Heavy Construction Equipment Market Size, Drivers, Overview, 2026-2034

REPORT DETAILS

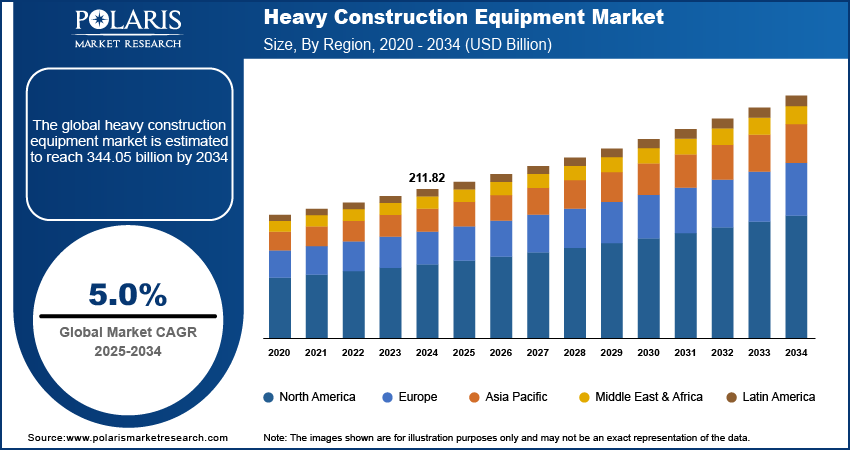

Heavy Construction Equipment Market Summary

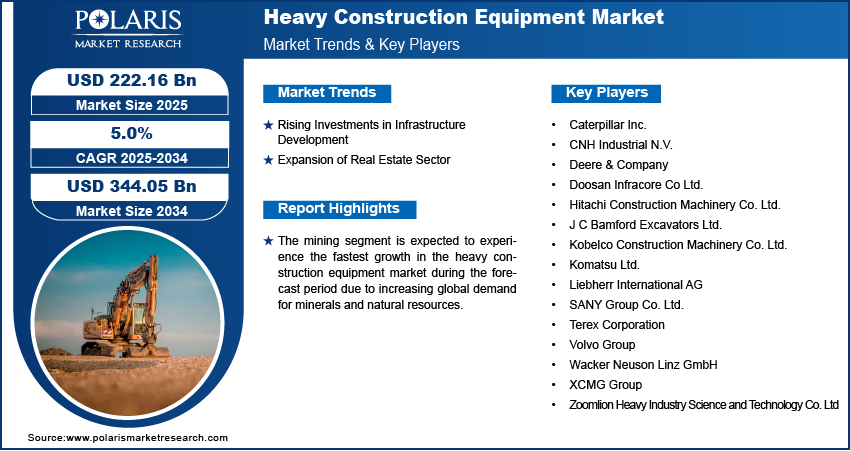

The global heavy construction equipment market size was valued at USD 222.16 billion in 2025, growing at a CAGR of 5.0% from 2026 to 2034. The increased demand for housing and infrastructure development due to rapid urbanization and rising private investments fuels the market expansion. Market momentum is also supported by the growing adoption of telematics in construction equipment and rising equipment rental penetration in major construction hubs. At the same time, early adoption of electric construction equipment is rising as contractors focus on worker safety and emission compliance.

Market Statistics

Key Takeaways

- The Asia Pacific heavy construction equipment market led the market in 2025, accounting for more than 45.7% of total revenue. This is attributed to rapid industrialization and significant infrastructure development in the region.

- The North America heavy construction equipment market is projected to register the fastest growth, with a CAGR of 6.1% during the forecast period. The growth is driven by increased infrastructure investments, especially in the U.S. and Canada.

- The material handling equipment segment accounted for the largest market share in 2025, contributing 52.4% of total revenue. This is because of its crucial role in enhancing construction site productivity and efficiency.

- The mining segment is expected to register the fastest growth during the projection period, with a CAGR of 6.4%, due to the growing global need for natural resources and rising mineral demand.

- The <100 HP segment led the market with 25.3% revenue share in 2025. With increasing urbanization, the demand for heavy construction equipment with less than 100 HP is expected to rise.

