Collagen Market Share, Size, Global Analysis Report, 2026-2034

REPORT DETAILS

Collagen Market Summary

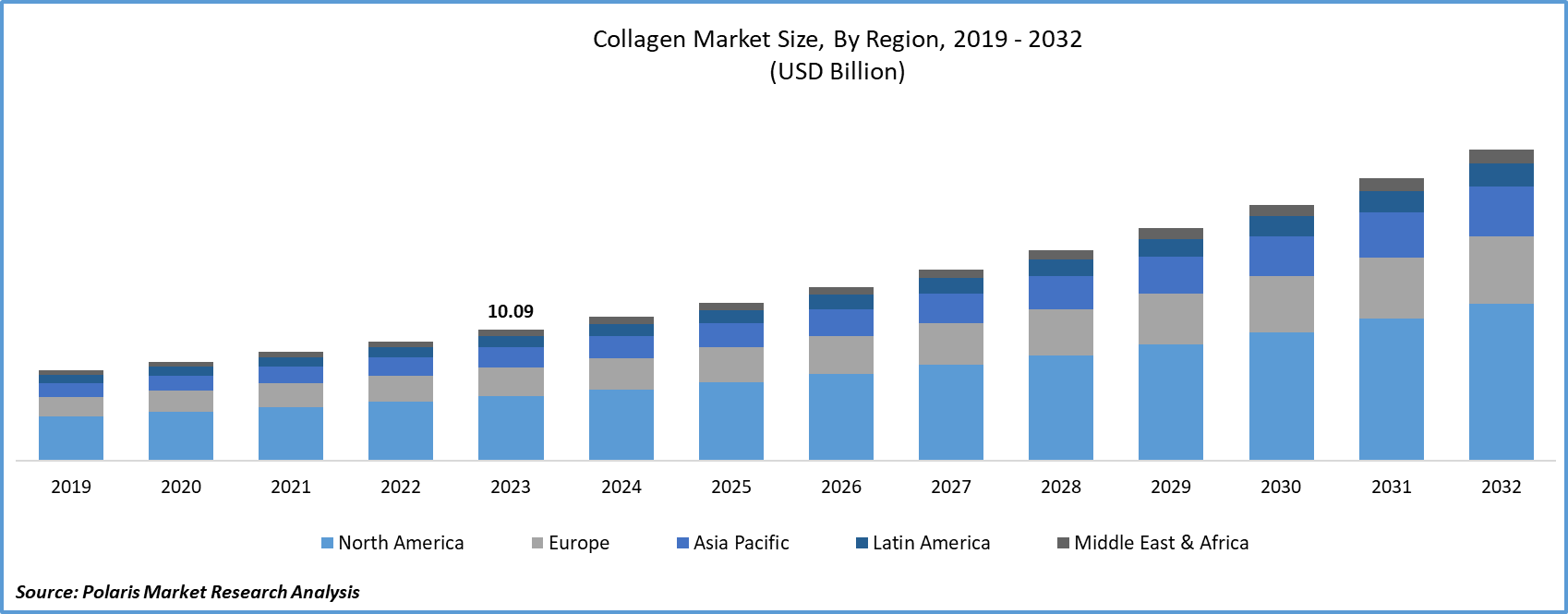

The collagen market size was valued at USD 11.06 billion in 2025, exhibiting a CAGR of 11.2% during 2026–2034. The market is driven by rising demand in cosmetics, healthcare, and food industries and increasing aging population propel collagen demand. The growing awareness of collagen benefits, advancements in extraction technology, and expanding applications in wound care and supplements drive the market growth.

Market Statistics

Key Takeaways

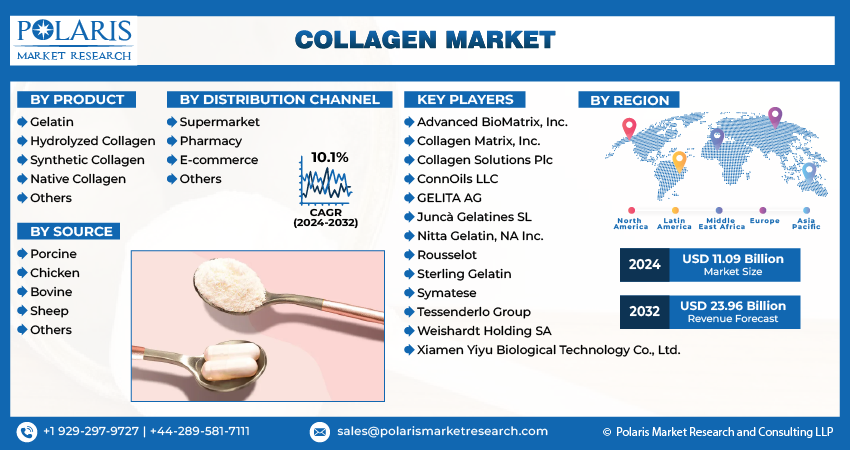

- The gelatin segment contributed to the largest market share in 2025. It is used in a wide range of applications in the food and pharmaceutical industries. Gelatin is economical due to its well-established production processes.

