Aerospace Coatings Market Research Report, Size, Share & Forecast by 2026 - 2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Aerospace Coatings Market Summary

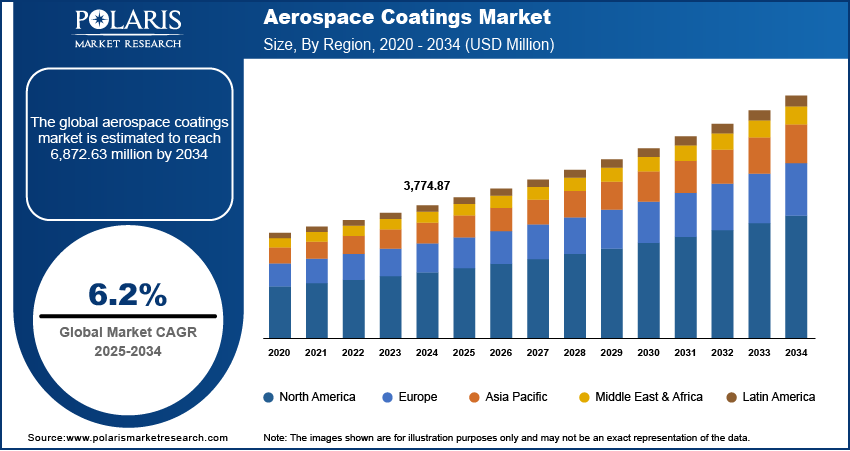

The global aerospace coatings market size was valued at USD 4,002.87 million in 2025 and is projected to register a CAGR of 6.2% from 2026 to 2034. This growth is driven by the rising tourism across the world and increasing aircraft production. Growing preference for lightweight, fuel-efficient coatings will also drive market expansion in the coming years. The market growth is attributed to aircraft lifecycle management, including new aircraft production (OEM demand) and recurring maintenance, repair, and overhaul (MRO) activities. Aerospace coatings are not one-time applications. Aircraft exterior surfaces are repainted every 5–7 years. It is creating steady aftermarket demand throughout the operational life of aircraft.

Market Statistics

Key Takeaways

- The top-coat segment held the largest revenue share in 2025. Its critical role in providing aesthetic and functional benefits for aircraft surfaces contributed to its dominance.

- The exterior segment accounted for a significant market share in 2025. It is driven by its essential role in protecting aircraft from harsh environmental conditions and enhancing operational efficiency.

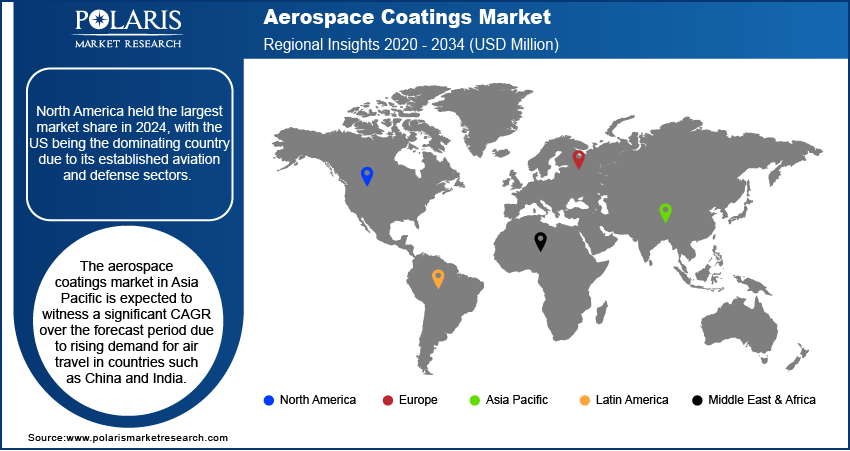

- North America held the largest market share in 2025. North America’s extensive MRO operations ensure its dominance in the global market.

- The Asia Pacific aerospace coatings market is expected to register a significant CAGR during the forecast period. The growth is attributed to the rising demand for air travel in countries such as China and India.

