Asphalt Release Agents Market Business Trends, Strategies, and Forecasts, 2025-2034

REPORT DETAILS

REPORT DETAILS

Market Statistics

What is Asphalt Release Agents Market Size?

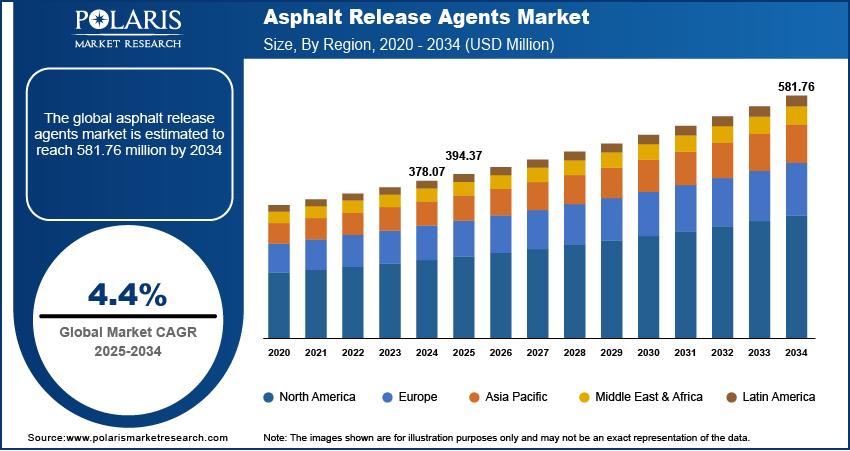

The global asphalt release agents market size was valued at USD 378.07 million in 2024, growing at a CAGR of 4.4% from 2025–2034. Key factors driving the growth is expansion of road construction, growing environmental regulations, and technological advancement.

Key Insights

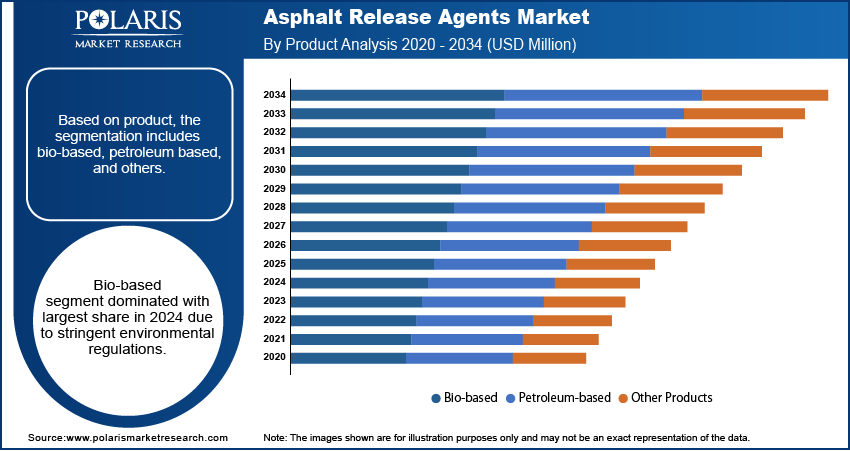

- Bio-based segment dominated with largest share in 2024 due to stringent environmental regulations

- Rollers segment is expected to witness a significant share over the forecast period as it is extensively used in asphalt compaction

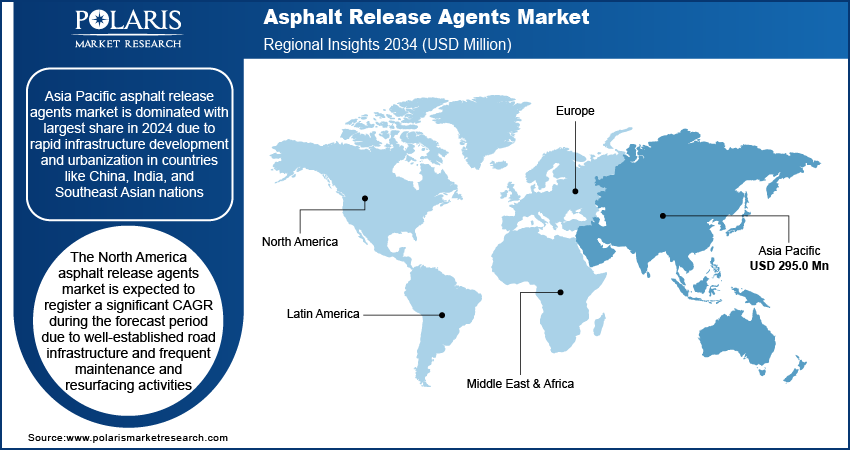

- Asia Pacific asphalt release agents market is dominated with largest share in 2024 due to rapid infrastructure development and urbanization in countries like China, India, and Southeast Asian nations

- The North America asphalt release agents market is expected to register a significant CAGR during the forecast period due to well-established road infrastructure and frequent maintenance and resurfacing activities

Industry Dynamics

- The rise in number of road constructions is driving the growth.

