Industrial Robotics Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

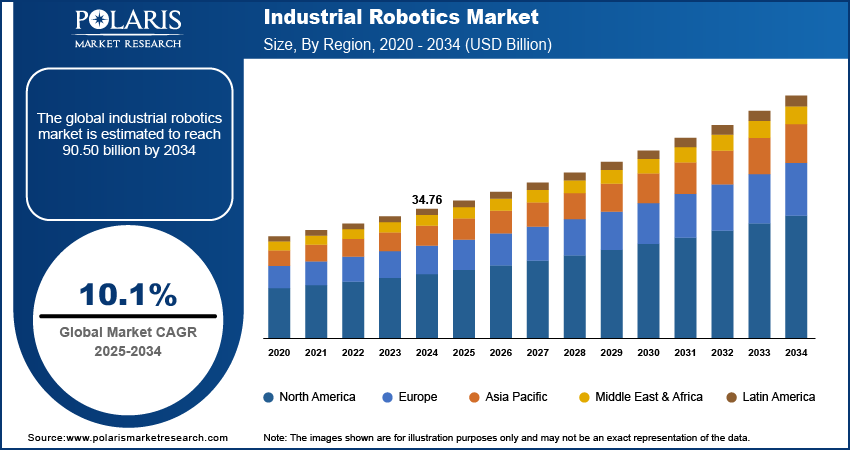

Industrial Robotics Market Summary

The industrial robotics market was valued at USD 38.13 billion in 2025 and is expected to grow at a CAGR of 10.1% during the forecast period. The factors attributed to the growing demand for industrial robotics are the shortage of skilled labor in manufacturing and the ever-increasing demand for cobots across several sectors.

Market Statistics

Key Takeaways

- The Robot Arms segment accounting for 39.9% market share in 2025 in the industrial robotics market is mainly due to its central role as the core functional unit of any robotic system.

- The collaborative industrial robots accounted 23.6% revenue share in 2025 due to its multiple advantages and related applications.

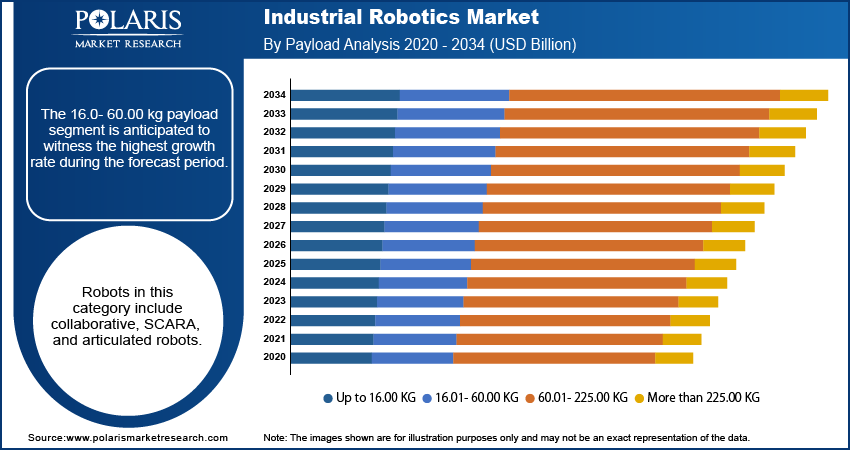

- The 16.0- 60.00 kg segment is expected to witness significant growth of 31.2% share due to rising demand for automation in arc welding, spot welding, and painting.

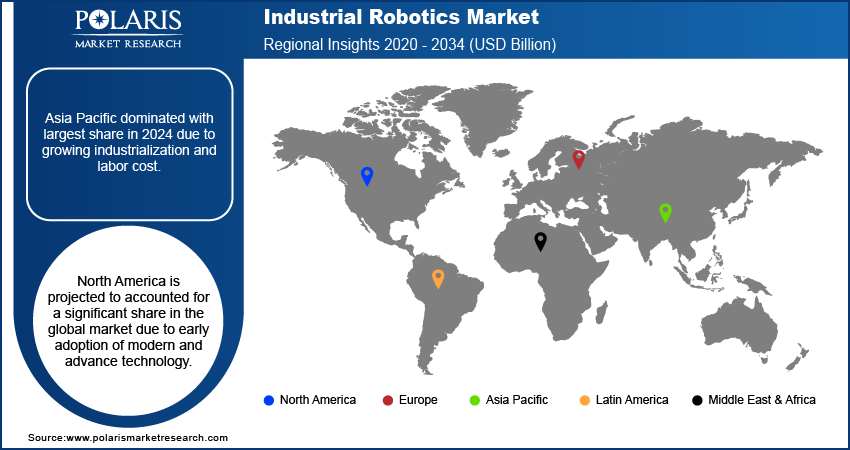

- Asia Pacific dominated with largest share in 2025 by holding 40.25% revenue share, due to growing industrialization and labor cost.

