Healthcare Mobile Application Market Trends, Business Trends, Strategies, 2025-2034

REPORT DETAILS

REPORT DETAILS

Market Statistics

Market Overview

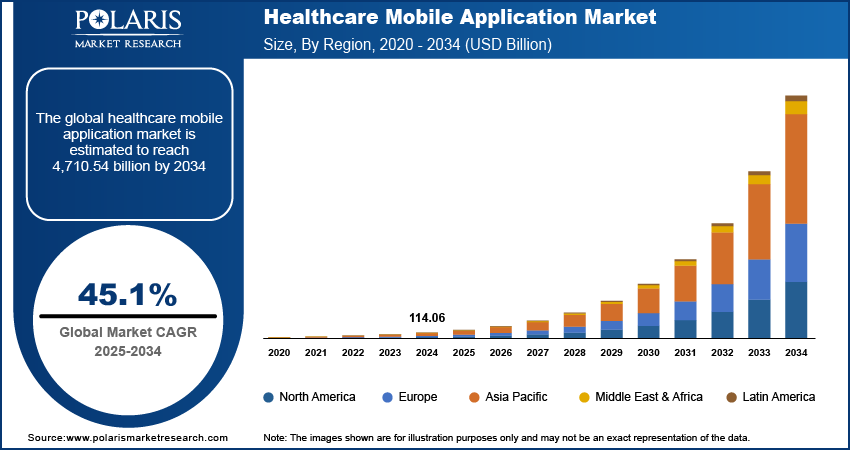

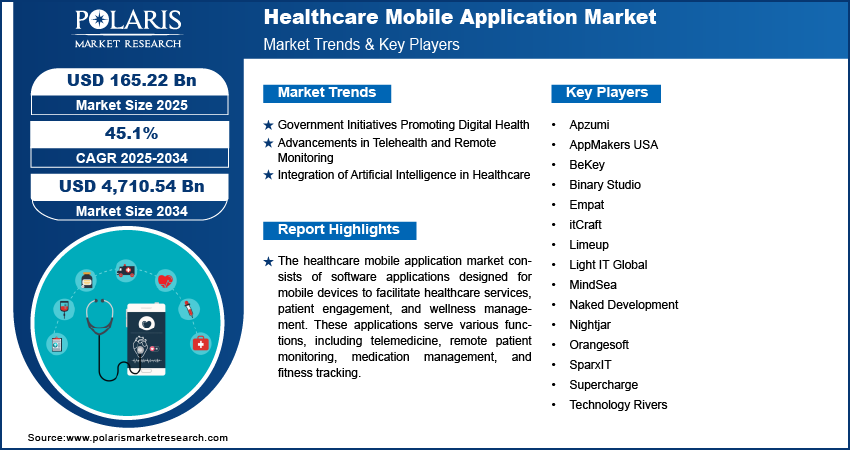

The global healthcare mobile application market size was valued at USD 114.06 billion in 2024. The market is projected to grow from USD 165.22 billion in 2025 to USD 4,710.54 billion by 2034, exhibiting a CAGR of 45.1% during 2025–2034.

The healthcare mobile application market encompasses software solutions designed for smartphones, tablets, and other mobile devices to facilitate medical and health-related services. These applications support various functions, including remote patient monitoring devices, telemedicine, medication management, and fitness tracking. The market is driven by increasing smartphone penetration, advancements in wireless technology, and the growing adoption of digital health solutions. The rising prevalence of chronic diseases, the demand for remote healthcare services, and regulatory support for digital health initiatives further contribute to market expansion.

Key drivers of the healthcare mobile application market demand include the increasing need for patient engagement solutions, the widespread adoption of wearable devices, and the integration of artificial intelligence (AI) in mobile health applications. The expansion of telehealth services, coupled with rising healthcare costs, has further accelerated the demand for mobile applications that enhance accessibility and efficiency. Moreover, stringent data security regulations and concerns regarding interoperability remain challenges for market growth. However, continuous advancements in mobile health technologies and increasing investments in digital health infrastructure are expected to drive further expansion in the coming years.

