Europe Edge Computing Market Demands, Industry Report, 2024-2032

REPORT DETAILS

REPORT DETAILS

Europe Edge Computing Market Summery

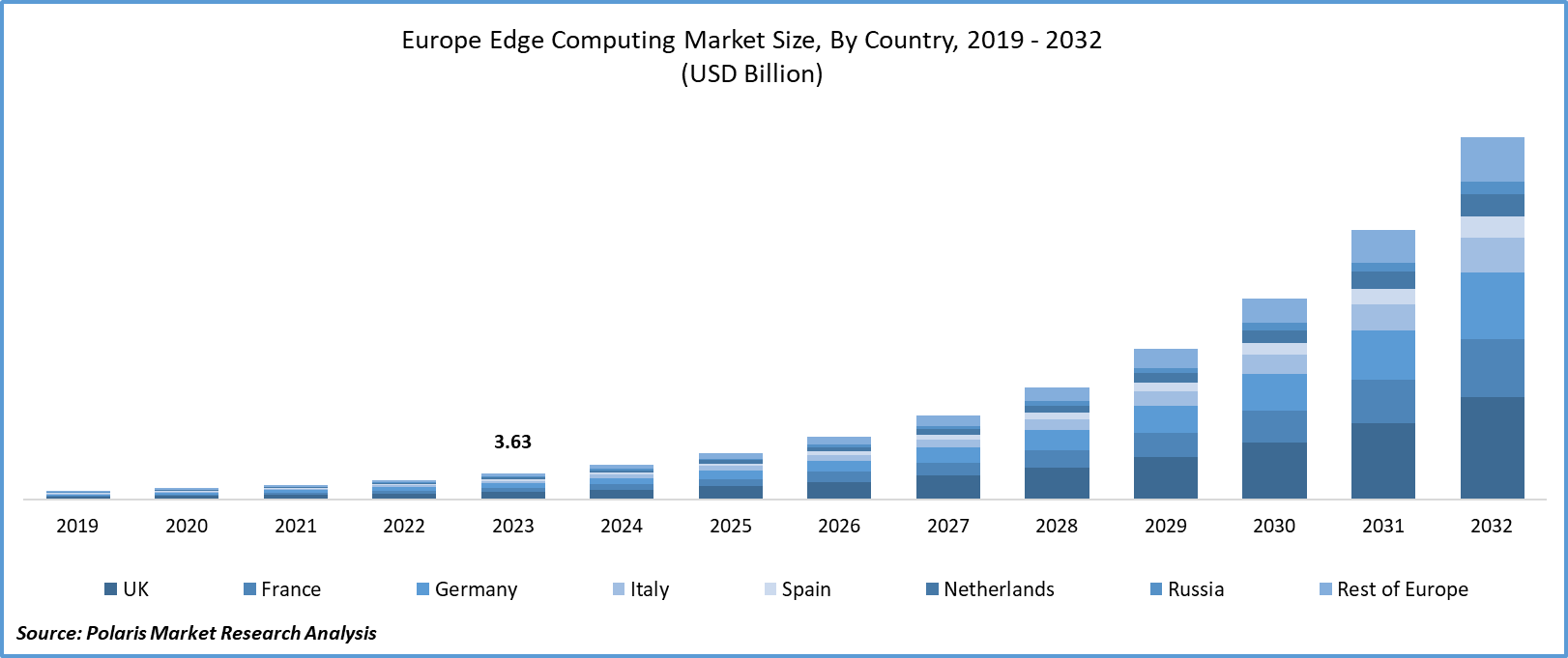

The europe edge computing market size was valued at USD 3.63 billion in 2023. The market is anticipated to grow from USD 4.86 billion in 2024 to USD 50.78 billion by 2032, exhibiting the CAGR of 34.1% during the forecast period.