- The 5-10L segment led the market in 2025, accounting for 43.2% share. There is a rise in various commercial projects, including roads, dams, urban infrastructure, and railways. This factor propelled demand for heavy construction equipment with a 5-10 L capacity.

Industry Dynamics

- The market demand for heavy construction equipment is driven by major infrastructure investments by governments worldwide in projects such as railways, roads, and bridges.

- The market's revenue is being driven by improving living standards and rapid urbanization, which are boosting the real estate construction sector.

- Growing demand for electrified and hybrid-powered construction equipment is opening new market opportunities.

- Cost and equipment maintenance costs could be a restraining factor for this market to grow.

- Rental, leasing, and fleet optimization are driving more procurement trends. As project durations shorten, rental companies and dealers are expanding their service offerings. Contractors are focusing on utilization, availability, service-level agreements, and monthly operating costs.

- Buyers are prioritizing the cost of ownership over purchase costs. As such, aftermarket services and parts are becoming a key competitiveness lever.

Source: Polaris Market Research Analysis

What is Heavy Construction Equipment?

Heavy construction equipment refers to construction machinery and vehicles specifically designed for various construction tasks and operations such as grading, drilling, excavating, hauling, and paving. These machines are used across various end-user industries, including mining, oil and gas, construction, manufacturing, forestry, and infrastructure.

For this study, heavy construction equipment covers large machines used for major construction work, such as digging, lifting, moving materials, and demolition. This includes heavy-duty construction machines for excavation, tunneling equipment, heavy lifting machines, and material handling machinery. Smaller construction equipment is included when they are used to support these heavy-duty construction activities.

Heavy construction equipment, such as loaders, excavators, and others, is essential for mining exploration. Governments in Latin American countries are placing a strong emphasis on the expansion of the mining sector to meet the rising demand for metals and ores. The expansion of the mining sector in the region fosters heavy construction equipment market growth. Furthermore, there is an increase in the utilization of earthmoving equipment, such as loaders, which are used in various industries for transporting heavy waste material, dirt, sand, and other materials. This shift results in higher fleet additions and replacement cycles for loaders and material-handling equipment in mining-led corridors.

The continuous movement of people from rural to urban areas increases the demand for housing and infrastructure. This urban expansion necessitates substantial construction activities. This has boosted the need for heavy construction equipment. Furthermore, the increasing focus on PPPs facilitates the execution of large-scale infrastructure projects. PPP megaprojects typically increase demand visibility over multi-year timelines. This improves OEM backlog stability and dealer inventory planning.

Benefits of Heavy Construction Equipment

Heavy construction equipment improves productivity and supports complete projects in less time. It reduces long-term labor costs and helps large-scale operations. It improves accuracy and work quality, leading to better project outcomes. Advanced machines improve site safety and reduce operational risks. Modern equipment helps lower fuel consumption and maintenance expenses, improving overall profitability. Better project planning is a direct result, along with fewer delays and a more efficient allocation of resources. For workers, heavy equipment minimizes physical effort and improves task efficiency. It supports safer working conditions and better control during operations.

Market Trend Analysis

Increasing Investment in Infrastructure Development

The governments across the globe are contributing significantly to the construction of infrastructure such as roads, bridges, railways, and airports. For example, in an article published in October 2024 by the WatchBlog of the United States Government Accountability Office, China invested about USD 679 billion in the construction of infrastructure through the Belt and Road Initiative in over 150 countries spanning from 2013 to 2022. These investments aim at boosting economic growth. They also seek to address critical gaps in developing nations by improving trade connectivity. The construction of these infrastructures calls for the use of heavy equipment, thus contributing to the development and growth of the heavy construction equipment market.

Expansion of Real Estate Sector

The growing real estate industry, driven by rapid urbanization and improving lifestyles, is one of the major factors contributing to revenue growth in the heavy construction equipment market. For example, according to the projection of the India Brand Equity Foundation, by 2047, the Indian real estate sector is expected to reach a market size of ~USD 5.8 trillion. It is expected that this growth will increase its share of the nation's GDP from the current 7.3% to approximately 15.5%. Such a booming sector has high demand for construction and, subsequently, heavy construction machinery such as excavators, loaders, and cranes, which are essential for meeting these construction requirements efficiently.

