Data Center Liquid Cooling Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Data Center Liquid Cooling Market Summary

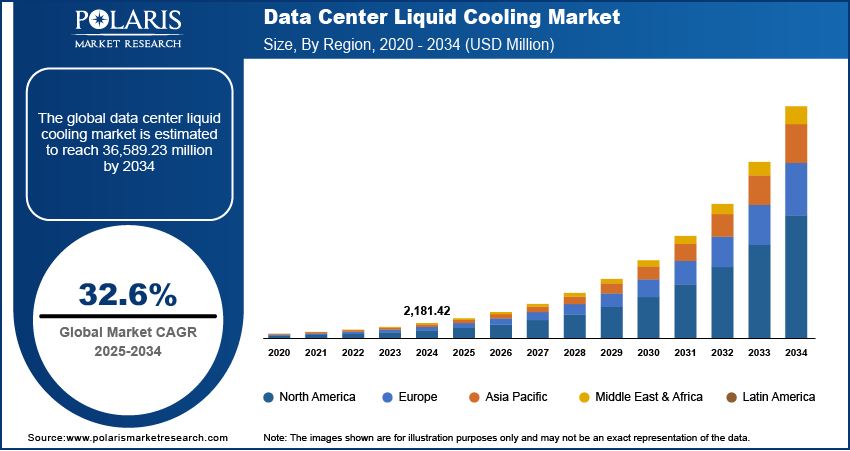

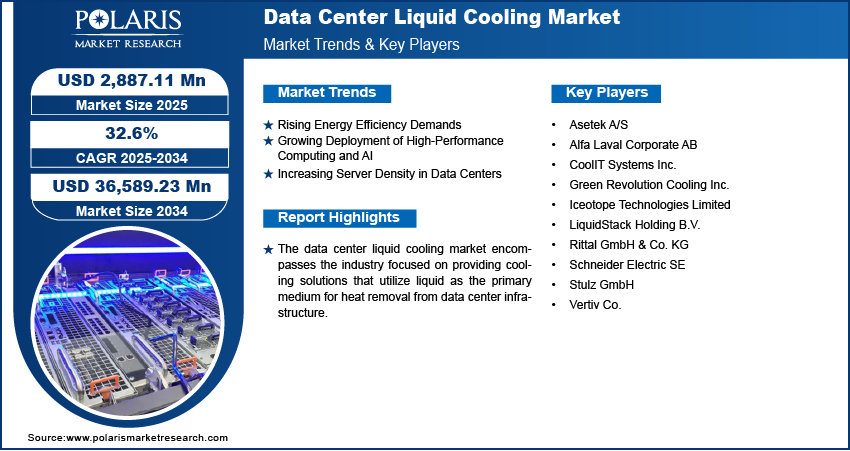

The data center liquid cooling market size was valued at USD 2,887.48 million in 2025 and is projected to register a CAGR of 32.6% from 2026 to 2034. The industry is driven by growing demand for higher energy efficiency and rising heat densities. The growing need for sustainability, the rising focus on reducing operational costs, and the widespread adoption of high-performance computing all drive demand for data center liquid cooling solutions.

Market Statistics

Key Takeaways

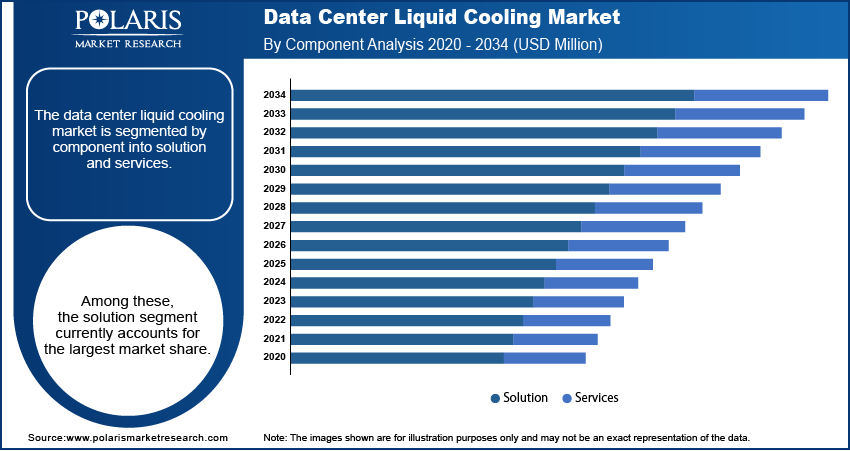

- The solution segment held 72.2% of the revenue share in 2025. This dominance is attributed to the growing demand for the physical infrastructure and technologies that comprise liquid cooling systems.

