Copper Scrap Market Outlook, Growth Analysis, 2026-2034

REPORT DETAILS

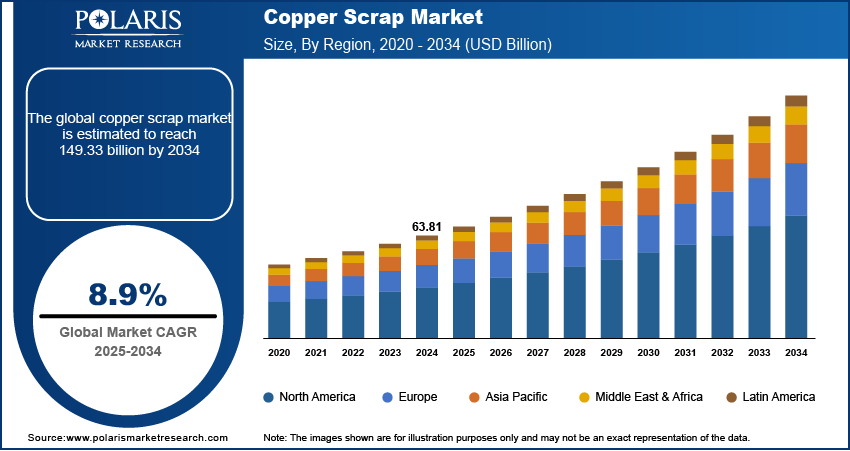

Copper Scrap Market Summary

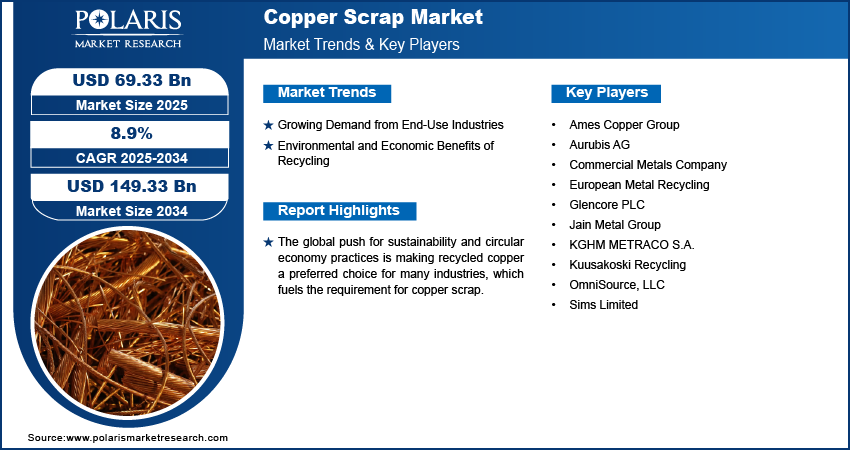

The global copper scrap market size was valued at USD 69.17 billion in 2025 and is anticipated to register a CAGR of 8.9% from 2026 to 2034. The increased global demand for copper, especially from the electrical and electronics and construction industries, boosts the market expansion. In addition, the growing electric vehicle sector and the shift toward green and renewable energy propel the demand for copper scrap. Another key factor is the increasing focus on sustainability and recycling, which promotes the use of scrap copper over newly mined copper to reduce environmental impact.

