Catalyst Market Demand, Global Analysis Report, 2026-2034

REPORT DETAILS

Catalyst Market Summary

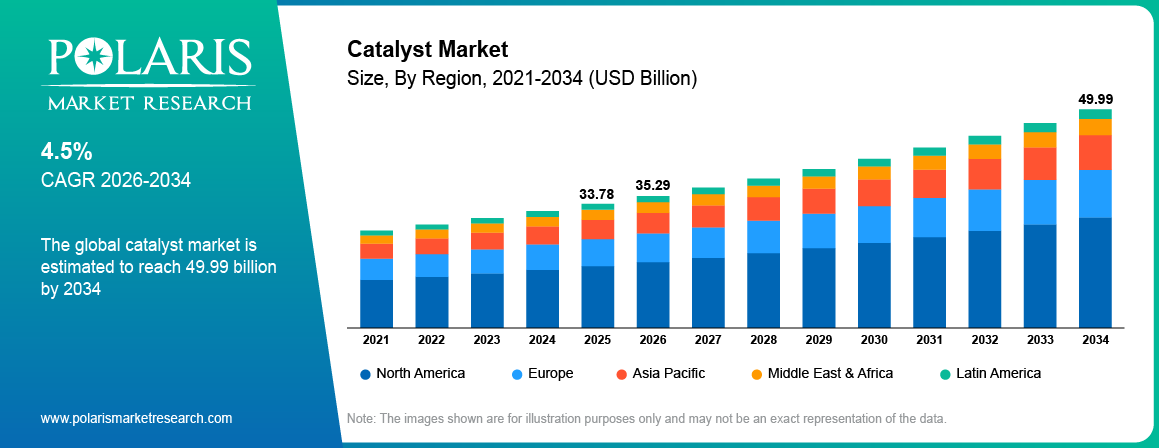

The catalyst market size was valued at USD 33.78 billion in 2025 and is expected to register a CAGR of 4.5% from 2026 to 2034. Rapid industrialization across the world drives the demand for catalysts. The rising requirement for high-performance catalysts is expected to grow as global fuel consumption rises.

Market Statistics

Key Takeaways

- As per our catalyst industry outlook, Asia Pacific accounted for a major market share of 36.42% in 2025. Rapid industrialization, expanding petrochemical capacity, and increasing demand from the automotive and refining sectors boost the leading position.

- The catalyst industry in North America is expected to expand at a 3.4% CAGR in the coming years. The rigorous environmental regulations and the strong automotive and industrial base fuel the growth.

- Heterogeneous catalysts accounted for a 73.2% share in the market in 2025, due to their wide range of applications and high efficiency along with easy separation from reaction mixtures.

- The recycling segment had the largest market share with 35.7% revenue contribution in 2025, owing to its lower cost and compliance requirements with regulations.

- The homogeneous catalyst segment has shown steady growth at 5.1% CAGR during the forecast period, due to their better selectivity and efficiency.

Industry Dynamics

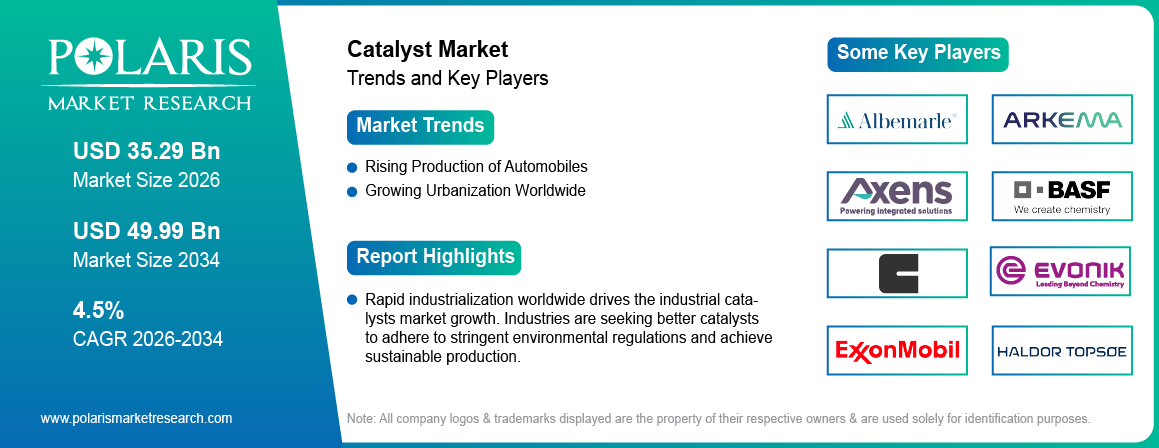

- Automobile manufacturers integrate catalytic converters into vehicle exhaust systems to comply with stringent environmental regulations. Hence, the rising production of automobiles boosts the expansion of the catalyst market.

