Capsule Endoscopy Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Capsule Endoscopy Market Summary

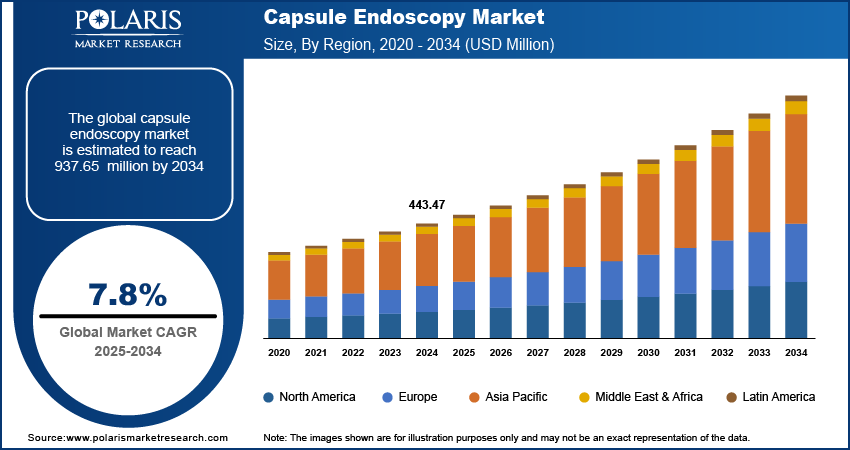

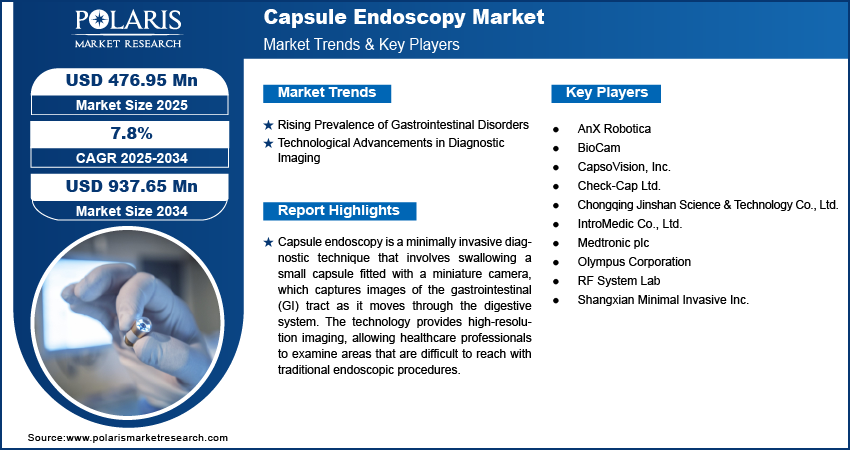

The capsule endoscopy market size was valued at USD 476.07 million in 2025, registering a CAGR of 7.8% from 2026 to 2034. The rising prevalence of gastrointestinal disorders fuels the need for innovative diagnostic tools. Additionally, increasing advancements in imaging technology have contributed to the market expansion.

Market Statistics

Key Takeaways

- The small bowel capsule endoscopy segment held the largest revenue share in 2025. The increasing adoption of minimally invasive diagnostic procedures for gastrointestinal disorders contributed to the dominance.

- The OGIB (Obscure GI Tract Bleeding) segment dominated revenue share in 2025. The dominance is primarily attributed to the shift toward capsule-based endoscopic screening over traditional methods.

- North America led the global market share in 2025. This dominance is fueled by the region's advanced healthcare infrastructure and a significant prevalence of gastrointestinal disorders.

- The Asia Pacific capsule endoscopy market is registering the highest CAGR during the forecast period. This growth is propelled by improving healthcare infrastructure and increasing healthcare expenditure.

Industry Dynamics

- The rising prevalence of GI disorders across the world boosts the growth of the capsule endoscopy industry.

- Increasing focus on technological advancements in diagnostic imaging is expected to drive the market growth is the coming years.

- Growing awareness about noninvasive screening methods has contributed to the rising demand for capsule endoscopy.

- Capsule retention risk and variability in reimbursement coverage restrain the market growth.

- Limited battery life and lack of real-time control hinder the expansion of the market.

AI Impact on Capsule Endoscopy Market

What AI Does?

- Artificial intelligence helps automatically triage normal vs abnormal studies. It enables physicians to prioritize high-risk cases.