Market Statistics

Key Takeaways

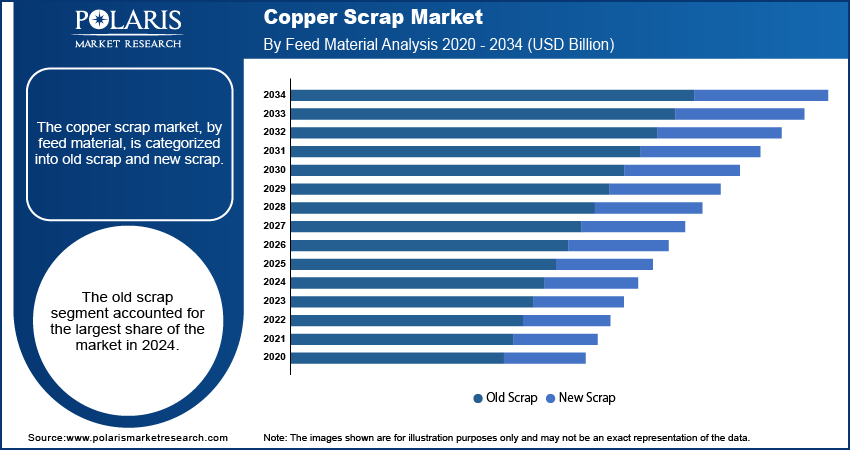

- By feed material, the old scrap segment held the substantial share of 45.3% in 2025 due to the huge, consistent supply of discarded copper from end-of-life products.

- By scrap grade, the #2 copper scrap segment held 19.7% in 2025 as it includes a broad range of widely available materials.

- By application, the wire rod mills segment held the largest share in 2025 with a share of 34.79% since there is high demand for electrical wiring and cables in various sectors.

- By end use, the electrical & electronics segment is the biggest consumer of copper scrap due to widespread use of copper in power cables and transformers, circuit boards, and consumer devices. This segment held approximately 28% of market revenue share.

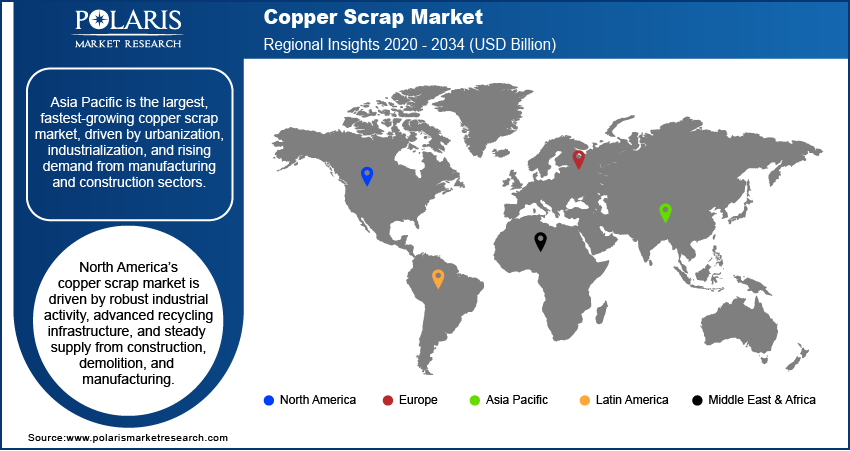

- By region, Asia Pacific held the largest revenue share in 2025, holding approximately 61.43%, due to its massive urbanization and rapid industrialization.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The increasing global focus on a circular economy and sustainable practices is a significant driver. Recycling copper requires much less energy compared to producing it from new ore, which helps reduce carbon emissions and meets the growing demand for eco-friendly materials from various industries. This trend is also encouraged by government policies.

- A major driver is the rising demand from key industries such as construction, electrical and electronics, and electric vehicles. For example, the need for copper in building new infrastructure and producing consumer electronics propels the market growth. Also, the rising requirement for copper in EV batteries and charging stations is boosting the need for new and recycled copper.

- The increasing volatility and price of newly mined copper are pushing manufacturers to look for more affordable alternatives. Scrap copper, which is typically sold at a lower price than new copper, has become a cost-effective option for many companies. This helps them manage their costs while still meeting their production needs.

AI Impact on Copper Scrap Market

- Artificial intelligence (AI) technology is disrupting the copper scrap market. In scrap sorting, AI tools are used due to their accuracy and speed.

- The conventional sorting process includes significant manual labor and can lead to material loss. AI algorithms help cut operational costs by eliminating these risks.

- AI-based robots and vision systems also identify and separate copper from mixed scrap with increased recovery rates and reduced contamination. It help in recovering a high-quality recycled copper, which meets industrial standards and fetches better prices.

