Immersive VR market Overview | Size, Share & Revenue Forecast, 2024-2032

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Market Statistics

Market Overview

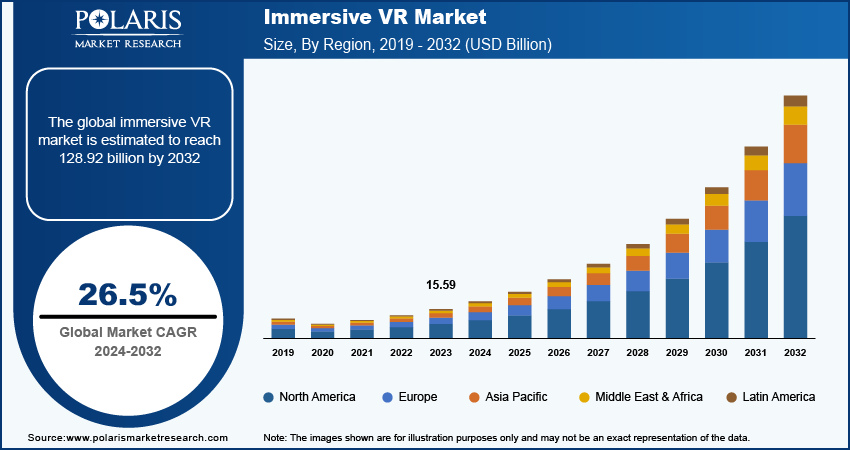

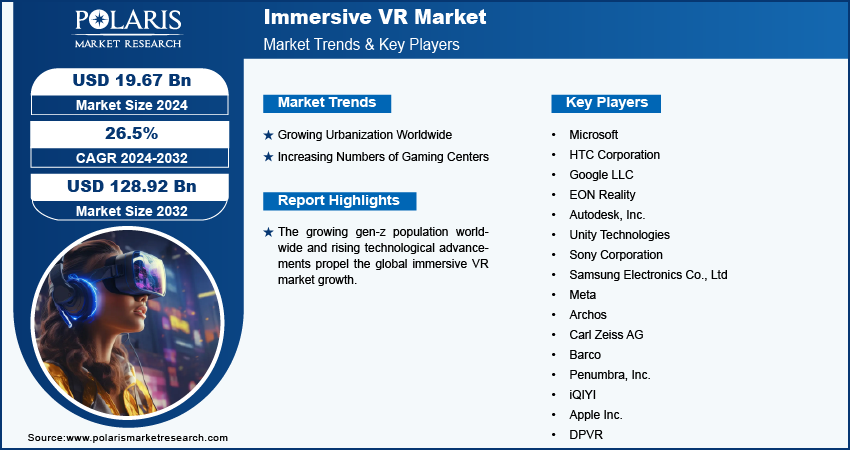

The immersive VR market size was valued at USD 15.59 billion in 2023. The market is projected to grow from USD 19.67 billion in 2024 to USD 128.92 billion by 2032, exhibiting a CAGR of 26.5% during 2024–2032.

Immersive virtual reality (VR) represents an advanced technology designed to transport users into fully interactive, three-dimensional computer-generated environments. This immersive experience is characterized by its ability to engage users deeply, allowing them to interact with virtual worlds as if they were physically present. The core of immersive VR includes head-mounted displays (HMDs), motion tracking systems, and haptic feedback devices.

The growing gen-z population worldwide is driving the immersive VR market. As per published data, Gen Z is estimated to make up more than a quarter, roughly 26%, of the total population worldwide in 2021. This population prefers interactive and engaging forms of entertainment. VR offers unique, immersive experiences that traditional media can't match, making it an appealing technology among Gen-Z for gaming, movies, and social interactions.

The rising technological advancements are projected to propel the global immersive VR market. Advances in VR hardware, such as lighter headsets with better resolution, wider fields of view, and improved tracking systems, make the experience more comfortable and engaging, which attracts more consumers. Additionally, innovations in software, including better graphics, more realistic physics, and more sophisticated AI, create richer and more immersive experiences. Such specifications attract gamers as well as industries such as education, healthcare, and training that leverage VR for various applications.

