Nicotine Pouches Market Size & Share Global Analysis Report, 2026-2034

REPORT DETAILS

REPORT DETAILS

Nicotine Pouches Market Summary

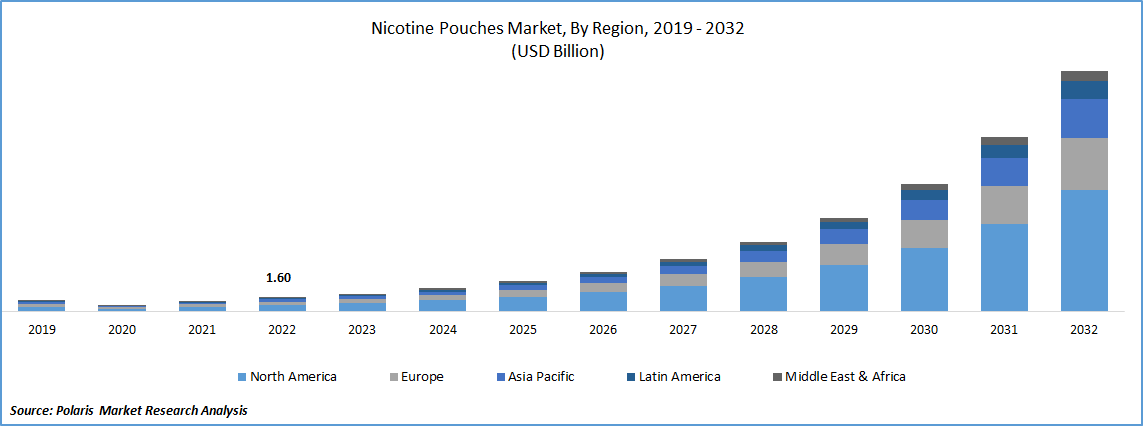

The nicotine pouches market size was valued at USD 3.39 billion in 2025 and is expected to register a CAGR of 25.23% from 2026 to 2034. Nicotine pouches are small, smokeless, tobacco-free products placed between the gum and lip to deliver nicotine. The rising demand for smoke-free alternatives, expansion of e-commerce and retail availability, and the introduction of various flavors and strengths fuel the market growth.

Market Statistics

Key Takeaways

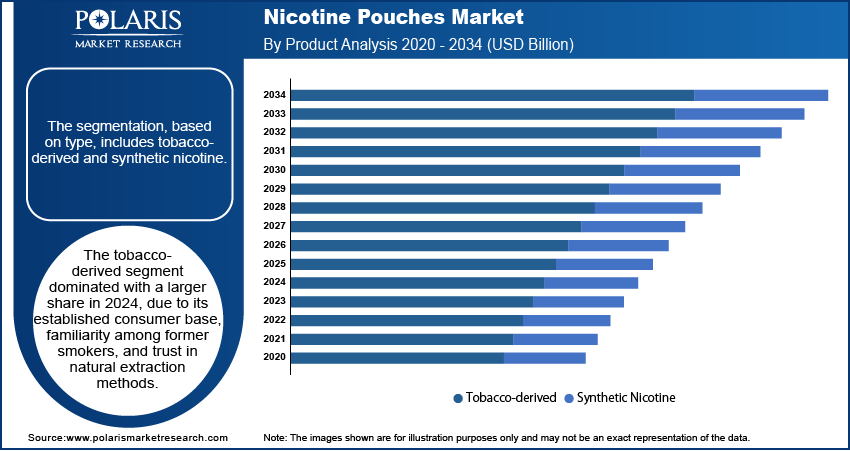

- The tobacco-derived nicotine pouches segment dominated the revenue share in 2025. The segment dominance is attributed to its established consumer base, familiarity among smokers, and familiarity with natural extraction methods.

- The synthetic nicotine pouches market is gaining traction. Nicotine pouch brands emphasize “clean-label” nicotine delivery. Also, regulations are imposed to govern nicotine pouches. Further, there are evolving product authorization requirements in certain markets. These factors boost segment growth.

