U.S. Building Envelope Adhesives & Sealants Market Report Outlook, 2025-2034

REPORT DETAILS

Market Statistics

Market Overview

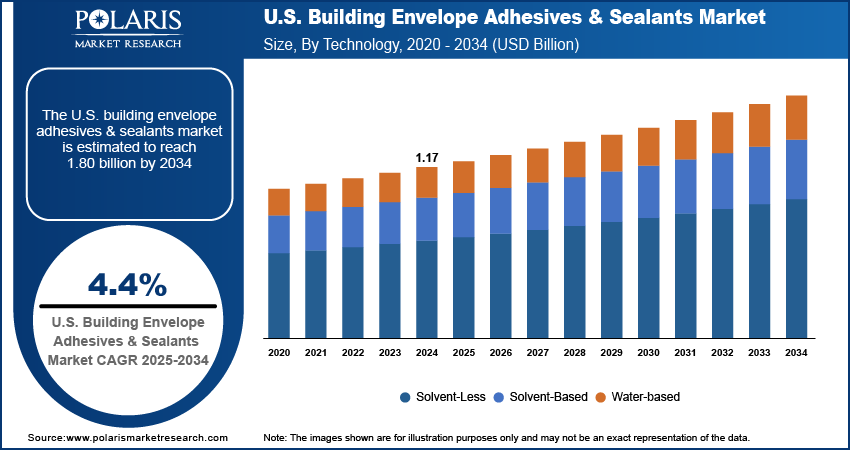

The U.S. building envelope adhesives & sealants market size was valued at USD 1.17 billion in 2024 and is anticipated to register a CAGR of 4.4% from 2025 to 2034. Main growth factors for the market are a rise in construction and infrastructure projects and a growing focus on energy efficiency. The increasing use of environmentally friendly products and the need for durable materials in buildings boost the demand for building envelope adhesives and sealants in the U.S.

Key Insights

- By technology, the water-based segment held the largest share in the U.S. market in 2024. The dominance is driven by a growing preference for products that are better for the environment and contain fewer harmful substances. Their reliability and wide range of use in different building projects have made them a popular choice.

- By adhesive resin, the polyurethane segment led the market in 2024 due to its balanced properties. Its strong adhesion, flexibility, and resistance to weather make it a versatile material that works well on many different surfaces in construction.

- By adhesive applications, the roofing segment dominated the market in 2024 due to the crucial role of adhesives and sealants in protecting the main shield of a building from harsh weather and other outside elements. The constant need for both new roof installations and repairs drives demand.

- By sealant resin, the silicone segment held the largest market share in 2024 due to its superior weather resistance, UV stability, and flexibility. These qualities make it a very reliable choice for sealing joints, windows, and other building envelope components.

- By sealant application, the sealant application for wall joints is a major segment. Sealants are essential for creating durable and airtight seals in a building's walls, which is crucial for overall energy efficiency and protecting the structure from moisture.

Industry Dynamics

- There is a growing focus on energy efficiency in buildings. This has led to an increased demand for high-performance adhesives and sealants that improve the insulation and airtightness of building structures, which helps lower energy consumption.

- The rising number of new construction and renovation projects, particularly in the residential and commercial sectors, is a major growth factor. These projects rely on these products for applications such as roofing, walls, and flooring to ensure durability.

- The industry is moving rapidly toward sustainable and eco-friendly building materials. This is boosting the use of adhesives and sealants that have low or zero volatile organic compound (VOC) content, which is in line with strict government rules and green building certifications.

