GLP-1 Receptor Agonist Market Demand, Opportunity, 2026-2034

REPORT DETAILS

GLP-1 Receptor Agonist Market Overview

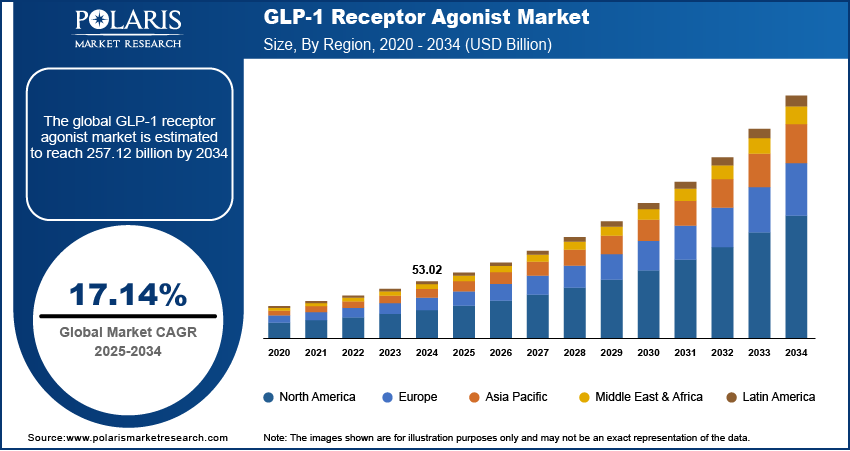

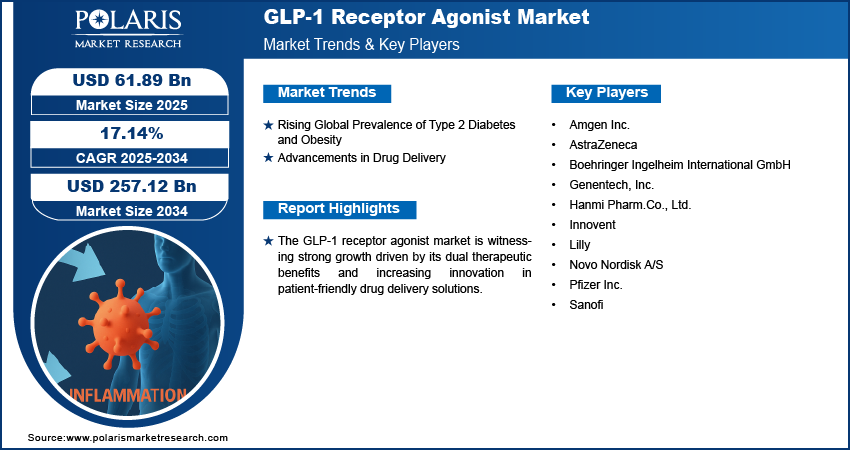

The global GLP-1 receptor agonist market size was valued at USD 61.89 billion in 2025. The market is projected to grow at a CAGR of 17.14% during 2026–2034. The market growth is driven by the dual efficacy of the drug in glycemic control and weight loss.

Market Statistics

Key Takeaways

- North America led with a 75.46% revenue share in 2025. The high prevalence of metabolic disorders and early adoption of novel therapeutics contribute to the regional market dominance.

- Asia Pacific is projected to witness rapid growth at a 14.1% CAGR. This is due to the rapidly rising prevalence of diabetes and obesity across major economies.

- The ozempic segment dominated the market with a 32.15% market share in 2025 due to its strong clinical performance.

- The obesity segment is expected to witness substantial growth at a 131% CAGR as the global burden of obesity continues to rise.

- The oral segment is expected to grow rapidly at a 22.9% CAGR. This is due to its convenience and noninvasive administration.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

GLP-1 Receptor Agonist Market Dynamics

- The rising prevalence of type 2 diabetes and obesity has resulted in increased demand for GLP-1 receptor agonists.

- Innovations in drug delivery such as once-weekly formulations and auto-injectors are contributing to the market demand.

- The growing focus on developing oral formulations to improve patient adherence is expected to present several market opportunities.

What is a GLP-1 Receptor Agonist?

GLP-1 receptor agonists are injectable and oral medications. These drugs mimic the actions of natural GLP-1 to stimulate insulin secretion and regulate blood sugar levels. They are used to treat type 2 diabetes and obesity. The demand for GLP-1 receptor agonists is growing due to the favorable policies from various government institutions across the globe.