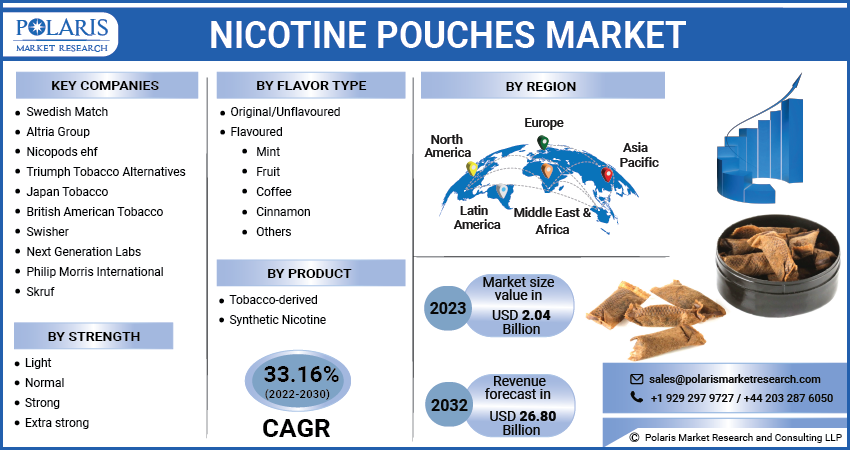

- The original/unflavored segment held the largest market share in 2025, due to its simplicity, minimalism, and appeal to users who are selectively focused on nicotine delivery.

- The strong segment is expected to record the fastest CAGR between 2026 and 2034, as this variant delivers faster and more intense effects, making it ideal for heavy smokers or those with higher tolerance levels.

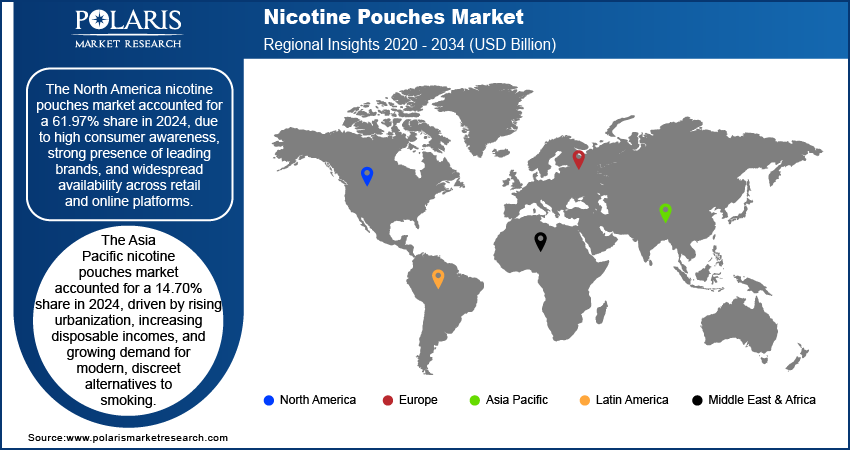

- North America held the largest share of global market in 2025. High consumer awareness and the strong presence of leading brands propel the dominance. In addition, widespread availability across various sales platforms fuels the regional market growth.

- Asia Pacific is expected to hold a significant revenue share in the coming years. It is driven by rising urbanization and increasing disposable incomes. Further, growing awareness of modern, discreet alternatives to smoking boosts the growth.

Market Dynamics

- The availability of attractive flavors such as mint, citrus, berry, and coffee fuels the popularity of nicotine pouches.

- With the rising number of smokers, amid population growth, urbanization, and lifestyle changes, the need for harm-reduction products such as nicotine pouches also increases.

- Awareness campaigns from health organizations and governments to educate people about the harmful effects of smoking and alternatives available are expected to serve as attractive growth opportunities in the future.

- Uncertain regulatory frameworks and restrictions on flavored products, consumer concerns about addiction and long-term health impacts, and limited research outcomes on safety are the prime hindrances in the market.

AI Impact on Nicotine Pouches Market

- AI tools are used to track buying habits, browsing patterns, and social media discussions of people to understand shifts in preferences toward tobacco-free nicotine alternatives. They also enable brands to design targeted campaigns based on demographics, consumption patterns, and lifestyle data.

- Using machine learning makes it easier to examine consumer feedback. It accelerates the development of new products with various flavors, strengths, and pouch designs.

- AI tools help monitor complex and changing regulations related to nicotine products. They ensure correct labeling and responsible marketing campaigns.

- AI is integrated into imaging and testing systems. These systems improve consistency in pouch filling, nicotine content, and packaging standards.

- AI-based evaluation tools can identify patterns of misuse or overconsumption. It helps companies design safer usage guidelines.

To Understand More About this Research: Download Sample Report

What are Nicotine Pouches?

Nicotine pouches are small, smokeless, tobacco-free products placed between the gum and lip to deliver nicotine. These pouches are alternative to smoking or chewing tobacco. They are available in various flavors and strengths.