- AI-based inspection tools detect impurities in copper scrap more efficiently than manual quality checks, which ensures consistent product quality.

What is Copper Scrap?

The copper scrap involves collecting, processing, and recycling used copper materials from various sources such as old wires, pipes, and electronics. These materials are processed to recover pure copper, which is then used as a raw material for new products. Copper recovery offers a sustainable alternative to mining new copper.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

The increasing urbanization and infrastructure development in developing nations drive the market growth. As countries invest more in building cities, homes, and electrical grids, the demand for copper for wiring, plumbing, and other construction uses goes up. This creates a need for all types of copper, including recycled scrap, to meet the huge demand.

Another important, but often overlooked, driver is the growing complexity of electronic devices. The rise of new technologies such as 5G networks and modern consumer electronics is fueling a constant need for copper, a key material in their components. This trend leads to a steady increase in "new scrap" from manufacturing processes as well as "old scrap" from discarded devices.

Drivers and Trends

Growing Demand from End-Use Industries: Various industries such as electrical and electronics, construction, and transportation rely heavily on copper due to its excellent conductivity and durability. As these sectors expand globally, especially with the growing focus on electrification and technology, the demand for both newly mined and recycled copper increases. This creates a strong pull for copper scrap as a valuable resource to supplement the supply of primary copper.

The need for copper in clean energy technologies is growing rapidly. According to the U.S. Department of Energy (DOE) in its 2023 Critical Materials Assessment, copper was added to the official critical materials list for the first time. The report highlighted the importance of copper for clean energy technologies and its role in meeting the nation's energy goals. Therefore, the increasing demand for copper from fast-growing end-use industries is directly driving the industry growth.

Environmental and Economic Benefits of Recycling: Another significant driver is the increasing focus on sustainability and the economic benefits of using recycled materials. Recycling copper uses much less energy and produces fewer greenhouse gas emissions compared to mining and processing new copper. This makes scrap copper a popular choice for manufacturers who want to lower their environmental impact and meet strict regulations. Additionally, scrap copper is often more affordable than new copper, giving companies a cost advantage.

This is supported by data from the U.S. Geological Survey (USGS). In the Mineral Commodity Summaries 2024 report, it was noted that in 2023, copper recovered from old, post-consumer scrap provided an estimated 150,000 tons of copper. This recovery helped meet 33% of the U.S. copper supply, showing how important recycling is to the overall supply chain. This environmental and economic appeal is actively driving the growth.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Copper Scrap Comparison Table

| Parameter | New Scrap | Old Scrap | Secondary Refined Copper |

| Source | Generated during manufacturing (cuttings, shavings, off-cuts) | End-of-life products (wires, pipes, electronics, buildings) | Produced by refining scrap (both new + old) into pure copper |

| Purity Level | High, clean, less contamination | Lower, often mixed with coatings, alloys, impurities | Very high, near primary copper quality |

| Processing Required | Minimal processing | Extensive sorting, cleaning, and separation | Advanced refining and smelting required |

| Consistency | Uniform and predictable | Variable quality and composition | Highly consistent and standardized |

| Cost | Moderate (cheaper than refined copper) | Lowest cost among all types | Higher due to refining process |

| Availability | Limited to industrial production waste | Large and continuous supply | Depends on scrap availability and refining capacity |

| Usage | Direct reuse in manufacturing | Used after processing in multiple industries | Used like primary copper in high-end applications |

| Recycling Efficiency | Very high (easy to recycle) | Moderate (due to impurities) | High (already refined material) |

| Market Role | Fastest growing segment | Dominant segment (largest share) | Value-added refined output from scrap |

Source: Polaris Market Research Analysis

Segmental Insights

Feed Material Analysis

Based on feed material, the segmentation includes old scrap and new scrap. The old scrap segment held the largest share in 2025. This dominance is attributed to the sheer volume of old copper materials available from sources such as old buildings, appliances, and vehicles. As infrastructure in developed regions ages and is replaced, there is a constant supply of old copper wire, copper tubes, pipes, and other items. The recycling process for old scrap is well-established, with a widespread collection network that includes scrap yards and waste management companies. This abundant and reliable supply makes it a primary source for secondary copper production, especially as industries prefer sustainable materials. The continuous flow of old products reaching the end of their life cycle ensures a steady supply.

