 2034.

Growth is driven by an aging population. Healthcare spending is also increasing. New polymer materials are also helping with growth.

Thermoplastics lead the market. They are easy to use and cost-effective.

Common polymers include PE, PP, and PVC. High-performance materials like PEEK are also used.

Key trends include smart polymers, sustainability, and 3D printing. These are changing the market.

Key players include Asahi Kasei Corporation, Arkema, Dow, DuPont, Evonik Industries AG, Lubrizol, Mitsubishi Chemical Group, Shin-Etsu Polymer Co., Ltd., Solvay, Sumitomo Chemical Co., Ltd., TORAY INDUSTRIES, INC, and Ube Industries.

The aging population is driving up the need for medical devices. This, in turn, fuels demand for both implants and disposable items.

Smart polymers can react to changes like heat or pressure. They are used in advanced medical products.

Yes, there is growing use of recyclable plastics. The focus on sustainability is increasing.

PMDA is the regulatory body. It checks the safety and quality of medical products.

Medical plastics are used in devices, packaging, implants, and testing equipment.

Download Sample Report of Japan Medical Plastics Market

Please fill out the form to request a customized copy of the research report.