Bioethanol Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

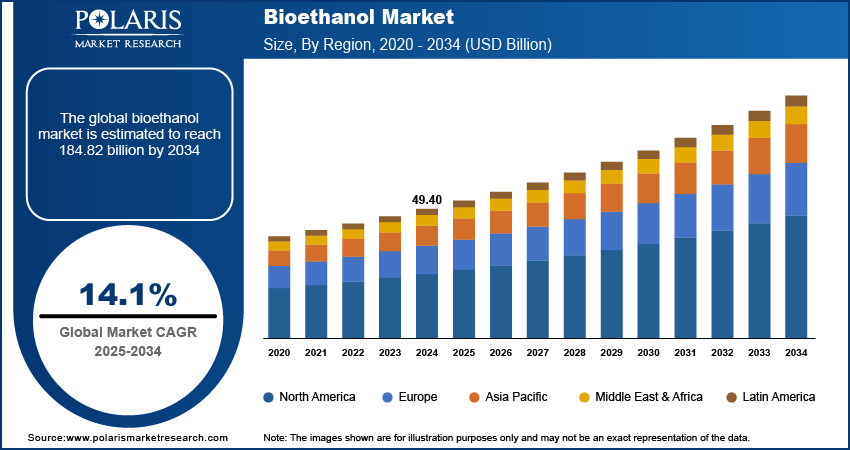

Bioethanol Market Summary

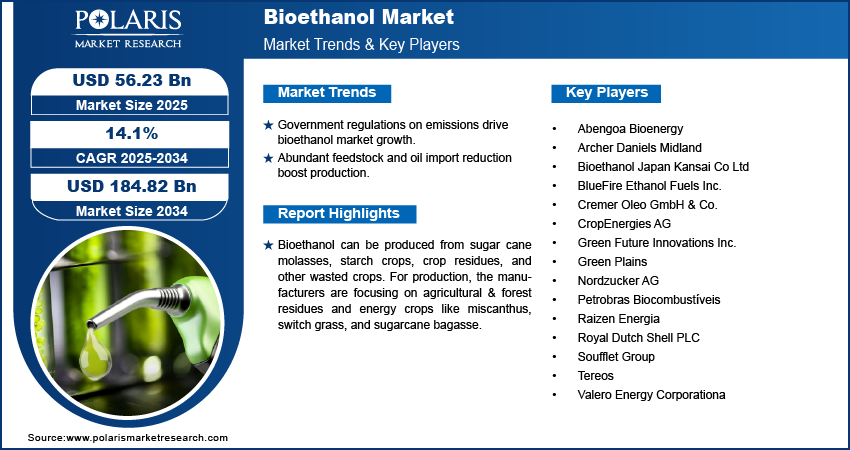

The global bioethanol market was valued at USD 56.23 billion in 2025 and is expected to grow at a CAGR of 14.1% during the forecast period. The bioethanol market dynamics help industry players align their business strategies with current and future trends. It examines technological advances and breakthroughs in the industry and their impact on the market presence. Furthermore, a detailed regional analysis of the industry at the local, national, and global levels has been provided.

Market Statistics

Key Takeaways

- North America dominated the market with 36.0% share in 2025 due to the increasing approvals and government backing for developing eco-friendly and sustainable fuels.

- Asia Pacific is expected to witness rapid growth at a CAGR of 15.3% during the forecast period. This is due to government-led energy security policies and strong agricultural production capabilities.

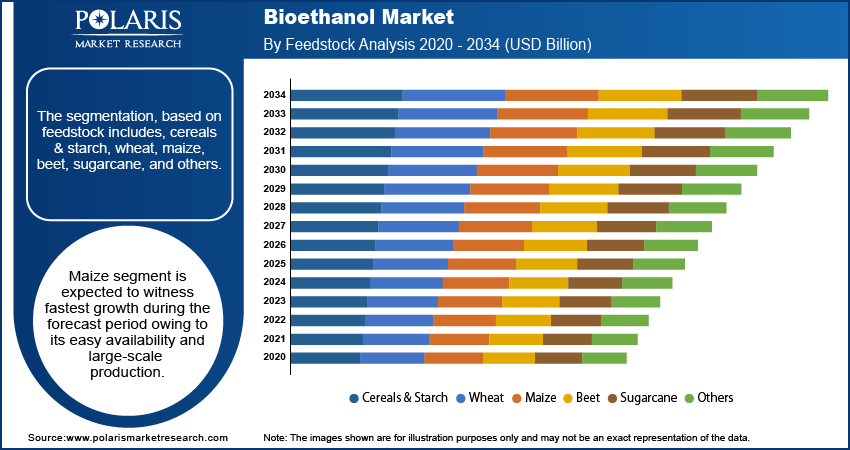

- The maize segment is expected to witness rapid growth at a CAGR of 14.4% during the forecast period. This is due to its easy availability and large-scale production.