Industry Dynamics

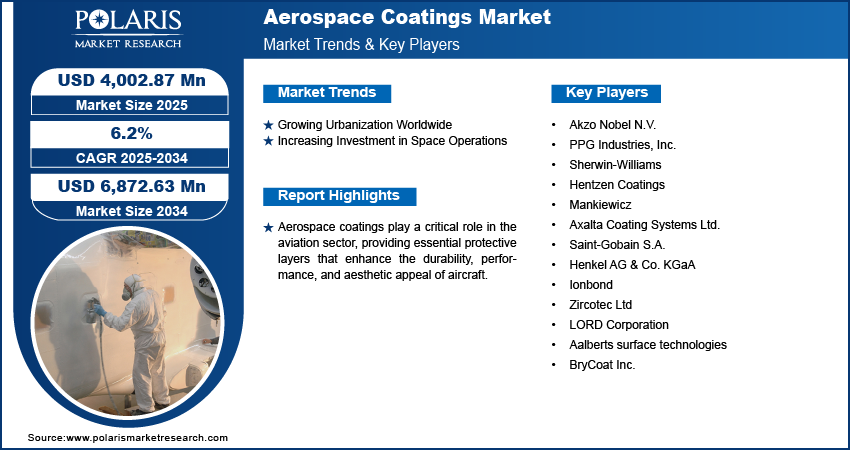

- Urbanization propels economic growth and disposable income. It encourages people to travel, further fueling commercial aviation. Thus, rapid urbanization drives the aerospace coatings market growth.

- Rising investments in space operations across various countries fuels the global aerospace coating market growth.

- Volatility in coating prices restrains the demand for aerospace coatings.

- Increasing preference for lightweight, fuel-efficient coatings is expected to create lucrative opportunities for the industry players in the coming years.

AI Impact on Aerospace Coatings Market

- Predictive Maintenance: AI-enabled analytics are used to predict coating degradation. This cuts downtime and extends the service life of aircraft.

- Smart Formulations: Machine learning (ML) accelerates the development of better coatings. These coatings resist corrosion, UV radiation, and extreme temperatures.

- Cost Optimization: AI models streamline raw material usage and application processes. It lowers operational costs and maintains performance standards.

- Quality Control: Automated vision systems powered by AI detect micro-defects in coatings. This function ensures higher reliability and safety in aerospace operations.

- Sustainability: AI supports eco-friendly innovations by finding greener alternatives to traditional chemical compounds. It meets regulatory requirements.

- Customization: The recommendation allows for tailored coating solutions for aircraft models and mission profiles. It enhances the efficiency and durability of aircraft.

- Supply Chain Efficiency: Predictive algorithms improve inventory management and logistics for coating materials. This cuts down delays in aerospace manufacturing.

- Competitive Advantage: Companies use AI for shorter innovation cycles. This keeps them ahead in a highly regulated and technology-driven market.

Aerospace coatings play a critical role in the aviation sector, providing essential protective layers that enhance the durability, performance, and aesthetic appeal of aircraft. These coatings are specifically formulated to withstand extreme flight conditions, including rapid altitude changes, temperature fluctuations, and exposure to harsh environmental elements such as UV radiation and corrosive substances. Exterior aerospace coatings, particularly polyurethane-based systems, dominate market value. They have superior weather resistance, gloss retention, and lightweight properties. These benefits directly impact fuel efficiency and operating costs for airlines.

The rise in global tourism boosts the expansion of the aerospace coatings industry. According to the UN Tourism World Tourism Barometer, around 1.1 million international tourist arrivals (overnight visitors) were reported from January to September 2024. This represents an increase of approximately 11% compared with the same period in 2023. Due to rising tourism, airlines expand fleets to accommodate the increasing number of passengers and rising flight frequencies. This causes increased wear on aircraft. It necessitates regular maintenance, painting and coating to ensure performance, safety, and appearance of aircraft. This, in turn, raises the demand for aerospace coatings. Additionally, airlines often update their branding and livery to attract more customers, which also increases the need for high-quality coatings. The rising global air passenger traffic and upsurging aircraft utilization accelerate repainting and maintenance cycles. It is increasing demand for aerospace coatings.

Growing government investments in modernizing and upgrading existing aircraft propel the aerospace coatings market demand. Modernization efforts include refurbishing older aircraft to meet new safety standards, improve fuel efficiency, and incorporate new technologies. These processes need specialized aerospace coatings to protect aircraft surfaces and improve aerodynamics. These coatings help resist environmental factors such as corrosion and temperature changes. This increase in government-funded modernization boosts the demand for coatings for military aircraft.

Defense aviation is a high-margin segment for aerospace coatings. It need to meet stringent performance requirements, including corrosion resistance, infrared suppression, and thermal protection. Government-funded fleet modernization programs support long-term demand stability for aerospace coatings manufacturers.