- The technology uses deep-learning image recognition. It supports real-time lesion detection (bleeding, ulcers, polyps, tumors).

- It is used to filter redundant frames and highlight suspected pathology. Thus, AI use reduces reading time by 60–80%

- AI enhances diagnostic consistency as it minimizes inter-reader variability and fatigue-related errors.

- This technology facilitates structured reporting and automated severity scoring. It helps healthcare experts make faster clinical decisions.

What are AI Adoption Barriers?

- It requires large, clinically validated datasets to comply with regulatory and medico-legal standards.

- Integration challenges with existing hospital PACS, EMR, and endoscopy reporting systems are significant.

- High costs for software licenses and IT infrastructure make it hard for small GI centers to adopt these systems.

- "Black-box" algorithms and concerns about liability lead to trust issues among physicians.

Why AI Changes Market Economics?

- Increases case throughput per physician, improving ROI for capsule platforms.

- Reduces specialist reading time, which lowers labor costs.

- Enables scalable tele-gastroenterology and centralized reading hubs.

- Makes capsule endoscopy more competitive with traditional endoscopy for screening and monitoring.

To Understand More About this Research: Download Sample Report

What is Capsule Endoscopy? How Does it Work?

Capsule endoscopy, which is also called video capsule endoscopy or wireless capsule endoscopy, is a minimally invasive diagnostic procedure. This technique uses a small, swallowable capsule that has a camera. It captures high-resolution images of the gastrointestinal system. The images help detect conditions such as ulcers, polyps, and internal bleeding. It is used to visualize the gastrointestinal tract, particularly the small intestine areas, which are difficult to assess using conventional endoscopy. The procedure supports early detection. It monitors gastrointestinal (GI) diseases by enabling detailed imaging without sedation. Thus, demand for minimally invasive GI diagnostics across hospitals and diagnostic centers boosts the capsule endoscopy industry growth.

Capsule endoscopy’ can provide a painless and efficient alternative to traditional endoscopic methods. It improves patient comfort and diagnostic precision. Healthcare providers look for better solutions for early disease detection. As a result, the demand for capsule endoscopy is high in hospitals, diagnostic centers, and specialty clinics. Supportive government initiatives and growing healthcare expenditures boost the capsule endoscopy adoption. Also, the industry growth is fueled by the rising adoption of telemedicine. The market is expected to witness steady growth in the coming years with continuous research and development efforts aimed at improving capsule design and functionality.

Capsule Endoscopy vs Colonoscopy vs Upper Endoscopy vs CT/MR Enterography

| Parameter | Capsule Endoscopy | Colonoscopy | Upper Endoscopy (EGD) | CT / MR Enterography |

| Primary Anatomical Reach | Entire small bowel (mucosal surface) | Colon + terminal ileum | Esophagus, stomach, duodenum | Small bowel wall + extraluminal structures |

| Key Use Cases | Obscure GI bleeding, small-bowel Crohn’s, celiac disease, tumors, iron-deficiency anemia | Colorectal cancer screening, IBD, polyps, bleeding | Upper GI bleeding, GERD complications, ulcers, malignancy | Crohn’s disease extent, strictures, fistulas, abscesses, tumors |

| Invasiveness | Non-invasive (swallowed capsule) | Invasive, endoscopic | Invasive, endoscopic | Non-invasive imaging |

| Typical Clinical Setting | Outpatient; ambulatory | Endoscopy suite/hospital | Endoscopy suite/hospital | Radiology department |

| Preparation | Fasting + bowel prep | Full bowel prep + sedation | Fasting + sedation | Fasting + oral/IV contrast |

| Key Limitations | No tissue sampling, passive movement, incomplete exams, retention risk | Sedation risk, perforation, discomfort | Limited to upper GI, sedation risk | Radiation (CT), contrast risks, lower mucosal sensitivity |

| Typical Risks | Capsule retention, obstruction (in strictures) | Bleeding, perforation, anesthesia risks | Bleeding, perforation, anesthesia risks | Radiation exposure (CT), contrast allergy, nephrotoxicity |

| Visualization Strength | Excellent small-bowel mucosal detail | High-resolution colon mucosa | High-resolution upper GI mucosa | Excellent bowel wall + extra-intestinal disease |

| Patient Comfort | High | Moderate–low | Moderate | High |

| Market Role / Strength | Expands small-bowel diagnostics; screening adjunct | Gold standard for colon pathology | Gold standard for upper GI disorders | Disease staging and complication assessment |

| Typical B2B Buyers | GI clinics, diagnostic centers, hospitals | Hospitals, GI centers | Hospitals, GI centers | Hospitals, imaging centers |