To Understand More About this Research: Download Sample Report

The immersive VR market is driven by the rising accessibility of VR content. The availability of VR content on popular streaming platforms makes it easier for users to access high-quality experiences without needing to invest in specialized hardware. This leads to increased interest and experimentation with VR.

Market Driver Analysis

Growing Urbanization Worldwide

There is rising urbanization across the world. According to the World Bank, the world's urban population is expected to increase by more than double by 2050. Urban areas typically have better access to high-speed internet and advanced technology. This infrastructure supports the use of VR, making it easier for residents to engage with immersive content and applications. Furthermore, urban centers are hubs for culture and creativity. VR enhances access to cultural experiences such as virtual museum tours or art installations, enabling residents to engage with local art and history in innovative ways. Therefore, the increasing urbanization across the globe drives the immersive VR market growth.

Increasing Numbers of Gaming Centers

Gaming centers allow users to try VR without needing to invest in expensive equipment. This hands-on experience may lead to increased interest and demand as users discover the engaging nature of immersive VR. Furthermore, gaming centers frequently host events and tournaments, which draw in crowds and create excitement around VR gaming. This community engagement helps promote the VR genre and builds a loyal customer base. Hence, the increasing number of gaming centers worldwide propels the global immersive VR market growth.

Market Segment Insights

Market Breakdown, By Component

Based on component, the global immersive VR market is segmented into hardware, software, and services. The hardware segment accounted for a major share of the market in 2023 due to rapid technological advancements and a growing consumer demand for high-quality immersive experiences. Key components such as headsets, controllers, and motion sensors contributed significantly to this growth as manufacturers continuously improved resolution, field of view, and comfort. The proliferation of gaming, training, and simulation applications also fueled hardware sales, with major brands releasing new models that catered to casual users and professionals. Additionally, the increasing integration of virtual reality into sectors such as education and healthcare accelerated the need for robust hardware solutions, further contributing to its major position in the market.

The software segment is expected to grow at a robust pace in the coming years owing to the expansion of content libraries, including games, educational programs, and virtual social environments. Furthermore, the growing emphasis on customization and personalization in software applications is estimated to enhance user satisfaction and retention, making this segment a vital area of investment. The segment is set to capture a significant share of the market as developers continue to innovate and improve software capabilities.

Market Breakdown By Technology

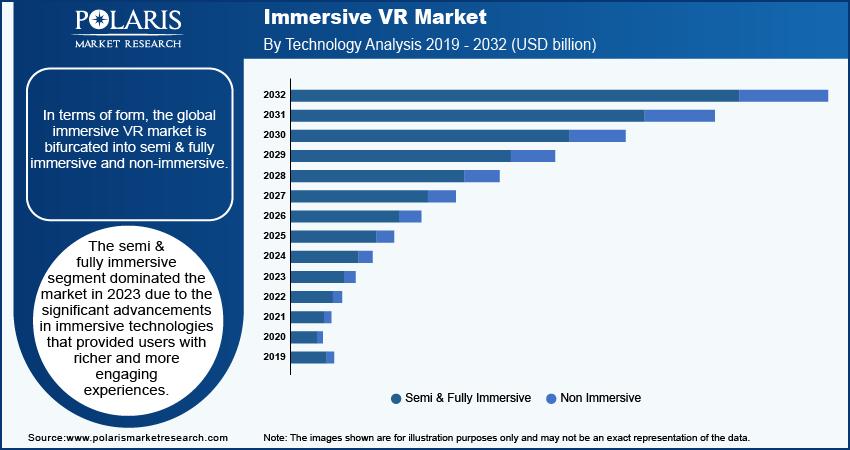

In terms of Technology, the global immersive VR market is bifurcated into semi & fully immersive and non-immersive. The semi & fully immersive segment dominated the market in 2023 due to the significant advancements in immersive technologies that provided users with richer and more engaging experiences. Industries such as gaming, training, and therapy increasingly adopted these technologies to create environments that closely mimic real-life interactions. The availability of high-quality headsets and responsive tracking systems enhanced user experience, driving demand among both consumers and businesses. Moreover, organizations recognized the effectiveness of fully and semi-immersive solutions in training programs, leading to improved learning outcomes and increased efficiency. This contributed to the segment's dominant position in the market.

