Linerless Labels Market Size & Share Global Analysis Report, 2026-2034

REPORT DETAILS

REPORT DETAILS

Linerless Labels Market Summary

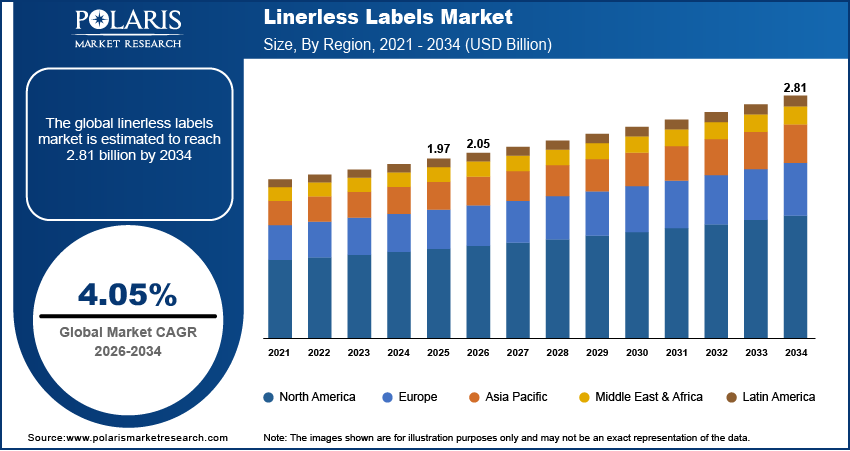

The linerless labels market size was valued at USD 1.97 billion in 2025. According to our linerless labels market forecast, the market is expected to grow at a CAGR of 4.05% from 2026 to 2034. Key factors driving the demand for linerless labels include increasing demand for packaged food and beverages and growing focus on sustainability. Cost-efficiency and operational benefits of linerless labels also drive market growth.

Market Statistics

Key Takeaways

- The hot melt-based segment led the linerless labels market in 2025. This is due to the versatility and strong adhesion properties of hot melt adhesives.

- The digital printing segment is projected to witness the fastest growth. The growing demand for customized and short-run label applications contributes to the segment’s growth.

- Europe accounted for the largest market in 2025. Stringent environmental regulations promoting sustainable packaging solutions drive the region’s leading market position.

- Asia Pacific is projected to register the fastest growth. This is due to the growth of end-use industries and rising investments in manufacturing in the region.

Linerless labels are a form of label that does not require the use of a liner, thus contributing to waste reduction and faster processing in high-speed labeling applications. The demand for linerless labels is rising in the packaged food industry, retail price tagging, and logistics/shipping applications in the e-commerce industry. This is due to businesses looking for sustainable labeling options that also improve operational efficiency.

Industry Dynamics

- Changing consumer lifestyles have led to increased demand for packaged foods and beverages. This is driving market growth.

- Increased focus on sustainability is boosting the adoption of linerless labels.

- The incorporation of smart labeling technologies such as RFID and NFC is expected to present several market opportunities.

- Limited compatibility with existing labeling equipment may hinder market growth.

To Understand More About this Research: Download Sample Report

Linerless labels have a unique adhesive and a silicone release coating, which enables them to stick to the product and also be easily removed. This makes them environmentally friendly because they generate less waste and have lower disposal costs. Additionally, linerless labels have a positive environmental impact by reducing the business or warehouse's footprint. The rolls of linerless labels hold more labels than traditional labels, making them more environmentally friendly because they reduce transportation and storage costs. Linerless labels also make manufacturing more efficient since there are fewer media roll changes between print runs.

With linerless labels, a release coating prevents the adhesive from bonding with the label below it on the roll, making dispensing easy without any waste of the liner. This enables more labels to be accommodated on a roll, increasing labeling speed in the food industry, retail, and logistics sectors. The performance may differ based on the material, temperature, and humidity levels. This is why it’s important to choose the right adhesive and printing technology to make sure that the barcode scans properly and the labels are strong.