- The chicken collagen segment held a significant share in 2025. It is increasingly being used as an alternative as it is versatile for people with religious/dietary limitations. It is beneficial for joint health.

- The supermarkets and pharmacies segment dominated the revenue share in 2025. It is due to their convenience and consumers' trust in them for health-related shopping.

- North America led the global market share in 2025. The dominance is driven by substantial expenditure on healthcare products and robust research and development (R&D) efforts in collagen-based developments.

- Asia Pacific is witnessing rapid growth. Growing disposable incomes of middle-class population, aging populations, and rising demand for wellness and beauty supplements boost the growth.

Industry Dynamics

- The high digestibility and bioavailability of hydrolyzed collagen drive its popularity as a functional food and supplement.

- Gelatin is favored because of its low cost and wide use in the food, pharmaceutical, and film industries.

- The demand for collagen from bovines benefits from a stable supply and a high content of Type I and III collagen for bone, hair, and skin.

- E-commerce enhances collagen availability through reviews, diversity, and convenience. Thus, the rising penetration of online platforms favors direct-to-consumer (D2C) brand expansion.

- Concerns about ethics and diet restrictions on animal-based collagen sources limit acceptance among some demographic and cultural groups.

Source: Polaris Market Research Analysis

The global collagen market is a rapidly expanding segment of the protein ingredients and biomaterials industry. Rising industrial utilization across nutraceuticals, pharmaceuticals, functional foods, and medical applications propels market growth. Collagen demand is increasingly driven by formulation efficiency, raw material availability, extraction technology advancements, and regulatory compliance. Thus, it has become a strategically important ingredient category for manufacturers and product developers. Preventive healthcare trends and expanding clinical and biomedical use cases are driving the adoption of collagen.

Collagen supports connective tissues like skin, bones, tendons, and ligaments. It maintains strength and elasticity in the body. The collagen industry involves making and selling collagen and its derivatives, such as hydrolyzed collagen and gelatin. These substances come from animal by-products, including bovine, porcine, and marine sources. They are widely used in various areas, including nutraceuticals, personal care products, cosmetics, food and beverages, and healthcare. Growing consumer awareness and the known benefits for skin health, joint function, and overall well-being drive the demand for collagen products.

The expansion of the collagen industry is driven by the surging demand for anti-aging supplements and solutions. Skin mobility and joint concerns from the globally aging population boost the demand for these products. Moreover, the rising interest in functional foods and dietary supplements, which contain collagen peptides, also contributes greatly to the growth. This is due to their bioavailability and health benefits. Additionally, the personal care and cosmetic industry is a major user of collagen because of its perceived anti-aging properties. This drives the increasing use of collagen in skincare products. The growing refinement of extraction and processing technologies for collagen is enabling an enhancement in the quality and versatility of collagen products, deepening the effectiveness across numerous end-use industries, and expanding the overall scope of this primal protein.

Regulatory Impact on Collagen Industry

| Aspect | FDA (US) | EFSA (EU) | Asia (varies) |

| Pre-market approval | Not required for collagen supplements | Required for novel foods, strict entry for new sources | Often required (China, Korea); variable (Japan FOSHU/FFC) |

| Health claims | Allowed structure/function w/ disclaimer | Strictly evaluated & authorized | Country-specific Japan has FOSHU/FFC China has strict regulations Other countries have mixed rules and regulations |

| Safety oversight | Post-market monitoring | Pre-market and post-market | Pre-market common but varies by country |

| Market entry speed | Fastest | Slowest (EFSA approvals) | Mixed. Some fast (Japan FFC), some slow (China registration) |

Source: Polaris Market Research Analysis

Collagen Market Drivers

Rising Demand from the Aging Population

With aging, the human body produces less natural collagen. It leads to visible signs of aging, including wrinkles, reduced skin elasticity, and joint discomfort. Data from the NCBI indicates that the U.S. population aged 65 and above is expected to nearly double by 206. It is expected to increase from approximately 56 million in 2020 to around 95 million by 2060. This demographic shift has created a high demand for antiaging product to alleviate age-related concerns, particularly those addressed by collagen supplementation. Older adults focus on maintaining a youthful appearance and an active lifestyle directly. This demographic trend is expanding the market for anti-aging and joint health solutions. Therefore, global aging population is driving the demand for collagen products.