The non-immersive segment is projected to grow at a rapid pace during the forecast period, owing to its accessibility and versatility. The demand for non-immersive applications continues to rise as more users engage with virtual environments through mobile devices and traditional screens. Businesses increasingly leverage non-immersive solutions for marketing, education, and collaboration, allowing them to reach a broader audience without the need for specialized hardware. Additionally, as organizations seek cost-effective alternatives to fully immersive setups, they find non-immersive technologies to be a practical choice for training and remote collaboration.

Regional Insights

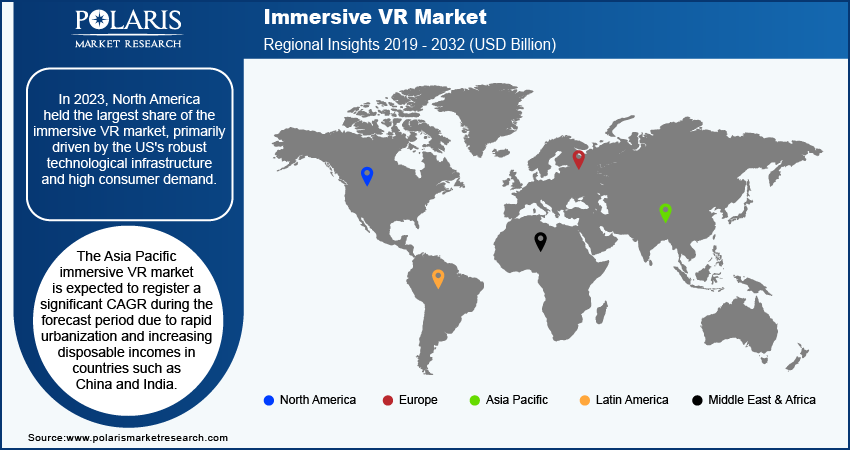

By region, the study provides market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2023, North America held the largest share of the global immersive VR market, primarily driven by the US's robust technological infrastructure and high consumer demand. The US leads in innovation, with numerous companies actively developing innovative hardware and software solutions that cater to entertainment and enterprise applications. The presence of major tech firms and startups in the region fosters a competitive environment that accelerates advancements in virtual experiences. Additionally, sectors such as gaming, education, and healthcare increasingly adopt these technologies, recognizing their potential to enhance user engagement and training effectiveness. Investments in research and development also play a crucial role as businesses seek to integrate immersive solutions into their operations, further contributing to North America’s prominent position.

The Asia Pacific immersive VR market is expected to record a significant CAGR during the forecast period due to rapid urbanization and increasing disposable incomes in countries such as China and India. Both mobile and console gaming continue to embrace virtual reality as the gaming industry experiences exponential growth in the region, attracting a younger audience for immersive content. Additionally, significant government initiatives aimed at fostering technological development, along with a growing focus on education and training applications, position the region for remarkable expansion. The Asia Pacific market is set to emerge as a key region in the coming years, with increasing investments from local and international companies in immersive technology.

Key Players and Competitive Insights

Major market players are investing heavily in research and development to expand their offerings, which will help the immersive VR market grow even more. Market participants are also undertaking a variety of strategic activities to expand their global footprint, with important market developments such as innovative launches, international collaborations, higher investments, and mergers and acquisitions between organizations. To expand and survive in a more competitive and rising market environment, immersive VR industry players must offer innovative solutions.

The immersive VR market is fragmented, with the presence of numerous global and regional market players. Major market players are Microsoft; HTC Corporation; Google LLC; EON Reality; Autodesk, Inc.; Unity Technologies; Sony Corporation; Samsung Electronics Co., Ltd; Meta; Archos; Carl Zeiss AG; Barco; Penumbra, Inc.; iQIYI; Apple Inc.; and DPVR.