Market Statistics

Industry Trends

The Europe edge computing market has witnessed significant growth in recent years, driven by the increasing adoption of IoT (Internet of Things) devices, the proliferation of data generated at the network edge, and the growing demand for low-latency computing solutions. Edge computing refers to the paradigm where data processing and analysis are performed closer to the data source, thereby reducing latency and improving the efficiency of data-intensive applications. This market has been propelled by various industry verticals, including manufacturing, healthcare, retail, transportation, and telecommunications, which are leveraging edge computing to enhance operational efficiency, customer experience, and overall business agility.

To Understand More About this Research: Download Sample Report

One of the prominent market trends shaping the Europe edge computing market is the rising adoption of 5G technology. With the deployment of 5G networks across the region, there has been an increased need for edge computing infrastructure to support the high bandwidth, low latency, and real-time processing requirements of 5G-enabled applications such as autonomous vehicles, augmented reality, and smart cities. Edge computing plays a crucial role in optimizing network performance and delivering enhanced user experiences in the 5G ecosystem, thereby driving the demand for edge computing solutions and services.

Furthermore, the COVID-19 pandemic has accelerated the adoption of edge computing in Europe as organizations strive to build resilient and agile IT architectures capable of supporting remote work, digital collaboration, and remote monitoring of critical assets. The shift towards remote operations has highlighted the importance of edge computing in enabling distributed data processing and ensuring seamless connectivity between edge devices and centralized data centers or cloud environments. As a result, enterprises across various sectors are investing in edge computing technologies to address the evolving needs of remote workforce and digital business operations.

Despite the growth prospects, the market is facing challenges like the complexity associated with deploying and managing edge computing infrastructure. Setting up edge computing nodes at distributed locations requires careful planning, coordination, and investment in networking, security, and management tools.

Key Takeaways

- UK dominated the market and contributed over 27% of the market share in 2023

- By application category, the industrial internet of things (IoT) segment accounted for the largest Europe edge computing market share in 2023

- By vertical category, the manufacturing segment is anticipated to grow with a lucrative CAGR over the Europe edge computing market forecast period

What are the market drivers driving the demand for market?

Increasing demand for efficient data processing and reduced latency drives the European edge computing market growth.

The market is experiencing significant growth due to the escalating demand for efficient data processing and the urgent need for reduced latency. As industries increasingly rely on data-driven decision-making and real-time insights, traditional cloud computing models need to improve in addressing latency-sensitive applications. Edge computing offers a solution by decentralizing data processing closer to the point of data generation, reducing the time it takes for information to travel to centralized servers and back. This proximity enhances efficiency and responsiveness, which is crucial for applications such as autonomous vehicles, smart manufacturing, and augmented reality. Also, stringent data privacy regulations in Europe incentivize local processing, further fueling the adoption of edge computing technologies across industries and driving market expansion and innovation.

Which factor is restraining the demand for market?

Concerns around data privacy and security affects the European market growth.

Concerns regarding data privacy and security significantly impact the growth of the market. Europe boasts some of the world's most stringent data protection regulations, such as the General Data Protection Regulation (GDPR), which imposes stringent requirements on how companies handle personal data. In the context of edge computing, where data processing often occurs closer to the point of generation, ensuring compliance with these regulations becomes increasingly complex.

Companies need to navigate intricate legal frameworks to guarantee that data is processed lawfully and transparently while also safeguarding against potential security breaches or unauthorized access. Failure to address these concerns adequately leads to severe penalties and reputational damage. Consequently, businesses may proceed with caution or invest heavily in robust data privacy and security measures, potentially slowing down market growth as they strive to navigate these intricate regulatory landscapes.