Market Statistics

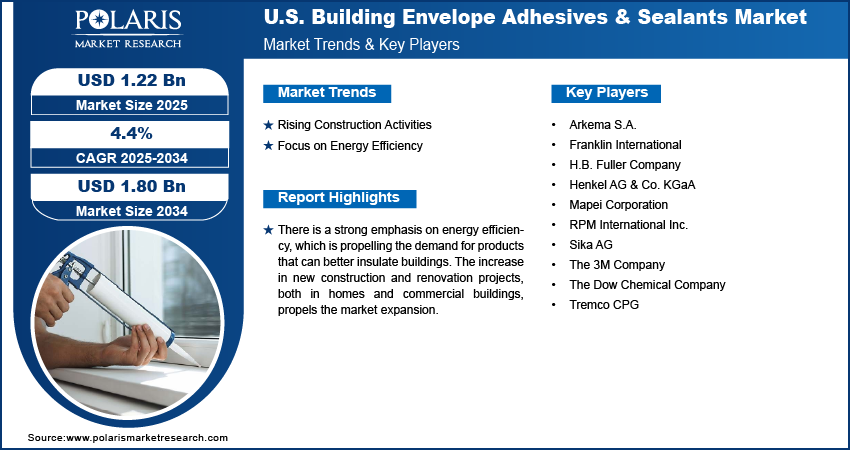

- 2024 Market Size: USD 1.17 billion

- 2034 Projected Market Size: USD: 1.80 billion

- CAGR (2025–2034): 4.4%

The U.S. building envelope adhesives and sealants market includes a wide range of products used to protect a building's structure from outside elements such as air, moisture, and heat. These materials are used in many parts of a building's shell, such as the roof, walls, windows, and floors, to ensure they are sealed properly. This helps improve the building's energy efficiency and makes it more durable over time.

Source: Polaris Market Research Analysis

One factor influencing this market is the shift toward using advanced construction adhesive methods, such as modular and prefabricated buildings. These methods involve building large parts of a structure in a factory before they are moved to the building site. This has increased the need for specialized adhesives and sealants that can create strong bonds on a variety of materials and cure quickly, which helps speed up the building process.

Another key driver is the increasing number of strict building and safety regulations. These rules require building materials to meet certain performance standards, especially for things such as fire safety and emissions. For example, some government regulations require that materials used in buildings, such as adhesives and sealants, have low levels of volatile organic compounds (VOCs) to improve indoor air quality. The WHO provides guidance on air quality that has led to these kinds of regulations being adopted by various jurisdictions.

Drivers and Trends

Rising Construction Activities: The growing U.S. construction industry propels the demand for building envelope adhesives and sealants. As new buildings are constructed and older ones are renovated, there is a consistent need for these products to ensure the structures are properly sealed and protected. This includes everything from residential homes to commercial and public infrastructure projects. The growth in this sector directly drives the need for more materials to seal the building envelopes.

According to a U.S. Census Bureau report from August 2025 titled "Monthly Construction Spending, June 2025," the value of construction put in place was estimated at a seasonally adjusted annual rate of over $2.13 trillion in June 2025. This shows a strong level of ongoing construction work across the country. The constant activity in new construction and remodeling ensures a steady need for building envelope adhesives and sealants.

Focus on Energy Efficiency: There is a growing emphasis on creating buildings that are more energy efficient. This is driven by environmental concerns and the desire to lower energy costs for both owners and tenants. Adhesives and sealants are used to achieve this goal as they prevent air and moisture leaks, which can greatly reduce a building's insulation effectiveness. With the use of high-performance sealing products, buildings can maintain stable indoor temperatures and lower the amount of energy needed for heating and cooling.

A September 2023 report from the U.S. Department of Energy's National Renewable Energy Laboratory, titled "NREL Researchers Reveal How Buildings Across United States Do—and Could—Use Energy," highlighted that buildings are responsible for a large percentage of total energy use in the U.S. The report showed that residential buildings in Ohio could reduce their energy use by a significant amount by adding insulation and air sealing improvements. This shows that the increasing focus on saving energy in buildings propels the demand for products that make them more efficient.

Source: Polaris Market Research Analysis

Segmental Insights

Technology Analysis

Based on technology, the U.S. building envelope adhesives & sealants market segmentation includes solvent-less, solvent-based, and water-based. The water-based segment held the largest share in 2024. The high demand for these products is attributed to their environmentally friendly nature and minimal presence of harmful substances. Construction companies and builders have become more aware of the environmental impact of their materials. As a result, they are moving toward solutions that follow green building standards. Water-based technologies are considered as a safe and reliable option for numerous applications, from residential construction to large commercial projects. Their performance in sealing gaps and providing strong bonds for various building components makes them a go-to choice, which has allowed this segment to take the lead in terms of overall market share. This high level of use and preference for water-based products is a key reason for the segment's strong position in the industry.

