Portable Ultrasound Devices Market Growth, Industry Trends, Global Report, 2025-2034

REPORT DETAILS

Market Statistics

Market Overview

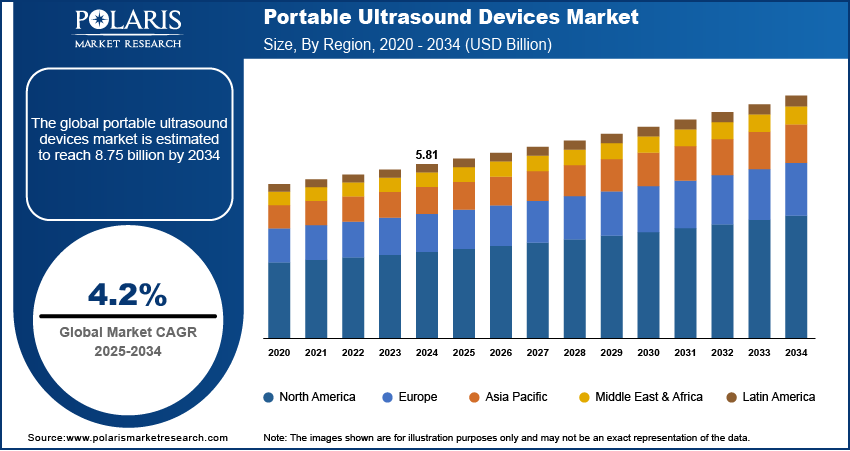

The global portable ultrasound devices market was valued at USD 5.81 billion in 2024 and is projected to grow at a CAGR of 4.2% from 2025 to 2034. The market is largely driven by the increasing demand for point-of-care diagnostics, enabling quick assessments in various settings. Another key factor is ongoing technological advancements, including better imaging and AI integration, which enhance device capabilities.

Key Insights

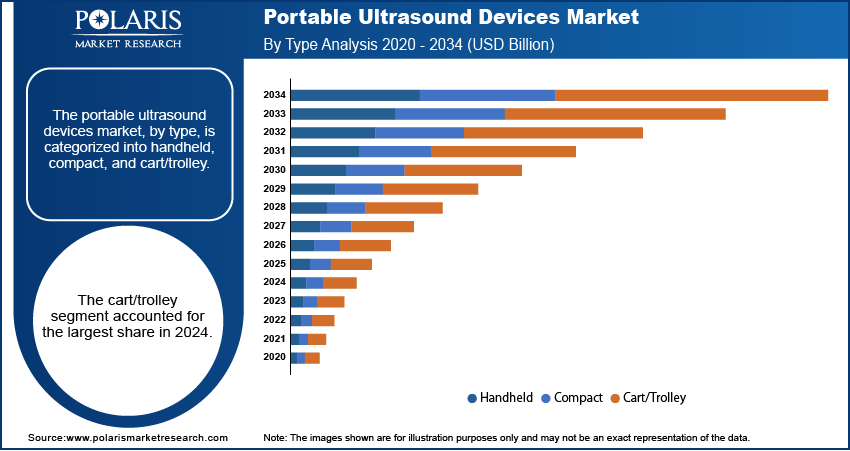

- By type, the cart/trolley-based ultrasound devices segment held the largest share in 2024, due to their robust features, superior imaging quality, and versatility for comprehensive examinations. Their design allows for easy movement within healthcare facilities.

- By technology, the doppler ultrasound technology segment held the largest share in 2024, primarily because of its critical role in assessing blood flow and diagnosing cardiovascular and vascular conditions.

- By application, the obstetrics/gynecology (OB/GYN) segment held the largest share in 2024, driven by the routine and essential nature of ultrasound examinations throughout pregnancy.

- By end use, the hospitals and specialty clinics segment held the largest share in 2024, attributed to their high patient volume, broad range of medical specialties, and established infrastructure.

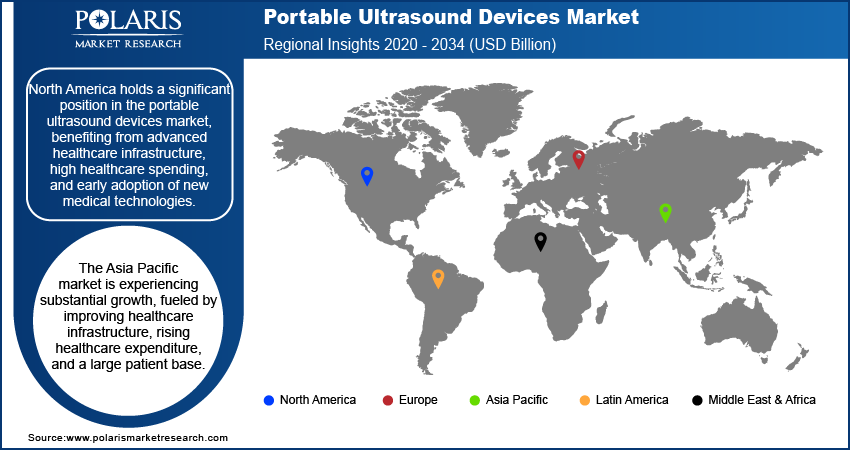

- By region, North America held a significant position in the global portable ultrasound devices industry in 2024, benefiting from advanced healthcare infrastructure, high healthcare spending, and early adoption of new medical technologies.

