Plasma Fractionation Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

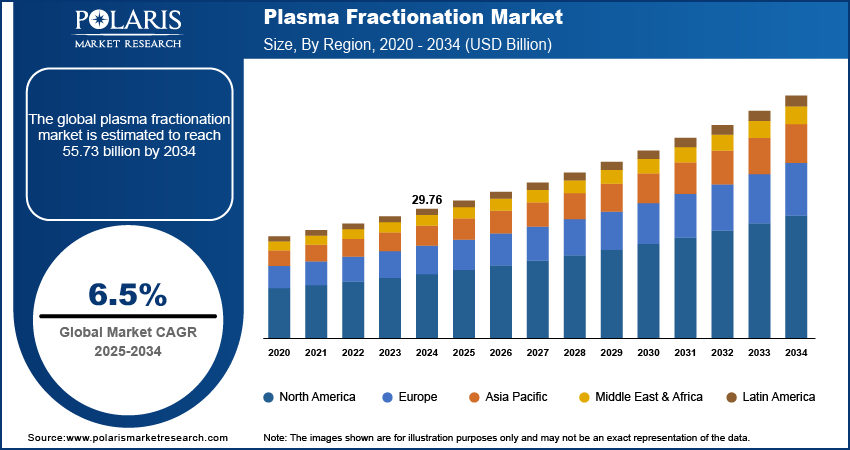

Plasma Fractionation Market Summary

The global plasma fractionation market was valued at USD 31.75 billion in 2025 and is expected to grow at a CAGR of 6.8% from 2026 to 2034. Growth is attributed to the rising geriatric population and increasing prevalence of chronic and infectious diseases. Also, expanding clinical use of plasma-derived products such as immunoglobulins (IVIG), albumin, and coagulation factors propels the growth. Additionally, expanding plasma collection infrastructure and investments in fractionation capacity shape supply availability and competitive positioning across regions.

Market Statistics

Key Takeaways

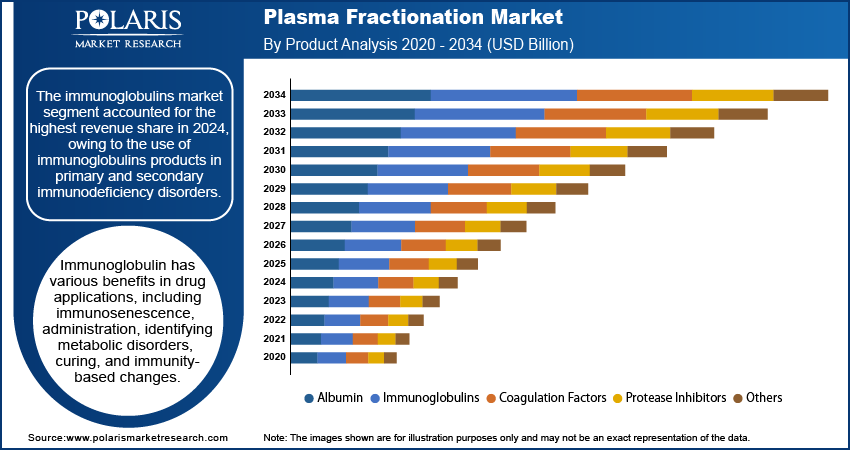

- Immunoglobulins segment accounted for the largest share in 2025. The dominance of the immunoglobulins (IVIG) segment is driven by broader use across immune-mediated and neurological indications. Also, the rising prevalence and diagnosis of primary immunodeficiency boost the adoption of IVIG therapy.

- The oncology segment is projected to grow strongly during the forecast period. supported by rising hospital utilization of plasma-derived therapies and increasing specialty-care demand.

- Centrifugation accounted for a significant share in 2025, supported by increasing demand for efficient plasma separation steps within fractionation workflows. Chromatography purification is also gaining attention for improving selectivity and enabling high-purity plasma protein therapeutics.