Electrification and Hybridization of Construction Fleets

To meet the need for sustainable equipment, manufacturers of construction machinery have begun introducing electric and hybrid heavy construction equipment to their ranges. The initial application targets machinery that operates for prolonged periods, such as when the savings in fuel and emissions benefits are visible to contractors. At present, widespread adoption is hampered by the unavailability of charging points and the high cost of batteries. However, usage is increasing in geographies that have started to incorporate sustainability considerations in equipment purchasing.

Telematics, Machine Control, and Automation-Ready Equipment

Telematics and machine control systems have also seen increased use on large projects. Contractors receive valuable information on how machines are being used, and it also decreases machine idling, aids in scheduling, and enhances construction productivity on the worksite. Machines that can be used to support automation processes, such as grading, help projects move faster. Crews can also work this way to reduce errors and increase accuracy through greater precision on projects like roads, excavations, and large infrastructure projects.

Source: Polaris Market Research Analysis

Segmental Insights

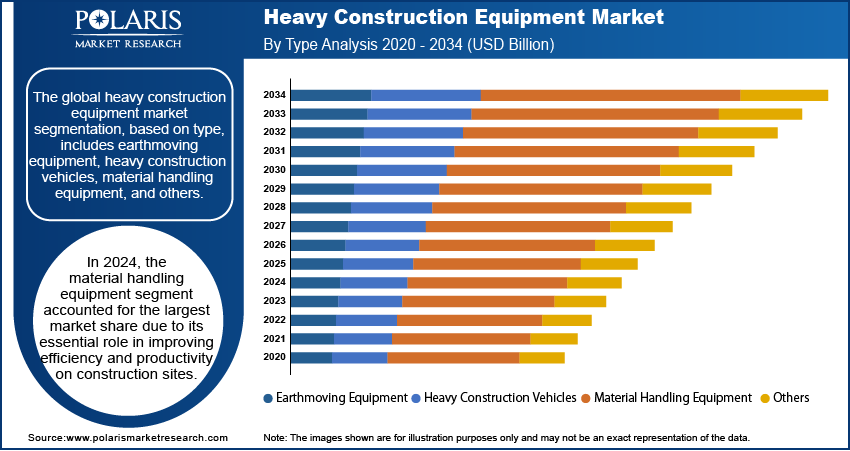

Evaluation Based on Type

The global heavy construction equipment market, based on type, is segmented into earthmoving equipment, heavy construction vehicles, material handling equipment, and others. The material handling equipment segment held the largest market share in 2025. This is driven by its primary role in increasing efficiency and productivity during the construction process. Material handling equipment, comprising forklift trucks, conveyors, and cranes, is essential for the lifting, loading, and unloading processes involved in the movement of construction materials during large construction activities. The increasing demand for fast construction and reduced operational expenditures is expected to lead to greater adoption. Technological development and the need for smart equipment, including telematics-enabled equipment and robotic systems, are expected to further enhance equipment productivity. So, the segment is projected to maintain its dominant position in the market.

Evaluation Based on End User

The global heavy construction equipment market, on the basis of end user, is divided into mining, infrastructure, construction, oil and gas, manufacturing, and other end-use industries. The mining category is anticipated to witness the fastest growth between 2025 and 2034. The mining segment is growing due to increased demand for minerals and natural resources worldwide, driven by industrialization and infrastructure development, especially in emerging regions. The demand for raw materials like coal, metals, and minerals is increasing significantly, thereby stimulating the development of the mining industry. In addition, technological developments in the mining industry are making operations more efficient. This has led to rapid growth in the mining segment.

Evaluation Based on Power Output

The power output segmentation of the heavy construction equipment market is done into <100HP, 101-200 HP, 201 - 400 HP, and >400 HP. The <100 HP segment led the market in 2025. Heavy construction equipment that has a power output of less than 100 HP allows for tasks in a limited space. Their use is common in projects such as highway repair and maintenance in urban areas, as the space here is often limited. Some commonly used low-power heavy machine equipment includes loaders, excavators, and compactors. As urbanization increases, the demand for heavy construction equipment with less than 100 HP is expected to rise.

