Graphene-Enhanced Conductive Polymers Market Future Demand 2025-2034

REPORT DETAILS

REPORT DETAILS

Market Statistics

What is Graphene-Enhanced Conductive Polymers Market Size?

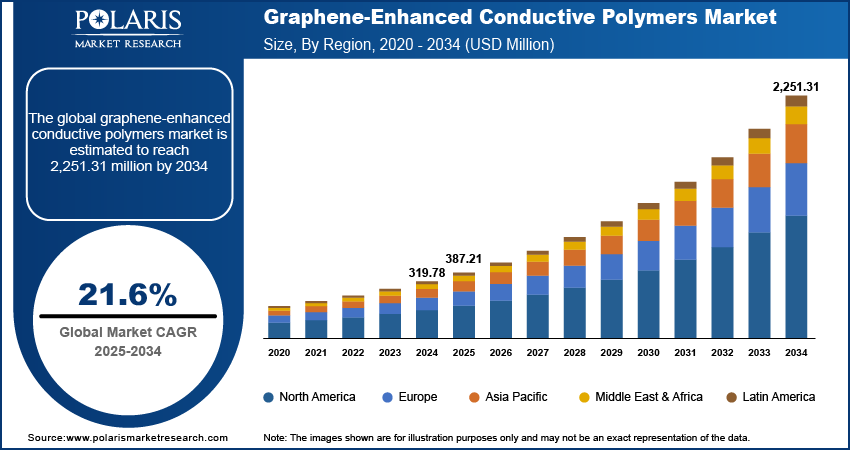

The global graphene-enhanced conductive polymers market size was valued at USD 319.78 million in 2024, growing at a CAGR of 21.6% from 2025–2034. Key factors driving the growth is rise in demand from automotive industry, growing adoption of battery storage, and technological advancement.

Key Insights

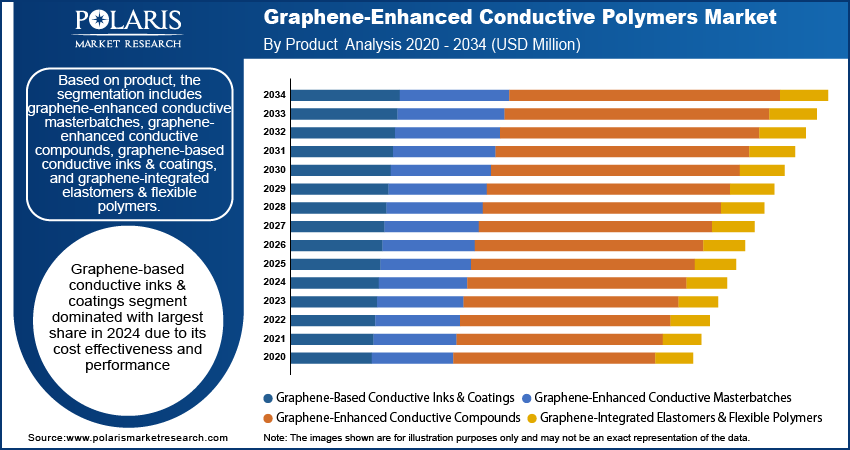

- Graphene-based conductive inks & coatings segment dominated with largest share in 2024 due to its cost effectiveness and performance.

- Electronics & ESD components segment is expected to witness a significant share over the forecast period due to advantages in protection and reliability provided by graphene conductive polymer.

