Medical Stampings Market Growth Trends, 2026-2034

REPORT DETAILS

Medical Stampings Market Summary

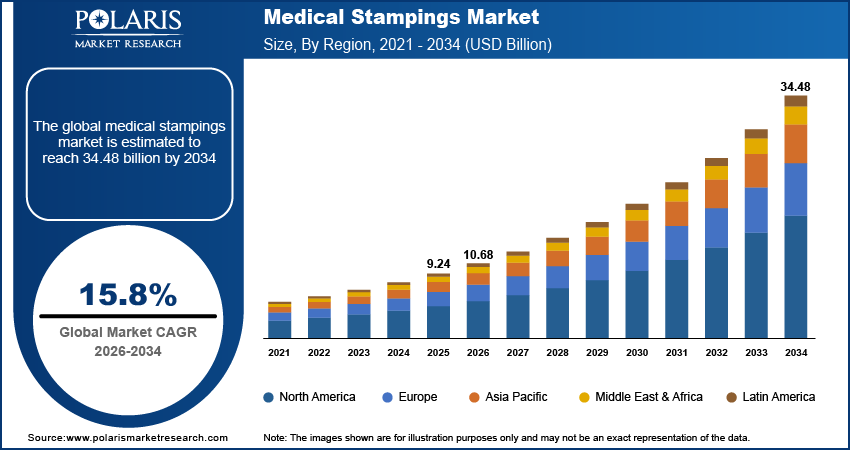

The global medical stampings market is estimated around USD 9.24 billion in 2025, with consistent growth anticipated during 2026–2034. Growth is supported by rising surgical procedure volumes, expanding implantable device production, and increasing demand for high-tolerance metal components across minimally invasive surgery platforms. The market is projected to grow at a CAGR of 15.8% during the forecast period.

Market Statistics

Key Takeaways

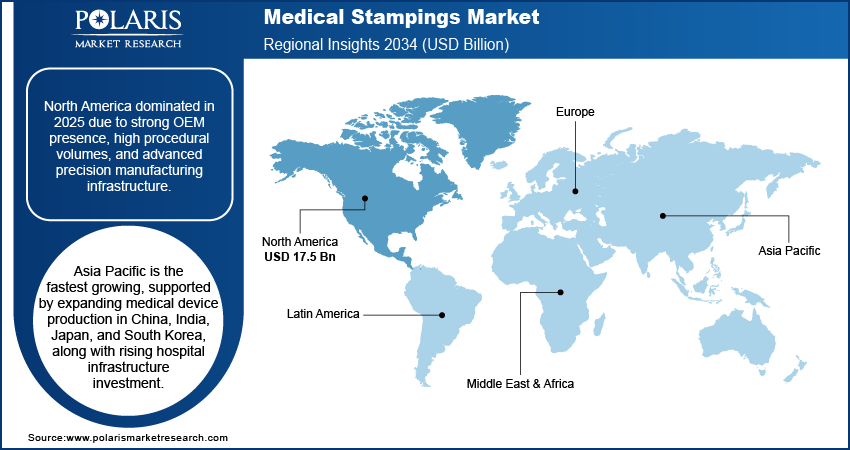

- North America accounted for the largest regional share of around 37.9% in 2025, driven by strong OEM presence, advanced medical device manufacturing infrastructure, and increasing investments in robotic-assisted and minimally invasive technologies.

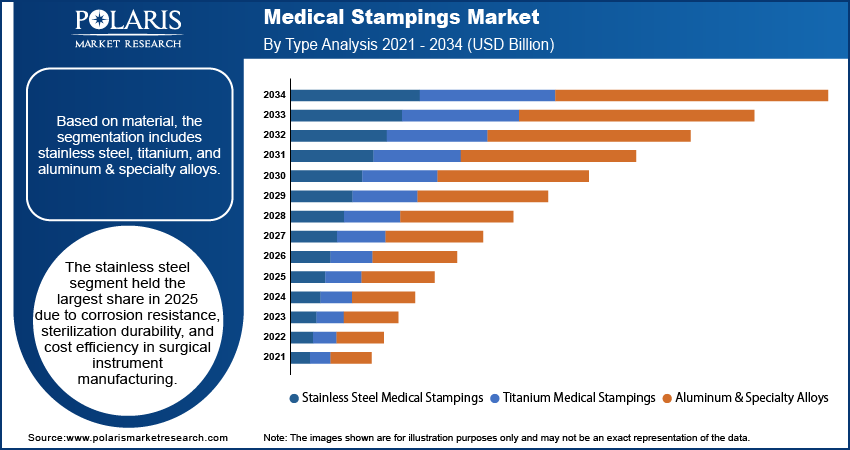

- By Material, Stainless Steel segment accounted for the largest share of approximately 61.7% in 2025, supported by superior corrosion resistance, mechanical strength, and cost efficiency in surgical instrument manufacturing.