Industry Dynamics

Increasing Demand for Packaged Food and Beverages

The growing demand for packaged food and beverages is the primary driver of the linerless labels market. The increased demand is associated with changing consumer lifestyles. Hectic schedules and a need for convenience foods characterize modern consumer lifestyles. This creates demand for effective labeling solutions across a range of products. Here, linerless labels have an edge over traditional labels in terms of labeling speed and material consumption. Linerless packaging is particularly suited for high-volume items and fast-moving consumer goods. It is typically used for date coding, ingredient and handling labels, and variable information labeling on packaged food lines. Hence, the growing demand for linerless labels is driven by the surge in packaged food and beverage sales.

Growing Focus on Sustainability

Another driving force in the linerless labels market is the increasing requirement for sustainability and environmental protection. The United Nations Environment Programme (UNEP) highlighted in a 2022 report the importance of minimizing plastic waste and adopting circular economy principles in packaging. Linerless labels contribute to this by eliminating the requirement for the silicone-coated release liner, thus minimizing the volume of waste generated and the environmental impact of disposing of the labels. Besides minimizing waste, linerless rolls can also optimize transportation by allowing more labels to be packed in a single roll. This optimizes the density of the labels and may eliminate the need for frequent shipments and storage in large-scale applications. This meets sustainability requirements and is thus another factor contributing to the adoption of linerless labels.

Cost-Efficiency and Operational Benefits

The cost-effectiveness and operational advantages of linerless labels make it a significant driver of their growing adoption. Linerless labels minimize roll changes by holding more labels per roll than conventional labels, resulting in reduced downtime for labeling and improved productivity in the labeling process. The Bureau of Energy Efficiency (BEE), Government of India, highlighted in a 2021 report the significance of energy and material efficiency in industrial operations. Linerless labels help conserve materials in packaging. They may also reduce transportation and storage costs due to their higher density. These economic and environmental benefits make linerless labels an attractive option for businesses looking to optimize their supply chains and reduce overall expenses.

Challenges and Adoption Barriers

Although there are many efficiency advantages associated with linerless labels, their use can be hampered by printer and applicator compatibility, as in some cases the equipment used in the operation may need to be specifically designed for them. Linerless labels challenges such as adhesive buildup, edge lifting, or changes in humidity and temperature may also affect their suitability for a particular application. As a result, many buyers choose to conduct a pilot test before using them on a large scale.

Segmental Insights

Assessment By Product Type

By product type, the segmentation includes water-based, solvent-based, hot melt-based, UV curable, and others. This segmentation of linerless adhesive types is a reflection of the chemistry of choice in adhesives that affect the bonding strength, durability, and performance under specific handling and storage conditions. Of these, the hot melt-based segment accounted for the largest revenue share in 2025. This is mainly because of the versatility and strong adhesion properties of hot melt adhesives. Hot melt linerless labels can bond well to various surfaces. They are also cost-effective for large-scale applications. This makes them a popular choice across many industries. The strong performance and existing infrastructure for hot melt-based linerless labels have played an important role in establishing them as the dominant segment.

The UV curable segment is expected to have the highest growth rate during the forecast period. This is due to the growing demand for high-quality and aesthetically pleasing labels. The UV-curable adhesive has high resistance to chemicals, abrasion, and environmental conditions, making it suitable for applications where a long-lasting, high-quality finish is desired. In addition, improvements in the UV curing system and technology have resulted in increased processing speed and lower energy consumption.

Evaluation By Printing Technology

In terms of printing technology, the segmentation includes digital printing, flexo printing, offset printing, letterpress, gravure printing, screen printing, and others. The flexo printing type accounted for the largest revenue share in 2025 due to its ability to efficiently handle long print runs and support a variety of materials, which are essential for the diverse applications of linerless labels. The existing infrastructure and cost-effective mass production also led to the widespread use of flexo printed linerless labels.

Digital printing is expected to be the fastest-growing printing technology segment. The growing demand for customized, short-run label applications drives the high growth rate of digital printing. Digital printing can efficiently meet this without the use of printing plates. The various benefits of digital printing are making it an attractive option for businesses. This contributes to its high growth rate.