- North America is expected to register a CAGR of 10.9% during the forecast period, due to early adoption of modern and advance technology.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

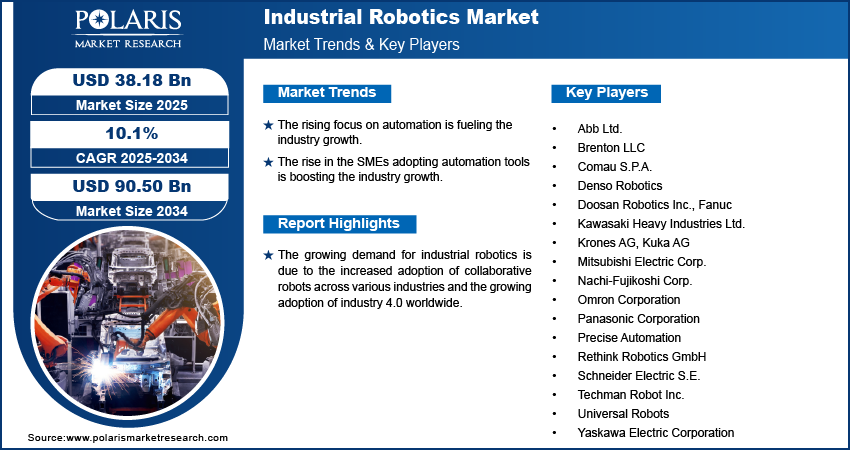

- The rising focus on automation is fueling the industry growth.

- The rise in the SMEs adopting automation tools is boosting the industry growth.

- Technological advancement is driving the growth.

- High initial investment and integration costs is limiting the adoption.

Source: Polaris Market Research Analysis

Impact of AI on Industry

- AI helps industrial robots to analyze data, learn from experience, and make real-time decisions which improve the manufacturing efficiency.

- AI-integrated vision systems enable robots to perform precise object recognition, quality inspection, and defect detection.

- AI helps to reduce downtime and maintenance cost by predicting failures before its happens.

What is Industrial Robotics?

Industrial robotics refers to the use of programmable, automated machines, such as robotic arms and collaborative robots (cobots). They are used to perform manufacturing and industrial tasks, including welding, assembly, material handling, and packaging. These systems enhance precision, efficiency, and consistency. It enables scalable production, reduced labor dependency, and improved safety across diverse industrial sectors.

What is the Difference Between Industrial Robots and Collaborative Robots (Cobots)?

| Aspect | Industrial Robots | Collaborative Robots (Cobots) |

| Design Purpose | Built for high-speed, repetitive, and heavy-duty industrial tasks | Designed to work safely alongside humans in shared workspaces |

| Safety Features | Operate in fenced or isolated environments for safety | Equipped with sensors and force-limiting features to prevent injuries |

| Payload Capacity | High payload capacity, suitable for heavy materials and large components | Lower payload capacity, ideal for light to medium tasks |

| Speed & Power | High speed and strength for mass production | Slower speeds to ensure human safety |

| Flexibility | Less flexible; requires reprogramming and setup for changes | Highly flexible; easy to program and redeploy for different tasks |

| Cost | Higher initial investment and integration costs | Lower cost, easier installation, and faster ROI |

| Ease of Use | Requires skilled programmers and engineers | User-friendly interfaces; can be programmed with minimal expertise |

| Typical Applications | Welding, painting, assembly lines, heavy material handling | Pick-and-place, packaging, quality inspection, small assembly tasks |

Source: Polaris Market Research Analysis

The beneficial advantages of industrial robots, such as system flexibility, cost-effectiveness, advanced data analytics, reduced waste, and workplace safety, are anticipated to accelerate the market's growth. Additionally, the market is driven due to the increased utilization of industrial robots across several verticals, such as automotive, pharmaceutics, cosmetics, food & beverages, and others. Industrial robots facilitate high payload lifting during the manufacture of vehicles and machinery customization. The market potential will increase as smart factories become more prevalent. Factors including growing consumer goods demand elevated public awareness of industrial mishaps, and employee safety are all fostering the development of the market.