Consumers demand safer alternatives due to rising awareness regarding the health risks associated with smoking and chewing tobacco. Nicotine pouches offer a smokeless and tobacco-free option. It makes them attractive to users trying to quit or reduce their tobacco consumption. These pouches don't create smoke, ash, or strong odors. Thus, they have become more acceptable in social and public settings. Health organizations and governments run campaigns against tobacco consumption. Thus, most users prefer nicotine pouches, which fuels market growth.

Modern consumers often prefer products that fit easily into their busy lifestyles. Nicotine pouches are discreet and easy to use. Because of this convenience, users can enjoy nicotine in places like offices, public transport, and restaurants where smoking is not allowed. The simple packaging and easy disposal attract users who want a clean and socially acceptable way to use nicotine. This convenience is a major factor in the industry's growth. Online sales of nicotine pouches, which include direct-to-consumer models, subscriptions, and retail growth supported by store locators, also boost this convenience. It supports a stronger nicotine pouches market growth in urban and high-compliance retail environments.

The nicotine pouches industry is benefiting from improved distribution channel penetration, including convenience stores, gas stations, specialty tobacco outlets, and regulated online platforms with age-gating. Brands are using digital merchandising (bundles, trials, subscriptions) to increase repeat purchases, which drives online nicotine pouches market. Offline retail supports impulse discovery and brand switching. The rising e-commerce penetration is strengthening the sales of nicotine pouches of major brands across high-volume geographies.

Industry Dynamics

Availability of Flavors and Strength

Companies operating in the nicotine pouch industry are offering the variety of flavors and strengths available. Unlike traditional tobacco products, these pouches are available in mint, citrus, berry, coffee, and other unique flavors. These variety of flavors attracts new and experienced users. Companies offer different nicotine strengths, letting users choose based on their comfort level. This wide selection makes nicotine pouches more appealing. It mostly attracts younger adults who seek personalized and enjoyable alternatives to smoking. The ability to tailor the experience helps expand the customer base, propelling the demand for nicotine pouches.

Rising Number of Smokers

The number of smokers is increasing due to population growth and hectic lifestyle. According to the Center for Disease Control and Prevention (CDC), 49.2 million people in the U.S. were reported using tobacco products. The need for harm-reduction products such as nicotine pouches increases as smoking rates rise. These pouches offer a cleaner, smoke-free alternative. They appeal to smokers who want to switch to a safer choice. As more people learn about the health risks of smoking, even in developing areas, smokers are looking for safer nicotine options. This increasing number of smokers creates a big chance for nicotine pouch brands to enter new markets and grow their presence, driving their growth.

Segmental Insights

Product Analysis

The segmentation, based on type, includes tobacco-derived and synthetic nicotine. The tobacco-derived segment dominated with a larger share in 2025. It is attributed to its established consumer base and familiarity among former smokers. Also, trust in natural extraction methods boosts the segment growth. Robust distribution networks and consistent product quality boost the demand for tobacco-derived nicotine pouches. The dominance is driven by regulatory clarity in many regions. The association with well-known brands adds to consumer confidence, while their effectiveness in aiding smoking cessation boosts adoption. Additionally, traditional users prefer the natural origin of tobacco-derived nicotine. They see it as a more authentic experience. Long-standing usage patterns and marketing support from legacy tobacco companies drive the segment growth.

The synthetic nicotine segment is expected to grow considerably from 2026 to 2034. This growth is driven by the increasing demand for tobacco-free alternatives, especially among health-conscious and younger consumers. These pouches attract users looking for clean-label, plant-free options with stable nicotine levels. Their increasing popularity is supported by innovation in formulation, flexible branding, and fewer restrictions in some regulatory environments. Synthetic variants are perceived as modern, safer choices that align with wellness trends as awareness grows. Convenient online availability, social media marketing, and flavor variety further improve visibility and adoption, thereby driving the segment growth.

By Flavor Type Analysis

The segmentation includes original/unflavored and flavored. The original/unflavored segment dominated with a larger share in 2025. Its simplicity and minimalism drive the segment growth. Original or unflavored nicotine pouches offer pure experience without flavor distractions. This is especially suitable for users moving away from traditional tobacco. The straightforward formulation is considered cleaner and more purposeful, making it popular with health-conscious users. They avoid rules linked to flavored products. This regulatory ease helps increase access. Additionally, unflavored pouches are often used in professional environments where discreet and odorless use matters.

By Strength Analysis

By strength, market is segmented into light, normal, strong, and extra strong. The strong segment is expected to witness the fastest growth during 2026-2034. Increasing demand from experienced users seeking higher nicotine satisfaction fuels growth. These products offer faster and stronger effects. They are ideal for heavy smokers or people with a higher tolerance. The growth comes from the rising demand for effective smoking alternatives that match the strength of traditional tobacco. Strong options also draw in consumers looking for quick relief from cravings. This makes them more attractive in stressful times. As brands expand their range based on strength, consumers enjoy more personalized choices.