Industry Dynamics

- The growing adoption of point-of-care testing across various healthcare settings is a significant driver. This allows medical professionals to quickly diagnose and monitor patient conditions at the bedside or in remote locations, improving patient outcomes and reducing the need for traditional, often larger medical imaging equipment.

- Continuous technological advancements are also pushing industry growth. Innovations such as improved image clarity, smaller device sizes, and enhanced software features, including artificial intelligence for better analysis, make these tools more versatile and accurate.

- The increasing global burden of chronic diseases such as heart conditions, liver ailments, and cancer significantly boosts demand. These conditions often require frequent monitoring and early detection, where compact and accessible diagnostic tools play a crucial role.

Market Statistics

- 2024 Market Size: USD 5.81 billion

- 2034 Projected Market Size: USD 8.75 billion

- CAGR (2025–2034): 4.2%

- North America: Largest market in 2024

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Portable ultrasound devices are compact and mobile medical imaging systems that use sound waves to create real-time images of organs and structures inside the body. Unlike larger, traditional ultrasound machines, these devices are designed for easy transport and use in various clinical settings, including patient bedsides, emergency rooms, and remote locations. They offer flexibility and immediate diagnostic capabilities for a wide range of medical applications.

The increasing adoption of telemedicine and remote healthcare services promotes the demand for remote ultrasound devices. As healthcare delivery shifts toward virtual consultations and monitoring, portable ultrasound tools become essential for providing diagnostic capabilities outside of traditional hospital settings. This trend enables healthcare providers to conduct real-time assessments and offer timely care, especially in areas with limited access to specialized medical facilities, thereby enhancing patient convenience and extending care reach.

Another significant driver is the expanding role of remote ultrasound systems in emergency medical services (EMS) and pre-hospital care. The ability to perform rapid assessments for trauma or critical conditions directly at the scene of an accident or during patient transport can greatly improve immediate care. For example, EMS personnel can use portable ultrasound to quickly check for internal bleeding in trauma patients, as supported by various studies, allowing for faster decision-making and potentially life-saving interventions before the patient even reaches the hospital. This real-time imaging capability is crucial for managing critical situations.

Drivers and Trends

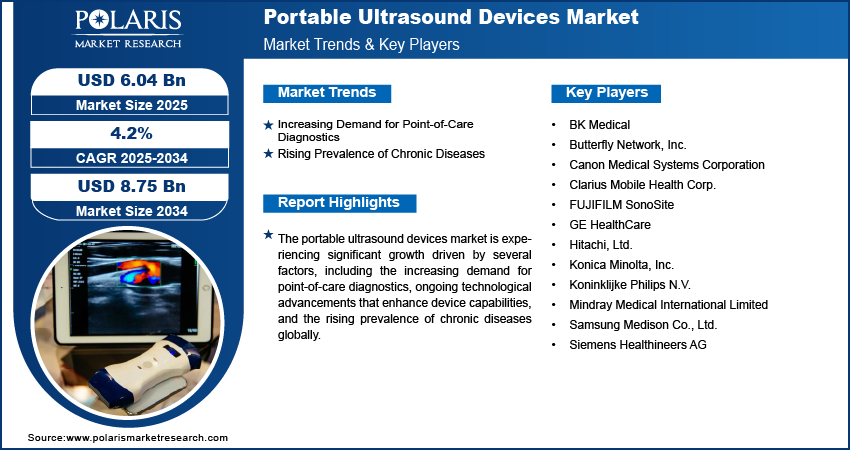

Increasing Demand for Point-of-Care Diagnostics: The growing trend toward point-of-care (POC) diagnostics is a primary factor for shaping the industry growth. Healthcare providers increasingly seek to deliver immediate diagnostic insights at the patient's bedside or in non-traditional settings such as clinics, emergency departments, and remote areas. This shift aims to reduce diagnosis time, improve patient flow, and enable quicker treatment decisions. Portable ultrasound devices, with their compact size and real-time imaging capabilities, are ideally suited for these applications, allowing for rapid and efficient assessments without the need to transport patients to dedicated imaging departments.

The utility of POC ultrasound is evident in its increasing use in emergency settings. Emergency departments in the U.S. report regular use of portable ultrasound devices.. This adoption is driven by the fact that these devices can reduce the time of diagnosis in critical situations. Such efficiency in urgent care scenarios directly contributes to improved patient outcomes. This increasing integration into immediate care settings is a strong driver for the growth.