Market Dynamics

Capsule Endoscopy Market Drivers

Rising Prevalence of Gastrointestinal Disorders

The increasing incidence of gastrointestinal (GI) disorders, such as Crohn's disease, celiac disease, and obscure gastrointestinal bleeding, has significantly heightened the demand for advanced diagnostic tools like capsule endoscopy. According to a 2022 report by the National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK), approximately 60 to 70 million people in the United States are affected by digestive diseases, underscoring the widespread nature of these conditions. Capsule endoscopy offers a non-invasive, patient-friendly alternative to traditional endoscopic procedures, enabling comprehensive visualization of the small intestine, which is challenging to assess with conventional methods. This capability is particularly crucial for diagnosing conditions such as obscure GI bleeding, where the source of bleeding is not identified through standard endoscopy or colonoscopy. The ability of capsule endoscopy to provide detailed images of the entire small bowel improves diagnostic accuracy, facilitating timely and appropriate therapeutic interventions. Capsule endoscopy improves diagnostic yield in small bowel evaluation, which supports higher utilization in GI diagnostics pathways. Thus, the escalating prevalence of GI disorders directly contributes to the market growth.

Technological Advancements in Diagnostic Imaging

Growing advancements in medical imaging technology improve the efficacy and applicability of capsule endoscopy. Modern capsules are equipped with high-resolution cameras, extended battery life, and enhanced data transmission capabilities. They allow for more precise and thorough examination of the gastrointestinal tract. A 2023 study published in the Journal of Gastrointestinal and Liver Diseases highlighted a development of capsules that have adjustable frame rates and better illumination. This greatly improves image quality and diagnostic results. Further, advancements in capsule endoscopy software algorithms are increasing. These innovations in image analysis lead to easy interpretation. They cut down the time doctors spend reviewing the large amounts of data created during the procedure. These technological improvements boost the diagnostic accuracy of capsule endoscopy. They also expand its uses, making it a more flexible tool for detecting and monitoring various GI issues. These advances support better integration with AI in capsule endoscopy. This helps doctors concentrate on key images and reduce their workload. As these innovations continue to develop, they play a key role in driving market demand.

Rising demand for non-invasive screening and outpatient diagnostics

Increasing emphasis on early detection and outpatient-friendly GI testing supports the capsule endoscopy adoption. It is particularly used in settings where sedation-based procedures are constrained by patient preference, capacity limitations, or procedural costs. There is a rising focus on expanding access to noninvasive GI screening and improving patient compliance. Thus, capsule endoscopy is increasingly positioned as a patient-centered option within gastrointestinal endoscopy devices and GI diagnostics pathways.

Capsule Endoscopy Market Restraint

Capsule Retention Risk and Variability in Reimbursement Coverage

The risk of capsule retention, particularly in patients with suspected strictures or bowel obstruction, hinders the capsule endoscopy demand. In addition, there is a volatility in capsule endoscopy reimbursement levels and coverage criteria across countries. It can adversely influence provider adoption and procedural volumes. Thus, inconsistency in capsule endoscopy reimbursement and rising concerns on capsule retention risks restrain the market growth.

