Blue Hydrogen Market Size, Share & Forecast Report, 2026 - 2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Blue Hydrogen Market Overview

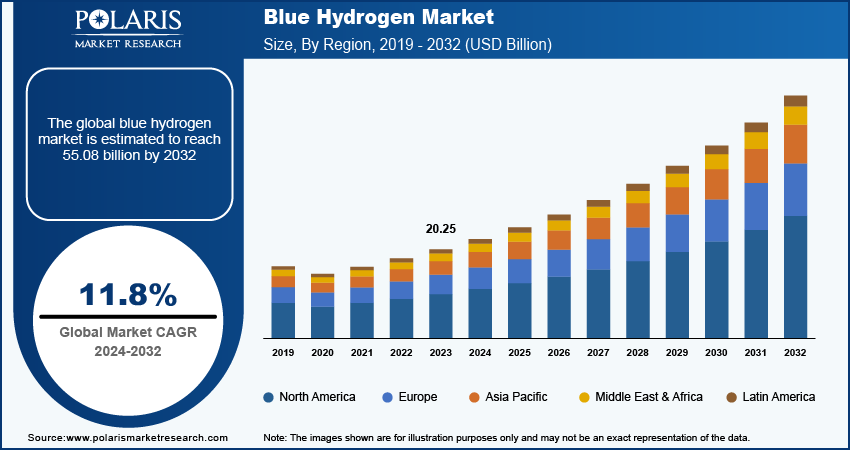

The global blue hydrogen market size was valued at USD 25.64 billion in 2025. The market is projected to exhibit a CAGR of 14.3% from 2026 to 2034. The market growth is primarily fueled by the growing global emphasis on reducing greenhouse gas emissions and advancing renewable energy sources.

Market Statistics

Key Takeaways

- North America accounted for the largest market share of 81.16% in 2025. This is due to the presence of substantial natural gas resources in the region.

- Europe is anticipated to witness the highest CAGR of 10.40% during the projection period. The region's strong commitment to achieving ambitious climate targets and lowering carbon emissions drives its robust growth.

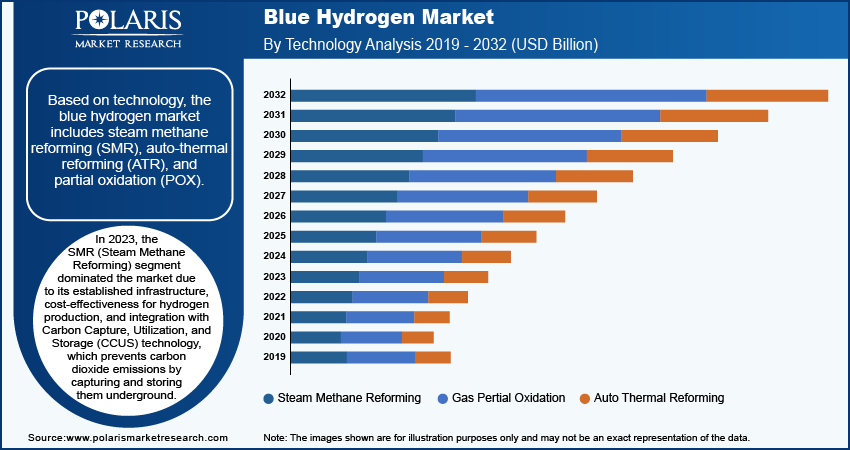

- The SMR segment accounted for the largest market share of 60.21% in 2025. This is owing to the ability of SMR technology to produce blue hydrogen that's free from greenhouse gas and carbon emissions.

- The power generation segment led with 45.10% market share in 2025. This is because blue hydrogen emits fewer greenhouse gases during operation.

- The refinery segment is anticipated to register the highest growth rate of 8.10% CAGR. The segment's growth is fueled by the implementation of sustainable methods by companies to meet their sustainability objectives.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The rising need for clean energy solutions and robust growth in fuel-cell electric vehicles are driving the market growth.

- The growing focus on achieving net zero emissions is fueling the demand for blue hydrogen, as it has the potential to play a crucial role in the decarbonization of the global energy system.