OEM vs MRO Demand Split in Global Aerospace Coatings Industry

| Aspect | OEM (Original Equipment Manufacturer) Demand | MRO (Maintenance, Repair & Overhaul) Demand |

| Primary Application | New aircraft manufacturing and factory finishing | Repainting, touch-ups, corrosion repair, and refurbishment |

| Demand Driver | Aircraft production rates and new fleet deliveries | Aging fleet, regulatory repaint cycles, and corrosion protection needs |

| Coating Type Focus | High-performance primers, topcoats, and specialty functional coatings | Durable, fast-curing, easy-application coating systems |

| Volume Pattern | Lower frequency but higher coating value per aircraft | Higher frequency with recurring repaint cycles |

| Revenue Stability | Cyclical, dependent on OEM order backlogs | More stable and recurring due to mandatory maintenance intervals |

| Customization Level | Strict OEM specifications and color schemes | Flexible color changes and livery refresh requirements |

| Margin Profile | Lower margins due to long-term supply contracts | Higher margins from service-based and urgent coating demand |

| Market Share Trend | Growing with rising aircraft deliveries | Dominant share driven by global fleet expansion and life extension programs |

Market Dynamics

Aerospace Coatings Market Drivers

Growing Urbanization Worldwide

The growing urbanization worldwide is projected to propel the global market growth. As per data published by the United Nations Population Fund, more than half of the world's population, which is about 4 million, lives in cities and towns and is expected to increase to about 5 million by 2030. There is a greater need for efficient transportation networks, including air travel, to connect cities and support economic activity as urbanization spurs. This rise in urban connectivity leads to an increase in airline operations, necessitating frequent maintenance and the use of aerospace coatings to protect and enhance aircraft surfaces. Urbanization also drives the construction of new airports and the expansion of existing ones. It requires updated aircraft coated with durable, weather-resistant finishes. Additionally, urbanization propels economic growth and disposable income. It encourages people to travel across regions. This factor fuels demand for aerospace coatings in commercial aviation.

Increasing Investment in Space Operations

The increasing investment in space operations is estimated to fuel the global market. The production and maintenance of spacecraft are increasing as government agencies and private companies invest in ambitious space missions. These missions include satellite launches, space exploration, and space tourism. This growth requires special coatings, such as aerospace coatings. These coatings improve durability, ensure thermal regulation, and boost the performance of spacecraft and satellite launch vehicles in the harsh vacuum of space. Additionally, the increased focus on reusable spacecraft and longer mission lengths raises the demand for new aerospace coatings. The rising investments in space operations expand the use of aerospace coatings beyond traditional aircraft. Reusable launch vehicles, satellites, and spacecraft require specialized aerospace coatings for thermal regulation, radiation shielding, and surface durability in extreme space environments, It supports demand for space vehicle coatings.

Segment Analysis

By Product Type

Based on product type, the segmentation includes top coats, primers, and others. The top coats segment held the largest share in 2025. Top coats provide important aesthetic and functional benefits for aircraft surfaces. Airlines and manufacturers prefer top coats to improve the visual appeal of aircraft while ensuring durability, UV resistance, and protection against tough environmental conditions like corrosion, extreme temperatures, and abrasion. The increasing focus on branding and customization of aircraft has further driven the demand for these coatings. Additionally, technological advancements have resulted in high-performance, lightweight material top coats. These products enhance fuel efficiency and lower emissions. The aerospace top coats segment remains dominant due to their frequent need for replacement and their direct exposure to environmental stressors.

The primers segment is expected to grow rapidly during the forecast period. Primers are crucial in the coating process. They improve adhesion, protect the underlying material from corrosion, and create a smooth surface for additional layers. The increasing use of composite materials in aircraft manufacturing propels the demand for specialized primers that bond well with these materials. Additionally, governments and private companies are investing heavily in updating aging fleets. It requires thorough surface preparation and reapplication of protective coatings, including primers. The growth of the aerospace primers market is driven by the increased use of composite materials in modern aircraft structures, which need specialized adhesion and corrosion protection systems.

