Conductive Inks Market Research Report, Share & Forecast By 2026 - 2034

REPORT DETAILS

REPORT DETAILS

Conductive Inks Market Summary

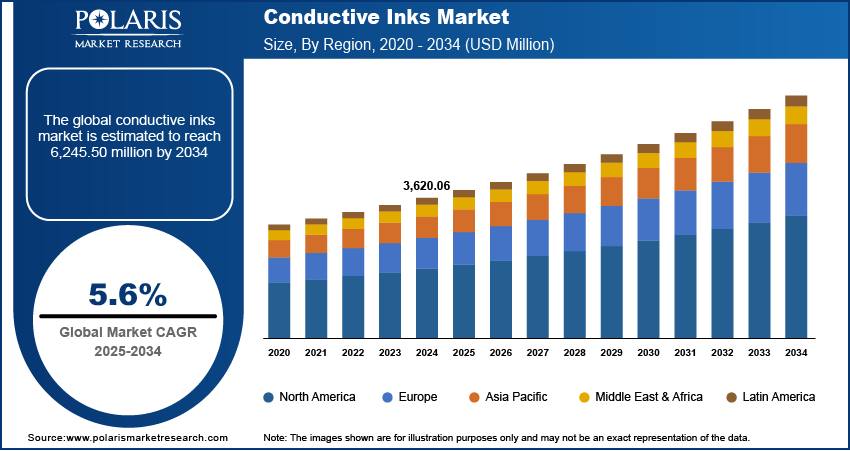

The global conductive inks market size was valued at USD 3,818.60 million in 2025. The market is projected to grow at a CAGR of 5.6% from 2026 to 2034. Rising technological advancements in photovoltaic systems and the introduction of thin film PV technologies are driving market development.

Market Statistics

Key Takeaways

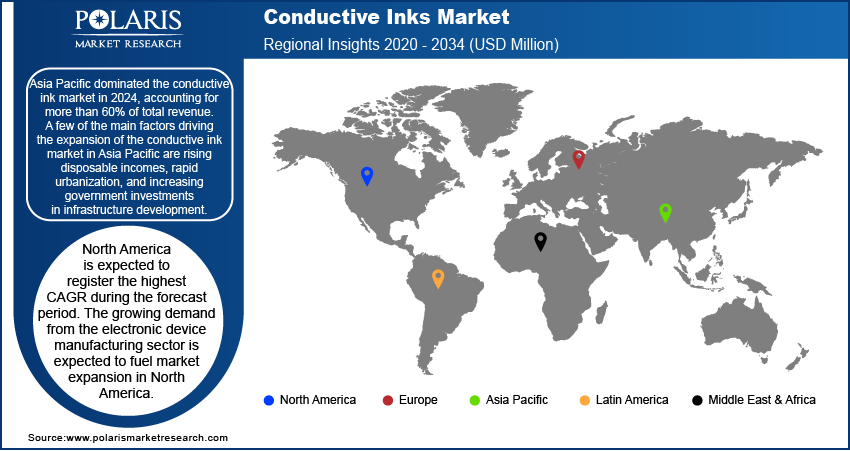

- Asia Pacific accounted for the largest market share of 46.5% in 2025. The regional market dominance is attributed to rapid urbanization and growing focus on offering reasonably priced modern electronics.

- The market in North America is expected to grow at a 6.1% CAGR. This is owing to increased demand for conductive inks from the electronic device manufacturing sector.

- The conductive silver ink segment led the market with a 68.4% share in 2025. This is primarily due to its increased popularity across sectors such as flexible electronics and printed electronics.

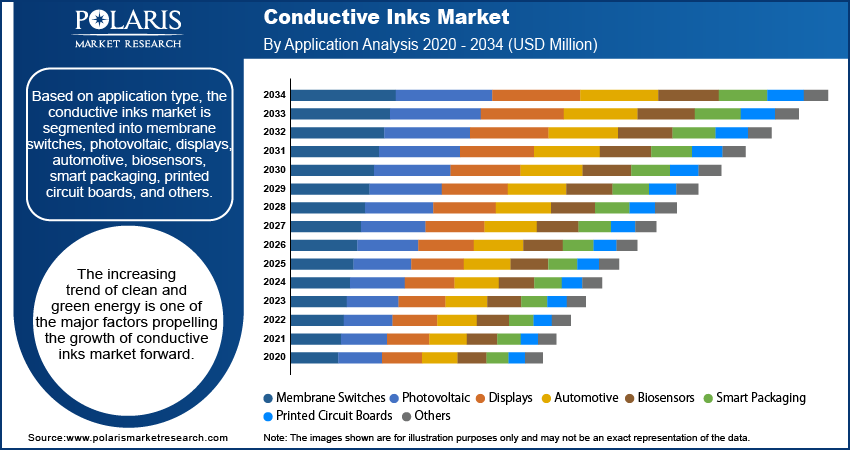

- The photovoltaic segment dominated the market with a 33.7% share in 2025. Rising use in the fabrication of photovoltaic textiles contributes to the segment’s leading position.