By Distribution Channel Analysis

By distribution channel, the market offline and online. The offline sales segment leads in revenue share. This is due to retail visibility, impulse buying, and strict age verification in regulated stores. However, the online channel is growing quickly. Increasing focus on direct-to-consumer websites and authorized e-commerce accelerates the growth. It is backed by a wider range of products, including strengths, flavors, and trial packs, as well as the ease of repeat ordering. The growth of the online channel is changing the competitive landscape. Brands are investing in digital marketing and local fulfillment capabilities. They are also focusing on customer retention programs.

Regulatory Landscape & Compliance

The regulations for nicotine pouches differ by country. These rules affect product availability, flavor options, marketing strategies, and international online sales. Common regulatory factors include enforcing minimum age and setting limits on advertising and influencer marketing. Other factors involve packaging and labeling requirements, like disclosing nicotine content and providing warnings, along with discussions about flavored nicotine products. For businesses in this market, being ready to comply with regulations has become an important competitive edge. It directly influences their go-to-market strategy and the nicotine pouches market forecast in regions with strict regulations.

Regional Analysis

North America Nicotine Pouches Market Trends

The North America market accounted for a 62.80% share in 2025. High consumer awareness and strong presence of leading brands fuel the dominance. It is also fueled by widespread availability across retail and online retail platforms. Supportive regulatory frameworks and growing acceptance of smokeless tobacco products encourage consumer adoption. The region benefits from a well-developed tobacco industry. The industry rapidly embraces innovation. The region witnesses increasing demand for convenient, discreet, and odorless nicotine delivery. Marketing campaigns, product variety, and rising interest in harm-reduction solutions further drive regional market growth. Moreover, a health-conscious population and advanced distribution channels drive the industry growth in North America. North America industry growth is supported by broad retail reach and high awareness. Brand strategies increasingly incorporate compliance-by-design (labeling, age-gating, marketing restrictions). It is influencing SKU mix between flavored and unflavored nicotine pouches. These strategies are shaping competitive positioning in the U.S. nicotine pouches industry.

U.S. Nicotine Pouches Market Assessment

The U.S. market accounted for 82.40% of regional share in 2025. It is due to strong consumer demand for tobacco-free and smoke-free alternatives. There is a rising availability of flavored and synthetic options catering to younger, tech-savvy users. This factor drives U.S. market expansion. High awareness, innovative branding, and the presence of major industry players support rapid growth. Retail expansion, e-commerce accessibility, and growing interest in wellness-focused products are key drivers. Government efforts to reduce smoking have further encouraged shifts toward modern oral nicotine products, thereby driving the growth.

Asia Pacific Nicotine Pouches Market Overview

The Asia Pacific market accounted for 15.20% share in 2025, driven by rising urbanization, increasing disposable incomes, and growing demand for modern, discreet alternatives to smoking. Younger consumers in countries such as India, South Korea, and Australia are showing interest in innovative nicotine formats. Expanding awareness through digital marketing, health-focused choices, and entering international markets drives growth. The region has a large population. Lifestyle habits of consumers are changing quickly. These factors support this market growth. Technology improvements and modern retail make access easier. It encourages the nicotine pouch adoption across the region. Growth in Asia Pacific may vary by country due to differences in tobacco control policies and how products are accepted. It can impact the nicotine pouches industry in country. This can also shape channel strategies for retail and e-commerce entry.

Japan Nicotine Pouches Market Insights

The Japan market is expected to experience significant growth during the forecast period, due to its openness to smokeless innovations and early adoption of reduced-risk products. Consumers favor discreet and clean options. It makes nicotine pouches a popular choice. The country’s tech-savvy culture, which helps the industry grow. Urban consumers like the convenience and low odor of pouches. Growth is also boosted by people already being familiar with non-combustible nicotine delivery systems. It eases market entry for new products, thereby driving the growth.

Europe Nicotine Pouches Market Overview

The Europe market accounted for 17.43% share in 2025. It is driven by strong demand for smoke-free alternatives. The region benefits from favorable consumer attitudes toward tobacco alternatives, along with widespread acceptance of modern oral products. Scandinavian countries, especially Sweden, have played a major role in popularizing nicotine pouches. Continued innovation, a variety of strengths and flavors, and support from public health initiatives encourage growth. Retail and e-commerce networks are well-developed, improving access across urban and rural areas and thereby driving the regional market growth. Europe is a key hub for modern oral nicotine adoption. Policy sensitivity around flavors and cross-border online sales can influence the nicotine pouches market share across countries. It makes compliance and portfolio flexibility central to long-term growth.