- The transportation segment dominated the market with 57.0% share in 2025. This is due to the utilization of bio-ethanol as a fuel and fuel additive in the automotive and transportation industries.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Strict government mandates and regulations for reducing emissions are driving the expansion opportunities.

- The feedstock availability and the need to reduce dependence on crude oil imports are accelerating the production of bioethanol and reducing energy dependence.

- The reliance on food-grade feedstock such as corn and sugarcane has created price unpredictability and concerns over resource allocation.

- Advances in cellulosic ethanol technology allows the use of unlocking sustainable production, non-food agricultural waste, and expansion into new feedstock sources.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

What is Bioethanol?

Bioethanol can be produced from sugar cane molasses, starch crops, crop residues, and other wasted crops. For production, the manufacturers are focusing on agricultural & forest residues and energy crops like miscanthus, switch grass, and sugarcane bagasse. It can be used as a fuel in isolation and in mixtures with other fossil fuels. Bioethanol is a biodegradable, renewable energy resource produced from biomass through sugar fermentation and chemical process. Bioethanol is an attractive substitute for conventional fuel sources due to its high octane value and lower greenhouse gas emissions.

Production involves different manufacturing steps, such as fermentation, distillation technologies, dehydration, etc. Bioethanol has various properties, such as homogeneity, physical stability, low viscosity, weak lubricity, anti-corrosiveness, and better antiknock characteristics. The versatility of bioethanol is used as feedstock in the chemical market, fuel for power generation, a substitute for petrol in road transport vehicles, etc.

Additionally, Sustainable Development Goals (SDG) is one of the primary goals of the United Nations, which slows down climate change and reduce global warming. Biofuels play an essential role in this. Also, depleting energy resources and increasing focus on renewable energy sources are expected to boost the market growth. Technological advances and increased R&D to produce ethanol from algae are expected to increase market demand due to its rapid production rate and natural occurrence in the sea, lowering production costs. Furthermore, consumption will rise due to low prices compared to diesel and petrol.

Bioethanol vs Conventional Fossil Fuels

| Parameter | Bioethanol | Conventional Fossil Fuels |

| Emissions | Produces lower greenhouse gas emissions during combustion and can reduce overall air pollutants when blended with gasoline. | Generates higher carbon dioxide, sulfur oxides, and other harmful emissions, contributing significantly to air pollution and climate change. |

| Renewability | Derived from renewable biomass sources such as corn, sugarcane, wheat, and agricultural residues, making it a sustainable fuel option. | Produced from finite petroleum reserves that require millions of years to form and are subject to depletion. |

| Carbon Footprint | Offers a lower lifecycle carbon footprint as feedstock crops absorb carbon dioxide during growth, partially offsetting emissions from fuel use. | Has a higher lifecycle carbon footprint due to extraction, refining, transportation, and combustion processes that release stored carbon into the atmosphere. |

| Energy Efficiency | Contains lower energy density than gasoline, resulting in slightly lower fuel economy, though modern engines can effectively utilize ethanol blends. | Provides higher energy density and generally delivers greater mileage per unit of fuel consumed. |

| Feedstock Sourcing | Produced from agricultural crops, organic waste, and cellulosic biomass, supporting diversification of energy resources and rural economies. | Extracted from crude oil reserves through drilling, exploration, and refining activities concentrated in specific geographic regions. |

| Environmental Impact | Supports reduced dependence on fossil fuels and can lower net emissions, though land use and water consumption concerns remain for some feedstocks. | Associated with habitat disruption, oil spills, resource depletion, and significant environmental impacts throughout extraction and refining operations. |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Know more about this report: Download Sample Report

Industry Dynamics

Growth Drivers

The primary driver for the global bioethanol market is government regulatory bodies encouraging production. Growing demand for blending in gasoline and increased government initiatives to produce and use greener fuels such as bio-ethanol are driving the market growth. Implementing stringent regulations has encouraged companies to focus on building better, cleaner, and less expensive energy. Technological advancements in the market have resulted in the development of second and third-generation bioethanol, which is expected to remain a viable prospect in the global market.

The factors driving the global bioethanol market are rising environmental concerns, which encourage manufacturers to produce bioethanol, blending mandates from regulatory bodies such as the EPA (Environmental Protection Agency), and abundant raw material availability.

Countries are focusing on energy security as demand for energy has increased significantly due to economic expansion, population growth, increased consumer income, and the discovery of new energy use. Many countries continue to import massive amounts of crude oil and could use it as a substitute for crude oil, thus, reducing their dependence. As a result, the increased focus on improving energy security is expected to provide lucrative opportunities for the global bioethanol oil market.