- The hyperscale data center segment held 41.2% of the revenue share in 2025. This is primarily due to the massive scale and high power densities characteristic of hyperscale facilities operated by major cloud service providers and internet companies.

- The IT & telecom sector is expected to have the 23.2% data center liquid cooling market share during the forecast period. This can be associated with the intensive data processing and storage required by telecommunication firms and their service providers.

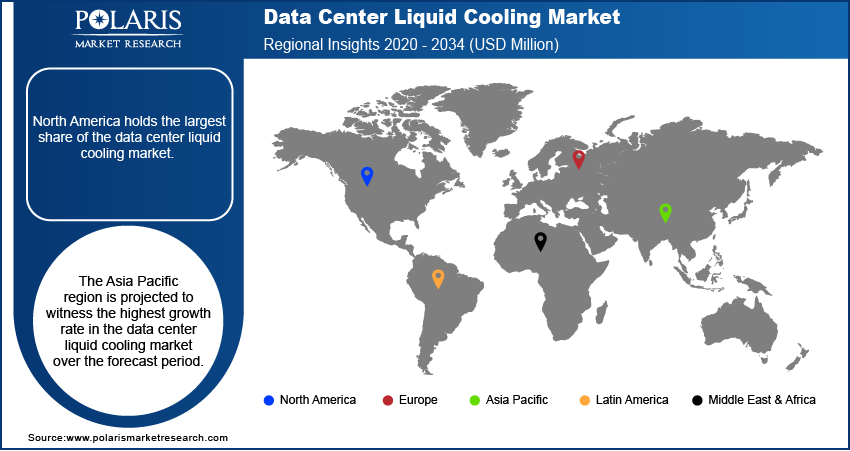

- North America held the largest revenue share of 37.6% in 2025, driven by numerous hyperscale data centers operated by major cloud service providers. The dominance is fueled by a strong emphasis on technological advancements and early adoption of advanced cooling solutions.

- The Asia Pacific data center liquid cooling industry is projected to grow at the highest CAGR at 33.6% during the forecast period. This growth is fueled by the increasing investments in data center infrastructure to support the burgeoning digital economy across countries, such as China and India.

Industry Dynamics

- The increasing demand for energy-efficient cooling solutions is a crucial driver of market growth for data center liquid cooling.

- The growing deployment of high-performance computing (HPC) and artificial intelligence (AI) workloads, including AI data centers, is driving demand for advanced cooling technologies, such as liquid cooling.

- Rising server density within data centers is expected to offer lucrative opportunities for the market during the forecast period.

- The high capital expenditure requirements hinder the adoption of data center liquid cooling systems.

AI Impact on Data Center Liquid Cooling Market

- Artificial intelligence (AI) is reshaping the data center liquid cooling market ecosystem, driving rapid innovation and infrastructure upgrades.

- AI tools dynamically optimize cooling by leveraging real-time heat maps, energy sourcing strategies, and predictive fault detection.

- AI-integrated control systems and predictive maintenance enhance leak detection, coolant management, and power usage effectiveness (PUE) for liquid cooled deployments.

- Edge computing and on-prem AI deployments are driving demand for small-scale liquid cooling solutions that perform well at higher temperatures.

- The growth in AI data centers and GPUs has also been driving an increase in rack power density, beyond the capacity of air-based cooling. The growth in AI data center cooling is therefore moving towards methods such as liquid-based, direct-to-chip, or immersion-based cooling, specifically for GPUs.

- AI-controlled systems optimize cooling through predictive maintenance and optimal coolant distribution. On the other hand, edge or on-premises installations have fueled interest in liquid cooling solutions that are small enough to cool high-temperature areas effectively.

What is Liquid Cooling?

Liquid cooling is a thermal management method that uses fluids—typically water or specialized coolants—to absorb and transfer heat away from electronic components like CPUs, GPUs, and servers. The liquid flows through plates or pipes, takes heat from components, and moves it to a radiator to release it. It is better than air cooling because it removes heat faster, manages high power systems, and uses less energy.