- The increasing emphasis on the usage of blue hydrogen for power generation is expected to create several market opportunities.

- Energy loss during hydrogen technology production may present market challenges.

AI Impact on Blue Hydrogen Market

- The use of AI in blue hydrogen production contributes to process optimization, including steam methane reforming and carbon capture operations.

- It is useful in making carbon capture operations more efficient through emission monitoring and problem identification.

- AI aids predictive maintenance, enabling the detection of machine malfunctions before significant losses are incurred in hydrogen facilities.

- It assists in managing energy consumption and operational expenses through data analysis.

To Understand More About this Research: Download Sample Report

Blue hydrogen provides a low-carbon alternative to conventional hydrogen production methods, which depend on fossil fuels and generate substantial greenhouse gas emissions. The blue hydrogen industry is witnessing remarkable growth owing to the rising need for clean energy solutions and captive investments in the sector. Governments worldwide are establishing ambitious emission reduction targets and investing in low-carbon technologies, including blue hydrogen. For instance, the European Union (EU) announced to reduce greenhouse gas emissions (GHGs) by nearly 55% by 2030. It is also making substantial investments in blue hydrogen as a crucial element of its energy transition strategy.

Government initiatives and regulations play a crucial role in driving the overall global market. To combat climate change and air pollution, governments worldwide are implementing policies that promote the use of low-carbon fuels, including hydrogen. Additionally, carbon pricing and taxes are being introduced to incentivize the shift toward low-carbon energy sources.

Renewable energy policies such as renewable portfolio standards (RPS) and feed-in tariffs are fueling the expansion of renewable sources such as wind and solar power. Blue hydrogen is generated using these renewable energy sources, minimizing its carbon footprint. To promote the adoption of blue hydrogen, governments are providing several incentives, which is further fueling industry expansion.

How Blue Hydrogen is Produced?

Blue hydrogen can be produced through steam methane reforming (SMR) or autothermal reforming (ATR). Here, natural gas is transformed to produce hydrogen and carbon dioxide. Then, a carbon capture technology is applied that helps in capturing most of the carbon dioxide and preventing it from being emitted into the air. Afterward, the carbon can be either disposed of underground or utilized for other purposes.

Market Dynamics

Rising Need for Clean Energy Solutions with Low Carbon Emissions

The blue hydrogen market is driven by the rising need for cleaner energy solutions and strong growth in fuel-cell electric vehicles. Fuel cell electric vehicles (FCEVs) are increasingly popular due to their low refueling and maintenance costs. Governments across the globe are promoting the adoption of such vehicles by offering favorable initiatives, such as tax rebates and subsidies. These efforts are designed to minimize carbon emissions and reduce reliance on fossil fuels. For instance, according to a report from vehicle technologies office, Hydrogen has the potential to deliver clean energy across various US economic sectors, including transportation, by significantly reducing greenhouse gas emissions from trucks, buses, planes, and ships. As a fuel and energy carrier, hydrogen powers vehicles through fuel cells without emitting harmful pollutants. It plays a vital role in lowering emissions from heavy-duty vehicles, which, though only 5% of vehicles on US roads, contribute over 20% of transportation-related emissions and are the largest source of mobile nitrogen-oxide emissions in the country.

Rising Focus on Net Zero Emissions

Under a net zero emissions scenario, hydrogen production undergoes a transformative shift. By 2030, global hydrogen output is expected to reach 200 million tonnes (Mt), with 70% generated through low-carbon technologies. By 2050, hydrogen production is anticipated to rise to 500 Mt, driven primarily by such methods. Achieving net zero emissions by 2050 will require extensive modifications to the energy system, utilizing a range of technologies. Moreover, blue hydrogen is expected to further play a crucial role in the decarbonization of the global energy system. The key pillars supporting this transition include renewable energy sources (solar, wind, and hydro) and carbon capture utilization and storage (CCUS). These elements collectively aim to reduce emissions and enhance energy sustainability by improving operational efficiency, transitioning to cleaner energy solutions, and leveraging advanced technologies like CCUS and blue hydrogen.