The new scrap segment is anticipated to register the highest growth rate during the forecast period. New scrap is the waste material generated during manufacturing and fabrication processes, such as leftover cuttings, shavings, and off-cuts. The quality of new scrap is often higher and more consistent because it has not been exposed to the elements or mixed with other materials. The rapid growth of industries that use large amounts of copper, such as electronics, telecommunications, and electric vehicle manufacturing, is leading to a significant increase in this type of scrap. These industries are focused on efficiency and are quickly adopting recycling practices to reuse this high-quality material in their own production lines, which drives the strong growth of this segment.

Scrap Grade Analysis

Based on scrap grade, the segmentation includes bare bright, #1 copper scrap, #2 copper scrap, and other grades. The #2 copper scrap segment held the largest share in 2024. It includes a wide range of common materials that are more readily available than higher-grade options. This grade typically consists of miscellaneous unalloyed wires, pipes, and other solid metals that may have coatings, solder, or paint. Its prevalence is a result of it being sourced from everyday items and older, less clean sources, such as discarded household items, old plumbing, and some electrical wiring. The process to recycle this material is more involved, as it requires extra steps to remove impurities, but its abundance makes it a cornerstone of the copper recycling industry. The large and steady supply of these materials makes it the most dominant segment.

The bare bright segment is anticipated to register the highest growth rate during the forecast period. This premium-grade scrap is highly sought after because of its purity. It consists of clean, uncoated, and unalloyed copper wire, typically from new manufacturing processes or carefully stripped electrical cables. The rising demand for this high-quality scrap is linked to the growth of industries that require high-purity copper for their products, such as those in the electrical and electronics, and telecommunications sectors. Manufacturers in these fields prefer bare bright because it minimizes the need for further processing, which reduces production costs and energy consumption. The demand for this type of clean, ready-to-use scrap is growing quickly as many industries look to improve efficiency and produce high-quality, sustainable goods.

Application Analysis

Based on application, the segmentation includes wire rod mills, brass mills, ingot makers, foundries, and other industries. The wire rod mills segment held the largest share in 2025. This dominance is attributed to the high demand for electrical wiring and cables, which are essential for everything from building modular construction to telecommunications infrastructure and automotive manufacturing. Wire rod mills use large amounts of high-purity copper scrap, often in the form of bare bright or #1 copper, to produce the wire rods that are later drawn into various sizes of wire. The constant need for new electrical grids, appliances, and electronic devices ensures a steady and massive flow of material to these mills. The ability of wire rod mills to process large volumes of high-grade copper scrap efficiently solidifies this segment as the primary application.

The ingot makers and foundries segment is anticipated to register the highest growth rate during the forecast period. This part uses copper scrap to create copper ingots and cast products. Unlike wire rod mills that need high-purity scrap, ingot makers and foundries can use a broader range of scrap grades, including lower-quality and mixed-alloy materials. The growth in this segment is attributed to the increasing use of specialized copper alloys in various applications, such as industrial machinery, marine parts, and decorative items. As manufacturers look for custom and cost-effective solutions, the use of scrap in foundries becomes more attractive. This flexibility and the growing demand for cast copper products are driving the rapid expansion of the ingot makers and foundries segment.

End Use Analysis

Based on end use, the segmentation includes building & construction, electrical & electronics, industrial machinery & equipment, transportation equipment, and consumer & general products. The electrical & electronics segment held the largest share in 2025. This is because copper is a fundamental component in a vast number of electrical and electronic products due to its high electrical conductivity. Everything from power cables and transformers to circuit boards and consumer electronics such as smartphones and computers relies on copper. The constant innovation and production in this industry, combined with the short lifespan of many electronic devices, create a huge and continuous supply of end-of-life products that are a major source for copper scrap. The sheer volume of copper used in this segment for wiring, connectors, and other components makes it a dominating force.