The data center liquid cooling market is gaining momentum as traditional air-cooling methods struggle to handle the heat generated by high-density data centers. Data center liquid cooling effectively removes and dissipates heat generated by servers, processors, and Graphics Processing Units in a direct, efficient manner. Data center liquid cooling has emerged as an essential component of thermal management design in data centers today. Compared to liquid cooling and air cooling, liquid cooling has higher densities and lower energy costs.

Source: Polaris Market Research Analysis

The data center liquid cooling market is the sector focused on providing cooling solutions that use liquid coolants rather than air to manage the heat generated by data center equipment. The market is experiencing growth driven by demand for High Performance Computing (HPC), Artificial Intelligence (AI), and cloud computing. Such applications generate immense heat. Air cooling, in this regard, has become inefficient. Liquid cooling technologies, such as direct-to-chip and immersion cooling, are superior. They provide better temperature regulation, require less power consumption, and enable more servers to be accommodated in a given area. These attributes are paramount in a contemporary data center.

The main driver is the increasing need for energy efficiency and sustainability, because liquid cooling systems use significantly less power than air-cooling systems. Additionally, government regulations and green initiatives push data centers to reduce their carbon footprint. Further advances in technology have made liquid cooling highly viable, with new modular designs easing installation and allowing for scalability. For that matter, the increase in deployment of high-density servers and the rise in operational costs associated with traditional methods act as additional accelerants toward switching to liquid cooling solutions.

Industry Dynamics

Rising Energy Efficiency Demands

The current trend toward energy-efficient data center infrastructure is also driving the adoption of liquid cooling technology, as traditional airflow-based cooling systems are becoming ineffective and power-hungry in high-density environments. The liquid cooling system provides an energy-efficient data center cooling solution by enabling the cooling of data servers or systems at a short distance. This increases thermal efficiency in data centers.

According to a 2021 study published in Nature Energy, data centers globally accounted for approximately 1% of total electricity consumption, and this figure is projected to grow. The U.S. Department of Energy notes that cooling can account for a substantial portion of a data center's operational expenses. A more feasible alternative to traditional air-cooling technology is liquid-based cooling, which is more efficient at removing heat. The economic and environmental benefits of energy efficiency have become a significant factor in the growing demand for energy-efficient cooling solutions.

Growing Deployment of High-Performance Computing and AI

The increasing demand for high-performance computing and AI applications, such as data centers for AI, is a major driver of the adoption of advanced cooling systems like liquid cooling. This is due to the processing units and related components they use, which produce more heat than in other applications. The National Institutes of Health recognizes the growing trend of deploying HPC across scientific communities that require heavy cooling systems. Air-cooling systems may fail to cool the large amounts of heat generated by these HPC applications; hence, effective cooling measures for these applications can be an important factor in transforming the market for advanced cooling solutions.

Increasing Server Density in Data Centers

Higher server densities in high-density data centers remain a major driver of the data center liquid cooling market. Operators face the challenge of increased heat generation as they seek to conserve space, pack more servers into the same area, and keep up with the growing demand for data storage. High server densities make air-cooling designs struggle with airflow and hotspots. Liquid cooling solutions overcome these challenges by uniformly cooling compact spaces, enabling higher equipment density without compromising performance or uptime.

Source: Polaris Market Research Analysis

Immersion vs Direct-to-Chip vs Air Cooling

| Type | How it works | Cooling efficiency | Use Case | Limitation |

| Immersion Cooling | Servers fully placed in liquid coolant | Very high, uniform cooling | High-density data centers, AI workloads | High initial cost, complex maintenance |

| Direct-to-Chip Cooling | Liquid flows through plates on CPU/GPU | High, targets main heat components | HPC, GPU-heavy systems | Partial cooling, still needs air support |

| Air Cooling | Uses fans and airflow to remove heat | Lower compared to liquid | Traditional data centers | Less efficient for high density, higher energy use |

Source: Polaris Market Research Analysis

Segmental Insights

Market Assessment By Component

The solution segment accounts for the largest data center liquid cooling market share in 2025. This is largely due to the fundamental requirement for the physical infrastructure that underpins liquid cooling technologies. This includes hardware components such as cooling units, pumps, heat exchangers, and fluids that are crucial to establishing a liquid cooling infrastructure in a data center. The substantial investments required to deploy these systems to address increasing thermal management challenges contribute to the solution segment's significant share.