Moreover, in order to include AI and create advanced sensors, manufacturers are focusing on R&D efforts, which will accelerate the market's growth over the forecast timeline. Venture capitalists are willing to invest in startups that create, test, and manufacture robots due to market shifts.

On the other hand, companies are progressively returning to their normal levels of production and services. Industrial robot companies are anticipated to restart operating at full capacity, which is anticipated to aid in the market's recovery over the forecast period.

Source: Polaris Market Research Analysis

Cost vs Productivity Benefits of Industrial Robots

| Aspect | Cost Considerations | Productivity Benefits |

| Initial Investment | High upfront cost for robot purchase, integration, and programming | Enables long-term automation with scalable output |

| Operating Costs | Maintenance, energy consumption, and skilled technicians required | Lower labor costs over time and reduced dependency on manual workforce |

| Production Speed | Setup and programming may take time initially | Faster cycle times and continuous 24/7 operation |

| Quality & Accuracy | Calibration and upgrades add to cost | High precision reduces defects, rework, and material waste |

| Workforce Impact | Training and potential workforce restructuring costs | Human workers can focus on higher-value tasks, improving overall efficiency |

| Return on Investment (ROI) | Payback period can be moderate to long depending on scale | Increased throughput and consistency drive strong ROI over time |

Source: Polaris Market Research Analysis

Industry Dynamics

Growth Drivers

The demand for industrial robots has increased due to the ongoing shift from manual to automated processes, the primary driver fueling the market's expansion. For industrial workflows to run smoothly, management, production, and control must be coordinated. Industrial robots are becoming more significant due to their ability to improve workflow accuracy and efficiency while facilitating operational procedures. Furthermore, there is an increasing need for industrial robots due to the rise of small enterprises, more automation investments, and stringent regulatory rules on handling hazardous materials and products. These robots also assist with lifting hefty weights while creating machines and automobiles. The introduction of smart factories increases the market's potential. Major firms are concentrating on mergers and acquisitions to increase their market position, thereby fueling the expansion.

Why are industries investing in Industrial Robots?

The adoption of robots offers high flexibility. Users can adapt to sudden changes in demand using robotic systems. Robotics also helps enhance product quality and reduce operating and capital costs. It provides energy and resource efficiency. Robotics adoption enables end-use businesses to remain competitive in the industry landscape. Owing to all these benefits, there is a rising installation of industrial robots worldwide.

| Annual Installations of Industrial Robots by End-Use Industries Across the World | |||

| End-Use Industry | 2021 | 2022 | 2023 |

| Automotive | 117.303 | 136.112 | 135.461 |

| Electrical/Electronics | 142.637 | 156.92 | 125.804 |

| Metal & Machinery | 68.385 | 66.115 | 76.831 |

| Plastic and Chemical Products | 25.025 | 23.54 | 22.402 |

| Food | 15.381 | 15.107 | 14.685 |

| Others | 54.963 | 60.997 | 74.838 |

| Unspecified | 102.45 | 94.155 | 91.281 |

Source: Polaris Market Research Analysis

Report Segmentation

The market is primarily segmented based on type, payload, component, application, end-use industry, and region.

| By Type | By Payload | By Component | By Application | By End-Use Industry | By Region |

|

|

|

|

|

|

Source: Polaris Market Research Analysis

Collaborative industrial type accounted the largest market share in 2025

The collaborative industrial robots accounted 23.6% revenue share in 2025 as these robots are designed to collaborate with people in a shared workspace. Collaborative robots are utilized in a wide range of applications, including packaging, pick-and-place, screw driving, assembly, lab testing, and quality inspection, as they can automate the work quickly. They can also usually be taught instead of programmed by an operator. Additionally, since collaborative robots can do repetitive tasks more quickly, they help enterprises increase manufacturing productivity while improving workplace safety. Due to its multiple advantages and related applications, the demand for collaborative robots is constantly increasing across various industrial verticals, including retail, healthcare, and automotive manufacturing. All these factors are responsible for the segment’s growth.

Source: Polaris Market Research Analysis

16.01-60.00 kg payload is expected to witness highest growth rate

The 16.0- 60.00 kg segment is expected to witness significant growth rate of 10.9% during the forecast period. Robots in this category include collaborative, SCARA, and articulated robots. The 16.01–60.00 kg payload capacity robots are mainly adopted in the automotive industry for arc welding, spot welding, painting, and many others. The rapidly expanding demand for automation in the electrical and electronics industry, where SCARA robots are widely employed for assembly and handling applications, is responsible for the segment's rapid expansion in the up to 16.01-60.00 kg weight range. SCARA robots have a higher operating speed and optional cleanroom requirements.