The solvent-less segment is anticipated to register the highest growth rate during the forecast period. This high growth is fueled by an increasing demand for products that are more sustainable and have low or no volatile organic compound (VOC) emissions. Many countries and regions have imposed stringent rules to control air pollution from construction materials. Hence, companies demand newer and better alternatives. The solvent-less products, which include reactive adhesives, provide high performance without the use of harsh chemicals, making them a good choice for projects that need to meet strict environmental and health standards. As more companies invest in developing these advanced formulas and as regulations continue to get stricter, this segment is expected to report rapid expansion during 2025–2034.

Adhesive Resin Analysis

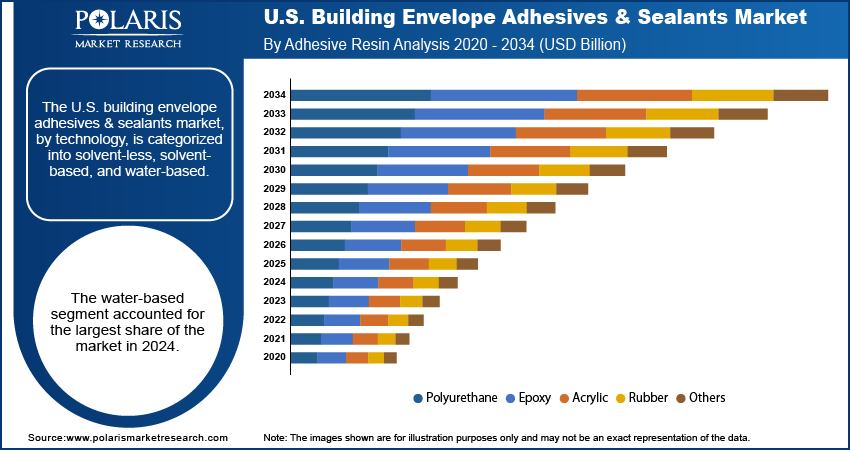

Based on adhesive resin, the U.S. building envelope adhesives & sealants market segmentation includes polyurethane, epoxy, acrylic, rubber, and others. The polyurethane segment held the largest share in 2024. These products are widely used due to their excellent balance of properties, including strong adhesion, flexibility, and resistance to weather. Polyurethane is a versatile material that works well on a variety of surfaces, such as concrete, wood, and metals, which are all common in building projects. Its ability to create a lasting and effective seal for gaps and joints in walls, floors, and roofing is a major reason for its high demand. The versatility and reliable performance of polyurethane have made it the go-to resin for many builders and contractors, giving it a commanding share of the overall market.

The acrylic segment is anticipated to register the highest growth rate during the forecast period. The rise in demand for acrylic-based products is attributed to their cost-effectiveness and good performance in many building applications. These products are easy to apply, quick to dry, and can be painted over. Therefore, they are popular for large commercial projects and home renovations. Furthermore, ongoing developments in technology have led to better acrylic formulas with improved flexibility and resistance to weather, which is helping them compete with other resin types. The strong demand for these products is also being supported by an increased focus on using materials that are safe for people and the environment, as many acrylic formulas are water-based with low emissions. This combination of strong performance and environmental benefits is a key reason propelling the expansion of the acrylic segment.

Adhesive Applications Analysis

Based on adhesive applications, the U.S. building envelope adhesives & sealants market segmentation includes roofing, walls, subfloors, and others. The roofing segment held the largest share in 2024. Roof is the primary shield of a building, and it must withstand harsh weather, temperature changes, and constant exposure to the sun. The proper installation of roofing materials, including tiles, shingles, and membranes, relies heavily on high-quality adhesives and sealants to create a tight and durable seal. These products are important for protecting a building from moisture and air leaks, which helps with energy efficiency and the overall structural health of the building. With new construction and the ongoing need for roof repair and replacement, the demand for these products remains consistently high.

The walls segment is anticipated to register the highest growth rate during 2025–2034. The increased use of modern building methods and materials for walls, such as prefabricated panels and insulated siding, propels the demand for specialized adhesives and sealants. The materials require specific bonding agents to be installed correctly and to ensure their performance over time. Additionally, there is a rising focus on making walls more airtight to enhance a building's energy efficiency. This trend is leading to the rising use of advanced adhesives and sealants to seal gaps and cracks effectively. It reduces heat loss and helps create more sustainable buildings. The ongoing trend in creating high-performance building exteriors is contributing to the growth of the application segment.