The services segment is anticipated to exhibit the highest growth rate over the anticipated years. This growth is driven by the increasing complexity of liquid cooling deployments and the need for specialized expertise in installation, maintenance, and optimization. With an increase in the number of data centers implementing such advanced cooling solutions, the requirement for professional services such as consulting, design, and implementation is expected to increase substantially. The need to provide optimal cooling for such expensive IT equipment is a paramount requirement, driving the growth of the services market.

Market Evaluation By Data Center Type

The hyperscale data center segment holds the largest share during the forecast period. Notably, such a high share is attributed to the massive scale and high power density of hyperscale data centers, which are common among giant cloud service providers and internet companies. Due to the large server farms, data centers produce a lot of heat; hence, the need for advanced cooling systems to cool the surrounding areas. The market is growing as adoption worldwide increases; many such setups are being implemented in hyperscale data centers.

The colocation data center market is expected to grow at the highest rate in the coming years. This growth rate has been fueled by enterprises that use colocation services to outsource their data center infrastructure when High-Performance Computing is needed. Since colocation sites host clients with heavy workloads, liquid cooling solutions have been widely adopted to gain a competitive edge. It is also driven by the scalability and flexibility of the colocation provider, combined with the growing demand for advanced cooling required to serve a diverse customer base, which continues to drive strong segment growth.

Market Assessment By End-Use

The IT & telecom sector is expected to account for the largest share in the anticipated period. This is mainly because of the huge volume of information that the telecom companies and their service providers deal with day in and day out, both in processing and storage. Data traffic continues to increase yearly. The rollout of 5G networks has also increased the pressure. Besides this, the telecom firms are increasingly becoming dependent on cloud-based services. For these reasons, state-of-the-art cooling systems are increasingly required to keep data centers running efficiently and reliably. The large scale of operations and high power consumption in IT and telecom data centers are significant factors contributing to their market dominance.

The healthcare sector is anticipated to experience the highest growth rate in the data center liquid cooling market during the forecast period. This rapid growth is attributed to the increasing adoption of digital health records, the rise of telemedicine, and the growing use of advanced technologies like AI in diagnostics and treatment. These applications generate significant data processing requirements, requiring high-performance computing infrastructure that demands efficient liquid cooling solutions. Furthermore, stringent regulatory requirements for data security and patient privacy are driving investments in robust, reliable data center infrastructure in the healthcare industry, thereby accelerating the adoption of liquid cooling technologies.

Source: Polaris Market Research Analysis

Regional Analysis

The North America data center liquid cooling market is expected to hold the largest share during the forecast period. This is because a large number of hyperscale data centers are operated by major cloud service providers, largely due to their strong focus on technological innovation and early adoption of new cooling solutions. Besides, strict energy-efficiency standards and government-led initiatives for sustainable data center operations in the region have led to increased adoption of liquid cooling technologies. Strong investments in data infrastructure and increasing demand for high-performance computing across industries will continue to solidify North America's leading position.

Asia Pacific data center liquid cooling market is also anticipated to grow at the fastest pace during the forecast period. This is due to rising interest in developing data centers to meet the evolving demands of the growing digital economy in countries such as China, India, and Southeast Asia. Furthermore, the rising demand for cloud services, the surge in the use of the internet, and the growing demand for data-intensive services such as artificial intelligence and big data analytics are some of the chief drivers for the growing interest in the use of data center liquid cooling solutions in the Asia Pacific region, hence making it the fastest-growing region.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

Some of the major players in the data center liquid cooling market include Vertiv Co., Schneider Electric SE, Rittal GmbH & Co. KG, CoolIT Systems Inc., Asetek A/S, LiquidStack Holding B.V., Green Revolution Cooling Inc., Stulz GmbH, Alfa Laval Corporate AB, and Iceotope Technologies Limited. These companies are actively offering a range of liquid cooling solutions and services for data centers.

The market involves large infrastructure providers as well as firms specializing in cooling solutions. The rivalry occurs through innovation, energy costs, pricing, and the adaptability of solutions to specific niches of the data center market. The need to extend their lines through partnerships, collaborations, or acquisitions has been prevalent among the players. The demand for HPC applications and eco-friendly cooling solutions has enhanced competition. This, in turn, is compelling vendors to offer highly advanced liquid cooling solutions.

List of Key Companies in Data Center Liquid Cooling Industry

- Asetek A/S

- Alfa Laval Corporate AB

- CoolIT Systems Inc.

- Green Revolution Cooling Inc.

- Iceotope Technologies Limited

- LiquidStack Holding B.V.