Google LLC is a prominent US-based multinational technology company founded in 1998 by Larry Page and Sergey Brin. Initially created as a search engine, Google has evolved into one of the most influential companies globally, operating under the umbrella of its parent company, Alphabet Inc. Google LLC has significantly influenced the development of immersive virtual reality (VR) technologies, positioning itself as a key player in this rapidly evolving field. In June 2020, the company created a new technology to take immersive augmented reality (AR) and virtual reality (VR) experiences to a new level on consumer devices.

Meta Platforms Inc., formerly known as Facebook, is a major technology company headquartered in Menlo Park, California. Founded in 2004 by Mark Zuckerberg, Meta has evolved from a social networking site into a multifaceted organization that encompasses various platforms, including Facebook, Instagram, WhatsApp, and Oculus. The company has emerged as a major force in the era of immersive virtual reality (VR), significantly shaping the landscape of this technology. Its commitment to VR is driven by its vision of creating a metaverse, a collective virtual space where users can interact, socialize, and engage in various activities through digital avatars. In April 2024, Meta announced its plans to bring its VR headset into classrooms for students as young as 13 to create an 44immersive learning experience.

Key Companies:

- Microsoft

- HTC Corporation

- Google LLC

- EON Reality

- Autodesk, Inc.

- Unity Technologies

- Sony Corporation

- Samsung Electronics Co., Ltd

- Meta

- Archos

- Carl Zeiss AG

- Barco

- Penumbra, Inc.

- iQIYI

- Apple Inc.

- DPVR

ndustry Developments

January 2025: Google bought part of HTC’s extended reality division for USD 250 million to speed up development of the Android XR platform.

January 2025: Infinite Reality raised USD 3 billion in funding, increasing its valuation to USD 12.25 billion after acquiring Landvault and The Drone Racing League.

January 2025: Aonic finalized a USD 110 million deal to acquire nDreams, strengthening its presence in VR and mixed reality gaming.

December 2024: Samsung started making an XR headset powered by Snapdragon XR2+ Gen 2, priced at about USD 2,000, with first production limited to 300,000 units.

March 2024: iQIYI, an innovative online entertainment service in China, launched its latest VR immersive theater in Xi'an, Shaanxi province.

Market Segmentation

By Component Outlook (Revenue, USD Billion, 2019–2032)

- Hardware

- Software

- Services

By Technology Outlook (Revenue, USD Billion, 2019–2032)

- Semi & Fully Immersive

- Non-Immersive

By Device Outlook (Revenue, USD Billion, 2019–2032)

- Head Mounted Display

- Gesture Tracking Device

- Projectors & Display Wall

By End Use Outlook (Revenue, USD Billion, 2019–2032)

- Aerospace & Defense

- Manufacturing

- Automotive

- Education

- Media & Entertainment

- Gaming

- Healthcare

- Retail & E-commerce

- Others

By Regional Outlook (Revenue, USD Billion, 2019–2032)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Immersive VR Report Scope

| Report Attributes | Details |

| Market Size Value in 2023 | USD 15.59 billion |

| Market Size Value in 2024 | USD 19.67 billion |

| Revenue Forecast by 2032 | USD 128.92 billion |

| CAGR | 26.5 % from 2024 to 2032 |

| Base Year | 2023 |

| Historical Data | 2019–2022 |

| Forecast Period | 2024–2032 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2024 to 2032 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global immersive VR market size was valued at USD 15.59 billion in 2023 and is projected to grow to USD 128.92 billion by 2032.

The global market is projected to register a CAGR of 26.5 % during 2024–2032.

North America accounted for the largest share of the global market in 2023.

A few key players in the market are Microsoft; HTC Corporation; Google LLC; EON Reality; Autodesk, Inc.; Unity Technologies; Sony Corporation; Samsung Electronics Co., Ltd; Meta; Archos; Carl Zeiss AG; Barco; Penumbra, Inc.; iQIYI; Apple Inc.; and DPVR.

The software segment is projected for significant growth in the global market during the forecast period.

The semi & fully immersive segment dominated the market in 2023.

Download Sample Report of Immersive VR market

Please fill out the form to request a customized copy of the research report.