Iron And Steel Market Demand, Industry Share, 2026-2034

REPORT DETAILS

Iron And Steel Market Summary

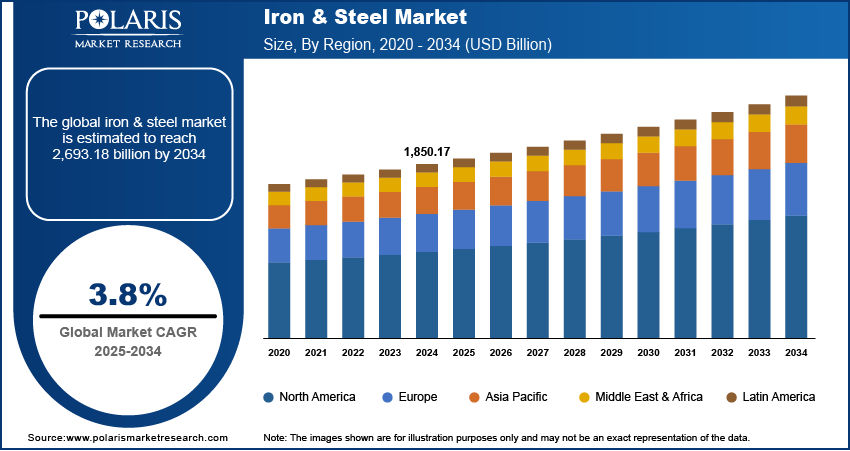

The global iron And steel market size was valued at USD 1.44 trillion in 2025, growing at a CAGR of 3.78% from 2026 to 2034. The expansion of automotive industry and rising urbanization across the world drive the demand for iron and steel.

Market Statistics

Key Takeaways

- Asia Pacific dominated with the largest share of 68.0% in 2025. The regional dominance is driven by rapid urbanization and strong infrastructure development.

- The market in North America is projected to witness substantial growth at a 3.2% CAGR. This is owing to increased construction activities and a growing automotive sector.

- The U.S. is expected to experience significant growth at a 3.0% CAGR. The market growth in the country is driven by federal infrastructure spending and a resurgence in domestic manufacturing.

- The steel segment dominated with a larger share of 82.0% in 2025. This is due to its wide usage in construction and transportation.

- The automotive and transportation segment is expected to experience significant growth at a 4.5% CAGR. Rising vehicle production in emerging regions and the increasing shift toward electric vehicles (EVs) in developed economies drive the segment’s growth.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The expansion of the automotive industry is driving the demand for high performance steel and iron ore.

- Rising urbanization is fueling the industry growth as the demand for commercial and residential buildings grows.

- Many developing countries are investing in manufacturing and industrial activities to support economic growth, thereby driving the demand for steel and iron.

- High energy costs and environmental regulations are restraining the iron and steel industry.

AI Impact on Iron and Steel Market

- AI contributes to increasing the output of iron and steel manufacturing processes through the effective operation of furnaces and reduced energy consumption.

- AI ensures better quality of iron and steel products through defect detection and uniform strength and composition.

- AI assists in predicting failures in machinery to minimize downtime.

- AI enhances supply chain management through demand prediction based on real-time analysis of data.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

What are Iron and Steel?

Iron and steel are strong, durable metals widely used in construction, transportation, and various manufacturing applications. Iron is a natural element extracted from ore, while alloy steel is made by combining iron with a small amount of carbon to improve strength and flexibility. Together, they form the backbone of modern infrastructure, from buildings and bridges to tools and machines.

The construction industry is expanding rapidly worldwide due to multiple factors. According to the HBI, in the U.S. alone, the employment in construction increased by 239,000 in 2024 compared to 2023. The construction industry uses iron and steel in almost every type of building such as residential, commercial, and industrial. From skyscrapers and factories to airports and shopping malls, steel provides the structural backbone. The need for high-quality steel increases as countries invest in modern infrastructure and repair old buildings. Additionally, government spending on housing, smart cities, and transportation hubs is growing, thereby driving the growth.