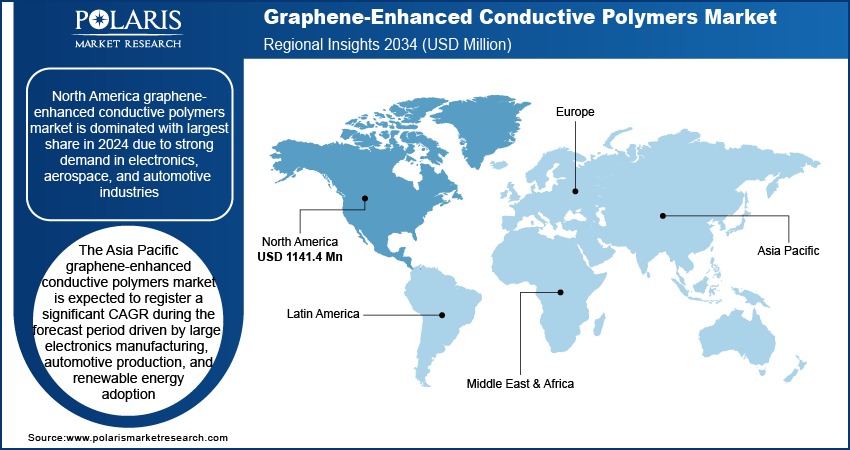

- North America graphene-enhanced conductive polymers market is dominated with largest share in 2024 due to strong demand in electronics, aerospace, and automotive industries.

- The Asia Pacific graphene-enhanced conductive polymers market is expected to register a significant CAGR during the forecast period driven by large electronics manufacturing, automotive production, and renewable energy adoption.

Industry Dynamics

- The rising adoption in automotive sector is driving the growth.

- Rising demand for battery energy storage is fueling the growth.

- Technological advancement is boosting the growth.

- High production costs limits the growth of the market.

Market Statistics

- 2024 Market Size: USD 319.78 Million

- 2034 Projected Market Size: USD 2,251.31 Million

- CAGR (2025-2034): 21.6%

- North America: Largest Market Share

A graphene-enhanced conductive polymer is a plastic material improved with small amounts of graphene to significantly increase its electrical conductivity, strength and durability. The graphene disperses within the polymer matrix, creating conductive pathways without compromising flexibility or processability. These materials enable lighter, more efficient components for electronics, sensors, energy storage, automotive parts and other high-performance applications.

The growing demand for the wearable electronics is fueling the industry growth. The demand for the wearable electronics is rising worldwide. This rise in the demand is fueled by technological advancement, expansion of the tech savvy population and rising disposable income. Consequently, the demand for the graphene-enhanced conductive polymers is rising. It combines electrical conductivity with mechanical flexibility and are durable for long duration. Traditional conductive fillers often compromise stretchability or add weight. Moreover, expansion of the wearable technology in wide range of applications is further fueling the demand, thereby driving the industry growth.

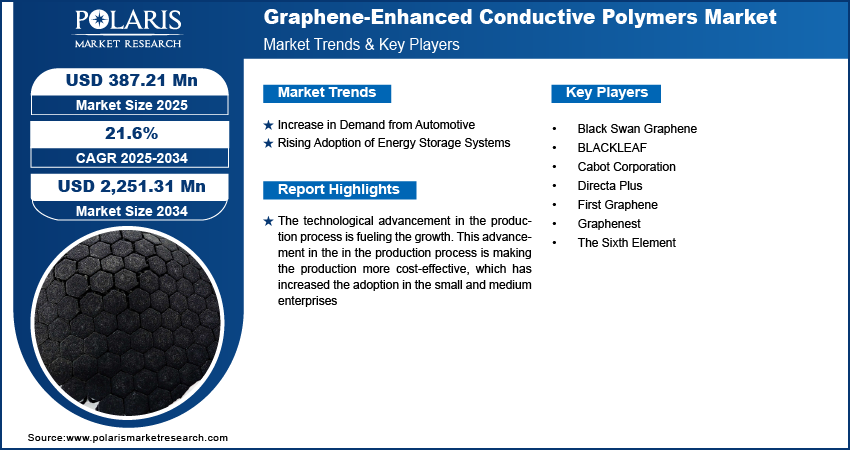

The technological advancement in the production process is fueling the growth. This advancement in the in the production process is making the production more cost-effective, which has increased the adoption in the small and medium enterprises. Further, the it has improved the appeal of the final product by producing consistent flake size, purity, and dispersion compatibility. These improvements make it easier for polymer and electronics manufacturers to integrate graphene into existing processes without costly adjustments. Moreover, rising research and development spending by the major players operating in the market is further driving the industry growth.

Drivers & Opportunities

What are Factors Driving Industry Growth?

Increase in Demand from Automotive: The demand for the graphene enhanced conductive polymers is rising in automotive industry. This industry is rapidly shifting to lightweight, conductive materials to improve vehicle efficiency, meet emissions and fuel economy regulations. Further rising focus on miniaturization, and improved performance has increased the demand as traditional metal conductive adds up extra weight to vehicles electronics. Moreover, the production of the personal vehicles is increasing worldwide due to expanding middle class, government incentives on the manufacturing, consequently fueling the demand for the graphene enhanced conductive polymers, thereby driving the industry growth.