To Understand More About this Research: Download Sample Report

Market Dynamics

Government Initiatives Promoting Digital Health

Government initiatives have significantly propelled the adoption of mobile health applications by establishing supportive frameworks and policies. In India, the Ayushman Bharat Digital Mission (ABDM), launched in 2021, aims to create an integrated digital health infrastructure by providing unique digital health IDs for citizens, facilitating seamless access to health records nationwide. This initiative underscores the government's commitment to improving healthcare delivery through digital means. Similarly, the Aarogya Setu mobile application, introduced by the Government of India, exemplifies efforts to utilize mobile technology for public health, particularly during the COVID-19 pandemic. These initiatives highlight the role of government initiatives and policies in driving the healthcare mobile application market growth.

Advancements in Telehealth and Remote Monitoring

The evolution of telehealth and remote monitoring technologies has been a pivotal driver in the healthcare mobile application market development. In India, telemedicine has expanded notably since 2018, offering new avenues for doctor consultations. On March 25, 2020, the Ministry of Health and Family Welfare issued India's Telemedicine Practice Guidelines, providing statutory support for telemedicine practices. Subsequently, in April 2020, the Union Health Ministry launched the eSanjeevani telemedicine service, operating at two levels: doctor-to-doctor and doctor-to-patient platforms. This service crossed five million teleconsultations within a year of its launch, indicating a conducive environment for the growth of telemedicine in India. These developments underscore the critical role of telehealth advancements in the proliferation of healthcare mobile applications.

Integration of Artificial Intelligence in Healthcare

The integration of artificial intelligence (AI) into healthcare systems has significantly influenced the development and adoption of mobile health applications. For instance, Philips has been integrating AI into diagnostic tools to enhance responsiveness and safety standards in medical technologies and patient care solutions. Similarly, companies such as Deep Medical are utilizing AI to minimize missed appointments, potentially saving millions annually. These instances illustrate how AI integration is enhancing the functionality and appeal of healthcare mobile applications, thereby driving market growth.

Market Segment Insights

Market Assessment – by Platform

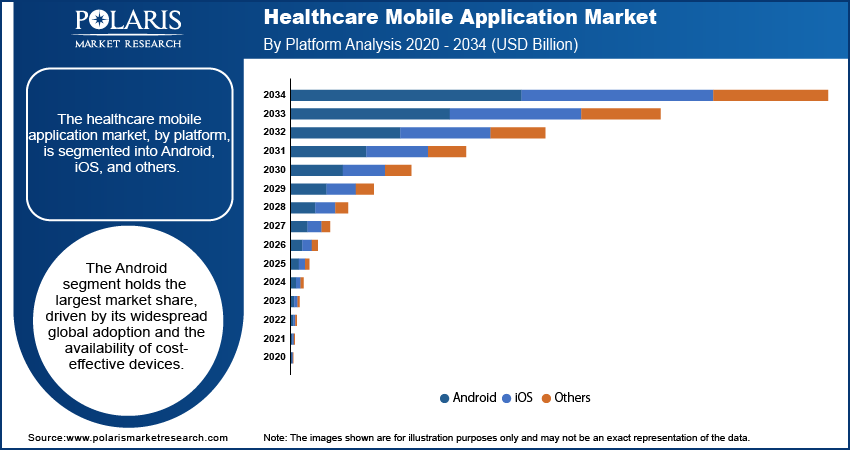

The healthcare mobile application market, by platform, is segmented into Android, iOS, and others. The Android segment holds the largest healthcare mobile application market share, driven by its widespread global adoption and the availability of cost-effective devices. Android's open-source nature allows developers to create a diverse range of healthcare applications, catering to various user needs. This flexibility has led to a proliferation of health apps on the Google Play Store, enhancing accessibility for users worldwide. The platform's extensive reach and affordability have been instrumental in its dominant position within the healthcare mobile application market.

The iOS platform is experiencing significant growth in the healthcare mobile application sector, attributed to its strong user base and the platform's emphasis on security and user experience. iOS users often engage more with health applications, benefiting from the platform's seamless integration with health monitoring features and devices. The controlled ecosystem of iOS ensures consistent performance and security, making it an attractive choice for healthcare providers and developers aiming to deliver reliable health applications. This focus on quality and user engagement is contributing to the rapid expansion of healthcare applications on the iOS platform.