- Hospitals and clinics are expected to support market growth, due to increasing admissions and expanding access to plasma-derived therapies in specialty and critical care.

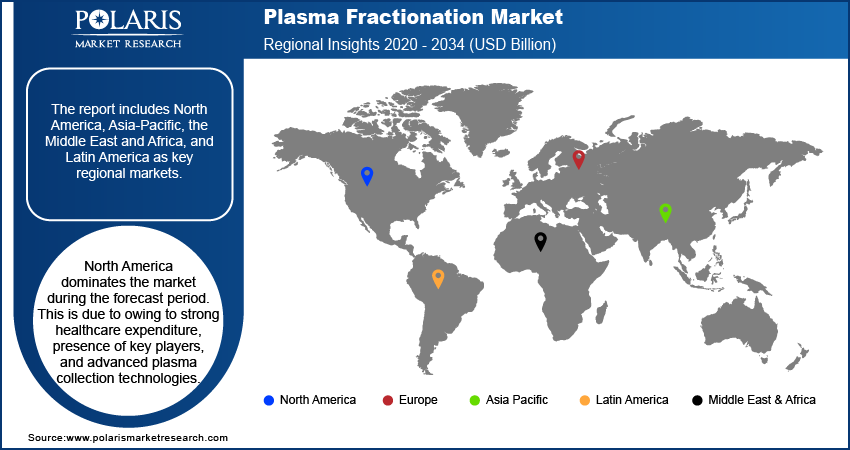

- The North America plasma fractionation market accounted for the largest share in 2025. The dominance is supported by high healthcare expenditure, strong plasma collection networks, and the presence of major industry players.

Industry Dynamics

- The market is rising prevalence of rare and chronic diseases such as hemophilia, primary immunodeficiency disorders, and alpha-1 antitrypsin deficiency.

- The market is fueling due to increasing use of immunoglobulins, albumin, and coagulation factors across hospitals and clinics.

- Advancements in fractionation techniques creates opportunities for manufacturers to expand their global footprint.

- The major challenges for the market is high cost of plasma-derived products, complex regulatory frameworks, and limited plasma collection infrastructure.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Plasma fractionation process is used to separate human plasma into therapeutic proteins, including albumin, immunoglobulins (IVIG), coagulation factors (e.g., Factor VIII/IX), and protease inhibitors. The process involves multiple purification and safety steps to meet stringent quality requirements. Thus, plasma sourcing, process efficiency, and compliance standards strongly influence overall market economics. Many blood collection facilities are available around the globe. With new technological advancements, blood collection is increasing. The rising government initiatives and investments in R&D in the biotechnology and pharmaceutical sectors boost industry growth.

As the R&D in the pharmaceutical & biotechnology sectors is increasing involving plasma treatments, many major players have started working together. The treatment of COVID-19 through plasma fractionation was conducted, and observed that people were fully recovered through this fractionation therapy. It is anticipated that the cost of the fractionation therapy will rise owing to increasing number of blood plasma donors prone to various diseases.

What is Difference Between Plasma Fractionation vs Plasma Therapeutics vs Plasma-Derived Products?

| Aspect | Plasma Fractionation | Plasma-Derived Products | Plasma Therapeutics |

| Definition | The industrial process of separating plasma proteins into individual components. | Specific products obtained from plasma after fractionation. | Therapeutic applications using plasma or plasma components to treat diseases. |

| Purpose | To isolate and purify individual proteins (e.g., albumin, immunoglobulins, clotting factors). | To provide finished biologic products for clinical use. | To treat patients, replacing missing proteins or modulating immune response. |

| Examples | Cold ethanol fractionation, chromatographic fractionation, and membrane filtration. | Immune globulins, albumin, factor VIII/IX, and alpha-1 antitrypsin. | Treatment of immunodeficiency, bleeding disorders, and autoimmune diseases. |

| Key Stakeholders | Fractionation facilities, bioprocess engineers, and contract manufacturers. | Biopharmaceutical companies, regulatory bodies, and distribution networks. | Healthcare providers, hospitals, clinicians, and payers. |