- Urbanization pushes governments and industries to build more infrastructure. This includes power plants, refineries, chemical manufacturing, and public transportation systems. These infrastructures depend a lot on catalytic processes to cut down environmental impact and meet regulations. Therefore, rapid urbanization worldwide propels industry expansion.

- It is complex and costly to remove catalyst from the reaction mixture, which hinders the market growth.

- The rising development of environmentally friendly catalysts, due to the imposition of stringent laws, is expected to offer lucrative opportunities during the forecast period.

- The growing use of nanocatalysts for better efficiency is driving market growth.

- Bio-based catalysts, low-temperature catalysts, and recyclable catalyst systems are becoming popular as industries aim for long-term sustainability.

- Green catalysts promote cleaner, more energy-efficient, and sustainable chemical processes. Increasing environmental regulations and industry pressure to lower emissions, waste, and harmful by-products create a strong demand for green catalysts.

AI Impact on Catalyst Market

- AI in catalyst design: Artificial intelligence (AI) accelerates catalyst discovery by simulating reaction pathways, predicting active sites, and optimizing compositions. It significantly reduces trial-and-error experimentation and time-to-market.

- Machine learning catalysts: Machine learning models examine large datasets of experiments and materials. They predict catalysts' performance, stability, and selectivity. This method helps identify effective catalysts quickly for specific applications.

- Catalyst R&D automation: Automation combines robotics, AI, and high-throughput screening to run multiple experiments at once, test formulations quickly, and produce consistent data. This is improving R&D efficiency while lowering development costs.

- HTS platforms automate characterization, synthesis, and performance testing. This is dramatically speeding up development cycles.

Rapid industrialization worldwide drives the industrial catalysts market growth. Industries are seeking better catalysts to adhere to stringent environmental regulations and achieve sustainable production. Sectors such as petroleum refining, pharmaceuticals, and chemical manufacturing use catalysts to boost output, cut energy consumption, and decrease costs. Moreover, emerging economies are funding large industrial projects that require catalysts to improve processes and maintain competitive production rates. Therefore, global industrialization is fueling the growth of the catalyst industry.

The demand for catalysts is rising due to increased fuel consumption worldwide. Catalysts help break down heavy hydrocarbons into lighter, more valuable fuels. This process helps refineries keep up with the growing demand for fuel. Fuel producers use better catalysts to adhere to stricter environmental rules. These catalysts lower sulfur and other harmful emissions. This change leads to cleaner-burning fuels. As a result, the growing need for fuels increases the demand for high-performance catalysts.

Catalyst use is enabling efficient chemical reactions across many sectors. It improves reaction efficiency and lowers energy use. The process also helps comply with stringent environmental standards. Catalysts are used across the petroleum refining, petrochemical, environmental protection, pharmaceutical, and polymer manufacturing industries. Thus, catalysts have become an essential part of modern industrial processes.

Industries are moving toward cleaner fuels, circular manufacturing, and energy-efficient production. Thus, the demand for advanced and sustainable catalyst technologies is increasing.

Source: Polaris Market Research Analysis

How Do Catalysts Work in Chemical Reactions?

Catalysts are materials that speed up the rate of a chemical reaction without changing the end products. This happens by reducing the activation energy required to activate the chemical reaction. All the molecular processes require energy in order to break and re-form new bonds. The catalysts reduce this energy requirement and allow for rapid reaction even at lower temperatures. Also, the catalysts are never consumed during this reaction.

For instance, in petroleum refining, catalysts accelerate the process of breaking down heavy hydrocarbon chains into lighter molecules, which include gasoline and diesel. In automobiles, catalytic converters employ catalysts to convert toxic compounds, including carbon monoxide and nitrogen oxides, into less harmful substances. Through enhancing the rate of reactions and optimizing energy efficiency, catalysts have a significant impact on the production of chemicals and industries.