Market Evaluation – by Type

The healthcare mobile application market, by type, is segmented into appointment booking & consultation, online pharmacy, diagnosis & testing, fitness products & training, nutrition & diet, healthcare insurance, remote patient monitoring, and others. The online pharmacy segment is expected to witness a significant market share during the forecast period. This growth is attributed to the increasing consumer preference for the convenience of ordering medications through mobile platforms. In India, companies such as Medlife and Tata 1mg have played pivotal roles in this sector.

Regional Insights

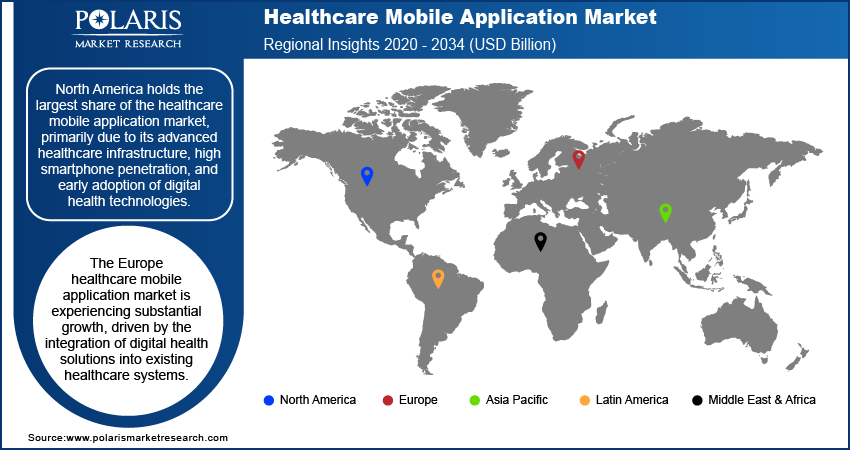

By region, the study provides healthcare mobile application market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America holds the largest share of the healthcare mobile application market revenue, primarily due to its advanced healthcare infrastructure, high smartphone penetration, and early adoption of digital health technologies. The region's emphasis on preventive healthcare and wellness has led to the widespread utilization of mobile health apps among consumers and healthcare providers. Additionally, supportive regulatory frameworks and substantial investments in health IT have fostered innovation and integration of mobile solutions in patient care. These factors collectively contribute to North America's dominant position in the global healthcare mobile application market.

The Europe healthcare mobile application market is experiencing substantial growth, driven by the integration of digital health solutions into existing healthcare systems. The region's strong emphasis on research and development, supported by robust public and private investments, has fostered innovation in digital health. For instance, European digital health startups raised significant investments in recent years, with France alone securing substantial funding in 2022. Additionally, regulatory frameworks, such as Germany's reimbursement of digital health applications across various disease areas and France's introduction of a fast-track reimbursement route for digital health solutions, have facilitated market adoption. These initiatives underscore Europe's commitment to integrating digital technologies into healthcare delivery.

The Asia Pacific healthcare mobile application market is rapidly expanding, propelled by favorable government initiatives, increasing smartphone penetration, and a rising demand for remote patient monitoring. Japan is witnessing a high prevalence of chronic diseases, necessitating efficient healthcare management solutions. The region's swift adoption of 5G technology is enhancing the functionality and accessibility of mobile health applications. For example, in Thailand, a collaboration among government agencies led to the development of an IT system and mobile application connecting services across numerous government hospitals, facilitating telemedicine services such as telepathology consultations and teleradiology. These developments highlight Asia Pacific's proactive approach to embracing digital health technologies to improve healthcare outcomes.

Key Players and Competitive Insights

The healthcare mobile application market features several active companies contributing to its growth and innovation. A few notable companies among these are Orangesoft, Apzumi, AppMakers USA, Naked Development, Technology Rivers, itCraft, Empat, MindSea, Limeup, SparxIT, BeKey, Light IT Global, Binary Studio, Nightjar, and Supercharge.

Each of these companies brings unique strengths to the healthcare mobile application landscape. For instance, Orangesoft and Apzumi are recognized for their expertise in developing user-friendly interfaces that enhance patient engagement. Companies such as Technology Rivers and itCraft focus on integrating advanced technologies such as artificial intelligence and machine learning to provide personalized healthcare solutions. Meanwhile, firms such as MindSea and Limeup emphasize seamless integration with existing healthcare systems, ensuring interoperability and data security.