Report Segmentation

The market is primarily segmented based on feedstock, end-use, and region.

| By Feedstock | By End-Use | By Region |

|

|

|

Source: Polaris Market Research Analysis

Know more about this report: Download Sample Report

Feedstock Analysis

The segmentation, based on feedstock includes, cereals & starch, wheat, maize, beet, sugarcane, and others. Maize segment is expected to witness fastest growth at a CAGR of 14.4% during the forecast period owing to its easy availability and large-scale production. Most of the bioethanol generated in the United States is derived from starch-based crops and processed in a dry or wet mill. A dry milling process is created when maize is crushed into flour, fermented to make ethanol, and coupled with co-products such as distillers’ grains and carbon dioxide. Wet mills have maize sweeteners and ethanol, and a variety of by-products. Maize is separated into starch, protein, and fiber, then processed into products. Usage of maize mills is expected to grow globally, which will boost the bioethanol market's growth.

Source: Polaris Market Research Analysis

End Use Analysis

Based on end use, the segmentation, includes food & beverages, power generation, transportation, industrial, medical, and others. The transportation segment accounted for the largest market share of 57.0% in 2025.

The automotive and transportation industries utilize bio-ethanol as a fuel and fuel additive. It is used in conjunction with conventional petrol to fuel petrol engines in automotive. Bioethanol is less expensive and more environmentally friendly than petroleum. A small amount of bioethanol is mixed with pure gasoline to create blends, which burn more efficiently and emit no carbon dioxide. As a result, bioethanol fuel blends are required in many countries worldwide. This rising use of bioethanol in the transportation end-use market is thus driving its market towards growth.

Regional Analysis

North America Bioethanol Market Assessment

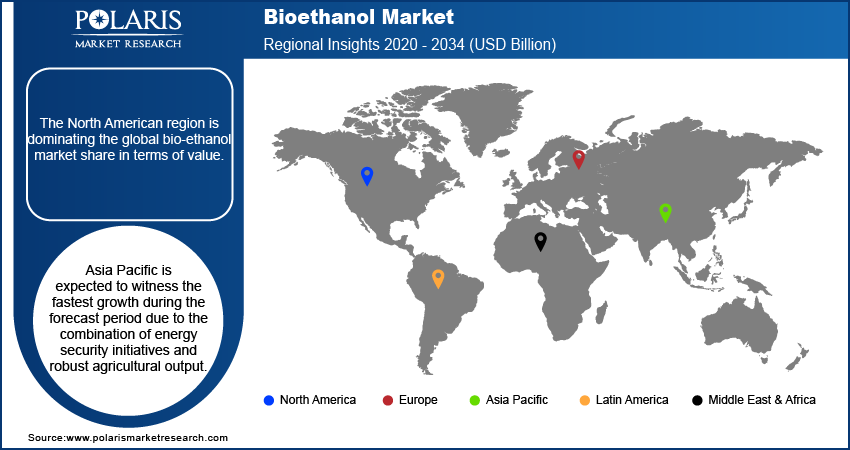

In 2025, the North American region is dominating the global bio-ethanol market share of 36.0% in terms of value. North America is one of the largest consumers of fuel in the world and uses different ethanol fuel blends. The United States is the largest producer and consumer of bioethanol worldwide, followed by Brazil, China, India, and Canada.

North America accounts for a significant share owing to increasing approvals and government backing for developing eco-friendly and sustainable fuels. Countries in this region have mandated using higher blends in vehicles. Bio-ethanol production has increased due to higher renewable fuel standard targets and growth in domestic motor gasoline consumption, which is now blended with 10% ethanol by volume. The enormous quantity of maize growing in North America has created an enticing and fertile economic environment for the region's bioethanol market.

Asia Pacific Bioethanol Market Insight

Asia Pacific is expected to witness the fastest growth at a CAGR of 15.3% during the forecast period due to the combination of energy security initiatives and robust agricultural output. The government in this region is establishing biofuel blending policies and initiatives with an aim to reduce dependence on imported fossil fuels to enhance energy independence and build strategic fuel reserves. This push creates a stable environment demand, with boosted investments in production capacity. Moreover, this region has an advantage due to the vast agricultural base, which provides cost-effective feedstock from sugarcane in tropical climates.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The competitive environment is characterized by focused investments in advanced feedstock processing to enhance yields and lessen reliance on food-grade products such as maize and sugarcane. Major vendor strategies focus on expansion opportunities in developing markets, across the Asia Pacific and Latin America where local government policies actually promote expansion to areas that have high agricultural residue to sell into value chains with large unfulfilled demand and opportunities. Insights and perspectives from industry leading firms suggest that technological advancement in both cellulosic and waste to energy conversion is a primary consideration for future supply chain alignment to competitive positioning and finding opportunities for joint ventures with energy majors and agribusiness firms. However, small to medium firms are having difficulty scaling due in part to high costs of capital and the disruption to supply chains because of feedstock price volatility.