Applications of Catalysts Across Industries

Catalysts have great importance in different industries. They increase reaction rates, conserve energy consumption, and comply with regulations.

- Oil Refining/Petrochemical Industry – Catalysts are applied in cracking, hydrotreating, and reforming to transform crude oil into fuel products or chemicals.

- Environmental Purification – Catalysts are applied in reducing emissions from vehicles by means of catalytic converters. Catalysts also purify water and air.

- Polymers/Chemicals Manufacturing – Catalysts control the rate of polymer formation and other reactions, for example, oxidation or hydrogenation.

- Pharmaceutical Industry – Catalysts have applications in the manufacturing of APIs.

Benefits vs Challenges of Catalysts

| Factor | Advantages | Challenges |

| Efficiency | Increases reaction rate and decreases energy consumption | Catalyst degradation with time lowers its efficiency |

| Cost | Cuts down costs with higher productivity | High start-up costs, particularly for noble metals used as catalysts |

| Sustainability | Facilitates cleaner production with fewer emissions and waste products | Difficult to recycle or recover some catalysts |

| Scalability | Enhances capability for mass manufacturing | Challenges in scaling up for certain catalysts owing to difficulties in separation |

Source: Polaris Market Research Analysis

Catalyst Market Drivers

Rising Production of Automobiles

Automobile manufacturers are increasingly adding catalytic converters to vehicle exhaust systems. It helps them comply with strict environmental regulations. These converters use catalysts made from platinum, palladium, and rhodium to turn toxic gases into less harmful substances. Improvements in automotive technology and the demand for cleaner, more efficient engines increase the need for high-performance catalysts. Also, the move toward hybrid vehicles, which still use combustion engines, drives the need for efficient catalysts. Therefore, the need for catalysts made from precious metals is increasing as more vehicles are produced globally. The European Automobile Manufacturers' Association stated the production of 85.4 million motor vehicles around the world in 2022, an increase of 5.7% compared to 2021. Hence, the rising production of automobiles boosts the catalyst market expansion.

Growing Urbanization Worldwide

Urbanization pushes governments and industries to develop infrastructure. It propels the development of power plants, refineries, chemical manufacturing, and public transportation systems. These infrastructures depend on catalytic processes. These processes help lower environmental impact and meet regulatory standards. Urban centers generate more waste and emissions. It creates a need for better pollution control technologies. To tackle these problems, municipalities invest in cleaner energy production and stricter emission controls, both of which rely on effective catalytic systems. Moreover, rising vehicle ownership and construction in urban areas increase the demand for catalysts used in exhaust treatment and the production of cleaner fuels and materials. The United Nations Development Programme stated in 2024 that cities host more than half of the global population, and this number is expected to double by 2050. This rapid urban growth is creating a sustained need for catalytic solutions that support sustainable development while maintaining industrial efficiency.

Catalyst Market Restraints

Complex Catalyst Recovery

It is complex and costly to remove the catalyst from the reaction mixture. Homogeneous catalysts dissolve in the reaction medium. It makes separation complex and requires additional downstream purification steps such as filtration, extraction, or distillation. These processes increase operational costs, energy consumption, and processing time. They also increase the risk of losing catalysts and contaminating final products. Stringent purity requirements restricts the reuse of catalysts and hinders process efficiency and sustainability. Catalyst deactivation, contamination, and recovery issues increase operational costs. High costs adversely impact the strategies of small and mid-sized chemical manufacturers. Consequently, complex catalyst recovery prevents widespread adoption in cost-sensitive markets.

Regulatory & Sustainability Framework

- Environmental regulations: The EPA, EU REACH, and China MEE impose stringent emission standards. It drives the need for catalysts in refining, chemicals, and emission control.

- Sustainability push: Regulations support catalysts that reduce energy use, improve selectivity, and minimize waste.

- Hazardous material controls: The regulations on toxic and heavy metals like chromium and cadmium influence the development of environmentally friendly and biobased catalysts.

- Circular Economy: It promotes catalysts recycling, precious metal recovery, and regeneration services.

- ESG compliance: The end-users require lifecycle assessments, carbon footprint analysis, and sustainably sourced raw materials.