Germany Nicotine Pouches Market Outlook

The Germany market is expected to experience significant growth during the forecast period. The growth is attributed to rising demand for tobacco-free nicotine solutions. Increasing consumer preference for cleaner, odorless options also boosts the expansion. Younger adults and former smokers prefer nicotine pouches due to the convenience and discretion of pouches. Strong brand presence and innovative product offerings accelerate the industry growth. The German market is also driven by greater availability in retail and digital channels. Public interest in wellness and safer options further fuels this growth. Ongoing consumer awareness and product visibility through marketing campaigns help the rapid uptake of these products.

Key Players and Competitive Analysis

The nicotine pouches industry features a competitive landscape. It is driven by innovation, branding, and global growth. Key players have strong distribution networks and established trust with consumers. Strategies include expanding product lines using variety of flavors and strengths. They emphasize using multiple sales channels, like retail and direct-to-consumer e-commerce. Companies focus on branding that meets regulations and on responsible marketing. Regional growth through partnerships and acquisitions is also important. Brands with deeper retail reach and consistent product quality can effectively protect their nicotine pouch market share as regulations tighten and price competition rises.

Nicotine pouch companies such as NIQO Co. (Swedish Match AB) and Skruf Snus AB lead in Scandinavia with diverse product portfolios. Companies such as Black Buffalo Inc. and Nicopods ehf. focus on niche markets and tobacco-free formulations. GN Tobacco, Swisher International, and SnusCentral cater to varied preferences across regions. New entrants and specialized brands, such as Tobacco Concept Factory, drive competition through flavor innovation, strength options, and targeted marketing.

Key Players

- Altria Group, Inc.

- Black Buffalo Inc.

- British American Tobacco

- GN Tobacco Sweden AB

- Japan Tobacco International

- Nicopods ehf.

- NIQO Co. (Swedish Match AB)

- Skruf Snus AB

- SnusCentral

- Swisher International Inc.

- Tobacco Concept Factory

Nicotine Pouches Industry Developments

- April 2025: Emplicure launched KLAR nicotine pouches in the UK. Unlike traditional cellulose-based pouches, KLAR uses a bioceramic-based powder for controlled nicotine and flavor release. The pouches are available in mint and citrus flavors. They have various strength options such as 3mg, 6mg, and 9mg. The product is available in 700 UK retail stores and online via Haypp.com. (Source: klar.com)

- February 2025: Nic Pouches launched its new UK-based online store. The store is offering over 300 high-quality nicotine pouch products. It offers nicotine pouches of brands such as ZYN, Velo, Killa, and Pablo in various flavors and strengths. (Source: globenewswire.com)

Nicotine Pouches Market Segmentation

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Tobacco-Derived

- Synthetic Nicotine

By Flavor Type Outlook (Revenue, USD Billion, 2021–2034)

- Original/Unflavored

- Flavored

- Mint

- Fruit

- Coffee

- Cinnamon

- Others

By Strength Outlook (Revenue, USD Billion, 2021–2034)

- Light

- Normal

- Strong

- Extra strong

By Distribution Channel Outlook (Revenue, USD Billion, 2021–2034)

- Online

- Offline

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Nicotine Pouches Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 3.39 billion |

| Market Size in 2026 | USD 4.43 billion |

| Revenue Forecast in 2034 | USD 26.80 billion |

| CAGR | 25.23% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market was valued at USD 3.39 billion in 2025. It is projected to reach USD 26.80 billion by 2034, at a CAGR of 25.23% during 2026-2034.

Rising health awareness and a strong consumer shift toward smoke-free, tobacco-free alternatives are the primary drivers, alongside product innovation, social media influence, and broader retail availability.

North America dominated with a revenue share of 62.80% in 2025. High health awareness among consumers and a strong retail network drive dominance. The presence of well-known brands like ZYN, Velo, and On! strengthens the leading position.

In January 2025, the FDA approved the marketing of 20 ZYN nicotine pouch products. The products were authorized through its premarket tobacco product application (PMTA) pathway. This marked the first approval for any nicotine pouch product in the U.S.

Establishing localized micro-manufacturing facilities in emerging markets like India, Indonesia, or Brazil can cut costs, improve supply chain reliability, and enable brands to adapt quickly to local preferences.

The strong segment is expected to witness the fastest growth during the forecast period.

Download Sample Report of Nicotine Pouches Market

Please fill out the form to request a customized copy of the research report.