- By Process, Progressive Die Stamping segment accounted for the largest share of around 54.3% in 2025, driven by its capability to produce high-volume, precision components through multi-stage tooling operations.

- By Application, Surgical Instruments segment accounted for the largest share of nearly 58.6% in 2025, supported by frequent hospital procurement and high surgical volumes requiring durable and sterilization-resistant stamped components.

Industry Dynamics

- Rising surgical intervention volumes and implantable device demand are strengthening consumption of precision metal stampings.

- The growing use of minimally invasive tools is driving the micro-precision and thin-gauge stamped components market.

- Price volatility in the stainless steel, titanium, and specialty alloys markets is creating cost challenges in stamping.

- Breakthroughs in micro-stamping, nano-forming, and inspection systems are opening up high-complexity growth opportunities.

What Are Medical Stampings?

The medical stampings market is the production of precision metal parts made using high-accuracy stamping technology optimized for the medical industry. Unlike general-purpose stamping, the medical metal stampings market must meet more stringent dimensional tolerances, material traceability, and regulatory documentation. These components are embedded within surgical instruments, implantable devices, and diagnostic equipment, where dimensional stability and surface integrity directly affect clinical performance. Precision medical stampings market activity includes thin-gauge stainless steel brackets used in orthopedic fixation systems, micro-formed springs and contacts in diagnostic analyzers, and injector pen components requiring repeatable actuation mechanics.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

What Is Included in the Medical Stampings Market?

The medical stampings market usually refers to raw stamped parts manufactured by progressive die stamping, deep drawing, and fine blanking techniques. The scope of the market also include secondary processing steps like deburring, heat treatment, electro-polishing, passivation, and surface coating, if these services are outsourced under contract. Some definitions of the medical stampings market further include sub-assemblies and partial OEM integration, where stamped parts are packaged together with fasteners, molded parts, and micro-electronic components before shipment.

Why Market Numbers Differ Across Reports?

Market size estimates differ based on the scope of the definition. Some market studies focus exclusively on raw medical component stampings, while others include finishing services, engineered assemblies, and contract manufacturing as part of the medical metal stampings market. Variations also occur based on whether dental, veterinary, and laboratory device markets are included in the scope of the market size estimate.

Drivers & Opportunities

Rising prevalence of chronic diseases and aging population: The rising incidence of chronic diseases leads to an overall rise in the number of surgical procedures in the areas of cardiovascular, orthopedic, oncologic, and respiratory medicine. The aging demographic trend further fuels the number of surgical procedures, as older people tend to have more surgical needs and demands for implantable solutions. The World Health Organization estimates that chronic diseases could be responsible for 86% of the estimated 90 million annual deaths by 2050 if the trend continues. This escalation in clinical demand directly expands the need for surgical tools, implantable hardware, and device assemblies that rely on precision-formed metal components.

Rising demand for minimally invasive surgical instruments and implantable devices: The trend towards minimally invasive procedures drives the need for smaller, lighter, and more tolerant components. These procedures rely on complex surgical instruments, endoscopic equipment, and miniature implantable devices that demand precision metal forming. Minimally invasive procedures have shown a 7% rise in the American Society of Plastic Surgeons’ 2023 report, signifying a continued preference for less invasive treatment options. This, in turn, directly fuels the demand for medical stampings that can provide dimensional accuracy, corrosion resistance, and biocompatibility in smaller sizes. The rise of minimally invasive procedures, therefore, fuels the long-term growth prospects in the medical stampings market.

Restraints & Challenges

Raw material volatility: Price variability in stainless steel, titanium, and specialty alloys introduces cost variability in medical stamping processes. The materials used in the medical industry have to adhere to strict regulatory requirements and biocompatibility. This reduces the ability to substitute materials when prices increase. The medical stampings market is constrained by raw material variability, which reduces the ability to standardize pricing in the industry.