Evaluation Based on Engine Capacity

The engine capacity segmentation of the heavy construction equipment market is done into <5L, 5-10L, and >10L. The 5-10L segment led the market in 2025. This engine capacity includes equipment such as compactors, road rollers, and crawler excavators. There has been a rise in various commercial projects. These include roads, dams, urban infrastructure, and railways. This has led to increased demand for heavy construction equipment with 5-10L capacity.

Source: Polaris Market Research Analysis

Regional Analysis

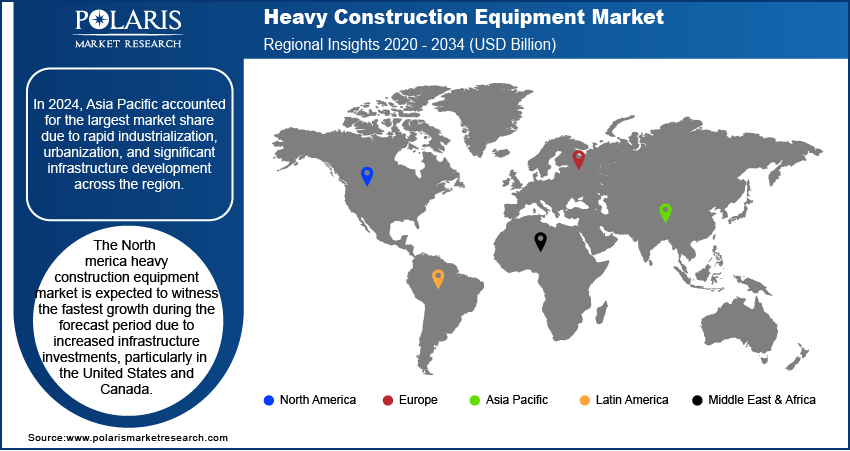

By geography, the heavy construction equipment market analysis covers North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific held the largest market share in 2025. This is because the region is witnessing fast-paced industrialization and infrastructure growth. Countries like China, India, and Japan are setting an example for other nations in large infrastructure projects, including the development of roads, bridges, airports, and residential buildings, which demand heavy construction equipment. For example, an article on the Asian Development Bank website in May 2024 stated that the total amount of potential infrastructure investments in Asia is expected to reach around USD 26 trillion by the end of 2030. This statement underscores the substantial demand for infrastructure development. It emphasizes the importance of heavy construction equipment in this region. Moreover, growing spending in the mining and manufacturing sectors contributes to the region's largest market share. In APAC, market expansion is further supported by large contractor ecosystems and high equipment utilization rates in fast-cycle urban development projects. Key market constraints in the region include cost inflation and OEM lead times for specialized equipment.

The North America heavy construction equipment market is expected to grow the fastest over the forecast period. Rising infrastructure expenditure, particularly in the US and Canada, is driving market growth. The region is experiencing an increase in projects initiated by the public and private sectors to modernize infrastructure networks, such as highways, bridges, and airports, using advanced construction equipment. Further, the growth of the real estate industry is driving the need for heavy construction equipment. The growing focus on energy infrastructure, specifically renewable energy sources such as wind and solar farms, is resulting in increased adoption of specialized heavy equipment in the North America market. For example, in October 2023, New York Governor Kathy Hochul announced the largest investment in renewable energy sources in the US. The project comprises 22 onshore and 3 offshore wind projects. It will produce a total of 6.4 GW of clean energy and enough electricity to supply 2.6 million homes and approximately 12% of New York's electricity demand at capacity. North America’s growth is also supported by fleet replacement cycles for aging fleets and stronger adoption of construction equipment telematics and machine control. In North America, emissions compliance and high maintenance cost pressures remain key operating considerations.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

The heavy construction equipment market is characterized by global and local players competing to capture a greater share through innovation, technological development, and strategic moves. The leading players in the market include Caterpillar Inc., Komatsu Ltd., Volvo Construction Equipment, Hitachi Construction Machinery, Liebherr Group, and Doosan Infracore. These players differentiate themselves by providing a wide portfolio of heavy construction equipment and by concentrating on innovations like automation of construction equipment, electric-powered construction machines, and sustainable construction machinery. Technological developments such as smart construction machines, telematics, and autonomous construction machines are transforming the market environment. Companies are focusing on fuel efficiency and environmental sustainability. Pursuing strategic moves like merger and acquisition activities, expanding geographical reach to capture emerging markets in new countries, and ensuring that all actions are customer-centric by providing services like after-sales service and maintenance services are some factors that companies are using to capture a greater share of the market and differentiate themselves in a highly dynamic market environment. Low emissions and high efficiency are driving manufacturers of construction machines to develop sustainable models.