Report Segmentation

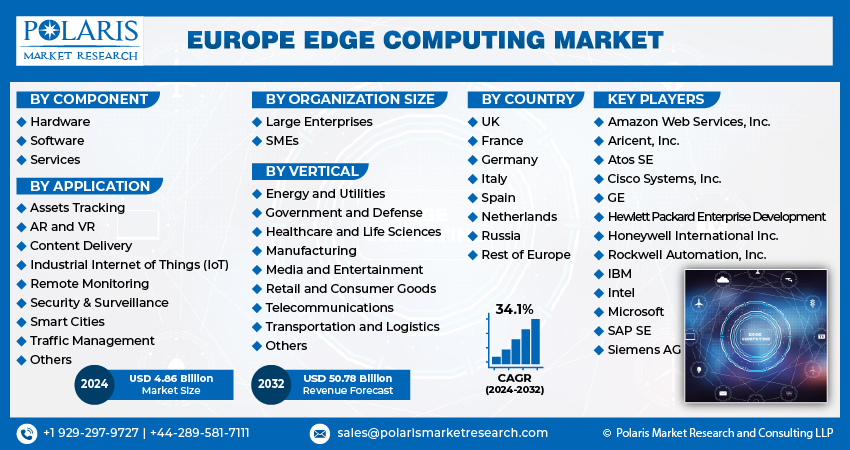

The market is primarily segmented based on component, application, organization size, vertical, and country.

| By Component | By Application | By Organization Size | By Vertical | By Country |

|

|

|

|

|

To Understand the Scope of this Report:Request Customization

Category Wise Insights

By Application Insights

Based on application analysis, the market is segmented on the basis of assets tracking, augmented reality (AR) and virtual reality (VR), content delivery, industrial internet of things (IoT), remote monitoring, security & surveillance, smart cities, traffic management, and others. The dominance of the industrial Internet of Things (IoT) segment in Europe's edge computing market in 2023 is due to industries such as manufacturing, energy, and transportation, which have been at the forefront of adopting IoT technologies to optimize operations, enhance efficiency, and reduce costs. These industries generate massive volumes of data from sensors, machines, and devices at the edge of their networks. Edge computing provides the necessary infrastructure to process this data locally, closer to its source, enabling real-time insights and decision-making while alleviating the strain on centralized cloud resources.

Also, the stringent requirements for low latency, high reliability, and data privacy in industrial applications make edge computing an ideal solution, further driving its adoption within this sector. As a result, the industrial IoT segment emerges as the primary driver of Europe's edge computing market growth, leveraging the transformative potential of edge technology to revolutionize various industrial processes.

By Vertical Insights

Based on vertical analysis, the market has been segmented on the basis of energy and utilities, government and defense, healthcare and life sciences, manufacturing, media and entertainment, retail and consumer goods, telecommunications, transportation and logistics, others. The manufacturing segment is expected to experience significant growth with a lucrative CAGR over the forecast period in Europe's edge computing market. Manufacturing operations are increasingly becoming digitized and connected, with the adoption of Industrial Internet of Things (IIoT) technologies aimed at improving productivity, efficiency, and quality control. These advancements result in the generation of vast amounts of data from sensors, machines, and production processes, requiring efficient processing and analysis.

Edge computing offers the capability to handle this data at the source, reducing latency and enabling real-time insights and decision-making critical for optimizing production processes and minimizing downtime. Additionally, edge computing enhances data security and privacy by processing sensitive information locally, addressing concerns about transmitting sensitive manufacturing data over wide-area networks.

Country-wise Insights

UK

The UK leads the edge computing market in Europe since the country possesses a global technology hub with a strong emphasis on innovation and digital transformation. The UK fosters a dynamic ecosystem conducive to the growth of edge computing solutions. The country's robust infrastructure, including high-speed internet connectivity and advanced data centers, provides a solid foundation for deploying edge computing architectures. Also, the UK's diverse industry verticals, including finance, healthcare, manufacturing, and transportation, drive demand for edge computing applications to enable real-time data processing and analytics at the network edge.