The transportation equipment segment is anticipated to register the highest growth rate during the forecast period, mainly because of the rapid rise in the production of electric vehicles (EVs). EVs use a much larger amount of copper than traditional gasoline-powered cars, with copper found in their motors, batteries, inverters, and charging infrastructure. As governments and consumers push for cleaner transportation, the demand for EVs is skyrocketing, which is fueling the need for copper. Since manufacturers are focused on sustainability and cost-efficiency, they are increasingly turning to recycled copper from scrapped vehicles and manufacturing processes to meet this demand. The expansion of the transportation equipment sector is driving a need for copper scrap.

Source: Polaris Market Research Analysis

To Understand More About this Research: Request Customization

Real-World Examples

Electrical wiring: New scrap from cable production waste. Secondary refined copper used in power cables and transformers.

Construction materials: Old scrap from buildings (pipes, roofing). Reused after processing in plumbing and structures.

Electronics recycling: Old scrap from phones, circuit boards, appliances. Refined into copper for new electronics.

Automotive parts: New scrap from manufacturing waste. Old scrap from vehicles reused in EV motors and batteries.

Regional Analysis

The Asia Pacific copper scrap market accounted for the largest share in 2024. This is mainly due to the rapid industrialization, massive urbanization, and huge infrastructure projects happening across many countries. This region has a huge demand for copper, driven by its booming manufacturing sectors in electrical and electronics, construction, and transportation. Owing to its high demand, the region is a major importer of copper scrap from other parts of the world to meet its industrial needs.

China Copper Scrap Market Insights

China holds the largest share in the Asia Pacific landscape. China is the largest consumer of copper scrap globally. The country's massive manufacturing and construction industries require enormous volumes of copper, which cannot be fully met by newly mined sources alone. While China has its own domestic scrap collection, it relies heavily on imported scrap to fuel its industrial production. The country's continued economic growth and industrial expansion make it the most influential country in the regional growth.

North America Copper Scrap Market Trends

The North America market for copper scrap is driven by strong industrial activity and a well-developed recycling infrastructure. The region has a consistent supply of old scrap from construction and demolition, as well as new scrap from manufacturing. The increasing focus on sustainability and the need to reduce reliance on primary copper mining have boosted the recycling industry here. This region's demand is also fueled by its large and growing automotive and electrical sectors, especially with the push toward electric vehicles.

U.S. Copper Scrap Market Outlook

The U.S. is a central part of North America, with a strong domestic recycling system and a large network of scrap processors. The country has a high rate of copper recovery from end-of-life products, contributing to a stable domestic supply. A significant portion of the demand in the U.S. comes from wire rod mills and foundries that serve the construction and electrical industries. The U.S. also plays a key role in global trade, exporting a lot of its collected scrap to other parts of the world.

Europe Copper Scrap Market Analysis

Europe is a significant region, known for its strong emphasis on the digital circular economy and strict environmental regulations. These policies promote a high recycling rate, making scrap a vital resource for the continent's manufacturing needs. The demand for copper scrap is high in Europe, particularly from industries such as electrical and electronics, as well as transportation. The region's commitment to reducing carbon emissions and dependence on imported raw materials continues to support the growth of its domestic copper recycling industry.

The Germany copper scrap market stands out as a key country in Europe. Its robust manufacturing base, especially in the automotive and machinery sectors, creates a strong demand for both new and old scrap. Germany has an advanced and efficient recycling infrastructure that allows it to process large volumes of scrap locally. This focus on domestic recycling helps the country maintain a steady supply of copper for its industries and reduces its need to import raw materials.