Many developing countries are investing in manufacturing and industrial activities to support economic growth. This includes building plants, machines, storage facilities, and transport systems, all of which use iron and steel. The demand for steel-based equipment and structures grows as countries expand their industrial base. This is especially evident in regions such as Southeast Asia, Africa, and parts of South America. Industrial development further leads to more demand for basic infrastructure, creating a cycle that supports continuous steel consumption in these regions.

Drivers/ Opportunities/ and Challenges

Expansion of Automotive Industry: The automotive sector utilizes substantial quantities of steel for manufacturing vehicle bodies, engines, and safety components. The demand for steel is increasing as more people in both developed and developing countries are purchasing vehicles. According to the Organization of Motor Vehicle Manufacturers, in North America Alone, 7,079,750 new passenger vehicles were registered. Even as electric vehicles become more common, steel remains a core material due to its strength and cost efficiency. Lightweight and high-strength steels are further being used to meet fuel efficiency and safety regulations. As a result, vehicle manufacturing remains a significant contributor to global steel consumption.

Rising Urbanization: The need for basic infrastructure, such as roads, bridges, housing, and public transportation, grows as more people move into cities. According to the World Bank Group, in 2024, 58% of the total population lived in urban areas. Iron and steel are essential materials in these projects because they provide structural support. Many developing countries are investing in new infrastructure to support growing populations, while developed countries are repairing or replacing old structures. This steady demand for construction materials keeps the iron and steel industry active. Moreover, large-scale public projects such as railways, airports, and water systems further depend on a consistent supply of steel products, thereby driving the growth.

Rise of Green Steel and Decarbonization Technologies

With the emergence of green steel and decarbonization, there has been a major change in the conventional steel-making industry, with increasing emphasis on reducing carbon emissions based on global climate targets. Within the realm of steel making, one of the new trends has been hydrogen-based steel making, where hydrogen has replaced coal as fuel to produce low-carbon or no-carbon emissions. Additionally, the use of technology like CCUS has seen widespread application within existing plants in order to reduce emissions. Yet another technology that has seen increasing popularity is EAF (Electric Arc Furnace), which uses scrap metal for energy conservation as compared to conventional steel plants.

Global Trade Policies and Tariff Impacts

Policies on international trade, tariffs, and quotas are vital in the iron and steel sector as far as cost, logistics, and competition are concerned. Export and import duties may affect the dynamics of trade by making steel costlier in some areas while protecting production at home elsewhere. Countries often implement trade barriers, anti-dumping laws, and quotas to control the movement of goods in the sector. Any changes in international political dynamics or foreign relations may also affect the logistics and supply chain of raw materials and finished products within the sector. There could be a disruption in the delivery processes, which may alter costs and supplies for international players in the market. Therefore, iron and steel producers should continually adapt to the changing business environment in terms of international policies and practices.

Raw Material and Energy Cost Challenges

The iron and steel industries are greatly influenced by price changes in terms of raw materials and energy costs. This factor has an immediate effect on production costs and profit. Inputs like iron ore, coking coal, natural gas, and electricity account for the majority of production costs. If prices of inputs become high or uncertain, production costs will be higher as well. There are several reasons for such a price change, including supply and demand changes, disturbances within mining, geopolitical factors, and energy price uncertainty. In addition, production requires great amounts of energy resources and thus is greatly dependent on the price of electricity and fuel. Such cost pressures affect profit margins but also shape the decision-making process of manufacturers in terms of production volumes, prices, and investment choices.