Some of the key market players in the bioethanol market are Abengoa Bioenergy, Archer Daniels Midland, Bioethanol Japan Kansai Co Ltd, BlueFire Ethanol Fuels Inc., Cremer Oleo GmbH & Co., CropEnergies AG, Green Future Innovations Inc., Green Plains, Nordzucker AG, Petrobras Biocombustíveis, Raizen Energia, Royal Dutch Shell PLC, Soufflet Group, Tereos, and Valero Energy Corporation. These players are expanding their presence across various geographies and entering new markets in developing regions to expand their customer base and strengthen their presence in the market. The companies are also introducing new innovative products to cater to the growing consumer demands.

Industry Developments

March 2026: Bharat Petroleum Corporation Ltd. (BPCL) commissioned its second-generation (2G) bioethanol refinery at Bargarh, India. The facility produces 100 KL/day of fuel-grade bioethanol. It is produced from rice straw through pretreatment, fermentation, and advanced lignocellulosic technology. (Source: bharatpetroleum.in)

September 2025: India inaugurated its first bamboo-based bio-refinery at Numaligarh Refinery Limited (NRL) in Golaghat district, aiming to promote clean energy and reduce dependence on fossil fuels. (Source: pib.gov)

February 2025, BPCL and NSI partnered to develop sweet sorghum–based bioethanol, investing INR 5 crores to improve yields and support India’s ethanol program. (Source: prnewswire.com)

January 2025: ADVANTA and Baidyanath Biofuels signed an MoU to use maize hybrids for bioethanol production, supporting India’s 20% ethanol blending target. (Source: advantaseeds.com)

February 2025: Nippon Paper Industries Co., Ltd., Sumitomo Corporation, and Green Earth Institute Co., Ltd. collaborated to establish a joint venture company, Morisora Bio Refinery LLC, to focus on the production and sale of bioethanol and biochemicals derived from woody biomass. (Source: nipponpaper.com)

What is the Future of Bioethanol Market?

The future of the market is expected to be fueled by rising adoption of renewable fuels and expanding ethanol blending mandates. Also, supportive government policies promoting decarbonization will drive market expansion. Advancements in second-generation and cellulosic bioethanol technologies improve production efficiency and enable the utilization of non-food biomass feedstocks. Rising investments in sustainable transportation fuels and growing demand for low-carbon energy solutions will accelerate market growth. Countries are intensifying efforts toward carbon neutrality, energy security, and reduced dependence on fossil fuels. Thus, bioethanol is expected to emerge as a critical component of the global clean energy and low-carbon fuel ecosystem.

Bioethanol Market Report Scope

| Report Attributes | Details |

| Market size value in 2025 | USD 56.23 billion |

| Market size value in 2026 | USD 64.04 billion |

| Revenue forecast in 2034 | USD 184.24 billion |

| CAGR | 14.1% from 2026 - 2034 |

| Base year | 2025 |

| Historical data | 2021 - 2024 |

| Forecast period | 2026 - 2034 |

| Quantitative units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Segments covered | By Feedstock, By End Use Industry, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies | Abengoa Bioenergy, Archer Daniels Midland, Bioethanol Japan Kansai Co Ltd, BlueFire Ethanol Fuels Inc., Cremer Oleo GmbH & Co., CropEnergies AG, Green Future Innovations Inc., Green Plains, Nordzucker AG, Petrobras Biocombustíveis, Raizen Energia, Royal Dutch Shell PLC, Soufflet Group, Tereos, and Valero Energy Corporation |

Source: Polaris Market Research Analysis

Want to check out the bioethanol market report before buying it? Then, our sample report has got you covered. It includes key market data points, ranging from trend analyses to industry estimates and forecasts. See for yourself by Download Sample Report.

FAQ's

• The global market size was valued at USD 56.23 billion in 2025 and is projected to grow to USD 184.24 billion by 2034.

• The global market is projected to register a CAGR of 14.1% during the forecast period.

• North America dominated the global market with 36.0% share in 2025.

• A few market players are Abengoa Bioenergy, Archer Daniels Midland, Bioethanol Japan Kansai Co Ltd, BlueFire Ethanol Fuels Inc., Cremer Oleo GmbH & Co., CropEnergies AG, Green Future Innovations Inc., Green Plains, Nordzucker AG, Petrobras Biocombustíveis, Raizen Energia, Royal Dutch Shell PLC, Soufflet Group, Tereos, and Valero Energy Corporation.

• The transportation segment dominated the market with 57.0% share in 2025.

• The maize segment is expected to witness rapid growth at a CAGR of 14.4% during the forecast period.

Download Sample Report of bioethanol market

Please fill out the form to request a customized copy of the research report.