Evaluation By Adhesion

Based on adhesion, the segmentation includes permanent, removable, repositionable, and others. The permanent segment led the linerless labels market in 2025. This is due to the high demand for secure, long-lasting labeling across industries such as pharmaceuticals and logistics. The reliability of permanent adhesives in keeping permanent linerless labels securely attached to the product for a long time has been a major factor in their widespread adoption.

The repositionable segment is expected to register the highest growth rate during the forecast period. Repositionable linerless labels are gaining popularity in retail price marking, promotional labeling, and temporary logistics identification, where flexibility and clean removal capabilities enhance handling efficiency. This is because the demand for flexible labels that can be easily removed or adjusted without damaging the product or the label itself is increasing. Repositionable linerless labels are being used in the retail sector, where price tags or promotional labels need to be changed frequently, and in the logistics sector, where temporary identification is required. This has led to increased demand for repositionable linerless labels, which are expected to drive the segment's growth.

Evaluation By End Use

By end use, the segmentation includes retail, food & beverages, home & personal care, logistics, pharmaceuticals, and others. The food & beverages industry accounted for the largest revenue share in 2025. This is due to the large number of packaged products that use linerless labels extensively for product identification, branding, and the provision of critical consumer information. The steady demand for packaged food & beverages products across the globe created a significant and constant demand for linerless labeling solutions.

The logistics segment is expected to register the fastest growth rate in the coming years. This is because of the increasing use of warehouse automation labels. There is also a need for efficient and sustainable labeling solutions in warehousing and inventory management. Linerless labels offer many advantages. These include reduced waste and increased roll capacity. These are very beneficial for optimizing logistics processes in the industry. The rising e-commerce industry and the resulting increase in shipping are also driving demand for linerless labels in logistics.

Regional Analysis

The Europe linerless labels market has recorded the largest market share in 2025. This is due to strict environmental regulations in the region, the adoption of sustainable packaging solutions, the presence of mature end-use industries such as food & beverage and pharmaceuticals, and the high level of technology adoption in labeling. The proactive approach to sustainability and the mature industrial base have driven substantial demand for linerless label solutions in Europe. The leadership position of Europe is also supported by mature food and retail supply chains.

The Asia Pacific region is expected to witness the highest growth rate during the forecast period. The high growth rate is driven by expanding end-use industries, particularly food processing, retail, and logistics. The growth is high in rapidly developing countries such as India, Thailand, and others. Rising investments in manufacturing, growing consumer awareness of sustainable packaging, and increasing demand for effective labeling solutions are among the key factors driving the growth of the Asia Pacific linerless labels market. Linerless labels demand in India and Southeast Asia is driven by the expansion of food processing capacity, growth in organized retail, and ongoing logistics modernization.

Key Players and Competitive Insights

Some of the major active players in the linerless labels market include Avery Dennison Corporation, Multi-Color Corporation, CCL Industries Inc., Constantia Flexibles Group GmbH, Coveris Management GmbH, Mondi Group, UPM Raflatac (UPM), Herma GmbH, SATO Holdings Corporation, Cenveo Corporation, and Fort Dearborn Company. These linerless labels market key players offer a diverse range of linerless label products catering to various end-use industries and applications.

The linerless labeling ecosystem comprises material suppliers like facestock, adhesive, and coating suppliers, as well as label converters and printer/applicator original equipment manufacturers. The competitive advantage is now being measured by sustainability and performance under different end-use conditions.

Global and regional rivals drive the linerless labels competitive landscape. The level of competition is sustained by factors such as innovation in products and materials, integration of printing technology, and the capacity to provide customized solutions that meet customers' specific requirements. The major strategies adopted by rivals include diversifying product lines, focusing on sustainable and cost-effective solutions, and improving distribution networks.

List of Key Companies

- Avery Dennison Corporation

- CCL Industries Inc.