Source: Polaris Market Research Analysis

Segmental Insights

Product Analysis

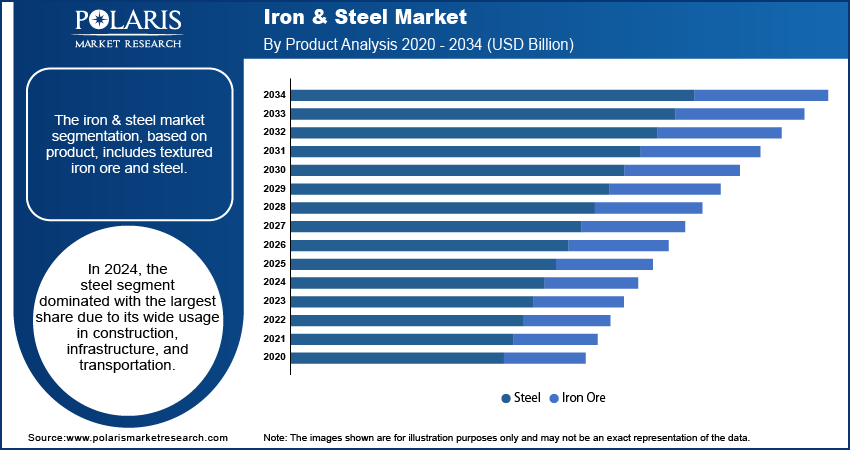

The segmentation, based on product, includes textured iron ore and steel. In 2025, the steel segment dominated with a larger share of 82.0% due to its wide usage in construction, infrastructure, and transportation. Steel is preferred over other materials because it offers high strength, flexibility, and cost-effectiveness. Countries with ongoing urban development projects, such as China, India, and several Middle Eastern nations, experience demand for structural and reinforcement steel. Developed regions such as North America and Europe also maintained strong consumption, especially in repairing old infrastructure. The availability of advanced steel types further fuels its demand across multiple sectors, thereby driving the segment growth.

The iron ore segment is expected to experience significant growth of 3.3% during the forecast period due to high production levels in key countries such as Australia, Brazil, and India. These countries supplied large amounts of iron ore to steel producers worldwide, especially in Asia. The demand from countries such as China, where steel production remains high, supported the iron ore industry. Despite price fluctuations, the consistent need for iron ore as the base material for steel-making helped it retain a central position in the global supply chain, especially in regions focused on manufacturing and heavy industry, thereby driving the segment growth.

End Use Analysis

The segmentation, based on end use, includes building And construction, automotive And transportation, heavy industry, consumer goods, and other. In 2025, the building and construction segment dominated with the largest share of 45.0% as urban development, population growth, and government-funded infrastructure projects fuels the demand. Countries in Asia Pacific, especially India and China, experience a rise in residential and commercial building activities. In developed regions, renovation of old infrastructure boosted steel consumption. Steel’s properties such as durability, cost efficiency, and ease of fabrication made it ideal for construction. From bridges and railways to high-rise buildings and warehouses, the material was in steady demand, thereby driving the segment growth.

The automotive And transportation segment is expected to experience significant growth of 4.5% during the forecast period due to rising vehicle production in emerging regions and the shift towards electric vehicles in developed economies. Automakers are increasingly using advanced high-strength steel to make vehicles lighter and more fuel-efficient while maintaining safety standards. Rail, air, and shipping transport systems also require strong, durable materials, which fuels steel usage, thereby driving the segment growth.