There have been several healthcare plans by countries and international health institutions that aim at managing diabetes and obesity. For instance, in September 2025, the World Health Organization (WHO) updated its Model Lists of Essential Medicines (EML). It added several new medicines, including GLP-1 receptor agonists, for the treatment of diabetes. Such developments have increased access to the therapy and also increased investments in its development and research.

Source: Polaris Market Research Analysis

The growing range of therapeutic applications beyond glycemic control further expands opportunities. The efficacy of the GLP-1 receptor agonist in treating patients with obesity, cardiovascular problems, and NASH in association with type 2 diabetes is being recognized increasingly. For instance, in January 2025, the FDA approved semaglutide (Ozempic) as a medication to reduce the risk of kidney failure, kidney disease progression, and cardiovascular death in adults with type 2 diabetes and chronic kidney disease (CKD). Thus, a shift toward increased clinical utility is influencing the industry competition in favor of GLP-1 receptor agonists and attracting investments into research and development projects aimed at improving therapeutic options. Given the multipurpose nature of GLP-1 receptor agonists, the adoption process of these drugs is expected to be significantly accelerated through the continuous emergence of additional clinical evidence.

GLP-1 Drugs vs. Insulin Treatment

| Parameter | GLP-1 Receptor Agonists | Insulin Therapy |

| Mechanism of Action | Enhances glucose-dependent insulin secretion and suppresses appetite | Directly replaces or supplements insulin hormone |

| Weight Impact | Promotes weight loss | Often associated with weight gain |

| Hypoglycemia Risk | Lower risk of severe hypoglycemia | Higher risk of hypoglycemia |

| Administration Frequency | Weekly or daily depending on formulation | Often requires multiple daily injections |

| Cost | Generally higher due to branded biologic therapies and newer formulations | Lower for conventional insulin, though analog insulins can still be expensive |

| Cardiovascular Benefit | Demonstrates cardiovascular risk reduction in many diabetic and obese patients | Limited direct cardiovascular protection benefits |

| Approval Indications | Approved for type 2 diabetes, obesity, and weight management in several formulations | Approved primarily for type 1 and type 2 diabetes management |

| Side Effect Profile | Commonly causes nausea, vomiting, diarrhea, and gastrointestinal discomfort | Commonly linked to hypoglycemia, weight gain, and injection-site reactions |

| Patient Compliance | Improved adherence with once-weekly options | Lower adherence due to frequent injections and glucose monitoring |

| Market Trend | Rapid growth driven by obesity and metabolic disease demand | Mature and highly established diabetes therapy market |

Source: Polaris Market Research Analysis

What is Driving the GLP-1 Receptor Agonist Market?

Rising Global Prevalence of Type 2 Diabetes and Obesity

The rising global prevalence of type 2 diabetes and obesity is boosting the need for the GLP-1 receptor agonist, as these conditions represent the primary therapeutic targets for this drug class. According to a report from WHO, in 2022, approximately 830 million people worldwide had diabetes, while 1 in 8 individuals globally were affected by obesity. There is a growing demand for effective treatments that go beyond traditional insulin therapy, as sedentary lifestyles, unhealthy diets, and aging populations contribute to the increasing incidence of metabolic disorders worldwide. These drugs offer dual benefits, improving glycemic control while boosting weight loss, which makes them a preferred option in managing both type 2 diabetes and obesity. The growing patient numbers directly lead to higher adoption rates, encouraging pharmaceutical companies to scale production and innovate within this segment to meet expanding clinical needs.

Advancements in Drug Delivery

Advancements in drug delivery play a major role in driving the market forward. Innovations such as once-weekly formulations, auto-injectors, and oral delivery systems have greatly improved patient convenience with treatment. For instance, in June 2024, UBC launched under-the-tongue insulin drops with rapid absorption, potentially replacing traditional injections for diabetes treatment. These improvements reduce the burden associated with frequent injections and make GLP-1 therapies more accessible to a broader population, such as those who may be hesitant about injectable medications. Furthermore, the integration of smart drug delivery platforms and patient-centric designs is further boosting acceptance among both patients and healthcare providers. Therefore, as delivery technologies continue to evolve, they are expected to differentiate GLP-1 therapies in an increasingly competitive sector.