- The biosensors segment is projected to grow at a 6.8% CAGR. Rising demand for advanced healthcare diagnostics drives the segment’s growth

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The implementation of environmental regulations by governments globally for the use of lightweight, advanced materials is fueling market expansion.

- Innovations in economical substitutes for silver-based conductive inks are propelling the development of the market.

- The growing demand for conductive inks from the automotive and renewable energy sectors presents significant market opportunities.

- High volatility of the silver price may present challenges to market growth.

AI Impact on Conductive Inks Market

- Artificial intelligence assists in the improvement of conductive ink composition based on materials analysis and enhancing conductivity.

- It enhances quality control by identifying any abnormalities during the production and printing process.

- It promotes manufacturing efficiency through minimizing wastage of materials and enhancing printing accuracy.

- It facilitates faster product development for applications such as flexible electronics, sensors, and printed circuit boards.

Conductive ink is a type of ink that conducts electricity when printed. It is created by mixing conductive materials such as graphite or silver particles into ink. Since the development of nanotechnology, there has been a growing interest in replacing metallic materials with nanomaterials. Conductive inks can be used to create electrical circuits on a wide range of materials, including wood, metal, textiles, some plastic types, compressed wood (cork), and paper. The inks can be used to replace traditional copper or wired circuits in electronics. They have a wide range of applications, including membrane switches, subdural electrodes, capacitive touch film sensors, screen-printed antennas, in-mold electronics, and e-textiles. Conductive inks are often used in wearable clothing as they can stretch and flex with the wearer.

Growing technological advancements in photovoltaic systems are expected to propel the global conductive ink market demand. PV cells are semiconductor devices used in direct electricity generation. The manufacturing process for PV cells is laborious. As a result, the introduction of thin film PV technologies resulted in a significant increase in market share. This factor is expected to contribute to the conductive ink market growth over the forecast period.

New product types are being developed that are suitable for rigid and flexible substrates and have low electrical resistivity, thereby contributing to the conductive ink market development. Rising demand for efficient and miniature consumer electronics has increased demand for conductive inks. Throughout the forecast period, these will replace energy-consuming wires and bulky circuits. These inks are used as a substitute for traditional wire circuits owing to their better power efficiency, durability, and smaller size.

Conductive Inks Market Dynamics

Growing Necessity of Miniaturization and Efficiency in Devices

Governments across the world have enforced environmental regulations to encourage industries to use lightweight, advanced materials instead of heavy ones in devices. Additionally, consumers' inclination for lightweight and compact devices has enhanced the need for product miniaturization in the consumer electronics sector. Conductive inks are commonly used instead of traditional wire and circuit arrangements to increase efficiency and reduce the weight of electronic components, as they are reliable, efficient, and effective. Therefore, the use of conductive inks to meet the rising demand for smaller and more effective devices propels the conductive inks market development.

Innovations in Economical Substitutes for Silver-Based Conductive Inks

Demand for more affordable substitutes for silver-based conductive inks is rising due to the growing silver cost. Conductive inks based on graphene have emerged as a substitute. Even at complex levels, graphene-based conductive inks can achieve high conductivity in complex devices. The primary ingredients used to make conductive inks are carbon, copper, and silver. Copper is less expensive but more susceptible to oxidation than silver, which is highly conductive but more costly. Graphene, on the other hand, is a useful substitute for these materials and can provide the same qualities at significantly lower costs. A number of businesses are using this alternative to provide efficient solutions in terms of cost and performance, which opens lucrative opportunities for conductive ink producers.

Flexible and Wearable Electronics Trends

The rising trend toward smart wearables, flexible displays, e-textiles, and connected healthcare devices has driven rapid growth in the use of conductive inks in the electronics industry. The use of stretchable, flexible conductive ink by manufacturers enables them to develop lightweight, bendable, and foldable electrical circuits that retain their electrical conductivity during use. Such features make conductive ink ideal for developing electronic items like smart watches, activity trackers, wearable medical sensors, flexible phones, and e-textiles. Moreover, developments in printed electronics and flexible substrates are contributing to the growth of the conductive inks market.

Conductive Inks Market Segment Insights

Outlook by Product Type

Based on product type, the conductive inks market is segmented as conductive silver ink, conductive polymers, conductive copper ink, conductive nanotube inks, carbon/graphene ink, dielectric ink, and others. The conductive silver ink segment dominated the market with 64.8% of the market share in 2025. In the coming years, the growing popularity of conductive silver ink in sectors such as flexible electronics and printed electronics is expected to drive the segment expansion. By facilitating the use of nanomaterials, product configuration advancements have helped to make conductive silver inks extremely popular across a range of industries.

Assessment by Applications Outlook

Based on application, the conductive inks market is segmented into membrane switches, photovoltaic, displays, automotive, biosensors, smart packaging, printed circuit boards, and others. The photovoltaic segment held the largest share of over 33.7% of the market revenue in 2025. The dominance is attributed to its use in the fabrication of photovoltaic textiles. During the forecast period, the growing importance of clean energy is probably going to drive the photovoltaic segment's growth. The rising development of solar plants is driven by the growing demand for electricity on a global scale. Therefore, the market for conductive inks is anticipated to grow at a strong rate during the forecast period due to the increasing demand for clean energy.