| Regulation Focus | Process controls and Good Manufacturing Practices (GMP). | Safety, purity, potency, and batch release specifications. | Clinical efficacy and safety, dosing guidelines. |

| Output | Purified protein intermediates. | Market-ready therapeutic products. | Clinical outcomes in patients. |

| Value Chain Role | Midstream manufacturing step. | Downstream commercial products. | End-use in healthcare outcomes. |

| Revenue Drivers | Process efficiency, yield, and technology adoption. | Product demand, pricing, and reimbursement. | Clinical guidelines, disease prevalence, and physician adoption. |

| Risk Factors | Contamination risk, yield loss, and technological barriers. | Regulatory hurdles, supply constraints, and safety. | Adverse effects, reimbursement pressures. |

| Primary Users | Manufacturers/bioprocessers. | Hospitals, clinics, pharmacies. | Patients with specific conditions. |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Industry Dynamics

Plasma Fractionation Market Drivers

Growth is supported by collaborations among key players to expand access to plasma-derived products, alongside government and corporate initiatives that strengthen plasma donation awareness and collection programs. Increasing R&D activities in various sectors are the major drivers of the industry’s growth. Many awareness programs are conducted to encourage people for blood donation. Government and corporates are taking initiatives to increase the awareness among people regarding the use of these fractionation therapy-based products.

The increasing prevalence of infectious diseases among the geriatric population across the globe has initiated much R&D in the sector. Cases of m any respiratory infections are increasing due to the changing lifestyle and spreading of disease. New methods are used for treating diseases, and with technological advancement, the industry is expected to flourish. This fractionation therapy is now used for many treatments, and positive success has been noticed. Further, the increasing prevalence of rare and chronic conditions such as hemophilia, primary immunodeficiency disorders, Von Willebrand disease, and alpha-1 antitrypsin deficiency sustains demand for immunoglobulins, albumin, and coagulation factors.

Market Restraint

Plasma supply constraints and high cost of plasma-derived products hinder the market growth. Also, complex regulatory requirements and the need for robust collection and cold-chain infrastructure restrict the industry expansion.

Immunoglobulin Segment Accounted for the Largest Share in 2025

The immunoglobulins market segment accounted for the highest revenue share in 2025, owing to the increasing use in primary and secondary immunodeficiency disorders. Immunoglobulin has various benefits in drug applications, including immunosenescence, administration, identifying metabolic disorders, curing, and immunity-based changes. With the increasing prevalence of infectious diseases, the use of immunoglobulins is expected to expand over the forecast year. The immunoglobulins market growth is also supported by broader diagnosis rates, improved access pathways in hospitals and clinics, and increasing demand for reliable plasma-derived immunoglobulin supply.

Furthermore, it is also expected that the market for coagulation factors will expand with high blood donation or transplantation, approvals of new medicines, and high bleeding disorders. The coagulation factors are majorly used in bleeding disorders like Hemophilia and Von Willebrand disease.

Source: Polaris Market Research Analysis

Oncology Segment are Expected to Spearhead the Market Growth

Based on application, neurology accounted for the highest share, with an increasing prevalence of neurological diseases and treatment of those by fractionation therapy. Additionally, the rising neurovascular illness like strokes and Alzheimer's in older people is leading to the increased use of plasma-based products for treatment.

Additionally, the oncology segment is expected to grow at a faster CAGR during the forecast period with the use of therapies for the treatment of cancer. The targets can be easily treated and cured through this fractionation therapy, which was not curable before.

Centrifugation Segment Shared Highest Revenue in 2025

The centrifugation segment dominated the market with a higher revenue share in 2025 and the fastest growth rate over the forecast period. Getting high-quality blood supernatant requires centrifugation. Centrifugation plasma separation helps researchers separate blood consistently. It improves patient clinical outcomes. Thus, the industry expansion would be aided by the rising need for centrifugation tools. As fractionation workflows scale, manufacturers are expanding the use of advanced purification approaches, such as industrial chromatography and filtration. It improves selectivity, supports high-purity outputs, and strengthens quality assurance for plasma protein therapeutics.