Source: Polaris Market Research Analysis

Segment Insights

Market Evaluation by Product

Based on the product, the market is divided into heterogeneous catalysts and homogeneous catalysts. The heterogeneous catalyst segment held the largest share of the global catalyst market in 2025 due to its broad industrial use, efficiency, and easy separation from reaction mixtures. Areas such as oil refinery, production of chemicals, and conservation of the environment use heterogeneous catalysts. Heterogeneous catalysts perform well even under challenging conditions and are inexpensive to replace. Fluid cracking process and hydrotreatment process have applications in both fuel production and pollutant removal. These processes primarily employ these catalyst types. Besides, the ever-growing energy consumption, along with more stringent environmental protection laws, has compelled refiners to use more effective, greener catalytic systems. This shift has raised the demand for heterogeneous catalysts.

The homogeneous catalysts segment is expected to grow rapidly in the coming years. This growth is due to their better selectivity and efficiency in fine chemical and pharmaceutical synthesis. Unlike mixed alternatives, these catalysts operate in the same phase as the reactants. This setup allows for precise molecular interactions and higher yields in complex reactions. The pharmaceutical industry is investing heavily in high-performance catalytic systems. This investment seeks to meet the growing demand for enantiomerically pure compounds and active pharmaceutical ingredients. Better ligand design and more stable metal complexes also increase the use of homogeneous catalysts. These factors make them an essential part of the next generation of chemical processes.

Heterogeneous Vs Homogeneous Catalysts Based on Cost, Scalability, Operational Efficiency, and Compliance Considerations

| B2B Decision Parameter | Heterogeneous Catalysts | Homogeneous Catalysts |

| Procurement cost structure | Higher upfront capex, lower lifecycle cost | Lower initial cost, higher ongoing operating cost |

| Catalyst recovery & reuse | Easy recovery; supports multiple reuse cycles | Difficult recovery; frequent replenishment needed |

| Operating cost (OPEX) | Lower due to simpler separation and reuse | Higher due to purification and catalyst loss |

| Process integration | Easy integration into continuous processes | Better suited for batch or semi-batch processes |

| Scale-up feasibility | Highly scalable for industrial production | Scale-up constrained by separation complexity |

| Production downtime | Minimal, predictable maintenance cycles | Higher downtime due to cleaning and separation steps |

| Regulatory & compliance risk | Lower risk due to minimal residuals | Higher risk from trace catalyst contamination |

| Supply chain reliability | Stable, bulk supply availability | Often dependent on specialty or precious metals |

| Sustainability metrics | Lower waste generation, better recyclability | Higher solvent use and waste intensity |

| Target end-user industries | Refining, petrochemicals, polymers, bulk chemicals | Pharmaceuticals, agrochemicals, fine chemicals |

Source: Polaris Market Research Analysis

Market Insight by Process

In terms of process, the market is segregated into recycling, regeneration, and rejuvenation. The recycling segment held a large market share in 2025 because it was cost-effective, met regulations, and focused on sustainable industrial practices. Industries, especially oil refining and chemical manufacturing, increasingly used recycling methods to recover valuable metals like platinum, palladium, and rhodium. These metals are crucial for catalytic activity and experienced significant price fluctuations and supply chain issues. This situation led manufacturers to invest in closed-loop recycling systems. Furthermore, strict environmental regulations in North America and Europe urged companies to reduce waste and emissions, making recycling even more attractive.

Technology Roadmap for the Catalyst Market: Evolution of AI-Driven Design, Nanostructured Materials, and Green Catalysts Across Short-, Mid-, and Long-Term Horizons

The technology roadmap shows a clear transition from efficiency-driven innovation (short term) to autonomous, circular, and carbon-neutral catalysis (long term). It aligns catalyst development with regulatory pressure, sustainability goals, and advanced manufacturing needs.