Source: Polaris Market Research Analysis

To Understand More About this Research: Request Customization

Key Players and Competitive Insights

The market is highly fragmented with a large number of local and regional players, as well as major global companies. These include Aurubis AG, Commercial Metals Company, Glencore PLC, Sims Limited, and OmniSource, LLC. These companies are involved in the collection, processing, and trading of copper scrap on a large scale, giving them a strong position in the global supply chain. The competitive landscape is also influenced by many smaller companies and a complex network of dealers, traders, and brokers.

A few prominent companies include Aurubis AG, Sims Limited, Glencore PLC, Commercial Metals Company, OmniSource, LLC, Ames Copper Group, Jain Metal Group, European Metal Recycling, Kuusakoski Recycling, and KGHM METRACO S.A.

Key Players

- Ames Copper Group

- Aurubis AG

- Commercial Metals Company

- European Metal Recycling

- Glencore PLC

- Jain Metal Group

- KGHM METRACO S.A.

- Kuusakoski Recycling

- OmniSource, LLC

- Sims Limited

Copper Scrap Industry Developments

- April 2026: Jain Resource Recycling reported 38% revenue growth and 65% profit rise in 9MFY26. Fueled by capacity increase and shift to high-value copper products via subsidiary Jain Green Technologies. (Source: ndtvprofit.com)

- April 2026: Rocklink India launched a new recycling facility in Uttar Pradesh. Concentration on permanent magnet alloys (NdFeB, SmCo, AlNiCo) from electric motors and generators. Introduced “Magcycle” model in India. (Source: entrepreneurindia.com)

- October 2025: Aurubis expanded its global recycling presence by commissioning a new copper smelter in Georgia, strengthening its recycled copper processing capacity, enhancing supply chain resilience, and reducing dependence on primary copper mining. (Source: aurubis.com)

- August 2025: Aurubis commissioned a new steam accumulator system at its Lünen recycling site in Germany. (Source: aurubis.com)

- May 2024: Metso launched the heavy-duty Outotec Kaldo L Furnace, designed to melt and process primary and secondary raw materials such as concentrates, copper scrap, anode slimes, and e-waste. (Source: metso.com)

- March 2024: Lithuania, Czech Republic, Latvia, and Estonia proposed to the European Union a ban on imports of Russian ferrous scrap, copper, and aluminum to curb reliance on Russian materials. (Source: gmk.center)

Copper Scrap Market Segmentation

By Feed Material Outlook (Revenue – USD Billion, 2021–2034)

- Old Scrap

- New Scrap

By Scrap Grade Outlook (Revenue – USD Billion, 2021–2034)

- Bare Bright

- #1 Copper Scrap

- #2 Copper Scrap

- Other Grades

By Application Outlook (Revenue – USD Billion, 2021–2034)

- Wire Rod Mills

- Brass Mills

- Ingot Makers

- Foundries

- Other Industries

By End Use Outlook (Revenue – USD Billion, 2021–2034)

- Building & Construction

- Electrical & Electronics

- Industrial Machinery & Equipment

- Transportation Equipment

- Consumer & General Products

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- Suth Korea

- Indnesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- Suth Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Copper Scrap Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 69.17 billion |

| Market Size in 2026 | USD 75.04 billion |

| Revenue Forecast by 2034 | USD 148.44 billion |

| CAGR | 8.9% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Insights |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The global market size was valued at USD 69.17 billion in 2025 and is projected to grow to USD 148.44 billion by 2034.

The global market is projected to register a CAGR of 8.9% during the forecast period.

Asia Pacific dominated the market share in 2025.

A few key players in the market include Aurubis AG, Sims Limited, Glencore PLC, Commercial Metals Company, OmniSource, LLC, Ames Copper Group, Jain Metal Group, European Metal Recycling, Kuusakoski Recycling, and KGHM METRACO S.A.

The old scrap segment accounted for the largest share of the market in 2025.

The bare bright segment is expected to witness the fastest growth during the forecast period.

Download Sample Report of Copper Scrap Market

Please fill out the form to request a customized copy of the research report.