Opportunity

Micro-precision and nano-stamping technologies: Technologies in micro-precision and nano-stamping are now capable of producing ultra-small components with high precision, which are needed for next-generation minimally invasive surgical instruments and micro-implants. The advancements in these technologies make it possible to achieve higher precision and repeatability, which can be integrated into smaller device architectures. As surgical instruments and micro-implants are being made smaller with increasing functionality, the need for advanced stamping technology is also growing. This trend is poised to help high-precision manufacturers tap into new opportunities in the medical stampings market.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the medical stampings market by material, manufacturing process, and application to help readers identify the fastest expanding and most attractive demand segments.

By Material

-

Stainless Steel Medical Stampings

Stainless Steel Medical Stampings account for the largest share due to their balance of corrosion resistance, mechanical strength, and cost efficiency. Types such as 304 and 316L remain a crucial part of surgical and reusable applications. Their resistance to multiple sterilization processes – autoclave, chemical, and plasma – makes them a vital component of medical stampings used in surgical instruments.

-

Titanium Medical Stampings

Titanium medical stampings have the fastest growth rate among materials owing to its excellent biocompatibility and strength-to-weight ratio. Implantable Device stampings and orthopedic device stampings are increasingly using titanium when corrosion resistance in the human body is a key factor.

-

Aluminum & Specialty Alloys

Aluminum medical stampings and copper alloy medical components are used in application-specific markets. Aluminum is used in diagnostic and minimally invasive device enclosures that require electromagnetic shielding or weight savings.

-

Portable vs Static CDU

Portable CDU systems are a growing niche market, especially in test lab settings and phased liquid cooling installations. Static systems are more common in permanent systems, offering more capacity and stability in the integration process.

By Manufacturing Process

-

Progressive Die Stamping

Progressive die medical stampings drive the market due to its use in precision metal stamping for the medical industry on a large scale. Multi-stage tooling enables cutting, forming, and piercing in one press operation.

-

Deep Draw Stamping

Deep draw medical stampings are chosen for cylindrical or cup-shaped parts such as implantable device housings or diagnostic device cases. This technique preserves integrity without weld lines. Compared to progressive stamping, deep draw emphasizes shape over speed. Wall thickness consistency and metal flow become essential when creating titanium or stainless steel shells.

-

Micro Stamping & Automation

Micro stamping medical components are the fastest-growing market segment. The need for smaller, minimally invasive device parts is driving tolerances below the sub-millimeter level. Automated medical stamping solutions combine vision inspection and robotic manipulation to ensure dimensional accuracy.

By Application

-

Surgical Instruments

Medical stampings for surgical instruments have the largest market share owing to its frequent hospital purchases. Forceps, retractors, scissors, and clamps use stainless steel stampings extensively. The demand is driven by the volume and is related to the number of surgical procedures performed.

-

Implantable & Orthopedic Devices

Stampings of implantable devices and stampings of orthopedic devices have the largest growth rate. Rising joint replacement procedures and trauma surgeries drive titanium adoption.

-

Cardiovascular & Diagnostic Equipment

Cardiovascular device components and diagnostic equipment stampings are for precision-driven applications. Thin stamped shields, connectors, and enclosures require very tight dimensional tolerances to prevent signal degradation.

Source: Polaris Market Research Analysis

Regulatory, Quality & Compliance Landscape - Medical Stampings Market

Regulation plays a direct role in determining suppliers in the medical stampings market. Medical-grade metal components require stringent documentation, validation, and traceability requirements that are in line with the overall medical device production compliance. OEMs are also evaluating stamping suppliers based on the maturity of process control, inspection, and the ability to provide audit-ready documentation.

-

FDA Quality & Manufacturing Controls

For FDA regulations concerning medical metal components, stamping suppliers must have validated processes, material certification, traceability of lots, and change control. Justification of differences in tooling changes and production processes is also required. In critical use and implantable devices, inspection results and statistical process control are necessary. Traceability in medical components requires investment in digital tracking systems, inspection automation, and controlled environments.

-

ISO 13485 & Quality Management

There is a growing trend in sourcing towards ISO 13485-certified stamping companies. ISO 13485 certification demonstrates a company’s systematic approach to quality management, corrective actions, and documented risk mitigation. For original equipment manufacturers, ISO 13485 compatibility reduces FDA risks and makes supplier selection easier.

-

EU MDR & Global Compliance Pressure

The EU MDR effect on the medical component industry has increased the complexity of documentation and the level of supplier audits. Component suppliers must now verify the origin of the materials used, the functionality of the components, and provide more detailed documentation. The global OEMs also stress the need for standardized documentation and cleanroom manufacturing processes, especially for MII and implant components.