GLP-1 Receptor Agonist Market Opportunities

A rising shift toward oral GLP-1 formulations and combination therapies would provide lucrative business opportunities. Oral semaglutide and other oral drugs under late-stage clinical development would give needle-free disease management to patients. Oral drugs would make home administration easy. Patients prefer oral pills over injections due to their ease of consumption. Combination therapy involves the use of GLP-1 agonists together with either GIP or glucagon receptor agonists. Combination therapy proves to be more effective than single-mechanism drugs for weight loss and management of blood glucose levels. Pharmaceutical companies understand that dual- or triple-agonist molecules have the potential to revolutionize treatments of obesity and type 2 diabetes. Therefore, they are investing heavily in combination therapies. With rising regulatory approvals and expanding manufacturing capacity, oral and combination therapies are expected to unlock new patient segments.

Integration with Digital Health & Telemedicine

The use of GLP-1 treatments is now gaining more acceptance from digital health platforms such as telemedicine, electronic prescriptions, and remote patient monitoring. It increases the accessibility of such drugs, promotes compliance, and results in improved patient outcomes. It enables the physician to track the progress of their patient in real-time and modify the treatment plan accordingly. Moreover, electronic tools like m-health applications assist patients in remaining on track regarding the use of medications and adopting new habits.

Regulatory Approvals & Global Adoption

GLP-1 receptor agonists have received approvals from several regulatory authorities. This has led to their large-scale use in treating diabetes and obesity. Increasing reimbursement practices and rising awareness within the healthcare industry have been key factors driving the global rise in GLP-1 receptor agonists. Apart from this, newer versions of the guidelines that recommend the use of these drugs in certain patient populations have added to their market position. Increased cooperation between drug manufacturers and health care practitioners will lead to better distribution and availability of GLP-1 receptor agonists

Source: Polaris Market Research Analysis

Segmental Insights

By Product Analysis

Which GLP-1 Drugs Have the Largest Market Share?

The segmentation, based on product, includes ozempic, trulicity, mounjaro, wegovy, rybelsus, saxenda, victoza, zepbound, and others. The ozempic segment dominated the market in 2025 with 32.15% share due to its strong clinical performance, high brand recognition, and widespread adoption for managing type 2 diabetes. Its once-weekly dosing regimen has improved patient observation compared to daily injections, while its proven benefits in weight reduction and cardiovascular risk minimization have expanded its clinical use. Healthcare providers have increasingly preferred Ozempic for its balanced efficacy and tolerability profile, further supported by favorable formulary placements and broad insurance coverage. These factors combined have positioned Ozempic as a preferred therapy within the GLP-1 treatment landscape.

Comparison Matrix: Ozempic vs Wegovy vs Mounjaro

| Parameter | Ozempic | Wegovy | Mounjaro |

| Manufacturer | Novo Nordisk | Novo Nordisk | Eli Lilly and Company |

| Drug Type | GLP-1 receptor agonist | GLP-1 receptor agonist | Dual GIP/GLP-1 receptor agonist |

| Primary Approved Use | Type 2 diabetes management | Chronic weight management/obesity | Type 2 diabetes management |

| Active Ingredient | Semaglutide | Semaglutide | Tirzepatide |

| Weight Loss Effectiveness | Moderate to high | High | Very high |

| Blood Sugar Control | Strong glycemic control | Moderate glycemic benefit | Very strong glycemic control |

| Typical Target Patients | Diabetes patients with cardiovascular risk | Obese or overweight individuals | Diabetes patients requiring stronger metabolic control |

| FDA Approval Timeline | Earlier GLP-1 diabetes therapy | Obesity-focused semaglutide expansion | New-generation dual-action therapy |

| Pricing Position | Premium diabetes therapy | Premium obesity therapy | Premium next-generation therapy |

| Demand Trend | Strong global demand | Rapid obesity-market expansion | Fastest-growing competitive entrant |

| Key Competitive Advantage | Established diabetes efficacy and cardiovascular benefits | Superior branded obesity positioning | Enhanced weight reduction and metabolic outcomes |

| Common Side Effects | Nausea, vomiting, diarrhea | Gastrointestinal discomfort, nausea | Gastrointestinal side effects, appetite suppression |

| Market Positioning | Diabetes-focused GLP-1 leader | Obesity treatment leader | High-efficacy challenger in metabolic therapy |

| Future Commercial Outlook | Continued expansion in diabetes care | Strong growth driven by obesity epidemic | Significant growth potential in obesity and diabetes segments |

Source: Polaris Market Research Analysis

By Application Analysis

Which GLP-1 Application Holds the Largest Share?