Growing Health and Wellness Awareness

Increased consumer awareness of the significant health benefits of collagen boosts its popularity. Various research studies consistently shown that collagen supports skin hydration, elasticity, and overall joint health. According to a review published in Heliyon in 2023, hydrolyzed collagen supplementation leads to positive changes in the skin. It reduces wrinkle formation and enhances skin elasticity and hydration. According to Nutrients in 2023, collagen supplementation improves pain relief and joint function for joint health. Such scientific findings are available on various research platforms such as PubMed and NCBI. This access helps consumers make informed choices. As a result, more people are accepting collagen as an important supplement for overall wellness. The growing awareness of collagen's various health benefits is driving new collagen health trends.

Scientific support from peer-reviewed studies and easier access to clinical research build trust among consumers and practitioners in collagen-based products. This change positions collagen not just as a supplement, but as an ingredient in preventive healthcare strategies. It also helps maintain steady market demand.

Expansion of Functional Foods and Beverages

Functional foods and beverages contain health-promoting ingredients. The increasing popularity of these foods and drinks drives collagen demand. Consumers seek foods and beverages that provide more nutrition and health benefits beyond the basics. Collagen fits this need because of its mild taste. It is easy to add to various products, like protein bars, drinks, and fortified snacks, which boosts its popularity. As a result, manufacturers develop and launch new collagen-infused products. This strategy makes collagen accessible to more consumers. Adding collagen to convenient and health-focused items increases demand.

Food and beverage companies want to add protein without losing taste or texture. From a production standpoint, collagen’s neutral flavor and flexibility make it highly appealing in the industry. This has accelerated its use in ready-to-drink (RTD) beverages, nutrition bars, and fortified dairy alternatives. These factors are increasing the reach of the collagen supply chain.

What are Collagen Market Risks and Limitations?

The collagen industry witnesses several risks and challenges. Regulatory divergence across the FDA, EFSA, and Asian authorities increases compliance costs and delays market entry. Strict health-claim approvals in the EU limit marketing flexibility and require solid clinical evidence. Raw material volatility from bovine, porcine, and marine sources exposes suppliers to price swings, disease outbreaks, and sustainability issues. Quality variability and contamination risks can lead to recalls and damage brand trust. Also, price competition, doubts about efficacy, and growing demand for plant-based alternatives create ongoing competitive pressure.

Source: Polaris Market Research Analysis

Segmental Insights

By Product

The collagen market by product is segmented into gelatin, hydrolyzed collagen, synthetic collagen, native collagen, and others. The gelatin segment held the largest market share in 2025. Gelatin exhibits gelling, binding, and stabilizing properties. Thus, in the food and beverage industry, it is commonly used in confectionery, dairy products, and desserts. Additionally, its wide-ranging applications in the pharmaceutical sector and its role in photographic films boosts it popularity. Most gelatin is produced using a well-established production infrastructure. Thus, it is relatively inexpensive compared to collagen forms. This affordability drives growth in the gelatin collagen market. Gelatin leads in volume, but synthetic and recombinant collagen are gaining popularity. In medical applications, tissue engineering, and cosmetic formulations, purity, consistency, and ethical sourcing matter. Because of this, synthetic and recombinant collagen are being used more in these products. However, high production costs currently limit large-scale commercialization. This factor hinders the synthetic collagen market expansion.

The hydrolyzed segment experiencing the highest growth rate during the forecast period. Hydrolyzed collagen have high bioavailability and ease of digestion. These hydrolyzed collagen benefits help explain its popularity in the growing nutraceutical and functional food markets. Its proven advantages for skin, joint, and gut health attract consumers seeking health improvements. The adaptability of collagen allows for easy inclusion in various products, such as powdered supplements, drinks, and protein bars. The shift in consumer interest toward proactive health management and the ongoing development of new uses create market opportunities for hydrolyzed collagen.

By Source

The bovine collagen segment leads the market. This is mainly because there is a large supply of raw materials from the cattle industry, including hides, bones, and cartilage byproducts from meat processing. The existing infrastructure for sourcing and processing bovine collagen makes it easy to access this type of vertebrate collagen. It is commonly used in the food, pharmaceutical, and cosmetic industries. This wide usage greatly contributes to its strong presence. Bovine collagen is especially important because it has high concentrations of type I and type III collagen. These types are crucial for keeping skin, hair, nails, and bones healthy. These benefits are propelling the bovine collagen market.