Segmental Insights

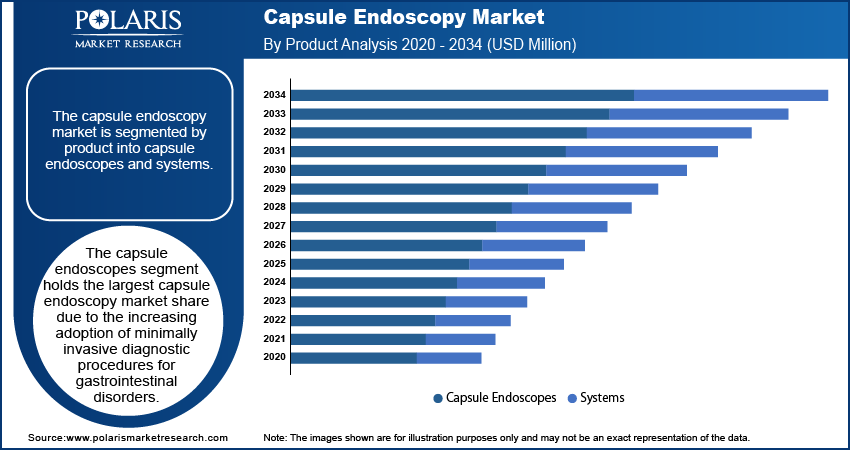

By Product

The market segmentation, based on product, includes small bowel capsule, colon capsule, esophagus capsule, specialized capsules, and others. The small bowel capsule endoscopy segment dominated the market in 2025. The dominance is driven by the increasing prevalence of obscure gastrointestinal bleeding, Crohn’s disease, and iron-deficiency anemia. Hospitals and diagnostic centers are increasingly choosing small bowel capsules as the first option for mid-GI evaluation. Their preference is growing because these capsules are noninvasive and provide better mucosal images. The use of AI-based reading software improves diagnostic efficiency and broadens screening applications. It strengthens clinical adoption across developed and emerging healthcare markets.

By Application

The capsule endoscopy industry is segmented by application into OGIB (Obscure GI Tract Bleeding), Crohn’s disease, small intestine tumor, and others. The OGIB (Obscure GI Tract Bleeding) segment led the revenue share in 2025. This dominance is attributed to the increasing utilization of capsule endoscopy for diagnosing obscure gastrointestinal bleeding. It offers real-time visualization and comprehensive assessment of the small intestine. The shift toward capsule-based endoscopic screening from traditional methods boost the segment dominance.

Regional Analysis

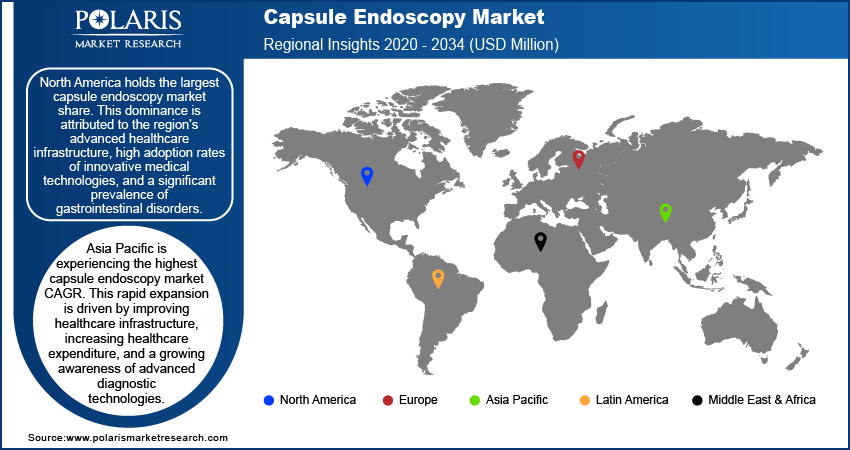

By region, the study provides the industry insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America held the largest market share in 2025. The region's dominance is fueled by its advanced healthcare infrastructure and high adoption rates of innovative medical technologies. Additionally, the presence of leading medical device manufacturers and ongoing research and development activities drive the North America capsule endoscopy market. Rising use of advanced GI diagnostic procedures and strong reimbursement for capsule endoscopy drive North America's leadership. The high use of capsule endoscopy in monitoring inflammatory bowel disease supports market growth. In the U.S., the established healthcare system and broad insurance coverage promote the widespread use of capsule endoscopy for diagnosing conditions like Crohn's disease and obscure gastrointestinal bleeding.

Asia Pacific is experiencing the highest market CAGR. Improving healthcare infrastructure and increasing healthcare expenditure boost the Asia Pacific capsule endoscopy market CAGR. Growing awareness of new diagnostic technologies is driving market growth in the region. Government efforts to improve healthcare access and quality, along with more people choosing minimally invasive procedures, are increasing market demand. The growth of private hospital networks and better gastroenterology facilities is boosting development in Asia Pacific. The rising need for minimally invasive GI diagnostics in densely populated countries also raises the demand for capsule endoscopy. Countries like China and India, with their large populations and increasing cases of gastrointestinal diseases, offer significant opportunities for industry players.

Key Players and Competitive Insights

The capsule endoscopy industry features several prominent companies actively offering relevant products. Key players include Medtronic plc; Olympus Corporation; CapsoVision, Inc.; IntroMedic Co., Ltd.; Chongqing Jinshan Science & Technology (Group) Co., Ltd.; Check-Cap Ltd.; RF System Lab; BioCam; Shangxian Minimal Invasive Inc.; and AnX Robotics.