Market Implication

The ability to comply with regulations has become the determinant of competitiveness. Stamping suppliers who invest in traceability technology, ISO compliance, and clean manufacturing processes will gain better alignment with the OEMs, while those who do not comply will see their role in the regulated medical supply chain shrink.

Regional Analysis

North America Medical Stampings Market Assessment

North America medical stampings market dominated the market due to concentrated OEM presence, advanced device manufacturing ecosystems, and sustained capital infusion into robotic and minimally invasive platforms. Large investments in robotic-assisted surgery and diagnostic equipment create a demand for tight tolerance biocompatible stamped components. In February 2026, Banner Health increased its base of surgical equipment with the installation of 49 da Vinci 5 systems from Intuitive Surgical, upgrading from the earlier versions. The high volume of procedures in the U.S. medical metal stampings industry, while localization of supply chains mitigates dependence on imported machining, improving the resilience of the regional manufacturing base.

Asia Pacific Medical Stampings Market Insight

Asia Pacific medical stampings market is growing at a rapid pace driven by growing medical device production capacity in countries such as China, India, Japan, and South Korea. China’s manufacturing centers speed up the production of surgical and implantable device components, enhancing the presence of China medical device stampings in the market. Japan’s history of Japan high-precision manufacturing enables the production of high-end orthopedic and cardiovascular assemblies that demand micron-level tolerances. The increasing number of hospital constructions, along with the growing investments in MedTech, India’s industry forecasted to expand from USD 14 billion to USD 30 billion in 2030, fuels the demand for tools and components. The supply chain becomes more localized, with OEMs incorporating stamping facilities near the final assembly lines of devices.

Europe Medical Stampings Market Overview

Europe medical stampings market progresses with strict government regulation and a robust local MedTech ecosystem. The German market is the foundation of regional manufacturing with its dominance in Germany precision medical components, in addition to existing manufacturers in Switzerland and France. The need for stamped parts in orthopedic fixation devices and cardiovascular systems continues to escalate with the importance of precision and traceability of materials remaining a top priority. Government regulations promote local procurement, and OEMs continue to develop local supply chains that meet EU medical device regulations.

Middle East Medical Stampings Market Assessment

Middle East market expands with the development of specialty hospitals and high-capacity surgical centers, especially in the UAE and Saudi Arabia. The rising use of advanced surgical equipment and implantable devices drives up the demand for the importation of precision-stamped components. Governments focus on the diversification of healthcare infrastructure, promoting collaboration with international device manufacturers and gradually localizing specific manufacturing processes. Although production ecosystems are still in their infancy compared to North America and Europe, supply chain development is increasingly integrating with regional healthcare expansion plans.

Heat Map Analysis

| Region | Market Position | Growth Momentum | Regulatory Strength | Recycling Infrastructure | Secondary Lead Production Base |

| North America | Dominant | High | Very High | Medium–High | Low |

| Asia Pacific | High | Very High | Medium | Medium | Low |

| Europe | High | Medium | Very High | High | Low |

| Middle East | Emerging | High | Medium | Low | Low |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The medical stampings industry is still moderately consolidated, with a focus on precision engineering companies and diversified medical technology suppliers. Medical metal stamping producers are differentiated by their ability to form within tight tolerances, have ISO 13485-certified systems in place, and maintain clean manufacturing environments that meet OEM audit requirements. From a purchasing perspective, supplier selection is driven by process validation, scalability, and integration support. Industry positioning is maintained through strategic partnerships in medical manufacturing and mergers & acquisitions in medical stampings to enhance technical and geographic diversity.