Recently, the use of purification methods and industrial-scale chromatographic fractionation has risen. Coagulation factors, protease inhibitors, and anticoagulants are among the new therapeutic plasma products that have been created. As a result, chromatography purification has enabled the development of novel therapeutics for treating patients with congenital or acquired abnormalities in plasma protein levels. It will therefore spur industry expansion.

Hospitals & Clinics Segment is Supposed to Be Bolstering Growth of the Market

In 2025, the hospitals & clinics segment had the most significant revenue share and is expected to grow during the forecast period. The category is predicted to grow considerably because of the rising off-label use of fractionation market products in hospitals to treat several ailments, improved infrastructure, and healthcare services. Furthermore, there is a high demand for these products due to the complicated illnesses that can be addressed in contemporary clinical settings.

North America Dominated Global Market in 2025

North America dominates the regional market, owing to increasing awareness and numerous advantages of plasma fractionation and rising prevalence of respiratory disorders. The North America plasma fractionation market expansion is aided by the existence of key players, an increase in the quantity of blood collection facilities, and a rise in the consumption of immunoglobulin. Also, the growth is driven by the availability of plasma due to the viability of plasma collections & distribution. Strong plasma collection network and supply chain maturity improve plasma availability and processing throughput. It strengthens regional leadership in plasma-derived therapeutics.

Asia Pacific is expected to expand the plasma fractionation market due to increasing government, private and public investment in R&D, favorable government regulations, an aging population with blood-related disorders, increased immunoglobulin use, and rising target disease prevalence are all contributing factors to the development of therapies.

Source: Polaris Market Research Analysis

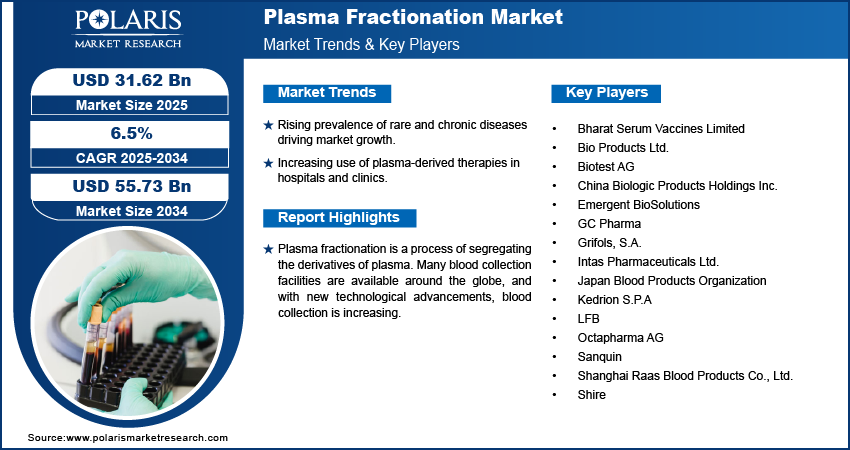

Key Players and Competitive Analysis

The plasma fractionation market is witnessing high competition. Key companies compete on capacity expansion and technological innovations. They also emphasize regulatory compliance to ensure supply reliability and product safety. Plasma fractionators focus on process efficiency and yield. However, manufacturers of plasma-derived products emphasize product quality, differentiation, and market access. Competition arises from regional players in emerging markets versus established global biopharmaceutical firms. Pricing pressures, supply constraints, and stringent regulations boost rivalry. Strategic partnerships, mergers and acquisitions, and investments in new fractionation technologies are critical strategies. Such initiatives help players gain a competitive advantage and meet growing therapeutic demand.