A few key heavy construction equipment market players are Caterpillar Inc., CNH Industrial N.V., Deere & Company, Doosan Infracore Co Ltd., Hitachi Construction Machinery Co. Ltd., J C Bamford Excavators Ltd., Kobelco Construction Machinery Co. Ltd., Komatsu Ltd., Liebherr International AG, SANY Group Co. Ltd., Terex Corporation, Volvo Group, Wacker Neuson Linz GmbH, XCMG Group, Zoomlion Heavy Industry Science, and Technology Co. Ltd.

Caterpillar Inc. is a global manufacturer and distributor of industrial gas turbines, mining and construction equipment, diesel and natural gas engines, and diesel-electric locomotives. Caterpillar product portfolio includes compactors, asphalt pavers, road reclaimers, cold planers, material handlers, forestry machines, track-type tractors, telehandlers, motor graders, excavators, and pipelayers, as well as a variety of loaders and related parts and tools. In addition, they offer electric rope and hydraulic shovels, rotary drills, draglines, hard rock vehicles, mining trucks, tractors, wheel loaders, autonomous trucks, wheel tractor scrapers, dozers, autonomous ready vehicles and solutions, machinery components, safety services, and mining performance solutions. The company’s Resource Industries segment focuses on providing machinery for heavy construction, mining, quarrying, and aggregates.

Volvo CE is one of the largest manufacturers of articulated haulers and wheel loaders and a leading global producer of excavation equipment, road development machines, and compact construction equipment. Volvo CE is a part of the Volvo Group, which is known for its manufacturing of buses, trucks, construction equipment, and marine and industrial engines. The company also offers other solutions to its customers, such as servicing, financing, used equipment, rental, and other related construction equipment services. It deals in various industry segments, including building, heavy infrastructure, road construction, quarries & aggregates, agriculture & landscaping, mining, recycling & waste, material handling, utilities, forestry, oil & gas, and demolition.

How Do Leading Companies Compete?

Leading manufacturers don't compete on just the price of the machine or its size. Instead, they focus on a few practical areas that really matter to contractors and fleet owners:

Electrification Plans: Companies are introducing electric and hybrid machines. They are focusing on equipment used for long hours. These are addressed through partnerships that support worksite charging needs.

Digital Connected Tools: Most manufacturers provide built-in systems that help monitor machines and their performance and predict where maintenance may be required. This helps minimize downtime by making it easier to manage a fleet from day to day.

Dealer and Rental Reach: A strong dealer network with rental operations keeps the manufacturer closer to the customer. This provides speedy support and ensures easy equipment availability across regions.

Long-term Availability of the Machine: Customers are increasingly interested in factors such as spare parts, service response time, and ongoing maintenance programs—essentially, all the means that can ensure long-term dependability.

Productivity-Enhancing Features: Technologies such as machine guidance, operator assistance, and systems designed for future automation help improve job-site efficiency while reducing operator effort and safety risks.

List of Key Companies

- Caterpillar Inc.

- CNH Industrial N.V.

- Deere & Company

- Doosan Infracore Co Ltd.

- Hitachi Construction Machinery Co. Ltd.

- J C Bamford Excavators Ltd.

- Kobelco Construction Machinery Co. Ltd.

- Komatsu Ltd.

- Liebherr International AG

- SANY Group Co. Ltd.

- Terex Corporation

- Volvo Group

- Wacker Neuson Linz GmbH

- XCMG Group

- Zoomlion Heavy Industry Science and Technology Co. Ltd.

