Central Inverter Market Size & Share Global Analysis Report, 2023-2032

REPORT DETAILS

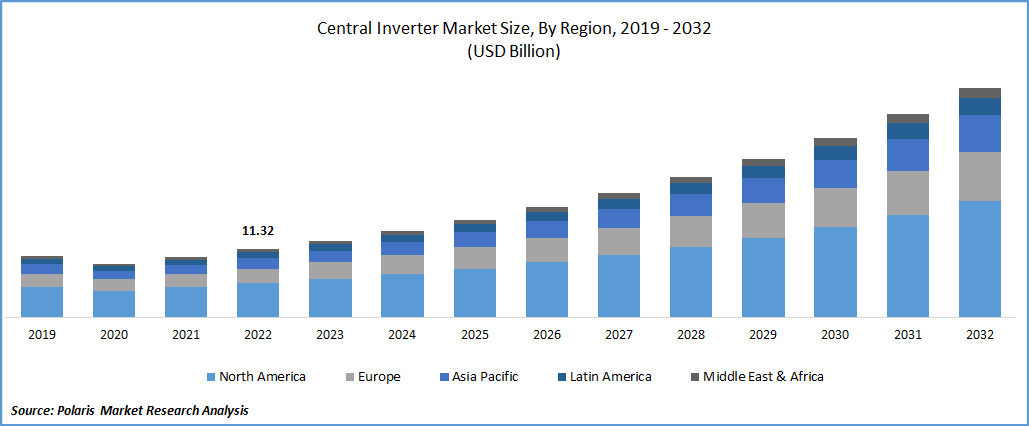

The global central inverter market was valued at USD 11.32 billion in 2022 and is expected to grow at a CAGR of 12.9% during the forecast period. The global market for central inverters is experiencing a surge in demand due to the increasing prevalence of eco-friendly, durable, and highly efficient central inverters that can reliably convert solar energy to electricity and offer grid connection and energy storage capabilities. The market is further driven by the rising demand for large central inverters in commercial installations, industrial locations, and utility-scale solar farms and the need for more advanced technological products with flexible features. These market trends create profitable growth opportunities for central inverter industry players, focusing on efficient and reliable solar power conversion to electricity.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

For Instance, In April 2022, SMA Solar Technology, a German inverter manufacturer, introduced a new range of inverters with power ratings ranging from 12-25 kW. These inverters are designed specifically for roof-top PV systems up to 135 kW in size.

The market for central inverters used in solar modules is expanding due to their ability to convert DC electricity from solar panels into AC power. Unlike multiple smaller inverters, central inverters are easier to install and have a greater capacity to handle power, resulting in higher DC-to-AC power conversion efficiency. Moreover, growing environmental concerns and the increasing world population drive the demand for limited energy supplies. This trend is anticipated to increase the market for central inverters for residential and industrial applications in the foreseeable future.

Furthermore, according to the International Energy Association, renewable energy sources are expected to witness the highest growth in the electrical industry. As a result, the market for central inverters will likely continue expanding in tandem with the adoption of renewable energy sources.

The outbreak of the COVID-19 pandemic has significantly impacted the growth of the global market. This pandemic caused a temporary decline in the demand for central inverters due to the slowdown in the solar energy industry, resulting from supply chain disruptions, labor shortages, and financing challenges. However, the pandemic also increased attention to renewable energy and energy security, leading some countries and regions to implement policies and incentives to support the adoption of solar energy and central inverters. This resulted in a rebound in demand for central inverters in markets; the long-term outlook for the market remains positive, propelled by the continued growth of solar energy and the rising demand for efficient and dependable conversion of solar power to electricity, particularly in regions with strong government support and favorable regulatory frameworks.

Source: Polaris Market Research Analysis

For Specific Research Requirements, Request for a Customized Report

Industry Dynamics

Growth Drivers

The global central inverter market growth is driven by adopting central inverters as an alternative to multiple smaller or micro-inverters in solar power systems. This trend is attributed to the energy-saving and eco-friendly nature of central inverters, which overcome issues related to maintenance and durability worldwide. Additionally, central inverters reduce the grid connection as compared to string inverters. Central inverters have a simpler design, making them easier to troubleshoot and link to the server. They are also easier to integrate into the SCADA network, which are major factors contributing to the growth of the global market.

Furthermore, the faster response time of central inverters compared to string inverters is a significant driver of demand in the market. String inverters are prone to latency issues due to their complex design and communication with multiple devices, whereas central inverters can respond quickly to controls by requiring only one inverter to receive commands instead of many. This advantage is expected to be a significant contributing factor to the market's ongoing growth over the forecast period.

Report Segmentation

The market is primarily segmented based on power rating, end-user, and region.

| By Power Rating | By End-User | By Region |

|

|

|

Source: Polaris Market Research Analysis

To Understand the Scope of this Report: Request Customization

500 kW to 1 MW segment accounted for the largest market share in 2022

The 500 kW to 1 MW segment accounted for the largest market share in the market due to the increasing demand for commercial and industrial-scale solar installations and utility-scale solar farms, where central inverters in this power range are most suitable. These installations require higher power output and reliability, making central inverters in this range a preferred choice for solar power conversion. Additionally, central inverters in this range offer grid connection and energy storage capabilities, essential features in large-scale solar power plants.

Furthermore, the greater than 1 MW segment contributed significantly to market growth as this segment caters to utility-scale solar farms and large commercial and industrial installations that require high-power central inverters. With the increasing demand for renewable energy sources, there is a growing need for large-scale solar power plants that require central inverters with a capacity greater than 1 MW. As a result, the segment is projected to continue driving the market's growth in the upcoming years.