Competitive Landscape

The competitive landscape for the European edge computing market is characterized by intense rivalry among key players striving to gain market share and differentiate themselves through innovation and strategic partnerships. Leading multinational technology companies such as IBM Cisco Systems, Inc. and Hewlett Packard Enterprise Development dominate the market with their comprehensive edge computing solutions tailored to various industry verticals. Amidst this landscape, collaboration between technology vendors, cloud service providers, and industry stakeholders remains crucial for driving innovation, expanding market reach, and addressing evolving customer demands in the European edge computing market.

Some of the major players operating in the European market include:

- Amazon Web Services, Inc.

- Aricent, Inc.

- Atos SE

- Cisco Systems, Inc.

- GE

- Hewlett Packard Enterprise Development

- Honeywell International Inc.

- IBM

- Intel

- Microsoft

- Rockwell Automation, Inc.

- SAP SE

- Siemens AG

Recent Developments

- In December 2024: Wasabi Technologies enhanced its data management offerings by integrating its storage regions with IBM Cloud’s London data center. Using IBM’s Multizone Region, the collaboration helps customers meet regulatory requirements, adopt AI securely, and support edge computing through real-time data processing and hybrid cloud integration.

- In October 2024: The European Commission announced an investment of EUR 865 million to strengthen digital infrastructure by 2027. The initiative focuses on expanding 5G networks, improving energy-efficient connectivity, integrating cloud and edge computing, and upgrading submarine cables to connect citizens and businesses by 2030.

- In July 2024: Barcelona-based Nearby Computing raised EUR 6.5 million in Series A funding to grow its edge computing solutions for industrial and telecom sectors. Led by Walter Ventures and JME Ventures, with support from Telefónica and Akamai, the funding will help expand the NearbyOne platform and improve orchestration, automation, and network management across industries such as IoT and defense.

- In February 2024: EY and Dell Technologies collaborated to establish the EY Edge Technologies Lab. The lab will showcase and evaluate the performance of local edge-based computing system applications, which have proven to be more advantageous than central cloud processing for specific Industry 4.0 applications.

- In February 2024: Gcore, an international provider of cloud, AI, and edge solutions, introduced FastEdge, a serverless product designed to transform application deployment and performance. FastEdge is a cloud-native development solution specifically designed to create responsive and personalized applications without the need for complex server management.

Report Coverage

The Europe Edge Computing market report emphasizes on key countries across the region to provide better understanding of the product to the users. Also, the report provides market insights into recent developments, trends and analyzes the technologies that are gaining traction around the region. Furthermore, the report covers in-depth qualitative analysis pertaining to various paradigm shifts associated with the transformation of these solutions.

The report provides detailed analysis of the market while focusing on various key aspects such as competitive analysis, component, application, organization size, vertical, and their futuristic growth opportunities.

Edge Computing Market Report Scope

| Report Attributes | Details |

| Market size value in 2024 | USD 4.86 billion |

| Revenue forecast in 2032 | USD 50.78 billion |

| CAGR | 34.1% from 2024 – 2032 |

| Base year | 2023 |

| Historical data | 2019 – 2022 |

| Forecast period | 2024 – 2032 |

| Quantitative units | Revenue in USD billion and CAGR from 2024 to 2032 |

| Segments covered | By Component, By Application, By Organization Size, By Vertical, By Country |

| Regional scope | UK, France, Germany, Italy, Spain, Netherlands, Russia, Rest of Europe |

| Customization | Report customization as per your requirements with respect to countries, region and segmentation. |

FAQ's

The Europe edge computing market size is expected to reach USD 50.78 Billion by 2032

Key players in the market are Amazon Web Services, Inc., Aricent, Inc., Atos SE, Cisco Systems, Inc., GE, Hewlett Packard Enterprise Development

Europe edge computing market exhibiting the CAGR of 34.1% during the forecast period.

The Europe Edge Computing Market report covering key segments are component, application, organization size, vertical, and country.

Download Sample Report of Europe Edge Computing Market

Please fill out the form to request a customized copy of the research report.