The competitive landscape of the market is characterized by continuous innovation and strategic initiatives among companies. Firms are increasingly investing in R&D activities to improve image quality and enhance battery performance. They also focus on improving data transmission in their products. Players in the capsule endoscopy industry use different strategies, including collaborations, partnerships, and expanding into new regions. These efforts help them strengthen their presence in the market and meet the rising demand for noninvasive diagnostic solutions. They also improve physician workflow with reading software and expand pediatric uses through regulatory approvals, as shown by recent FDA approvals in 2024 and 2025.

List of Key Companies

- AnX Robotica

- BioCam

- CapsoVision, Inc.

- Check-Cap Ltd.

- Chongqing Jinshan Science & Technology (Group) Co., Ltd.

- IntroMedic Co., Ltd.

- Medtronic plc

- Olympus Corporation

- RF System Lab

- Shangxian Minimal Invasive Inc.

Capsule Endoscopy Industry Developments

- January 2025: CapsoVision received U.S. FDA clearance for its CapsoCam Plus. It is approved for pediatric patients aged two and older. This milestone provides a noninvasive and comfortable diagnostic alternative. It minimizes the stress of traditional capsule endoscopy procedures for children.

- January 2024: AnX Robotics secured US FDA clearance for expanded indications of its NaviCam Small Bowel Video Capsule Endoscopy (SB), allowing its use in children aged two and above, as well as adults.

Capsule Endoscopy Market Segmentation

By Product Outlook (Revenue-USD Million, 2021–2034)

- Small Bowel Capsule

- Colon Capsule

- Esophagus Capsule

- Specialized Capsules

- Others

By Application Outlook (Revenue-USD Million, 2021–2034)

- OGIB (Obscure GI Tract Bleeding)

- Crohn’s Disease

- Small Intestine Tumor

- Others

By End Use Outlook (Revenue-USD Million, 2021–2034)

- Hospitals

- Ambulatory Surgery Centers

- Others

By Type Outlook (Revenue-USD Million, 2021–2034)

- Capsule Cystoscopies

- Capsule Neuro-Endoscopes

By Regional Outlook (Revenue-USD Million, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- Suth Korea

- Indnesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- Suth Africa

- Rest of Middle East & Africa

- Latin America

- Mexic

- Brazil

- Argentina

- Rest of Latin America

Capsule Endoscopy Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 476.07 million |

| Market Size in 2026 | USD 511.48 million |

| Revenue Forecast in 2034 | USD 935.89 million |

| CAGR | 7.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD million, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global capsule endoscopy market was valued at USD 476.07 million in 2025. It is projected to reach USD 935.89 million by 2034, registering 7.8% CAGR.

North America led the market in 2025, driven by advanced healthcare infrastructure and high GI disorder prevalence.

The obscure GI tract bleeding (OGIB) segment dominated revenue share in 2025, followed by Crohn's disease detection, small bowel tumor identification, celiac disease screening, and polyp detection applications.

A few major players include Medtronic, Olympus Corporation, CapsoVision, IntroMedic, and JINSHAN Science & Technology, RF Co., Ltd.

AI image analysis, high-definition imaging, long battery life, wireless data transmission, cloud integration, and telemedicine compatibility are revolutionizing how capsule endoscopy improves diagnosis and accessibility.

Patients swallow a pill-sized camera capsule. The capsule captures thousands of images while traveling through the digestive tract over 8-12 hours, then naturally passes out.

Capsule endoscopy costs range from USD 500 to more than USD 2,000. Factors such as region, facility type, insurance coverage, and device technology influence the costs.

Capsule endoscopy shows a diagnostic accuracy of 48 to 89% for small bowel disorders. It is more effective to detect bleeding sources, Crohn's disease lesions, and tumors than traditional methods.

Capsule retention (1-3% of cases) is a primary risk. It occurs when the capsule becomes lodged in strictures or obstructions. It requires endoscopic or surgical removal.

Retention and safety are major concerns of capsule endoscopy. Thus, patients having suspected intestinal obstruction, strictures, dysphagia, pacemakers, pregnancy, severe gastroparesis, or swallowing disorders must avoid capsule endoscopy.

Capsule endoscopy is noninvasive, painless procedure. It visualizes the entire small intestine, requires no sedation, and cannot take biopsies. However, colonoscopy allows tissue sampling and polyp removal.

Download Sample Report of Capsule Endoscopy Market

Please fill out the form to request a customized copy of the research report.