- Rittal GmbH & Co. KG

- Schneider Electric SE

- Stulz GmbH

- Vertiv Co.

Data Center Liquid Cooling Industry Developments

- April 2026: LG Electronics presented its Direct-to-Chip cooling lineup at Data Centre World 2026. The solution targets high-heat AI data center environments. Source: www.marketscreener.com

- April 2026: Accelsius introduced general availability of its NeuCool IR150 system. It is a two-phase liquid cooling solution. It can scale from single racks to full data center deployments. Source: www.businesswire.com

- March 2026: Panasonic entered the European market with its liquid cooling systems business. The focus is on generative AI data center operators. Source: news.panasonic.com

- February 2026: Schneider Electric set up a new liquid cooling manufacturing facility in Bengaluru, India. The expansion strengthens its Motivair portfolio. It focuses on supporting high-density and AI-driven data center infrastructure in the region. Source: www.se.com

- May 2025: Vertiv announced a collaboration with Compass Datacenters to develop a novel cooling solution that integrates both liquid and air-cooling capabilities. (Source: www.compassdatacenters.com)

- October 2024: Schneider Electric, a key player in the energy management and automation sector, finalized its acquisition of a controlling interest in Motivair Corporation. Motivair specializes in liquid cooling and advanced thermal management solutions for high-performance computing and data centers. (Source: www.motivaircorp.com)

Data Center Liquid Cooling Market Segmentation

By Component Outlook (Revenue – USD Million, 2021–2034)

- Solution

- Direct Liquid Cooling

- Indirect Liquid Cooling

- Services

- Design and Consulting

- Installation and Deployment

- Maintenance and Support

By Type of Cooling Outlook (Revenue – USD Million, 2021–2034)

- Immersion Cooling

- Cold Plate Cooling

- Spray Liquid Cooling

By Data Center Type Outlook (Revenue – USD Million, 2021–2034)

- Wholesale

- Enterprise

- Hyperscale

- Colocation

- Others

By End-Use Outlook (Revenue – USD Million, 2021–2034)

- IT & Telecom

- Retail

- Healthcare

- BFSI

- Media & Entertainment

- Others

By Regional Outlook (Revenue-USD Million, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Future Outlook

AI and high-performance computing workloads are rising and generating high heat. These systems need better cooling as air cooling struggles in high-density settings. Demand is also increasing due to the need for energy efficiency and lower operating costs in data centers. Growth of hyperscale data centers and increasing server density will help adoption further. Companies are focusing on sustainable and efficient cooling systems. Liquid cooling will become more common in modern infrastructure. It will play a key role in supporting next-generation data centers and AI-driven operations.

Data Center Liquid Cooling Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 2,887.48 Million |

| Market Size in 2026 | USD 3,818.40 Million |

| Revenue Forecast by 2034 | USD 36,593.53 Million |

| CAGR | 32.6% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD million, 2021–2034, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Data Center Liquid Cooling Market FAQ's

The market was valued at USD 2,887.48 million in 2025. It is expected to reach USD 36,593.53 million by 2034.

The main methods of liquid cooling are direct liquid cooling, immersion cooling, cold plate cooling, and spray liquid cooling. All of them are aimed at cooling in high-density systems.

The increasing workload of AI applications, the demands of high-performance computing, energy efficiency requirements, and server densities are all driving the growing requirement for liquid cooling technologies because air-based cooling is unable to handle the additional heat.

North America is at the forefront of the data center liquid cooling market because of the large hyperscale data centers it possesses. Asia Pacific has emerged as the second-fastest-growing market. This is mainly because of the digital expansion in countries like China and India.

The solution segment accounted for the larger share of the market in 2025.

High initial investment is a significant concern. Complexity in installing and managing liquid cooling systems is another concern. Maintenance is a concern as well. Lack of standardization is a problem. All these factors hinder the adoption of liquid cooling technology.

Data center liquid cooling is a method of dissipating heat generated by IT equipment using a liquid coolant instead of air. In this system, a liquid, typically water or a specialized dielectric fluid, circulates through cooling loops and cold plates that are in direct contact with heat-generating components like CPUs, GPUs, and memory modules. The liquid absorbs the heat, which is then transferred away from the equipment to a heat exchanger, where it is cooled before being recirculated.

Download Sample Report of Data Center Liquid Cooling Market

Please fill out the form to request a customized copy of the research report.