Asia-Pacific dominated the regional market

Asia Pacific dominated with largest share in 2025 by holding 40.25% revenue share due to rising labor costs, which forced manufacturers to automate their manufacturing processes to maintain a cost advantage. Additionally, due to moderate emissions and safety regulations, and government initiatives for foreign direct investment (FDI), automation in the APAC region will accelerate the growth of the global industrial robotics market. Major players in Asia pacific are at the leading edge in installing industrial robots, which also impels regional growth. The growing automotive and manufacturing industries in China & India are accelerating the product demand in this region.

North America is expected to register a CAGR of 10.9% during the forecast period. The region is one of the early adopters of advanced technologies and is home to several major players. North America also has significant investments in the manufacturing sector. Rising geopolitical tensions have prompted American manufacturers to bring production back to the region. At the same time, high labor costs make companies more reliant on robots rather than traditional factory workers. All these factors are driving the demand for industrial robotics in the region.

Source: Polaris Market Research Analysis

Some of the major players operating in the global market include:

- Abb Ltd.

- Brenton LLC

- Comau S.P.A.

- Denso Robotics

- Doosan Robotics Inc.

- Fanuc

- Kawasaki Heavy Industries Ltd.

- Krones AG

- Kuka AG

- Mitsubishi Electric Corp.

- Nachi-Fujikoshi Corp.

- Omron Corporation

- Panasonic Corporation

- Precise Automation

- Rethink Robotics GmbH

- Schneider Electric S.E.

- Techman Robot Inc.

- Universal Robots

- Yaskawa Electric Corporation

Recent developments

- February 2026: Kawasaki Heavy Industries, Ltd. launched CP110L, a high-speed palletizing robot. The robot has a maximum payload capacity of 110kg. (Source: global.kawasaki.com)

- July 2025: Bedrock Robotics, an autonomous vehicle startup founded by Waymo and Segment veterans, announced an $80 million funding round with support from investors Eclipse and 8VC. The company is developing a retrofitted self-driving kit for construction and other worksite vehicles. CEO Boris Sofman stated that existing fleets, equipped with intelligence, sensors, and computing, capable of understanding project goals and adapting to changing conditions, will be upgraded by Bedrock. (Source: techcrunch.com)

- May 2024: Neura Robotics and OMRON formed a strategic partnership to integrate AI-enhanced cognitive robots into manufacturing processes, thereby increasing productivity and safety. (Source: neura-robotics.com)

Industrial Robotics Market Report Scope

| Report Attributes | Details |

| Market size value in 2025 | USD 38.13 billion |

| Market size value in 2026 | USD 41.87 billion |

| Revenue forecast in 2034 | USD 90.63 billion |

| CAGR | 10.1% from 2026 - 2034 |

| Base year | 2025 |

| Historical data | 2021 - 2024 |

| Forecast period | 2026 - 2034 |

| Quantitative units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Segments Covered | By Type, By Payload, By Component, By Application, By End-Use Industry, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

| Key Companies | Abb Ltd., Brenton LLC, Comau S.P.A., Denso Robotics, Doosan Robotics Inc., Fanuc, Kawasaki Heavy Industries Ltd., Krones AG, Kuka AG, Mitsubishi Electric Corp., Nachi-Fujikoshi Corp., Omron Corporation, Panasonic Corporation, Precise Automation, Rethink Robotics GmbH, Schneider Electric S.E., Techman Robot Inc., Universal Robots, and Yaskawa Electric Corporation. |

Source: Polaris Market Research Analysis

FAQ's

The market size was valued at USD 38.13 Billion in 2025 and is projected to grow to USD 90.63 Billion by 2034.

The market is projected to register a CAGR of 10.1% during the forecast period.

A few of the key players in the market are Abb Ltd., Brenton LLC, Comau S.P.A., Denso Robotics, Doosan Robotics Inc., Fanuc, Kawasaki Heavy Industries Ltd., Krones AG, Kuka AG, Mitsubishi Electric Corp., Nachi-Fujikoshi Corp., Omron Corporation, Panasonic Corporation, Precise Automation, Rethink Robotics GmbH, Schneider Electric S.E., Techman Robot Inc., Universal Robots, and Yaskawa Electric Corporation.

The collaborative industrial robots accounted 23.6% revenue share in 2025.

The 16.0- 60.00 kg segment is expected to witness significant growth rate of 10.9%.

Download Sample Report of Industrial Robotics Market

Please fill out the form to request a customized copy of the research report.