Sealant Resin Analysis

Based on sealant resin, the U.S. building envelope adhesives & sealants market segmentation includes polyurethane, silicone, acrylic, silane modified polymer, and others. The silicone segment held the largest share in 2024. The demand for silicone-based sealants is high due to their excellent performance features. These products offer superior weather resistance, UV stability, and flexibility, which are critical for protecting a building's exterior from the elements. Silicone sealants can withstand extreme temperatures without losing their effectiveness. This benefit makes them a reliable choice for sealing joints, windows, and other parts of the building envelope. This reliability, as well as their long lifespan and strong adhesion to different materials, has made silicone sealants a preferred option for many builders, which is contributing to the dominating share of the segment.

The polyurethane segment is anticipated to register the highest growth rate during the forecast period. The growth in demand for polyurethane sealants is a result of their strong bonding capabilities and ability to be painted over, which is a major benefit in many construction projects. They are highly valued for their strength, flexibility, and resistance to chemicals. This makes them suitable for a wide range of applications, especially where there is a lot of movement in a building, such as expansion joints and concrete structures. Polyurethane can provide a durable and flexible seal that can also be finished with paint. Thus, it has become a popular choice among construction players.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

The U.S. building envelope adhesives & sealants market consists of several key players, including H.B. Fuller, Henkel, Sika, The Dow Chemical Company, and Tremco CPG. The companies are focused on a variety of strategies to gain a competitive advantage, such as developing new products that are more eco-friendly and improving existing product formulas to offer better performance. They also work on expanding their reach through mergers and acquisitions and building stronger supply chains. The competition is based on product performance, price, customer support, and the ability to meet specific building codes and regulations.

A few prominent companies include 3M Company, The Dow Chemical Company, Henkel AG & Co. KGaA, H.B. Fuller Company, Sika AG, Arkema S.A., RPM International Inc., Franklin International, Tremco CPG, and Mapei Corporation.

Key Players

- Arkema S.A.

- Franklin International

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Mapei Corporation

- RPM International Inc.

- Sika AG

- The 3M Company

- The Dow Chemical Company

- Tremco CPG

U.S. Building Envelope Adhesives & Sealants Industry Developments

March 2025: H.B. Fuller launched a new commercial roofing adhesive called Millennium PG-1 EF ECO2. This product uses a unique technology that is powered by atmospheric gases instead of traditional chemical propellants, which helps reduce its environmental impact.

U.S. Building Envelope Adhesives & Sealants Market Segmentation

By Technology Outlook (Revenue – USD Billion, 2020–2034)

- Solvent-Less

- Solvent-Based

- Water-Based

By Adhesive Resin Outlook (Revenue – USD Billion, 2020–2034)

- Polyurethane

- Epoxy

- Acrylic

- Rubber

- Others

By Adhesive Applications Outlook (Revenue – USD Billion, 2020–2034)

- Roofing

- Walls

- Subfloors

- Others

By Sealant Resin Outlook (Revenue – USD Billion, 2020–2034)

- Polyurethane

- Silicone

- Acrylic

- Silane Modified Polymer

- Others

By Sealant Application Outlook (Revenue – USD Billion, 2020–2034)

- Facade Panel Fixing

- Wall Joints

- Sanitary

- Passive Fire Protection

- Others

U.S. Building Envelope Adhesives & Sealants Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 1.17 billion |

| Market Size in 2025 | USD 1.22 billion |

| Revenue Forecast by 2034 | USD 1.80 billion |

| CAGR | 4.4% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Insights |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The market size was valued at USD 1.17 billion in 2024 and is projected to grow to USD 1.80 billion by 2034.

The market is projected to register a CAGR of 4.4% during the forecast period.

A few key players in the market include 3M Company, The Dow Chemical Company, Henkel AG & Co. KGaA, H.B. Fuller Company, Sika AG, Arkema S.A., RPM International Inc., Franklin International, Tremco CPG, and Mapei Corporation.

The water-based segment accounted for the largest share of the market in 2024.

The acrylic segment is expected to witness the fastest growth during the forecast period.

Download Sample Report of U.S. Building Envelope Adhesives & Sealants Market

Please fill out the form to request a customized copy of the research report.