Source: Polaris Market Research Analysis

Regional Analysis

Asia Pacific Iron And Steel Market Trends

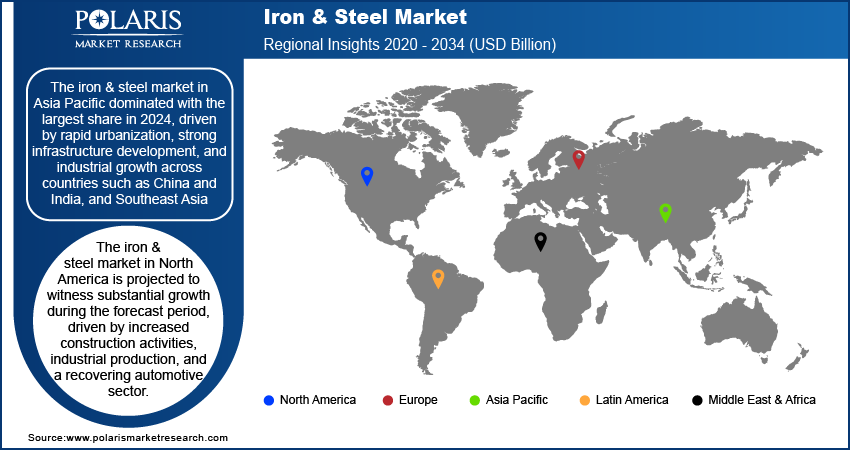

Asia Pacific dominated with the largest share of 68.0% in 2025, driven by rapid urbanization, strong infrastructure development, and industrial growth across countries such as China and India, as well as Southeast Asia. The region is home to several major steel-producing countries and further supports strong export. Government investments in transportation, housing, and energy infrastructure boost steel consumption. Additionally, local manufacturing and construction sectors are expanding, further increasing the use of iron and steel. Asia Pacific’s strong economic activity and large population further fuels both production and consumption, thereby driving the growth.

China Iron And Steel Market Insights

The industry in China is expected to witness significant growth at a CAGR of 3.0% during the forecast period, due to massive infrastructure projects, ongoing urbanization, and a strong manufacturing sector. China’s Belt and Road Initiative further fuels steel exports for international infrastructure projects. Production levels remain high due to internal needs and global demand. The growing construction, automotive, and industrial machinery sectors further fuels the market growth in China.

North America Iron And Steel Market Analysis

The market in North America is projected witness substantial growth at a CAGR of 3.2% in the coming years, driven by increased construction activities, industrial production, and a recovering automotive sector. The U.S., Canada, and Mexico benefit from integrated supply chains under trade agreements such as USMCA. Regional investments in infrastructure upgrades and energy projects further supported demand. The region imports a portion of its steel. Rising focus to modernize facilities and increase efficiency has fuel the local production. North America is further focusing on sustainable steelmaking practices, which could shape future demand and investments in low-emission technologies.

Source: Polaris Market Research Analysis

U.S. Iron And Steel Market Analysis

The U.S. iron And steel market is expected to experience significant growth at a CAGR of 3.0% during the forecast period, driven by federal infrastructure spending and a resurgence in domestic manufacturing. Key sectors such as construction, automotive, and energy contributed to rising steel demand. The government's push to improve roads, bridges, and public buildings boosted domestic steel consumption. The U.S. further experience an increase in steel recycling and electric arc furnace usage to meet sustainability goals. Moreover, trade policies and tariffs influenced the import-export balance, encouraging more domestic production, thereby driving the growth.

Europe Iron And Steel Market Insights

The industry in Europe is expected to experience rapid growth capturing 12.0% share in 2025, driven by infrastructure renewal, automotive production, and green energy projects. The region focuses heavily on sustainable steel production, investing in low-carbon technologies and recycling methods. Countries such as Germany, Italy, and France lead in both production and consumption. The European Union’s climate goals are influencing how steel is made, with a shift toward electric arc furnaces and hydrogen-based production. Additionally, strong demand from the construction and automotive sectors, combined with policy support for clean industry, boost the growth in Europe.

Germany Iron And Steel Market Assessment

The market growth in Germany is attributed to its strong industrial base and advanced manufacturing sector. The demand for steel in automotive production, machinery, and construction is growing. The country is further a leader in developing green steel technologies, with several pilot projects using hydrogen to reduce emissions in steelmaking. Germany imports a portion of its iron ore and has well-established steel production facilities, particularly in Ruhr. Government support for climate-friendly industry and ongoing infrastructure investments continue to drive demand for steel across the country.