The segmentation, based on application, includes type 2 diabetes mellitus and obesity. The obesity segment is expected to witness substantial growth rate of CAGR 55.21% during the forecast period as the global burden of obesity continues to escalate, driving demand for effective pharmacological interventions. GLP-1 receptor agonists have revealed notable weight loss outcomes, leading to their increasing use beyond diabetes care. Regulatory approvals for obesity-specific indications and the shifting perception of obesity as a chronic medical condition rather than a lifestyle issue are further improving market momentum. Additionally, rising awareness, coupled with broader access to treatment, is boosting more individuals to seek medical support for weight management, thereby strengthening growth in this segment.

By Route of Administration Analysis

Which Route of Administration of GLP-1 Led the Market Share?

The segmentation, based on route of administration, includes parenteral and oral. The oral segment is expected to grow rapidly with CAGR of 22.9% during the forecast period due to its convenience and noninvasive administration, which improves patient observation. Traditional injectable formulations often reflect psychological and practical barriers to treatment initiation and continuation. The introduction of oral GLP-1 therapies addresses these concerns, making treatment more accessible and acceptable to a wider population, particularly among newly diagnosed or injection-averse patients. This segment is expected to attract a growing share of prescriptions and patient interest as more oral formulations enter the market with proven efficacy.

By Distribution Channel Analysis

Which Distribution Channel Dominated the Revenue Share?

The segmentation, based on distribution channel, includes hospital pharmacies, retail pharmacies, and online pharmacies. The online pharmacies segment growth is driven by the increasing digitalization of healthcare services and shifting consumer preferences toward home delivery and convenience. Online platforms offer ease of access to medications, often at competitive pricing, while ensuring privacy, an appealing feature for patients managing chronic conditions such as diabetes or obesity. Additionally, the rise of e-prescriptions, telehealth integration, and subscription-based refill models have further supported the transition to digital pharmacy channels. This evolving distribution model is especially relevant in urban areas, where tech-savvy populations are more inclined to adopt e-commerce solutions for healthcare.

Source: Polaris Market Research Analysis

Regional Analysis

Which Region Leads the Global GLP-1 Market?

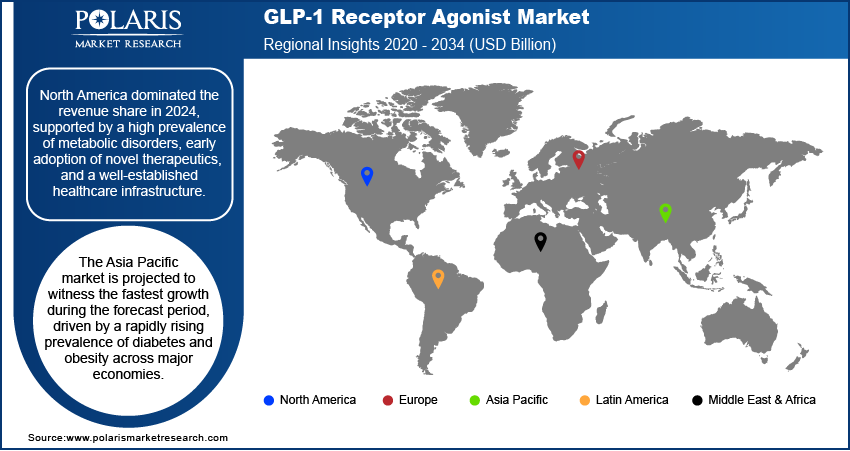

North America Leads GLP-1 Market with 75.46% Revenue Share in 2025

The report provides market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The North America GLP-1 receptor agonist market dominated the revenue with 75.46% share in 2025, supported by a high prevalence of metabolic disorders, early adoption of novel therapeutics, and a well-established healthcare infrastructure. The region benefits from advanced diagnostic capabilities, strong clinical awareness among healthcare providers, and robust reimbursement systems, which contribute to a higher uptake of GLP-1 therapies. For instance, in February 2024, the Ministry of Health, Canada, introduced Bill C-64 to establish universal pharmacare, covering diabetes drug such as insulin USD 900-USD 1,700/year, metformin ~USD 100/year, and adjunct therapies USD 100-USD 1,000+/year for type 1 and type 2 diabetes patients under single-payer insurance. In addition, the presence of major pharmaceutical companies and ongoing innovation in drug development and delivery technologies have boosted North America’s leadership position in this space.