In this competitive environment, differentiation often hinges on specialization and technological innovation. Companies that tailor their applications to specific medical fields or patient demographics can address unique needs, thereby capturing niche markets. Additionally, the ability to adapt to regulatory changes and ensure compliance with healthcare standards is crucial for maintaining credibility and trust among users. As the demand for digital health solutions continues to rise, these companies are well-positioned to contribute significantly to the evolution of healthcare delivery through mobile platforms.

Orangesoft is a mobile app and web development company established in 2011, with offices in the US and Poland. Over the years, they have expanded their team to over 80 professionals, delivering custom applications that address complex business challenges across various domains.

Apzumi is a boutique software agency specializing in digital health, wellness, and fitness solutions. With over 12 years in the market and a team of more than 70 experts, Apzumi has completed over 120 projects, focusing on creating digital solutions that make a significant impact on people's lives.

List of Key Companies

- Apzumi

- AppMakers USA

- BeKey

- Binary Studio

- Empat

- itCraft

- Limeup

- Light IT Global

- MindSea

- Naked Development

- Nightjar

- Orangesoft

- SparxIT

- Supercharge

- Technology Rivers

Industry Developments

- January 2025: Cipla introduced AI-powered mobile application for asthma screening in India.

- August 2024: The Union Health Ministry of India launched the myCGHS iOS app, providing CGHS beneficiaries with convenient access to healthcare services, including appointments, lab reports, and medical claims.

Market Segmentation

By Platform Outlook (Revenue – USD Billion, 2020–2034)

- Android

- iOS

- Others

By Type Outlook (Revenue – USD Billion, 2020–2034)

- Appointment Booking & Consultation

- Online Pharmacy

- Diagnosis & Testing

- Fitness Products & Training

- Nutrition & Diet

- Healthcare Insurance

- Remote Patient Monitoring

- Others

By Technology Outlook (Revenue – USD Billion, 2020–2034)

- AI-enabled

- Non-AI-enabled

By End Use Outlook (Revenue – USD Billion, 2020–2034)

- Consumer

- Hospitals/Healthcare Providers

- Healthcare Payers

- Others

By Regional Outlook (Revenue – USD Billion, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest f Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- Suth Korea

- Indnesia

- Australia

- Vietnam

- Rest f Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- Suth Africa

- Rest f Middle East & Africa

- Latin America

- Mexic

- Brazil

- Argentina

- Rest f Latin America

Healthcare Mobile Application Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2024 | USD 114.06 billion |

| Market Size Value in 2025 | USD 165.22 billion |

| Revenue Forecast by 2034 | USD 4,710.54 billion |

| CAGR | 45.1% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

How is the report valuable for an organization?

Workflow/Innovation Strategy: The healthcare mobile application market has been segmented into platform, type, technology, and end use. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Growth/Marketing Strategy: The healthcare mobile application market growth and marketing strategies focus on technological advancements, user engagement, and regulatory compliance. Companies emphasize AI integration, data security, and interoperability to enhance application functionality and usability. Strategic partnerships with healthcare providers, insurers, and technology firms drive market expansion, while targeted digital marketing, including app store optimization and social media outreach, boost user adoption. Additionally, adherence to healthcare regulations, such as HIPAA and GDPR, builds trust among consumers and institutions. Continuous updates and personalized features further enhance user retention and long-term market sustainability.

FAQ's

The healthcare mobile application market size was valued at USD 114.06 billion in 2024 and is projected to grow to USD 4,710.54 billion by 2034.

The market is projected to register a CAGR of 45.1% during the forecast period.

North America held the largest share of the market in 2024.

The healthcare mobile application market features several active companies contributing to its growth and innovation. A few notable players among these are Orangesoft, Apzumi, AppMakers USA, Naked Development, Technology Rivers, itCraft, Empat, MindSea, Limeup, SparxIT, BeKey, Light IT Global, Binary Studio, Nightjar, and Supercharge.

The Android segment accounted for the largest share of the market in 2024.

The online pharmacy segment is expected to witness a significant market share during the forecast period.

Download Sample Report of Healthcare Mobile Application Market

Please fill out the form to request a customized copy of the research report.