Rising Adoption of Energy Storage Systems: The adoption of the energy storage system is rising worldwide. The demand for batteries and supercapacitors is rising in wide range of applications such as consumer electronics, renewable energy and automotive. This has increased the demand for the graphene enhanced conductive polymers as it improves electron transport, electrode stability, and enable faster charge. Moreover, expansion of electric vehicles is further driving the demand. This expansion has boosted the demand for the lithium-ion batteries worldwide. As a result, the demand for the conductive polymers is rising, thereby boosting the market growth

Technological Advancement in Production Process:

| Advancement area | Specific technological advance | What changes in the production process |

| Processing route design | Comparative optimization of solution mixing vs in situ polymerization | Reviews from 2022–2024 show that shifting from simple solution mixing toward in situ polymerization and melt processing of graphene or graphene‑oxide dispersions improves filler dispersion, interfacial bonding, and conductive network formation in polymer matrices. |

| Hybrid filler architectures | Graphene–carbon nanotube hybrid fillers in polymers | Recent work on graphene hybrid filler polymer composites reports that combining graphene nanoplatelets with other carbon nanofillers in controlled ratios yields synergistic conductive networks and large gains in electrical and thermal conductivity compared with single‑filler systems. |

| In situ GO reduction | In situ reduction of graphene oxide during polymerization/melt processing | A critical review of in situ GO reduction shows that reducing GO directly during in situ polymerization or melt processing of conducting polymers dramatically lowers percolation thresholds and increases conductivity by several orders of magnitude versus ex situ reduction routes. |

| Masterbatch strategies | Graphene masterbatch routes for conductive blends | Masterbatch approaches where graphene oxide is first dispersed and reduced in an elastomer or copolymer, then diluted into the target polymer, provide better dispersion and allow high‑conductivity composites at low graphene loadings in scalable melt compounding lines. |

| Conductive polymer/graphene architectures | Tailored binary and ternary composite architectures | Reviews of conductive polymer/graphene composites describe engineered architectures (layered, core–shell, and porous structures) that maximize interfacial contact and electron transport, enabling higher specific capacitance and conductivity for supercapacitors and sensors. |

| Flexible CPCs | Self‑healing and flexible conductive polymer composites | Recent work on next‑generation conductive polymer composites for flexible electronics uses hybrid nanofillers including graphene to achieve combinations of high conductivity, flexibility, and self‑healing behavior through tailored filler networks and dynamic polymer matrices. |

| Roll‑to‑roll processing | Roll‑to‑roll processable graphene/polymer films | Studies on roll‑to‑roll processable graphene‑based composite films demonstrate continuous coating of graphene‑containing layers on polymer substrates, enabling scalable manufacturing of conductive films for EMI shielding and flexible electronics. |

| Scalable dispersion chemistries | Scalable chemistries for graphene dispersions | Work on chemically converted graphene outlines dispersion chemistries in aqueous and organic systems that are compatible with large‑scale polymer processing, improving uniform graphene distribution in conductive polymer composites. |

| Structure–property control | State‑of‑the‑art GRPC processing–property relations | A 2024 state‑of‑the‑art review on graphene‑reinforced polymer composites links specific processing routes (mechanical mixing, solution mixing, in situ polymerization, electrospinning, layer‑by‑layer) to tunable electrical, thermal, and mechanical performance in conductive polymers. |

| Performance‑oriented design | Graphene composites for high‑performance electronics | Recent analysis of graphene‑based polymer composites for high‑performance devices highlights how optimizing graphene content, dispersion, and alignment in polymers can deliver conductivities up to thousands of S/cm, suitable for advanced electronic applications. |

Segmental Insights

Why Graphene-Based Conductive Inks & Coatings Dominated in 2024?

Graphene-based conductive inks & coatings segment dominated with largest share in 2024 due to its cost effectiveness and performance. This graphene based conductive inks and coatings are compatible with common printing techniques and easily integrates into the existing production lines. This has increased the commercial production and has improved the accessibility. Moreover, the rising demand for the sensors, RFID, wearable electronics, and flexible circuits is further driving the need for the conductive inks and coatings. It offers exceptional conductivity, flexibility, and durability, thereby driving the growth.