| Technology Area | Short-Term (1–3 Years) | Mid-Term (3–5 Years) | Long-Term (5–10 Years) | Market Impact |

| AI & Digital Catalysis | AI-driven catalyst screening, ML-based performance prediction, automated lab testing | Generative AI for catalyst design, digital twins for reactors, scale-up optimization | Autonomous self-learning labs, multiscale AI models linking atom-level design to plant performance | Faster R&D cycles, lower development costs, and higher process efficiency |

| Nanotechnology & Advanced Materials | Nanoparticle catalysts, core–shell structures, MOFs, mesoporous supports | Single-atom catalysts (SACs), hierarchical pore structures, improved mass transfer | 2D materials, quantum-effect catalysts, integrated nano-systems for energy conversion | Higher activity, better selectivity, and reduced precious metal usage |

| Green & Sustainable Catalysts | Shift to earth-abundant metals, biomass-compatible catalysts, lower-toxicity formulations | Bioinspired & enzymatic hybrids, water/CO₂-based reaction systems | Carbon-neutral catalysts enabling CO₂ conversion, fully recyclable catalyst lifecycles | Regulatory compliance, lower carbon footprint, and ESG-driven adoption |

| Circular & Lifecycle Innovation | Catalyst regeneration and recovery technologies | Design-for-recycling catalysts, improved metal recovery | Closed-loop catalyst ecosystems with minimal waste | Cost reduction, supply security, and sustainability leadership |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

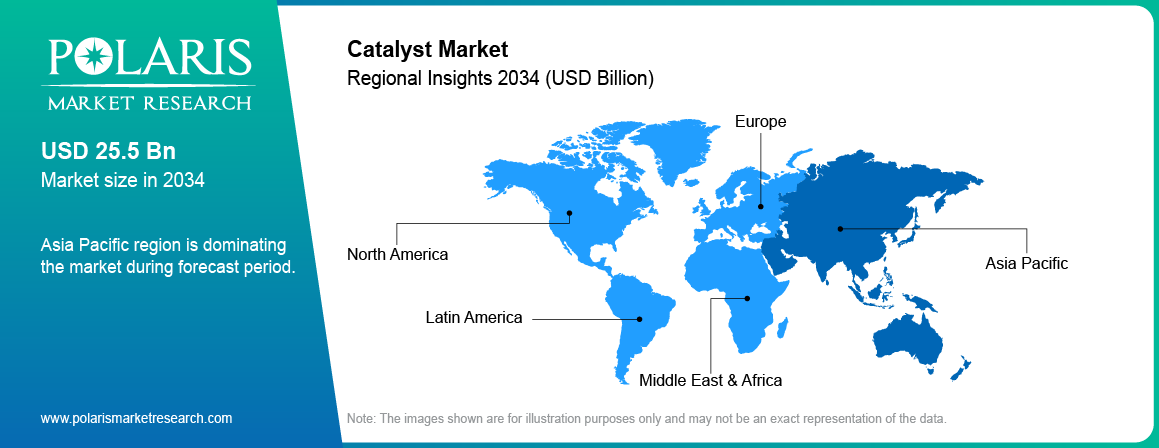

Regional Outlook

By region, the catalyst market report examines North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. Asia Pacific held a large market share in 2025 because of rapid industrialization, growing petrochemical capacity, and rising demand from the automotive and refining sectors. China contributed to the most significant revenue share in Asia Pacific. It is driven by its extensive manufacturing base and government-supported environmental policies. Ongoing investments in renewable energy and emission reduction technologies will also boost catalyst demand in the country. Rising focus on improving refining capabilities and implementing strict fuel standards increased demand for advanced catalytic processes in China. Additionally, India and Southeast Asian countries, such as Vietnam and Indonesia, saw strong market growth due to rising energy consumption, urbanization, and infrastructure development. For example, the World Bank reported that India is urbanizing quickly; by 2036, its towns and cities will be home to 600 million people, or 40% of the population, up from 31% in 2011.

The availability of low-cost labor, increasing chemical production, and favorable regulatory policies have all helped Asia Pacific lead in both catalyst consumption and production.

In North America, the catalysis industry is set to grow significantly in the coming years, driven by strict environmental rules and a strong automotive and industrial sector. The U.S. is expected to be the frontrunner in the regional industry during this time, due to its strong enforcement of air quality standards under laws like the Clean Air Act. These rules continue to encourage industries to adopt technologies that reduce emissions, particularly in areas like transportation, power generation, and refining. Furthermore, rising investments in electric vehicles and sustainable fuels have accelerated research and development efforts to enhance catalytic efficiency and durability. Canada is also expected to contribute to regional growth, supported by clean energy initiatives and its commitment to reducing greenhouse gas emissions.