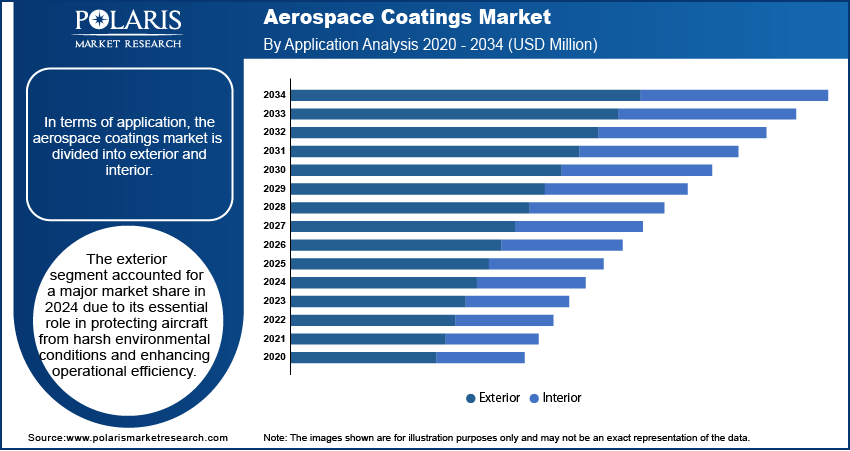

By Application

In terms of application, the aerospace coatings industry is divided into exterior and interior. The exterior segment accounted for a major market share in 2025 due to its essential role in protecting aircraft from harsh environmental conditions and enhancing operational efficiency. Exterior coatings protect aircraft surfaces from extreme temperatures, UV radiation, and moisture. This reduces the risk of corrosion and structural damage. Airlines and manufacturers are focusing more on exterior coatings to improve aerodynamics. This also helps with fuel efficiency and lowers carbon emissions. The increasing need for repainting and maintaining aging fleets, along with the rising demand for coatings that provide durability and lightweight properties, contributed to the segment dominance.

| Factor | Exterior Coatings | Interior Coatings |

| Performance Requirements | Must withstand UV, corrosion, erosion, de-icing fluids, fuel, and extreme temperatures | Focus on aesthetics, wear resistance, flame retardancy, and low toxicity |

| Coating System Complexity | Multi-layer systems (pretreatment, primer, topcoat, clear coat) with high material cost | Fewer layers and simpler formulations reduce system cost |

| Regulatory & Testing Costs | Extensive FAA/EASA qualification, weathering, and chemical resistance testing | Lower certification intensity compared to exterior systems |

| Application Area | Covers large surface areas including fuselage, wings, and tail | Applied to cabins, galleys, cargo holds, and cockpit components |

| Maintenance Cycle | Requires periodic full repainting and touch-ups | Replaced selectively during cabin refurbishments |

| Price per Liter | Significantly higher due to performance additives and specialty resins | Lower due to simpler chemistry and higher volume materials |

| Value Share Logic | Commands the majority of total coatings revenue despite lower volume due to premium pricing and complex systems | Represents smaller value share but steady demand from cabin upgrades and MRO activities |

Regional Insights

By region, the aerospace coatings industry is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. North America dominated the revenue share in 2025. The presence of large maintenance, repair, and overhaul hubs, along with strict standards related to emissions and coating performance, helped the region lead the market. The U.S. is the largest player in the aerospace coatings market in North America because of its strong aviation and defense sectors. The country’s commercial aviation industry comprises major airlines and aircraft manufacturers like Boeing. It creates steady demand for coatings that improve fleet performance and durability. Government allocate large defense budgets to update military aircraft. Such government support also boosts the market. The rising focus on sustainability and efficiency has led to using innovative coatings that reduce weight and improve fuel efficiency. The region’s extensive maintenance operations have ensured consistent demand, reinforcing North America’s position as the leading market.

The Asia Pacific aerospace coatings market is expected to record a significant CAGR during 2026-2034. Rising demand for air travel in countries such as China and India propels the industry growth. Increasing government initiatives for aerospace infrastructure and the expansion of low-cost carriers accelerate the region’s growth. Rapid fleet expansion, increasing aircraft deliveries, and rising investments in domestic aircraft manufacturing position Asia Pacific as the fastest-growing aerospace coatings industry globally. China is emerging as a key country in the region due to its growing domestic aviation market. The China's market expansion is driven by rising investments in aircraft manufacturing, including the development of indigenous commercial planes such as the COMAC C919.

Aerospace Coatings Key Market Players & Competitive Analysis Report

Major market players are investing heavily in research and development in order to expand their offerings, which will help the aerospace coatings industry grow even more. Market participants adopt various strategic activities. These strategies help them expand their global footprint. They also emphasis on important market developments, including innovative launches, international collaborations, higher investments, and mergers and acquisitions between organizations.

The aerospace coatings industry is fragmented, with the presence of numerous global and regional market players. Major players in the market include Akzo Nobel N.V.; PPG Industries, Inc.; Sherwin-Williams; Hentzen Coatings; Mankiewicz; Axalta Coating Systems Ltd.; Saint-Gobain S.A.; Henkel AG & Co. KGaA; Ionbond; Zircotec Ltd; LORD Corporation; Aalberts surface technologies; and BryCoat Inc.