Chicken collagen is experiencing the highest growth rates in the coming years. Chicken collagen demand is growing as consumers seek alternatives to traditional sources like porcine and bovine collagen. These preferences are shaped by dietary restrictions, religious beliefs, and worries about diseases that can transfer from animals to humans. Among various collagen sources, marine collagen is becoming more popular because it is more easily absorbed and closely linked to skin and beauty benefits. Chicken collagen is also expected to grow significantly due to its natural type II collagen content, which is especially good for joint health. The rising interest in diverse and specialized sources of collagen is a major trend influencing market demand. Chicken collagen's type II concentration makes it a strong choice for joint health and orthopedic nutrition products. Meanwhile, the marine collagen segment is gaining ground in premium beauty and skincare products. Its high absorption rate is driving growth in the marine collagen market.

By Distribution Channel

Supermarkets and pharmacies account for a large share of collagen product sales. This is mainly because they are widely available, making it easy for consumers to buy collagen supplements and products while shopping. Pharmacies, in particular, gain from consumer trust and provide professional advice, which is crucial for health-related purchases. Having immediate access to products and the chance for consumers to check them out in person adds to the popularity of these stores.

Online shopping is the fastest-growing segment for collagen product sales due to the rise of e-commerce platforms. Consumers can conveniently search for various collagen products from different brands without leaving home. Competitive pricing, detailed product descriptions, and easy access to customer reviews significantly influence purchasing choices. Manufacturers increasingly sell directly to consumers. Thus. e-commerce is a rapidly growing channel for selling collagen products.

Nutraceutical-Grade Collagen Vs. Pharma-Grade Collagen

| Parameter | Nutraceutical-Grade Collagen | Pharma-Grade Collagen | Buyer / Regulatory Implication |

| Primary Use | Dietary supplements, functional foods, beauty-from-within | Injectable, implantable, wound care, drug formulations | Determines regulatory pathway |

| Regulatory Category | Food/dietary supplement | Drug substance or medical-grade excipient | Drives approval complexity |

| Regulatory Oversight | FDA (DSHEA), EFSA (food/novel food), Asia food authorities | FDA (CDER/CBER), EMA, PMDA, MFDS | Pharma requires authority pre-approval |

| Pre-Market Approval | Not required in the U.S. In the EU and Asia, approval is required if novel | Mandatory clinical and regulatory approval | Longer timelines for pharma |

| Manufacturing Standard | Food GMP, dietary supplement GMP | Pharma GMP (ICH Q7, EU GMP Part II) | Higher CAPEX for pharma plants |

| Purity Level | Typically 90–97% | ≥99%, low endotoxin & bioburden | Impacts cost and yield |

| Molecular Control | Broad peptide distribution | Tight MW specification, batch consistency | Critical for injectables |

| Source Traceability | Required but flexible | End-to-end traceability, validated suppliers | Audit intensity higher |

| Sterility Requirement | Not required | Required (injectables, implants) | Major cost differentiator |

| Clinical Evidence | Limited human studies; functional support | Robust clinical trials (Phase I–III) | High R&D investment |

| Claims Allowed | Structure/function (e.g., skin, joints) | Therapeutic or clinical efficacy claims | Marketing freedom vs certainty |

| Formulation Types | Powders, capsules, RTD beverages | Injectable solutions, scaffolds, drug carriers | Different downstream industries |

| Quality Testing | Microbial limits, heavy metals | Endotoxin, viral safety, residual solvents | Expanded QC panels |

| Batch Release | Internal QA release | Qualified Person (QP) or regulatory release | Slower but safer supply chain |

| Time to Market | Short (weeks–months) | Long (5–10 years) | Impacts ROI horizon |

| Cost Structure | Low–moderate cost | Very high cost per kg | Pricing power in pharma |

| End-User Buyers | Supplement brands, food companies | Pharma, med-tech, hospital supply chains | Different procurement logic |

| Risk Profile | Higher post-market claim risk | High upfront regulatory risk, low post-market | Influences investment strategy |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Regional Analysis

The North America collagen market holds the largest share of the global market. A well-developed nutraceutical and dietary supplement industry propels the collagen demand in the region. Also , an advanced healthcare system drives the regional market growth. A high per capita income leads to increased spending on health products, particularly collagen. Additionally, significant research and development investments from various North American companies foster continuous innovation in functional foods and personal care products. It is expanding the range of nutrition and beauty items enhanced with collagen. Strong regulatory frameworks and established collagen ingredient suppliers support premium product development. All these benefits boost the growth of the collagen market in North America.