A few of the major players include CSL, Grifols, S.A., Shire, Octapharma AG, Kedrion S.P.A, LFB, Biotest AG, Sanquin, China Biologic Products Holdings Inc., GC Pharma, Bio Products Ltd., Japan Blood Products Organization, Emergent BioSolutions, Shanghai Raas Blood Products Co., Ltd., Intas Pharmaceuticals Ltd., Bharat Serum Vaccines Limited, SK Plasma, Sichuan Yuanda Shuyang Pharmaceutical Co., Ltd., KabaFusion, Centurion Pharma, ADMA Biologics, Inc., PlasmaGen BioSciences Pvt. Ltd., Virchow Biotech Private Limited, Fusion Healthcare, and Hemarus Therapeutics Limited.

List of Key Companies

- ADMA Biologics, Inc.

- Bharat Serum Vaccines Limited

- Bio Products Ltd.

- Biotest AG

- Centurion Pharma

- China Biologic Products Holdings Inc.

- CSL

- Emergent BioSolutions

- Fusion Healthcare

- GC Pharma

- Grifols, S.A.

- Hemarus Therapeutics Limited.

- Intas Pharmaceuticals Ltd.

- Japan Blood Products Organization

- KabaFusion

- Kedrion S.P.A

- LFB

- Octapharma AG

- PlasmaGen BioSciences Pvt. Ltd.

- Sanquin

- Shanghai Raas Blood Products Co., Ltd.

- Shire

- Sichuan Yuanda Shuyang Pharmaceutical Co., Ltd.

- SK Plasma

- Virchow Biotech Private Limited

Plasma Fractionation Industry Developments

- In July 2024, Biotest partnered with Kedrion to distribute FDA-approved Yimmugo, expanding its immunoglobulin product presence in the U.S.

- In January 2024, Takeda received FDA approval for its 10% IVIG therapy to treat adults with chronic inflammatory polyneuropathy.

Plasma Fractionation Market Segmentation

By Product Outlook (Revenue – USD Billion, 2021–2034)

- Albumin

- Immunoglobulins

- Coagulation Factors

- Protease Inhibitors

- Others

By Application Outlook (Revenue – USD Billion, 2021–2034)

- Neurology

- Hematology

- Oncology

- Immunology

- Pulmonology

- Others

By Method Outlook (Revenue – USD Billion, 2021–2034)

- Centrifugation

- Depth Filtration

- Chromatography

- Others

By End-Use Outlook (Revenue – USD Billion, 2021–2034)

- Hospitals & Clinics

- Clinical Research

- Others

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Malaysia

- Rest of Asia Pacific

- Latin America

- Argentina

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- Saudi Arabia

- Israel

- South Africa

- Rest of Middle East & Africa

Plasma Fractionation Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 31.75 billion |

| Market Size in 2026 | USD 33.88 billion |

| Revenue Forecast in 2034 | USD 57.54 billion |

| CAGR | 6.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

plasma fractionation market FAQ's

The global plasma fractionation market was valued at USD 31.75 billion in 2025. It is projected to reach USD 57.54 billion by 2034.

Immunoglobulins lead the market in 2025. The dominance is driven by rising immunodeficiency disorders, autoimmune diseases, and neurological conditions. These conditions require IVIG and SCIG therapeutic interventions across multiple therapeutic applications globally.

Major drivers include increasing aging populations, rising chronic disease prevalence, and expanding plasma collection networks. Also, technological advancements in fractionation methods drive the market growth. It is also fueled by increasing government support for plasma-derived medicinal product manufacturing and self-sufficiency.

North America dominated the global market in 2025. The market expansion is attributed to extensive plasma collection infrastructure and advanced healthcare systems. Additionally, the presence of major industry players and the highest per-capita consumption of immunoglobulins and coagulation factors support expansion.

Key challenges include high production costs and stringent regulatory requirements. Competition from recombinant alternatives and supply chain constraints are other concerns. The market growth is restrained by limited reimbursements and maintaining consistent plasma donor availability for sustainable therapeutic production.

Download Sample Report of plasma fractionation market

Please fill out the form to request a customized copy of the research report.