Which Segment by Application is Expected to Witness a Significant Share?

Electronics & ESD components segment is expected to witness a significant share over the forecast period due to advantages in protection and reliability provided by graphene conductive polymer. This material offers flexibility in the design and prevent damage from static discharge. The rising adoption in the consumer electronics, industrial sensors and circuits are driving the demand. Moreover, this material provides thermal stability in the electronics which is further driving the demand, thereby driving the segment growth.

Regional Analysis

What are Regional Statistics of Industry?

North America graphene-enhanced conductive polymers market is dominated with largest share in 2024 due to strong demand in electronics, aerospace, and automotive industries. The region benefits from advanced research infrastructure, innovative startups, and established manufacturing hubs that accelerate commercialization of graphene-based materials. Companies are increasingly adopting graphene polymers for lightweight, flexible, and highly conductive components in sensors, batteries, and wearable devices. Government support for advanced materials research and growing investment in next-generation electronics further fuel market growth in the region.

The Asia Pacific graphene-enhanced conductive polymers market is expected to register a significant CAGR during the forecast period driven by large electronics manufacturing, automotive production, and renewable energy adoption. Countries such as China, Japan, and South Korea lead in large-scale production, cost-effective graphene supply, and integration into printed electronics and energy storage systems. Rapid industrialization, increasing consumer demand for wearable and flexible electronics, and government initiatives supporting advanced materials fuels demand. Manufacturers benefit from lower production costs and scalable supply chains, making graphene-enhanced polymers more accessible, thereby fueling the growth.

Key Players & Competitive Analysis

The market is increasingly competitive as players like Black Swan Graphene, BLACKLEAF, Cabot, Directa Plus, First Graphene, Graphenest and The Sixth Element scale production and strengthen application pipelines. Companies differentiate through material quality, dispersion technology and cost-efficient masterbatches for electronics, automotive, energy storage and industrial components. The rising demand for lightweight, highly conductive materials, competition centers on performance, consistency and integration into existing polymer processing, driving rapid commercialization and accelerating adoption across high-value manufacturing sectors.

Key Players

- Black Swan Graphene

- BLACKLEAF

- Cabot Corporation

- Directa Plus

- First Graphene

- Graphenest

- The Sixth Element

Industry Developments

November 2025, First Graphene announced it had completed its first industrial-scale shipment of PureGRAPH 10 graphene-enhanced TPU masterbatch, delivering 500 kilograms for integration into safety boot soles and marking a significant commercial step toward broader adoption in high-wear polymer applications across industry.

Graphene-Enhanced Conductive Polymers Market Segmentation

By Product Outlook (Revenue, USD Million, 2020–2034)

- Graphene-Enhanced Conductive Masterbatches

- Graphene-Enhanced Conductive Compounds

- Graphene-Based Conductive Inks & Coatings

- Graphene-Integrated Elastomers & Flexible Polymers

By Application Outlook (Revenue, USD Million, 2020–2034)

- Electronics & ESD Components

- EMI/RFI Shielding Parts

- Printed Electronics & Sensors

- Energy Storage Components

- Automotive & Aerospace Lightweight Conductive Parts

- Other applications

By Regional Outlook (Revenue, USD Million, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Graphene-Enhanced Conductive Polymers Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 319.78 Million |

| Market Size in 2025 | USD 387.21 Million |

| Revenue Forecast by 2034 | USD 2,251.31 Million |

| CAGR | 21.6% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 319.78 million in 2024 and is projected to grow to USD 2,251.31 million by 2034.

The global market is projected to register a CAGR of 21.6% during the forecast period.

North America dominated the market in 2024

A few of the key players in the market are Black Swan Graphene, BLACKLEAF, Cabot Corporation, Directa Plus, First Graphene, Graphenest, and The Sixth Element.

The graphene based conductive ink and coatings segment dominated the market revenue share in 2024.

The electronics and ESD segment is projected to witness the fastest growth during the forecast period.

Download Sample Report of Graphene-Enhanced Conductive Polymers Market

Please fill out the form to request a customized copy of the research report.