US Holds Largest Share in North America Driven by High Healthcare Spending

The US GLP-1 receptor agonist market held the largest share in North America in 2025 due to its patient population, favorable regulatory environment, and high healthcare spending per capita. According to a December 2024 CMS report, in the US, healthcare spending grew 7.5% in 2023, totaling USD 4.9 trillion (USD 14,570 per capita). The country’s proactive perspective in treating type 2 diabetes and obesity, along with strong marketing efforts and access to cutting-edge therapies, has accelerated the adoption of GLP-1 receptor agonists.

Asia Pacific to Register Fastest Growth at 14.1% CAGR Through Forecast Period

The Asia Pacific GLP-1 receptor agonist market is projected to witness the fastest growth rate of CAGR 14.1% during the forecast period, driven by a rapidly rising prevalence of diabetes and obesity across major economies such as China, India, and Japan. Increasing healthcare awareness, growing disposable incomes, and expanding access to modern therapeutics are accelerating demand for advanced treatment options. Government initiatives aimed at supporting chronic disease management and the ongoing development of healthcare infrastructure are also supporting expansion opportunities. Furthermore, the rising adoption of lifestyle-related conditions and the growing presence of global pharmaceutical companies in the region are expected to boost the growth of GLP-1 therapies during the forecast period.

Canada GLP-1 Receptor Agonist Market Insights

Canada is seeing steady growth in the GLP-1 receptor agonist market as more people are diagnosed with diabetes and obesity. These therapies are driven by public healthcare coverage, increased access to prescription medicines, and increased awareness of weight management. Continued government efforts to improve diabetes care are also supporting market growth.

China GLP-1 Receptor Agonist Market Insights

China’s large diabetic population and increasing obesity rates are driving growth in the country’s GLP-1 receptor agonist market. Better access to innovative drugs is expanding treatment options. Increased healthcare spending and emphasis on chronic disease management are fueling the use of GLP-1 therapy. This is contributing to steady market growth.

India GLP-1 Receptor Agonist Market Insights

The India GLP-1 receptor agonist market is growing as diabetes and obesity become more common. Awareness of diabetes care has improved across the country in recent years. Expanding private healthcare services and better access to advanced treatment options areincreasing the use of GLP-1 therapies. These factors are contributing to market growth.

Germany GLP-1 Receptor Agonist Market Insights

The Germany GLP-1 receptor agonist market benefits from a well-established healthcare system and high awareness of diabetes care. Patients have good access to newer treatment options through favorable reimbursement policies. Early use of innovative therapies and growing attention to obesity management are increasing demand. This continues to strengthen the market.

Japan Market Poised for Steady Growth Amid Aging Population and Rising Diabetes Burden

The Japan GLP-1 receptor agonist market is expected to grow steadily during the forecast period, driven by a rising elderly population and a high prevalence of type 2 diabetes. According to World Bank data, Japan's diabetes prevalence among adults aged 20–79 was 6.6% of the total population in 2021. The country’s advanced healthcare infrastructure, combined with a strong focus on early diagnosis and chronic disease management, supports the increasing adoption of GLP-1 therapies. Moreover, the preference for innovative and less invasive treatment options aligns well with the ongoing development of oral and long-acting formulations. Japan presents a helping environment for market expansion in this segment with a strong regulatory framework that enables the introduction of novel therapies.

Europe Sees Substantial Growth Backed by Strong Healthcare Systems and Reimbursement Policies

The Europe GLP-1 receptor agonist market is projected to witness substantial growth during the forecast period due to strong healthcare systems, widespread clinical acceptance of GLP-1 therapies, and rising focus on integrating diabetes devices and obesity management. The region’s focus on evidence-based treatment protocols, with favorable reimbursement policies, is boosting wider adoption of GLP-1 drugs. Additionally, increasing investments in research and a growing focus on preventative healthcare are enabling innovation and therapeutic expansion within this class.

UK Market Expands on Government-Backed Obesity and Diabetes Initiatives

The UK GLP-1 receptor agonist market is projected to expand during the forecast period due to growing public health efforts to combat obesity and diabetes, supported by government-backed awareness campaigns and treatment guidelines. The National Health Service (NHS) continues to promote evidence-based interventions, creating a favorable setting for the wider adoption of GLP-1 drugs. Furthermore, increasing clinical trust in the benefits of GLP-1 therapies for weight and cardiovascular management is affecting prescribing patterns.