The International Renewable Energy Agency (IRENA) estimates that in a net zero emissions scenario, substantial growth in hydrogen demand, combined with cleaner production technologies, could avert up to 60 giga tonnes (Gt) of CO2 emissions from 2021 to 2050, contributing to around 6.5% of the total cumulative emissions reductions. Hydrogen fuel plays a crucial role in reducing greenhouse gas emissions in challenging-to-decarbonize sectors, such as heavy industry (especially steel and chemicals), heavy-duty transport, shipping, and aviation, where direct electrification faces significant limitations.

Blue Ammonia and Hydrogen Export Opportunities

The conversion of blue hydrogen into blue ammonia is becoming more common because blue ammonia is easier to store, handle, and transport than pure hydrogen. Many nations are developing blue ammonia plants, export terminals, storage facilities, and transportation logistics to facilitate global trade in hydrogen and energy cooperation. It can be noted that there is already an existing ammonia transportation system, making international commercialization easier within low-carbon energy markets. Moreover, blue ammonia is attracting interest for various applications such as electricity production, marine fuels, fertilizers, and energy systems for industries.

Blue Hydrogen vs Green Hydrogen vs Grey Hydrogen

| Feature | Blue Hydrogen | Green Hydrogen | Grey Hydrogen |

| Source of Production | Natural gas with carbon capture | Renewable energy electrolysis | Natural gas without carbon capture |

| Carbon Emissions | Low emissions | Lowest emissions | High emissions |

| Reliance on Renewable Energy | Partially | Entirely | Fossil fuel dependence |

| Infrastructure Availability | Strong existing infrastructure | Emerging infrastructure | Widely established |

| Cost to Produce | Medium | Higher currently | Low cost |

| Level of Sustainability | Transitory low carbon solution | Most sustainable | Least unsustainable |

Segment Insights

Market Evaluation by Technology Outlook

The global blue hydrogen market segmentation, based on technology, includes steam methane reforming (SMR), auto-thermal reforming (ATR), and gas partial oxidation (POX). In 2025, the SMR segment dominated the market with 60.12% share. In SMR technology, the carbon dioxide produced is not released into the atmosphere but is captured and stored underground through the Carbon Capture, Utilization, and Storage (CCUS) process. This approach results in the production of blue hydrogen, free from greenhouse gas and carbon emissions. SMR is recognized for its cost-effectiveness and energy efficiency in producing high-purity hydrogen. The projected rise in SMR adoption is expected to fuel growth during the forecast period.

Market Assessment by Application Outlook

The global blue hydrogen market, based on application, is segmented into chemicals, refinery, power generation, and others. The power generation segment held the largest revenue share of 45.10% in 2025. Approximately 96% of global hydrogen is produced from fossil fuels through a process known as reforming. In this process, the fuels are heated with steam to around 800°C. On the other hand, hydrogen fuel cell vehicles do not emit greenhouse gases during operation, which is anticipated to boost the demand for blue hydrogen in power generation and contribute to revenue growth.

The refinery segment is expected to register a substantial growth of CAGR 8.10% during the forecast period. To meet their sustainability objectives, key companies are implementing sustainable methods to manage the carbon dioxide produced during hydrogen generation. Petrochemical companies such as Exxon Mobil Corp. use steam methane reforming technology to produce hydrogen for their petroleum refineries. This shift allows them to transform grey hydrogen into blue hydrogen with zero carbon emissions.