Utility-scale segment is expected to witness highest growth in projected period

The utility-scale segment is expected to grow fastest at a CAGR over the projected period. This is primarily due to the increasing demand for renewable energy and the growing number of large-scale solar power projects undertaken worldwide. There is a rising demand for central inverters to meet the high-capacity requirements of utility-scale solar power plants. The growth segment is also driven by factors like increasing investments in solar power projects, particularly in emerging economies, government initiatives to promote the adoption of renewable energy, and the declining cost of solar panels and inverters.

Moreover, the Residential segment accounts for rapid market growth, which is highly accelerated by the abundance availability of resources and the adoption of favorable government policies and economies of scale as key ingredients in the production of the central inverters. It helps increase the opacity of the main inverter and raise awareness of the benefits of renewable energy, propelling the demand and growth of the segment over the coming years.

Asia Pacific region dominated the global market in 2022

The Asia Pacific region dominated the global market in 2022 with a healthy market share. The regional market growth can be attributed to rapid urbanization and continuously growing awareness regarding the regulation of increasing environmental awareness, government support, and initiatives to promote renewable energy and reduce carbon emissions. Additionally, the region’s fast-paced economic growth and rising population are expected to drive market development in Asia-Pacific further.

North America region is emerging as the fastest growing region with a significant growth rate over the coming years on account of increasing research & development-related activities aimed at innovating sustainable products with several new and more advanced features. The rising demand for renewable energy sources such as solar power and wind energy is driving the market growth in this region. Additionally, advancements in technology and increasing investments in the renewable energy sector are expected to accelerate further the development of the global market in the region.

The US Department of Commerce has recommended that anti-dumping and countervailing duties be extended to silicon solar cell and panel exports from Cambodia, Malaysia, Thailand, and Vietnam. This development is expected to increase demand for domestic central inverters in the US market, as Chinese manufacturers may face higher tariffs and restrictions.

Competitive Insight

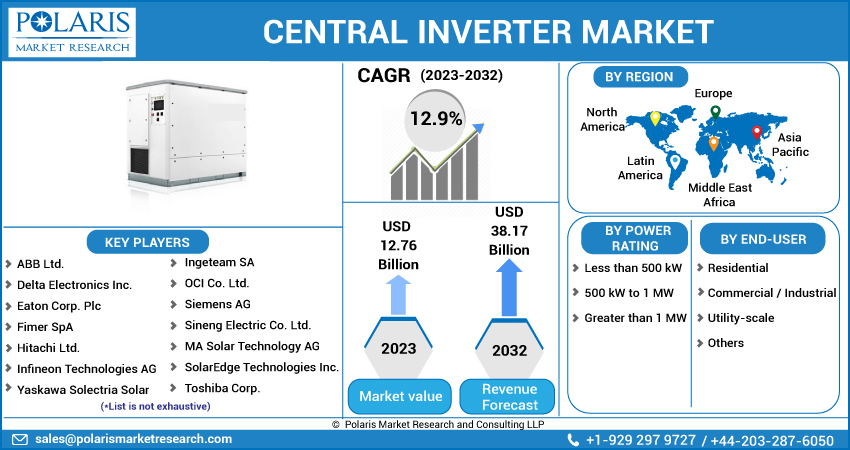

Some of the major players operating in the global market include ABB Ltd., Delta Electronics, Eaton Corp., Ginlong Technologies., Hitachi, Huawei Technologies, Infineon Technologies, Ingeteam, Shenzen Growatt, Siemens, Sineng Electric, SMA Solar Technology, SolarEdge Technologies, Sungrow Power Supply, Toshiba Corp., Yaskawa Solectria Solar, and Zhejiang CHINT Electrics.

Recent Developments

- In March 2022, Sungrow increased its fab capacity to 10GW/annum, which is a significant development in the manufacturing sector in India and is contributing to the growth of the inverter market.

Central inverter Market Report Scope

| Report Attributes | Details |

| Market size value in 2023 | USD 12.76 billion |

| Revenue forecast in 2032 | USD 38.17 billion |

| CAGR | 12.9% from 2023 – 2032 |

| Base year | 2022 |

| Historical data | 2019 – 2021 |

| Forecast period | 2023 – 2032 |

| Quantitative units | Revenue in USD billion and CAGR from 2023 to 2032 |

| Segments covered | By Power Rating, By End-User, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

| Key companies | ABB Ltd., Delta Electronics Inc., Eaton Corp. Plc, Fimer SpA, Ginlong Technologies Co. Ltd., Hitachi Ltd., Huawei Technologies Co. Ltd., Infineon Technologies AG, Ingeteam SA, OCI Co. Ltd., Shenzen Growatt New Energy Technology Co. Ltd., Siemens AG, Sineng Electric Co. Ltd., SMA Solar Technology AG, SolarEdge Technologies Inc., Sungrow Power Supply Co. Ltd., Toshiba Corp., Yaskawa Solectria Solar, and Zhejiang CHINT Electrics Co. Ltd. |

Source: Polaris Market Research Analysis

Central Inverter Market FAQ's

The global central inverter market size is expected to reach USD 38.17 billion by 2032.

Key players in the central inverter market are ABB Ltd., Delta Electronics, Eaton Corp., Ginlong Technologies., Hitachi, Huawei Technologies, Infineon Technologies, Ingeteam.

Asia Pacific contribute notably towards the global central inverter market.

The global central inverter market is expected to grow at a CAGR of 12.9% during the forecast period.

The central inverter market report covering key segments are power rating, end-user, and region.

Download Sample Report of Central Inverter Market

Please fill out the form to request a customized copy of the research report.