Source: Polaris Market Research Analysis

GLP-1 Receptor Agonist Market Trends

The GLP-1 receptor agonist market is moving toward more convenient and patient-friendly treatment. Companies are offering better delivery devices, oral drugs and once-a-week injections to make it more convenient. Digital health is also on the rise. Telemedicine, e-prescriptions, and remote patient monitoring support patients in remaining in touch with their healthcare providers and following their treatment plans. Another trend is that GLP-1 therapies are being used for more than diabetes and obesity. Researchers are studying these medicines for heart disease, kidney disease, and liver disease. The companies are coming out with new formulations and combination therapies to address different patient needs. As more studies are completed and additional approvals are received, these therapies are becoming part of treatment for a wider range of health conditions.

Key Players and Competitive Analysis

The GLP-1 receptor agonist sector is witnessing competition, driven by revenue growth opportunities in both developed and emerging markets. Players are leveraging investments and expansion opportunities to capitalize on the rising demand for diabetes and obesity treatment. Competitive intelligence reveals that companies are focusing on future development strategies, such as novel formulations and broader indications, to strengthen their positioning. Economic and geopolitical shifts are impacting region-wise market size projections. Technological advancements in delivery systems and oral formulations are creating disruptions and trends, forcing competitors to adapt their product offerings. Revenue share analysis indicates dominant players are expanding through mergers and acquisitions, while smaller firms target niche emerging market segments. Sustainable value chains and pricing insights are becoming critical differentiators as payers pressure costs. However, supply chain disruptions and regulatory policies impact competitive positioning, making vendor strategies and regional footprint optimization essential for long-term success.

Who Are the Leading GLP-1 Drug Manufacturers?

- Amgen Inc.

- AstraZeneca

- Boehringer Ingelheim International GmbH

- Genentech, Inc.

- Hanmi Pharm.Co., Ltd.

- Innovent

- Lilly

- Novo Nordisk A/S

- Pfizer Inc.

- Sanofi

Industry Developments

- July 2026: Novo Nordisk received CDSCO approval for Wegovy (semaglutide) as the first and only GLP-1 receptor agonist approved in India for noncirrhotic metabolic dysfunction-associated steatohepatitis (MASH) with moderate to advanced liver fibrosis, expanding the drug's indication beyond weight management and type 2 diabetes. (Source: biospectrumindia.com)

- April 2026: Eli Lilly and Company announced the U.S. FDA approved Foundayo (orforglipron) for chronic weight management in adults. The company stated that the daily, non-peptide oral GLP-1 receptor agonist can be taken anytime without food or water restrictions. (source: lilly.com)

- May 2025: Illumina and Ovation.io announced plans to develop a 25,000-patient clinical multiomic dataset from GLP-1 therapy users to aid drug discovery. The dataset will help study nonresponders (40% of Type 2 diabetes patients) and identify new biomarkers and drug targets. (Source: illumina.com)

November 2024: Ascendis Pharma licensed its TransCon technology to Novo Nordisk for metabolic and cardiovascular drug development, including a monthly GLP-1 agonist for obesity and diabetes. Ascendis would receive up to USD 285 million in payments. (Source: ascendispharma.com).

GLP-1 Receptor Agonist Market Segmentation

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Ozempic

- Trulicity

- Mounjaro

- Wegovy

- Rybelsus

- Saxenda

- Victoza

- Zepbound

- Others

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Type 2 Diabetes Mellitus

- Obesity

By Route of Administration Outlook (Revenue, USD Billion, 2021–2034)

- Parenteral

- Oral

By Distribution Channel Outlook (Revenue, USD Billion, 2021–2034)

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

GLP-1 Receptor Agonist Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 61.89 billion |

| Market Size in 2026 | USD 70.21 billion |

| Revenue Forecast by 2034 | USD 257.12 billion |

| CAGR | 17.14% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

GLP-1 Receptor Agonist Market FAQ's

The global market size was valued at USD 61.89 billion in 2025 and is projected to grow to USD 257.12 billion by 2034.

The global market is projected to register a CAGR of 17.14% during the forecast period.

North America dominated the market share in 2025 with 75.46% share.

A few of the key players in the market are Amgen Inc.; AstraZeneca; Boehringer Ingelheim International GmbH; Genentech, Inc.; Hanmi Pharm.Co., Ltd.; Innovent; Lilly; Novo Nordisk A/S; Pfizer Inc.; and Sanofi.

The ozempic segment dominated the market in 2025 with 32.15% share.

The obesity segment is expected to witness the fastest growth of CAGR 55.21% during the forecast period.

Download Sample Report of GLP-1 Receptor Agonist Market

Please fill out the form to request a customized copy of the research report.