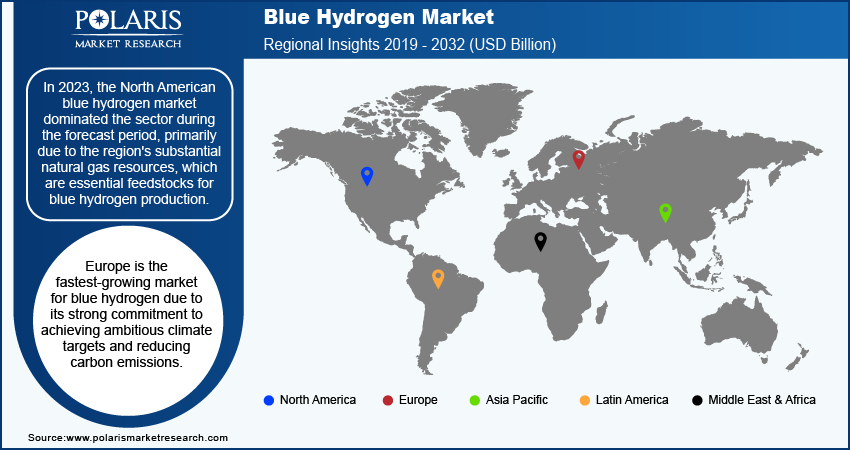

Regional Insights

By region, the study provides insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2025, the North American dominated the market with 81.16% share due to the region's substantial natural gas resources, which are essential feedstocks for blue hydrogen production. The United States, being the world’s largest natural gas producer as it provides a crucial feedstock for blue hydrogen production, allowing significant growth in low-carbon energy initiatives plays a pivotal role. Additionally, the growing demand for low-carbon energy in North America is driven by climate targets and increasing environmental concerns. Furthermore, California and New York, have set ambitious climate goals, while the Canadian government is committed to achieving net-zero emissions by 2050, further supporting the expansion in the region. For instance, in January 2023, the US government launched the Grannus Blue Ammonia and Hydrogen Project in Northern California. This initiative aims to produce 150,000 metric tons of blue ammonia and blue hydrogen annually.

Europe is expected to register fastest CAGR of 10.40% over the forecast period due to its strong commitment to achieving ambitious climate targets and reducing carbon emissions. The region has implemented supportive policies and substantial funding for low-carbon technologies, including hydrogen production integrated with carbon capture, utilization, and storage (CCUS). Additionally, Europe's focus on energy security and reducing reliance on imported fossil fuels drives investments in blue hydrogen as a cleaner energy alternative. For instance, according to a report by CSIS, in August 2020, the Russian government announced a roadmap to produce blue hydrogen in the country. The roadmap includes plans to invest around $127 million in developing technologies for the production, transportation, and storage of blue hydrogen.

Key Market Players and Competitive Insights

The competitive landscape is rapidly evolving, driven by strategic shifts informed by in-depth industry analysis focused on carbon mitigation and low-emission fuel alternatives. Stakeholders are leveraging targeted geographies expansion strategies to scale production capacities through investments in autothermal reforming (ATR) and steam methane reforming (SMR) with integrated carbon capture and storage (CCS) systems. The industry is witnessing a rise in joint ventures and strategic alliances between energy infrastructure companies and technology developers to accelerate the deployment of blue hydrogen projects and secure long-term offtake agreements. Several mergers and acquisitions are reshaping the value chain by aligning upstream natural gas assets with downstream hydrogen distribution networks.

Recent launches of demonstration-scale and commercial-scale blue hydrogen facilities signal a transition from pilot concepts to operational scalability. Post-merger integration efforts are centered around aligning CCS capabilities, optimizing syngas conversion efficiency, and consolidating hydrogen transportation networks. Technology advancements in CO₂ sequestration, process intensification, and low-NOx combustion systems are enhancing the environmental and economic viability of blue hydrogen production. As governments tighten decarbonization targets and incentivize low-carbon fuels, industry participants are aggressively positioning themselves through innovation, cross-sector collaboration, and infrastructure readiness, reinforcing the competitiveness of the blue hydrogen ecosystem.