- Cenveo Corporation

- Constantia Flexibles Group GmbH

- Coveris Management GmbH

- Fort Dearborn Company

- Herma GmbH

- Mondi Group

- Multi-Color Corporation

- SATO Holdings Corporation

- UPM Raflatac (UPM)

Linerless Labels Industry Developments

- August 2025: NAStar Inc. advanced its ongoing R&D sustainable innovation research. The company used eco-friendly water-based emulsion adhesives and its specialized coating technology to develop custom linerless solutions that meet specific application needs.

- June 2025: Coveris launched its new “Linerless Envelope.” The new envelope is a lightweight and environmentally friendly option compared to the traditional cartonboard sleeve. The new envelope is intended for high-speed automated applications. It features innovative linerless labeling technology that enables high-quality decorative printing and finishing without carrier backing paper.

- September 2024: Hubergroup Print Solutions introduced its three new solvent-based ink series. The series includes Gecko Gold, Gecko Platinum NT, and Gecko Platinum Plus. The inks are specially customized for the needs of the Asian market.

- March 2024: PM Raflatac, a global supplier of innovative and sustainable self-adhesive paper and film products, opened a new slitting and distribution terminal in Mumbai, India.

Linerless Labels Market Segmentation

By Product Type Outlook (Revenue – USD Billion, 2021–2034)

- Water-Based

- Solvent-Based

- Hot Melt-Based

- UV Curable

- Others

By Printing Technology Outlook (Revenue – USD Billion, 2021–2034)

- Digital Printing

- Flexo Printing

- Offset Printing

- Letterpress

- Gravure Printing

- Screen Printing

- Others

By Adhesion Outlook (Revenue – USD Billion, 2021–2034)

- Permanent

- Removable

- Repositionable

- Others

By Component Outlook (Revenue – USD Billion, 2021–2034)

- Facestock

- Adhesive

- Release Coating

By End Use Outlook (Revenue – USD Billion, 2021–2034)

- Retail

- Food & Beverages

- Home & personal care

- Logistics

- Pharmaceuticals

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Linerless Labels Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 1.97 billion |

| Market Size in 2026 | USD 2.05 billion |

| Revenue Forecast by 2034 | USD 2.81 billion |

| CAGR | 4.05% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Linerless Labels Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

How is the report valuable for an organization?

Workflow/Innovation Strategy: The linerless labels market has been segmented into detailed segments of product type, printing technology, adhesion, component, and end use. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Market Entry Strategies: Growth in the market is influenced by the focus on sustainability and cost-effectiveness. This will help the market appeal to environmentally responsible companies and those seeking ways to improve their operations. Marketing efforts will need to focus on waste reduction, reduced transportation costs, and improved productivity offered by linerless solutions. Partnerships with industries related to the end use of products, such as the food and beverage and logistics industries, to demonstrate successful implementations will also help promote growth. Educational efforts focusing on the versatility and advancements in linerless label technology will also be important.

FAQ's

The global linerless labels market stood at USD 1.97 billion in 2025. It is projected to reach USD 2.81 billion by 2034.

A few of the key players in the market include Avery Dennison Corporation, Multi-Color Corporation, CCL Industries Inc., Constantia Flexibles Group GmbH, Coveris Management GmbH, Mondi Group, UPM Raflatac (UPM), Herma GmbH, SATO Holdings Corporation, Cenveo Corporation, and Fort Dearborn Company.

Asia Pacific contributes notably to the linerless labels industry. This is due to the expansion of end-use industries, such as food and logistics, in the region.

The market is projected to account for a CAGR of 4.05% between 2026 and 2034.

Linerless labels are commonly used for product packaging, price tags, and shipping labels. Their use in these sectors saves space and allows more labels on a roll.

Linerless labels are more sustainable as they do not have a backing liner that is discarded.

Linerless labels require special printers or applicators that can support the labels without a backing liner.

Linerless labels can result in less waste as there is no liner to dispose of. The cost of equipment for linerless labels may be higher initially. However, companies can save money in the long run through lower material use.

Download Sample Report of Linerless Labels Market

Please fill out the form to request a customized copy of the research report.