Key Players and Competitive Analysis

The iron And steel market is highly competitive and dominated by a mix of global giants and regionally strong players. Leading companies such as Arcelor Mittal S.A., China BaoWu Steel Group Corporation Limited, and Nippon Steel Corporation maintain their positions through large-scale production capacities, technological advancements, and global distribution networks. Chinese firms such as HBIS Group, Jiangsu Shagang Group, and Shougang Group benefit from strong domestic demand and government support, contributing significantly to global steel output. JFE Steel Corporation and POSCO HOLDINGS INC. play key roles in Asia Pacific, focusing on innovation and high-grade steel products. Meanwhile, Tata Steel Limited represents one of the major players from India, expanding globally through strategic acquisitions and sustainable practices. The market is shaped by price volatility, raw material costs, trade regulations, and growing emphasis on green steel production, pushing competitors to invest in cleaner technologies and diversified product portfolios.

Key Players

- Arcelor Mittal S.A.

- China BaoWu Steel Group Corporation Limited

- HBIS Group

- JFE Steel Corporation

- Jiangsu Shagang Group

- Nippon Steel Corporation

- POSCO HOLDINGS INC.

- Shougang Group

- Tata Steel Limited

Industry Developments

- June 2026: Bhilai Steel Plant (BSP) inaugurated its vendor collaboration meet, “Samanvay-2026.” According to India’s Ministry of Steel, the meet is a part of BSP’s expansion program to scale up capacity from 6.8 million tonnes per annum (MTPA) to 10.2 MTPA by 2030. (source: pib.gov.in)

- June 2026: JSW Steel reported that the Blast Furnace 3 (BF3) at Vijayanagar is under shutdown for the upgradation of capacity. The company stated that the BF3 is expected to restart in the second fortnight of June 2026. (source: nseindia.com)

- July 2025: Tata Steel signed an MoU with Australia’s InQuik Group to launch modular bridge construction technology in India, expanding its infrastructure portfolio with sustainable, rapid-build solutions that strengthen rural connectivity and mark a major step in construction innovation. (Source: tatasteel.com)

- July 2025: ArcelorMittal Nippon Steel India commissioned a new galvanising line at its Hazira plant, enabling domestic production of advanced high-strength steel up to 1180 MPa for the automotive sector, as part of its USD 6.96 billion expansion project. (Source: amns.in)

- May 2025: Tata Steel inaugurated the Phase II expansion of its Kalinganagar plant, increasing crude steel capacity from 3 to 8 MTPA with an investment of USD 3.13 Billion, strengthening its infrastructure footprint and reinforcing Odisha as a key industrial hub. (Source: tatasteel.com)

Iron And Steel Market Segmentation

By Product Type Outlook (Volume, Million Tons, Revenue, USD Trillion, 2021–2034)

- Iron Ore

- Steel

By End Use Outlook (Volume, Million Tons, Revenue, USD Trillion, 2021–2034)

- Building And Construction

- Automotive And Transportation

- Heavy Industry

- Consumer Goods

- Other

By Regional Outlook (Volume, Million Tons, Revenue, USD Trillion, 2021–2034)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East And Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East And Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Iron And Steel Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 1.44 Billion |

| Market Size in 2026 | USD 1.49 Billion |

| Revenue Forecast by 2034 | USD 2.01 Billion |

| CAGR | 3.78% from 2026 to 2034 |

| Base Year | 2024 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Volume in Million Tons, Revenue in USD Trillion and CAGR from 2026 to 2034 |

| Report Coverage | Volume Forecast, Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Iron And Steel Market FAQ's

The global market size was valued at USD 1.44 trillion in 2025 and is projected to grow to USD 2.01 trillion by 2034.

The global market is projected to register a CAGR of 3.78% during the forecast period.

Asia Pacific dominated with the largest share of 68.0% in 2025.

A few of the key players in the market are Arcelor Mittal S.A., China BaoWu Steel Group Corporation Limited, HBIS Group, JFE Steel Corporation, Jiangsu Shagang Group, Nippon Steel Corporation, POSCO HOLDINGS INC., Shougang Group, and Tata Steel Limited.

The steel segment dominated with a larger share of 82.0% in 2025.

The automotive and transportation segment is expected to experience significant growth at a 4.5% CAGR.

Download Sample Report of Iron And Steel Market

Please fill out the form to request a customized copy of the research report.