- Rapid rising environmental regulations is fueling the growth.

- Technological advancement is boosting the growth.

- High production costs limits the growth of the market.

Market Statistics

- 2024 Market Size: USD 378.07 Million

- 2034 Projected Market Size: USD 581.76 Million

- CAGR (2025-2034): 4.4%

- Asia Pacific: Largest Market Share

An asphalt release agent is a chemical solution applied to truck beds, pavers, and equipment to prevent asphalt from sticking during transport and handling. It creates a temporary, non-stick barrier without affecting the asphalt mix. Many modern agents are biodegradable alternatives to diesel-based products.

The rising focus on workplace safety is driving the demand for the asphalt release agents. The number of cases related to workplace hazards is rising worldwide. According to the International Labour Organization, approx. 3 million workers die annually due to workplace hazards. This has emphasized the used of the materials that are non-toxic, non-flammable. Asphalt release agents are biodegradable agents an reduce workplace accidents, improve equipment handling conditions, which make them a preferred choice for contractors and road maintenance. Moreover, rising government regulation on the workplace safety is further fueling the demand for the asphalt release agents, thereby driving the industry growth.

Technological advancement in the production process is fueling the industry growth. These advancements have enabled manufacturers to produce product to meet environmental regulations. Manufacturers are producing the biodegradable, plant-based, and low-VOC solutions, which is fueling the adoption in developed as well as developing regions. Further, countries are implementing stricter construction standards which is further driving the demand for the advance asphalt release agents, further driving the expansion.

Drivers & Opportunities

What are Factors Driving Industry Growth?

Growing Road Construction and Maintenance Activity: Major developing countries such as India, Brazil, Vietnam are investing heavily in the for the road construction. According to the Invest India, the Indian Government invested approx. USD 60.3 billion for the 34,800 Km of highways to improve the connectivity across economic corridors. This growth in the investment for road construction is fueling the demand for the asphalt release agents. This is used to prevent asphalt from sticking to equipment during long construction projects. Further, most of the road in developed regions such as North America, and Europe are due for maintenance activities, which is further driving the demand for these agents, thereby driving the industry growth.

Environmental Regulations: The environmental regulations on the flammable and toxic material are rising. This rise in the regulations is driven by increase in the public awareness of health and environmental risks and a global push toward sustainability and international cooperation. This rise in the environmental regulations is fueling the demand for the asphalt release agent globally. It is biodegradable, non-toxic, and low-VOC formulations which meet the compliance standards and reduce environmental impact and improve operational safety, consequently driving the demand. Moreover, rising stricter regulations on emissions control, groundwater contamination, and workplace exposure is further driving the demand, thereby driving the growth.

Country Wise Government Regulation Scenario:

| Country | Description |

| U.S. | In the United States, the use of diesel as an asphalt release agent is prohibited under federal law. The Resource Conservation and Recovery Act (RCRA), the Clean Water Act, and the Oil Pollution Act all ban the use of diesel for this purpose. State Departments of Transportation (DOTs) enforce these bans strictly, and violations can result in significant fines and penalties. Diesel is considered a hazardous material due to its flammability, toxicity, and environmental impact. Most states require the use of approved, non-petroleum-based release agents for asphalt paving operations |

| Germany | In Germany, the use of diesel as an asphalt release agent is prohibited by law. Diesel is recognized as harmful to both the environment and worker health, and its use is strictly forbidden in road construction and asphalt mixing plants. The German government and industry bodies mandate the use of environmentally friendly, non-diesel alternatives for all asphalt release and cleaning applications |

| India | In India, there are no specific national regulations that explicitly ban diesel-based asphalt release agents. However, general environmental and occupational safety regulations under the Ministry of Environment, Forest and Climate Change and the Directorate General of Factory Advice Service and Labour Institutes (DGFASLI) discourage the use of hazardous substances like diesel in industrial applications. The use of diesel is discouraged due to its environmental and health risks, and industry guidelines recommend safer alternatives |

| Brazil | In Brazil, there are no specific federal regulations that explicitly ban diesel-based asphalt release agents. However, environmental agencies such as IBAMA (Brazilian Institute of Environment and Renewable Natural Resources) and state-level environmental departments discourage the use of hazardous substances in construction and road paving. Industry guidelines recommend the use of safer, non-diesel alternatives to minimize environmental impact. |

| Australia | In Australia, the use of diesel as an asphalt release agent is discouraged due to environmental and health regulations. The National Environment Protection Council (NEPC) and state environmental agencies recommend the use of safer, non-diesel alternatives for asphalt release and cleaning applications. Diesel is considered a hazardous substance and its use is regulated under occupational health and safety laws |

Segmental Insights

Why Bio-based Dominated in 2024?