Assessment by Regional Insights

By region, the report provides a thorough analysis and conductive inks market insights into Asia Pacific, North America, Europe, Latin America, and Middle East & Africa.

Asia Pacific dominated the conductive ink market with over 46.5% of the revenue share in 2025. A few of the main factors driving the conductive ink market expansion in Asia Pacific are rising disposable incomes, rapid urbanization, and improved government balance sheets that lead to higher infrastructure spending. Additionally, the rising focus on offering reasonably priced modern electronics is propelling the Asia Pacific market.

The growing demand from the electronic device manufacturing sector is expected to fuel market expansion in North America. With the presence of regional production sites of international automakers such as Ford, General Motors, Chevrolet, and Tesla, the US is one of the world's largest automakers. Major automakers' involvement in vehicle electrification is anticipated to increase demand for conductive inks in the production of electronic components used in these electric vehicles. Therefore, growing consumer demand for cars with more sophisticated features creates the requirement for more electronic devices and sensors in cars, which drives the regional conductive ink market expansion.

Key Players and Competitive Insights

The conductive ink market exhibits a consolidated and monopolistic structure. The market players are fiercely competitive with one another, primarily over product quality, pricing, and customization. The expansion of the conductive inks market's end-use segments is probably going to push producers to offer their clients better goods and technologies and to look into undiscovered markets. In order to grow their businesses and obtain a competitive edge over other major players in the market, manufacturers are taking part in strategic initiatives such as mergers and acquisitions, and partnerships.

The conductive inks market will continue to grow in the coming years as a result of the key players in the industry investing a major amount in research and development to broaden their product lines. A few of the major players involved in the market are DuPont.; Sun Chemical Corporation; PPG Industries; Henkel AG; Applied Nanotech Holdings, Inc.; Vorbeck Materials Corp.; Poly-Ink; Chem Associates, Inc.; Methode Electronics; Henkel Ag & Co. KgaA; and Fujikura Ltd.

List of Key Players

- DuPont.

- Sun Chemical Corp

- PPG Industries

- Henkel AG

- Applied Nanotech Holdings, Inc

- Vorbeck Materials Corp.

- Poly-Ink

- Chem Associates, Inc.

- Methode Electronics

- Henkel Ag & Co. KgaA

- Fujikura Ltd.

Future Outlook

The conductive ink market is likely to see robust growth prospects in the coming years due to factors such as the expansion of printed electronics applications, increased use of wearables and IoT devices, rising demand for photovoltaics, and developments in graphene-based and other nanomaterial conductive inks. New advances in the field of flexible electronics, sustainability, and printing have been driving market growth as well. Increased efforts in building devices that are smart and can generate power from renewable resources, coupled with connecting capabilities, are set to create new possibilities for businesses in the conductive inks industry. Conductive inks are expected to continue their significance in the smart electronics and renewable energy space.

Conductive Inks Industry Development

May 2026: Sun Chemical showcased the latest developments in sustainable inks and coatings for the packaging and labeling industry at Flexo & Labels Expo 2026. (source: sunchemical.com)

February 2026: Henkel showcased the company’s latest advances in conductive ink technologies and functional materials at LOPEC 2026. Among the technologies that were highlighted was its silver-plated copper (SPC) ink technology. This SPC technology is cost-effective with good technical performance. (source: henkel.com)

Conductive Inks Market Segmentation

By Product Type Outlook

- Conductive Silver Ink

- Conductive Polymers

- Conductive Copper Ink

- Conductive Nanotube Inks

- Carbon/Graphene Ink

- Dielectric Ink

- Others

By Application Type Outlook

- Membrane Switches

- Photovoltaic

- Displays

- Automotive

- Biosensors

- Smart Packaging

- Printed Circuit Boards

- Others

By Region Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Conductive Inks Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 3,818.60 Million |

| Market Size Value in 2026 | USD 4,101.21 Million |

| Revenue Forecast by 2034 | USD 6,245.50 Million |

| CAGR | 5.6 % from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The market is projected to grow from USD 3,818.60 million in 2025 to USD 6,245.50 million by 2034.

The market is expected to register a CAGR of 5.6% during the forecast period.

Asia Pacific held the largest market share in 2025 with over 46.5% of total conductive inks market revenue.

DuPont.; Vorbeck Materials Corp.; Sun Chemical Corporation; PPG Industries; Chem Associates, Inc.; Henkel AG; Applied Nanotech Holdings, Inc.; Poly-Ink; Methode Electronics; Henkel Ag & Co. KgaA; and Fujikura Ltd. are among the key players in the market.

The conductive silver ink segment dominated the market in 2025 with over 68.4% of the global revenue share.

The photovoltaic segment led the market with a revenue share of over 33.7% in 2025.

Download Sample Report of Conductive Inks Market

Please fill out the form to request a customized copy of the research report.