Market Developments

April 2026: Volvo Construction Equipment began serial production of electric articulated haulers, A30 Electric and A40 Electric. These haulers are expected to adopt zero-emission solutions in the quarrying and mining segments by February 2025: Liebherr AG unveiled its new generation of luffing jib cranes in Munich, Germany, upgrading its HC-L series with enhanced performance capabilities and reduced out-of-service downtime. (Source: volvoce.com)

June 2024: Volvo CE launched new electric machines at the Volvo Days held in Eskilstuna, Sweden. These models include the 23-tonne EC230 electric excavator and corded EW240 electric MH. The firm enhanced its offerings in sustainable construction equipment through the new models. (Source: volvoce.com)

May 2024: Volvo Construction Equipment introduced new products, refreshing its excavator line. This includes the EC500, EC400, and EC230, which feature advanced technology for better performance and fuel efficiency. In the same year, Volvo launched its first electric-wheeled excavator, the EWR150 Electric, as well as other electric products, the L90 Electric and L120 Electric, and wheel loaders. (Source: volvoce.com)

Collectively, these launches indicate an accelerating OEM focus on productivity upgrades and expansion into material-handling categories aligned with contractor demand for efficiency and lower emissions.

What is the future of the construction equipment industry?

The construction equipment industry is expected to grow steadily, backed by infrastructure development and urbanization. Companies are concentrating on advanced technologies such as automation and machine control systems to improve productivity and reduce project delays. The shift toward electric and hybrid equipment is increasing due to sustainability goals and emission regulations. Digital tools including telematics are helping improve equipment monitoring and maintenance. In addition, better planning and resource management are improving project efficiency. Despite challenges such as labor shortages and cost pressures, the industry is moving toward more efficient, cost-effective, and environmentally responsible operations in the coming years.

Market Segmentation

By Type Outlook (Revenue – USD Billion, 2021–2034)

- Earthmoving Equipment

- Heavy Construction Vehicles

- Material Handling Equipment

- Others

By Propulsion Outlook (Revenue – USD Billion, 2021–2034)

- ICE

- Electric

By Power Output Outlook (Revenue – USD Billion, 2021–2034)

- <100HP

- 101-200 HP

- 201 - 400 HP

- >400 HP

By Engine Capacity Outlook (Revenue – USD Billion, 2021–2034)

- <5L

- 5-10L

- >10L

By Application Outlook (Revenue – USD Billion, 2021–2034)

- Excavation & Demolition

- Tunneling

- Heavy Lifting

- Recycling & Waste Management

- Material Handling

By End User Outlook (Revenue – USD Billion, 2021–2034)

- Mining

- Infrastructure

- Construction

- Oil & Gas

- Manufacturing

- Others

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Research Methodology

This heavy construction equipment market assessment is based on information gathered from existing sources. The market research methodology includes industry reports, company documents, and government data, along with direct inputs from people working in the industry. The market size is estimated using both overall market data and individual segment-level data, and the results are cross-checked from multiple angles to ensure accuracy.

For forecast assumptions, the study looks at broader economic conditions, spending patterns in construction and infrastructure, how often equipment is replaced, and the pace at which new technologies like connected systems and electric equipment are being adopted.

Heavy Construction Equipment Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 222.16 billion |

| Market Size in 2026 | USD 233.05 billion |

| Revenue Forecast by 2034 | USD 344.05 billion |

| CAGR | 5.0% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Heavy Construction Equipment Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Heavy Construction Equipment Market FAQ's

The market for heavy construction equipment stood at USD 222.16 billion in 2025. It is projected to reach USD 344.05 billion by 2034.

The CAGR for the heavy construction equipment market is projected to be 5.0% between 2026 and 2034.

The demand for heavy construction equipment is expected to be driven by increasing investment in infrastructure development and the expansion of the real estate sector.

Asia Pacific held the largest market share in 2025. This is because the region is experiencing rapid industrialization and infrastructure development.

The material handling equipment segment led the heavy construction equipment market in 2025, owing to its role in increasing efficiency and productivity during the construction process.

• The mining segment is expected to witness the fastest growth during the forecast period due to increasing global demand for minerals and natural resources.

Download Sample Report of Heavy Construction Equipment Market

Please fill out the form to request a customized copy of the research report.