The Asia Pacific collagen market is recognized as the fastest-growing segment. This growth is mainly attributed to health-conscious consumers in developing countries like China and India. Rising incomes are leading to more spending on dietary supplements and "beauty-from-within" products. The region also values traditional health and wellness practices. Additionally, an aging population seek effective antiaging solutions. Furthermore, there is growing domestic innovation surrounding traditional and herbal sources of collagen. This approach aligns more closely with regional demand and enhances market penetration. China dominates the collagen market in Asia Pacific. China has a high collagen production capacity and export activity. However, India represents a high-growth consumption market supported by rising nutraceutical penetration.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

The competition environment in the collagen sector comprises a small number of dominating international players along with an emerging diverse group of niche and local operators. Old segments still focus on developing new products such as hydrolyzed collagen and collagen extracted from marine sources to fulfill specific consumer demands related to health and beauty. These firms are changing marketing strategies to make the product more soluble and palatable while sustaining ethical and responsible sourcing and manufacturing policies. These conditions encourage alternatives in collagen technology and applications.

Collagen market key players are emphasizing sustainability certifications, upcycled raw materials, clean-label positioning, and application-specific peptide development to differentiate their offerings. Strategic investments in R&D, capacity expansion, and regulatory approvals shape competitive advantage in the collagen industry.

List of Key Companies

- Amicogen Inc.

- Collagen Solutions Plc (a Rosen's Diversified Inc. company)

- Gelita AG

- Nippi Incorporated

- Nitta Gelatin Inc.

- PB Leiner (part of Tessenderlo Group)

- Rousselot (a Darling Ingredients brand)

- Weishardt International

Industry Developments

-

In September 2025, Evonik launched VECOLLAN, a new collagen product designed for medical device development. (Source: evonik.com)

-

In May 2025, Darling Ingredients and Tessenderlo Group formed a joint venture, Nextida, to expand in the collagen-based health, wellness, and nutrition market; Darling holds an 85% stake, and the company is expected to generate about USD 1.5 billion in revenue. (Source: investors.darlingii.com)

-

In April 2025, Rousselot, a Darling Ingredients brand, received Upcycled Certified status for its Peptan collagen peptides. (Source: darlingii.com)

Collagen Market Segmentation

By Product Outlook (Revenue – USD Billion, 2021–2034)

- Gelatin

- Hydrolyzed Collagen

- Synthetic Collagen

- Native Collagen

- Others

By Source Outlook (Revenue – USD Billion, 2021–2034)

- Porcine

- Chicken

- Bovine

- Sheep

- Others

By Application Outlook (Revenue – USD Billion, 2021–2034)

- Food & Beverage Products

- Nutritional Products

- Pharmaceutical Products

- Cosmetics & Personal Care

- Medical Devices & Research

- Textile Industry

- Others

By Distribution Channel Outlook (Revenue – USD Billion, 2021–2034)

- Supermarket

- Pharmacy

- E-commerce

- Others

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Collagen Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 11.06 Billion |

| Market Size in 2026 | USD 12.27 Billion |

| Revenue Forecast by 2034 | USD 28.84 Billion |

| CAGR | 11.2% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Collagen Market FAQ's

The market is projected to reach USD 28.84 billion by 2034, at a CAGR of 11.2% from 2026 to 2034.

The bovine collagen holds the largest revenue share. The segment is driven by abundant availability, cost-effectiveness, and widespread acceptance across the food and pharmaceutical industries.

Nutritional products and dietary supplements dominate the market due to rising awareness about their nutritional benefits.

The market in Asia Pacific is witnessing the fastest growth. Rising disposable incomes, health awareness, and strong beauty culture drive the market growth.

The hydrolyzed collagen segment dominates the revenue share. Hydrogen collagen is also known as collagen peptides. Its high bioavailability, easy absorption, and various uses in supplements and functional foods drive its dominance.

The following are some of the market trends: ? Increase in demand for tailored collagens: There is a growing demand not just for general collagen, but for specific types like type I, II, and III collagen, which are designed to aid skin, joints, and gut wellness. ? Emergence of eco-friendly and marine sources: Even though animal collagen still holds its market dominance, demand for marine collagen is increasing due to perceived greater bioavailability and sustainability.

Collagen can be described as a protein that is most prevalent in the human body, as it is one of the primary constituents of connective tissue. With regard to the body, collagen is a fibrous protein of great importance, responsible for strength, elasticity, and support to the skin, blood vessels, bones, cartilage, ligaments, tendons, and more. Its principal constituents are amino acids, including glycine, proline, and hydroxyproline, which are uniquely arranged in a triple helix, which provides collagen great rigidity and tensile strength.

Download Sample Report of Collagen Market

Please fill out the form to request a customized copy of the research report.