List of Key Companies

- Akzo Nobel N.V.

- PPG Industries, Inc.

- Sherwin-Williams

- Hentzen Coatings

- Mankiewicz

- Axalta Coating Systems Ltd.

- Saint-Gobain S.A.

- Henkel AG & Co. KGaA

- Ionbond

- Zircotec Ltd

- LORD Corporation

- Aalberts surface technologies

- BryCoat Inc.

Aerospace Coatings Industry Developments

- December 2024: Honeywell International Inc. announced that it was considering a potential divestiture of its aerospace division from its broader conglomerate portfolio.

- September 2023: Sherwin-Williams launched aerospace conductive coating (CM0485115). It is expected to enable aircraft owners to impart conductivity onto aluminum and composite substrates. The coating offers high conductivity to non-conductive substrates by producing an anti-static conductive film on their surfaces with a resistivity of 0.1 to 100,000 ohms per square meter.

- July 2022: PPG Industries, Inc., a major global supplier of paints, coatings, and specialty materials, announced that it will partner with Aerobrand, a U.K. airline brand and design consultancy, to provide airline customers with a unique service that combines paint supply with livery design. The partnership will enable customers to work closely with designers to create custom paint colors and give direct input on the design of their livery at PPG LIVERY LAB aircraft coatings and design facilities in Burbank, California, and Shildon, U.K.

- July 2022: Akzo Nobel N.V., a prominent Netherland-based multinational company specializing in the production of paints and performance coatings, announced a EUR 20 million investment to increase and improve production at two of its sites in France. A total of EUR 15 million will be spent on the company’s aerospace coatings facility in Pamiers, and another EUR 5 million will be spent on improving production flexibility at the decorative paints site in Montataire

Aerospace Coatings Market Segmentation

By Product Type Outlook (Volume, Tons; Revenue, USD Million, 2021–2034)

- Top-coat

- Primer

- Others

By Resin Type Outlook (Volume, Tons; Revenue, USD Million, 2021–2034)

- Polyurethanes

- Epoxy

- Others

By Technology Outlook (Volume, Tons; Revenue, USD Million, 2021–2034)

- Liquid Coating

- Powder Coating

- Others

By End User Outlook (Volume, Tons; Revenue, USD Million, 2021–2034)

- MRO

- OEM

By Application Outlook (Volume, Tons; Revenue, USD Million, 2021–2034)

- Exterior

- Interior

By Aviation Type Outlook (Volume, Tons; Revenue, USD Million, 2021–2034)

- Commercial Aviation

- Military Aviation

- General Aviation

- Others

By Regional Outlook (Volume, Tons; Revenue, USD Million, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Aerospace Coatings Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 4,002.87 million |

| Market Size in 2026 | USD 4,245.84 million |

| Revenue Forecast in 2034 | USD 6,872.63 million |

| CAGR | 6.2% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD million, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

• The global aerospace coatings market size was valued at USD 3,774.87 million in 2024 and is projected to grow to USD 6,872.63 million by 2034.

• The global market is projected to register a CAGR of 6.2% during the forecast period.

• North America had the largest share of the global market in 2024.

• Some of the key players in the market are Akzo Nobel N.V.; PPG Industries, Inc.; Sherwin-Williams; Hentzen Coatings; Mankiewicz; Axalta Coating Systems Ltd.; Saint-Gobain S.A.; Henkel AG & Co. KGaA; Ionbond; Zircotec Ltd; LORD Corporation; Aalberts surface technologies; and BryCoat Inc.

• The primer segment is projected for significant growth in the global market.

• The exterior segment dominated the aerospace coatings market in 2024.

The global aerospace coatings market is projected to reach USD 6,872.63 million by 2034, registering a CAGR of 6.2% during 2026–2034.

The polyurethanes segment leads the market due to their properties such as UV resistance, durability, corrosion protection, and composite compatibility.

Rising aircraft production and fleet expansion boost the industry growth. Also, stringent environmental regulations and increasing MRO activities drive the growth.

North America dominates with the largest market share. Robust aerospace manufacturing infrastructure and defense spending contributed to the dominance. Also, the presence of major OEMs contributes to the leading position.

The MRO (Maintenance, Repair, and Overhaul) segment leads with the largest share. The segment growth is fueled by rising number of aging fleets and regular repaint cycles. Also, expanding service operations accelerates the segment’s leadership.

Download Sample Report of Aerospace Coatings Market

Please fill out the form to request a customized copy of the research report.