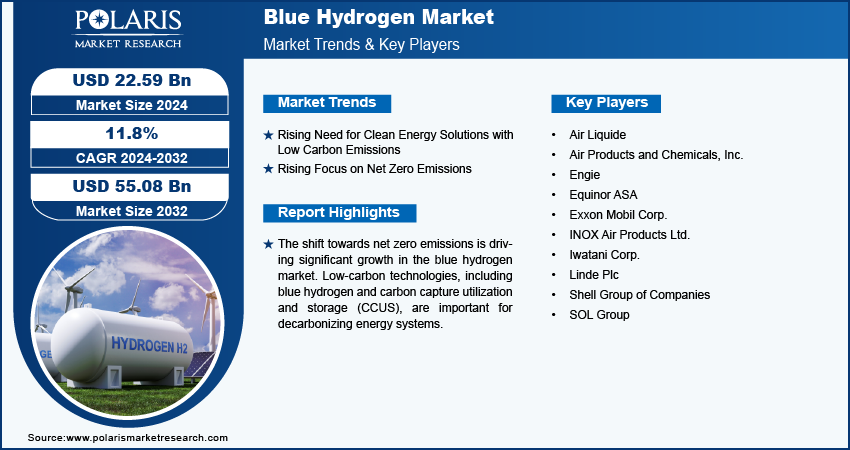

Linde Plc; Shell Group; Air Liquide; Air Products and Chemicals.; Engie; Equinor; SOL Group; Iwatani Corp.; INOX Air Products; and Exxon Mobil are among the major players in the blue hydrogen market.

Linde, an industrial gas supplier, operates in over 100 countries. Its primary products include atmospheric gases such as oxygen, nitrogen, and argon, as well as process gases such as hydrogen, CO2, and helium. The company also provides equipment for industrial gas production. Linde serves diverse end users, including chemicals, manufacturing, and steelmaking, and generated around USD 33 billion in revenue in 2023. In February 2023, Linde announced its plans to build a USD 1.8 billion blue hydrogen facility at Texas Gulf Coast to supply ammonia production. The company aims to commence production around 2025.

ExxonMobil is a global integrated oil and gas company involved in the exploration, production, and refining of oil. In 2023, it produced 2.4 million barrels of liquids and 7.7 billion cubic feet of natural gas/day. By the end of 2023, the company's reserves totaled 16.9 billion barrels of oil equivalent, with 66% being liquids. ExxonMobil is among the world's largest refiners, with a global refining capacity of 4.5 billion barrels of oil/day, and is also a manufacturer of commodity and specialty chemicals.

Key Companies

- Air Liquide

- Air Products and Chemicals, Inc.

- Engie

- Equinor ASA

- Exxon Mobil Corp.

- INOX Air Products Ltd.

- Iwatani Corp.

- Linde Plc

- Shell Group of Companies

- SOL Group

Industry Developments

April 2026: Air Liquide highlighted the development of its Normand’Hy project, a 200 MW PEM electrolyzer being constructed near Port-Jérôme-sur-Seine. The project is planned to be commissioned by 2026. It is designed for producing over 28,000 tonnes of low-carbon and renewable hydrogen annually. (source: airliquide.com)

December 2025: ENGIE confirmed its participation in the 2026 Hyvolution trade show in Paris. The company showcased its projects in low-carbon hydrogen and its applications in decarbonizing hard-to-abate sectors. (source: engie.com).

Segmentation

By Technology Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- Steam Methane Reforming

- Gas Partial Oxidation

- Auto Thermal Reforming

By Application Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- Chemicals

- Refinery

- Power Generation

- Others

By Transportation Mode Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- Pipeline

- Cryogenic Liquid Tankers

By Regional Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Blue Hydrogen Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 25.64 Billion |

| Market Size Value in 2026 | USD 27.11 Billion |

| Revenue Forecast in 2034 | USD 85.56 Billion |

| CAGR | 14.3% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Volume, Kilotons; Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

• The global blue hydrogen market size was valued at USD 25.64 billion in 2025 and is projected to grow to USD 85.56 billion by 2034.

The global market is projected to register a CAGR of 14.3% during 2026–2034.

In 2025, the North American blue hydrogen market dominated the market with 81.16% share, primarily due to the region's substantial natural gas resources, which are essential feedstocks for blue hydrogen production.

Key players in the market are Linde Plc, Shell Group, Air Liquide, Air Products and Chemicals., Engie, Equinor, SOL Group, Iwatani Corp., INOX Air Products, and Exxon Mobil.

The steam methane reforming segment dominated the market in 2025 with 60.12% share.

In 2025, the power generation segment accounted for the largest share of 45.10% in the global market.

Download Sample Report of Blue Hydrogen Market

Please fill out the form to request a customized copy of the research report.