Source: Polaris Market Research Analysis

Key Players and Competitive Analysis

The catalyst industry is fragmented and is anticipated to witness competition from several players. The demand for catalysts in petrol refining and pharmaceutical companies is likely to increase. Major players in the industry are making substantial investments in research and development to expand their product lines. Key market changes include the launch of new products, larger mergers and acquisitions, contractual agreements, and partnerships with other companies.

Leading catalyst market companies distinguish themselves with their unique catalyst formulas and innovative recycling technologies. They partner with refineries and chemical manufacturers for business expansion. Players focus on continuous investments in research and development and sustainable catalyst solutions. The digital transformation of catalyst testing processes shapes their competitive advantage.

The market is fragmented, with the presence of numerous global and regional market players. Major players in the market are Albemarle Corporation, Arkema, Axens, BASF SE, Clariant, Evonik Industries AG, Exxon Mobil Corporation, Haldor Topsoe A/S, Johnson Matthey, LyondellBasell Industries Holdings B.V., The Dow Chemical Company, Umicore, W. R. Grace & Co.-Conn., and Zeolyst International.

List of Key Companies

- Albemarle Corporation

- Arkema

- Axens

- BASF

- Clariant

- Evonik Industries AG

- Exxon Mobil Corporation

- Haldor Topsoe A/S

- Johnson Matthey

- LyondellBasell Industries Holdings B.V.

- The Dow Chemical Company

- Umicore

- W. R. Grace & Co.-Conn.

- Zeolyst International

Catalyst Industry Developments

In October 2025, Evonik launched its Noblyst® F catalyst portfolio for flow applications. It is helping pharma and fine-chemical customers use continuous processing with improved catalytic performance. (Source: evonik.com)

In September 2025, BASF’s SYNSPIRE® G1-110 catalyst helped Nan Ya Plastics cut steam use by 40,000 metric tons and lower CO₂ emissions by 38,000 metric tons each year. This brings significant savings in operating costs. (Source: basf.com)

In February 2025, WAN-IFRA partnered with OpenAI to launch the South Asia Newsroom AI Catalyst, an accelerator program to help newsrooms adopt artificial intelligence through structured training and coaching. (Source: wan-ifra.org)

Catalyst Market Segmentation

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Heterogeneous Catalyst

- Homogeneous Catalyst

By Raw Material Outlook (Revenue, USD Billion, 2021–2034)

- Chemical Compounds

- Peroxides

- Acids

- Amines & Others

- Metals

- Precious Metals

- Base Metals

- Zeolites

- Others

By Process Outlook (Revenue, USD Billion, 2021–2034)

- Recycling

- Regeneration

- Rejuvenation

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Petroleum Refining

- Fluid Catalytic Cracking (FCC)

- Alkylation Catalysts

- Hydro Processing Catalysts

- Catalytic Reforming

- Others

- Chemical Synthesis

- Polyolefins

- Catalytic Oxidation

- Hydrogenation Catalysts

- Others

- Polymer Catalysis

- Ziegler Natta

- Reaction Initiator

- Single Site

- Others

- Environmental

- Light Duty Vehicles

- Heavy Duty Vehicles

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Catalyst Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 33.78 Billion |

| Market Size in 2026 | USD 35.29 Billion |

| Revenue Forecast by 2034 | USD 49.99 Billion |

| CAGR | 4.5% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Catalyst Market FAQ's

The global market size was valued at USD 33.78 billion in 2025 and is projected to grow to USD 49.99 billion by 2034.

The global market is projected to register a CAGR of 4.5% during the forecast period.

Asia Pacific had the largest share of the global market in 2025.

A few of the key players in the market are Albemarle Corporation, Arkema, Axens, BASF SE, Clariant, Evonik Industries AG, Exxon Mobil Corporation, Haldor Topsoe A/S, Johnson Matthey, LyondellBasell Industries Holdings B.V., The Dow Chemical Company, Umicore, W. R. Grace & Co.-Conn., and Zeolyst International.

The recycling segment dominated the market revenue in 2025.

The homogeneous catalyst segment is expected to grow at the fastest pace in the coming years.

Download Sample Report of Catalyst Market

Please fill out the form to request a customized copy of the research report.