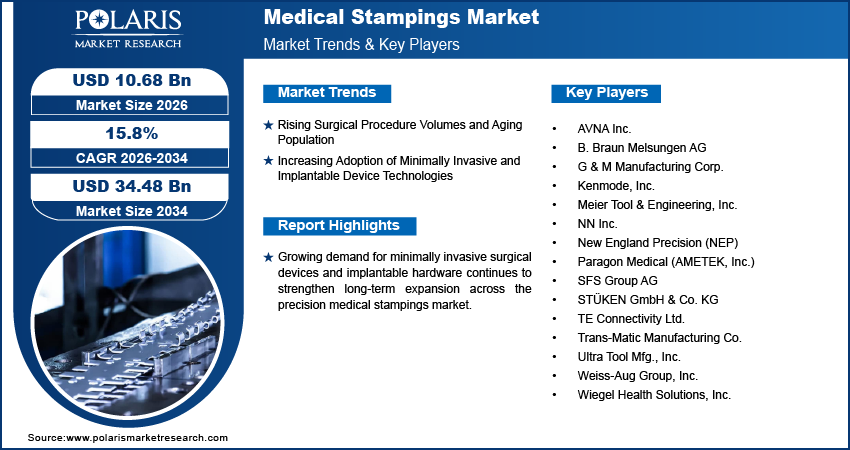

Major players shaping the global medical stamping market include AVNA Inc., B. Braun Melsungen AG, G & M Manufacturing Corp., Kenmode, Inc., Meier Tool & Engineering, Inc., NN Inc., New England Precision (NEP), Paragon Medical (AMETEK, Inc.), SFS Group AG, STÜKEN GmbH & Co. KG, TE Connectivity Ltd., Trans-Matic Manufacturing Co., Ultra Tool Mfg., Inc., Weiss-Aug Group, Inc., Wiegel Health Solutions, Inc.

Key Players

- AVNA Inc.

- B. Braun Melsungen AG

- G & M Manufacturing Corp.

- Kenmode, Inc.

- Meier Tool & Engineering, Inc.

- NN Inc.

- New England Precision (NEP)

- Paragon Medical (AMETEK, Inc.)

- SFS Group AG

- STÜKEN GmbH & Co. KG

- TE Connectivity Ltd.

- Trans-Matic Manufacturing Co.

- Ultra Tool Mfg., Inc.

- Weiss-Aug Group, Inc.

- Wiegel Health Solutions, Inc.

Industry Developments

- July 2025: Weiss-Aug announced a strategic rebranding that consolidated its operations into two industry-focused business units, with Weiss-Aug MedPharma dedicated to serving medical and pharmaceutical sectors including precision medical components and assemblies.

- October 2024: SFS Group expanded its market footprint in the Midwest US by acquiring Pro Fastening Systems Inc., a distributor of fasteners and related components for construction applications. It highlights SFS’s broader precision components capabilities that support its medical stampings and engineered components business in adjacent industrial segments.

- February 2025: Biometrics launched new vertically integrated Metal Injection Molding (MIM) services to provide end-to-end metal component production for medical device manufacturers. The expanded offering enhanced the company’s Medical Stampings portfolio by delivering precision metal parts with improved manufacturing efficiency and tighter quality control.

Medical Stampings Market Segmentation

By Material Outlook (Revenue, USD Billion, 2021-2034)

- Stainless Steel Medical Stampings

- Titanium Medical Stampings

- Aluminum & Specialty Alloys

By Manufacturing Process Outlook (Revenue, USD Billion, 2021-2034)

- Progressive Die Stamping

- Deep Draw Stamping

- Micro Stamping & Automation

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Surgical Instruments

- Implantable & Orthopedic Devices

- Cardiovascular & Diagnostic Equipment

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Medical Stampings Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 9.24 Billion |

| Market Size in 2026 | USD 10.68 Billion |

| Revenue Forecast by 2034 | USD 34.48 Billion |

| CAGR | 15.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Medical Stampings Market FAQ's

The global market size was valued at USD 9.24 billion in 2025 and is projected to grow to USD 34.48 billion by 2034.

North America dominates due to strong OEM concentration, high surgical volumes, and advanced medical device manufacturing ecosystems.

Surgical instrument manufacturers and implantable device producers represent the leading end users, supported by recurring hospital procurement and rising orthopedic and cardiovascular procedure volumes.

A few of the key players in the market are AVNA Inc., B. Braun Melsungen AG, G & M Manufacturing Corp., Kenmode, Inc., Meier Tool & Engineering, Inc., NN Inc., New England Precision (NEP), Paragon Medical (AMETEK, Inc.), SFS Group AG, STÜKEN GmbH & Co. KG, TE Connectivity Ltd., Trans-Matic Manufacturing Co., Ultra Tool Mfg., Inc., Weiss-Aug Group, Inc., and Wiegel Health Solutions, Inc.

Growth is driven by rising chronic disease burden, expansion of minimally invasive surgical procedures, increasing implantable device production, and demand for high-tolerance, biocompatible metal components.

Download Sample Report of Medical Stampings Market

Please fill out the form to request a customized copy of the research report.