Bio-based segment dominated with largest share in 2024 due to stringent environmental regulations. Governments worldwide are implementing stringent regulations on the traditional petroleum-based products. As a result, the demand for the advance biodegradable product in various applications is rising, including bio-based asphalt release agents. Traditional diesel-based release agents are now being replaced by new bio-based release agents as a result of these stricter regulations. Moreover, rising awareness and government standards on workplace safety is further fueling the segment growth.

Which Segment by Application is Expected to Witness a Significant Share?

Rollers segment is expected to witness a significant share over the forecast period as it is extensively used in asphalt compaction. Sticking asphalt on rollers can reduce the efficiency for long duration projects. This is driving the demand for the asphalt release agents. It prevents asphalt from sticking to construction equipment. Moreover, rising road construction activity in the urban as well as rural areas of developing countries is fueling the need for rollers and consequently for the asphalt release agents, thereby driving the growth.

Regional Analysis

What are Regional Statistics of Industry?

Asia Pacific asphalt release agents market is dominated with largest share in 2024 due to rapid infrastructure development and urbanization in countries like China, India, and Southeast Asian nations. Governments are investing heavily in road construction, highway expansion, and maintenance projects, driving demand for effective asphalt handling solutions. Additionally, increasing awareness of environmental regulations has encouraged the adoption of eco-friendly, bio-based release agents. The rising use of modern road construction machinery, including pavers and rollers, further fuels market expansion.

The North America asphalt release agents market is expected to register a significant CAGR during the forecast period due to well-established road infrastructure and frequent maintenance and resurfacing activities. The United States and Canada are increasingly focusing on sustainable construction practices, promoting the use of biodegradable and low-VOC asphalt release agents. Advanced road construction technologies and modern equipment, including high-capacity rollers and pavers, have increased the demand for efficient, non-stick solutions. Additionally, strict environmental and safety regulations have accelerated the shift from petrochemical to eco-friendly formulations. These trends, combined with high government and private sector investments in transportation projects, sustain strong market growth in North America.

Key Players & Competitive Analysis

The market is competitive, with players competing on formulation technology, environmental compliance, and distribution reach. Key companies, such as BG Chemical, Industrial Chemical Solutions, McGee Industries, Meyer Lab, Miller-Stephenson, Rhomar Industries, SoySolv, UCHS, Zeller+Gmelin, and Zep, emphasize biodegradable and non-hazardous products to meet tightening international regulations. Market differentiation relies on performance across varied climatic conditions, technical service capabilities, and partnerships with global road construction firms and equipment manufacturers to strengthen presence across North America, Europe, and Asia-Pacific.

Key Players

- BG Chemical

- Industrial Chemical Solutions

- McGee Industries, Inc.

- Meyer Lab

- Miller-Stephenson Chemical Company, Inc.

- Rhomar Industries Inc.

- SoySolv

- UCHS

- Zeller+Gmelin

- Zep

Industry Developments

April 2025, Harima Chemicals announced biomass-based asphalt regeneration additives developed with Japan’s Public Works Research Institute and Nihon University. The pine-derived agents reduced carbon emissions, improved wear resistance, and restored aged asphalt performance, supporting Japan’s goals for longer-lasting, lower-carbon road infrastructure.

Asphalt Release Agents Market Segmentation

By Product Outlook (Volume, Kilotons, Revenue, USD Million, 2020–2034)

- Bio-based

- Petroleum-based

- Other Products

By Application Outlook (Volume, Kilotons, Revenue, USD Million, 2020–2034)

- Truck Beds

- Pavers

- Rollers

- Other Applications

By Regional Outlook (Volume, Kilotons, Revenue, USD Million, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Asphalt Release Agents Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 378.07 Million |

| Market Size in 2025 | USD 394.37 Million |

| Revenue Forecast by 2034 | USD 581.76 Million |

| CAGR | 4.4% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Volume in Kiloton, Revenue in USD Million and CAGR from 2025 to 2034 |

| Report Coverage | Volume Forecast, Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 378.07 million in 2024 and is projected to grow to USD 581.76 million by 2034.

The global market is projected to register a CAGR of 4.4% during the forecast period.

Asia Pacific dominated the market in 2024

A few of the key players in the market are- BG Chemical, Industrial Chemical Solutions, McGee Industries, Inc., Meyer Lab, Miller-Stephenson Chemical Company, Inc., Rhomar Industries Inc., SoySolv, UCHS, Zeller+Gmelin, and Zep.

The bio-based segment dominated the market revenue share in 2024.

The rollers segment is projected to witness the fastest growth during the forecast period.

Download Sample Report of Asphalt Release Agents Market

Please fill out the form to request a customized copy of the research report.