Rising Prevalence of Chronic Diseases: The escalating global burden of chronic diseases is another major driver. Conditions such as cardiovascular diseases, diabetes, and various cancers require ongoing monitoring and timely diagnosis, including gastric cancer diagnosis, making accessible imaging tools essential. As populations age and lifestyle-related diseases become more common, there is a growing need for non-invasive, convenient diagnostic methods that can be easily deployed in different care environments, from hospitals to outpatient clinics and even home healthcare.

The impact of chronic diseases on demand for these devices is significant. According to the World Health Organization (WHO), cardiovascular diseases are the leading global cause of death, accounting for approximately 17.9 million fatalities annually. This high prevalence necessitates widespread diagnostic tools, including portable ultrasound, for early detection, monitoring disease progression, and guiding treatment. The continuous rise in chronic disease prevalence globally is thus a key factor driving the demand for portable ultrasound devices.

Source: Polaris Market Research Analysis

Segmental Insights

Type Analysis

Based on type, the segmentation includes handheld, compact, and cart/trolley. The cart/trolley segment held the largest share in 2024. This dominance is attributed to their robust features, superior imaging quality, and the ability to connect multiple probes, making them highly versatile for a wide array of medical applications. These systems are commonly found in hospitals and specialized clinics, where they offer a stable platform, larger display screens, and integrated software that supports detailed examinations in areas such as obstetrics, cardiology, and emergency medicine. Their design enables easy movement between different departments and patient rooms, ensuring that high-quality imaging is available wherever it is needed within a healthcare facility. This blend of advanced capabilities and mobility makes them a preferred choice for comprehensive diagnostic procedures.

The handheld ultrasound devices segment is anticipated to register the highest growth rate during the forecast period. This rapid growth is fueled by their extreme portability, ease of use, and increasing affordability, making them ideal for point-of-care diagnostics and remote patient monitoring. The demand for these compact tools has especially surged with the rising emphasis on home healthcare and the expansion of telemedicine services, where immediate and accessible diagnostic capabilities are crucial. These devices allow for quick scans and assessments in various non-traditional settings, including rural clinics, ambulances, and even patients' homes, contributing to a more distributed and efficient healthcare system. Their continuous technological advancements, such as improved image resolution and app-based functionalities, further enhance their utility and adoption across diverse clinical scenarios.

Technology Analysis

Based on technology, the segmentation includes 2D ultrasound, 3D & 4D ultrasound, doppler ultrasound, and high-intensity focused ultrasound. The doppler ultrasound segment held the largest share in 2024. This dominance stems from its critical role in assessing blood flow and diagnosing various cardiovascular and vascular conditions. Doppler ultrasound, which visualizes blood flow, is a noninvasive and highly effective tool for detecting issues such as blockages, narrowing of vessels, and blood clots. Its widespread use in cardiology, obstetrics, and emergency medicine, where real-time blood flow information is vital for diagnosis and treatment planning, firmly establishes its leading position. The integration of color Doppler and pulsed wave Doppler functionalities into portable devices further enhances their diagnostic capabilities, making them indispensable for a broad range of clinical examinations and contributing significantly to the overall segment's revenue.

The 3D and 4D ultrasound technology segment is anticipated to register the highest growth rate during the forecast period. This rapid expansion is driven by the enhanced visualization capabilities these technologies offer, providing detailed, multi-dimensional images that surpass traditional 2D views. In obstetrics, 3D ultrasound and 4D ultrasound imaging allows for a more comprehensive assessment of fetal development and detection of abnormalities, leading to increased demand from expectant parents and healthcare providers. Beyond obstetrics, these advanced modalities are finding increasing applications in areas such as cardiology for complex structural heart assessments and in general imaging for clearer anatomical understanding. The continuous innovation in software and processing power, making these sophisticated imaging capabilities more accessible on portable platforms, further fuels their adoption and rapid growth.

Application Analysis

Based on application, the segmentation includes obstetrics/gynecology, cardiovascular, urology, gastric, musculoskeletal, and others. The obstetrics/gynecology segment held the largest share in 2024, due to the routine and essential nature of ultrasound examinations throughout pregnancy for monitoring fetal development, assessing maternal health, and detecting potential complications. Portable devices offer immense convenience in OB/GYN clinics, rural areas, and for home visits, allowing healthcare providers to perform necessary scans without requiring patients to travel to larger imaging centers. Their noninvasive nature and ability to provide real-time visual information make them indispensable for prenatal care, gynecological diagnostics, and reproductive health assessments. The continuous need for prenatal screening and the increasing global birth rates significantly contribute to this segment's dominant position.

The cardiovascular application segment is anticipated to register the highest growth rate during the forecast period. This rapid expansion is driven by the rising global prevalence of cardiovascular diseases, which necessitates frequent and accessible diagnostic tools for early detection, monitoring, and management. Portable ultrasound systems are becoming increasingly vital for echocardiography, vascular assessments, and guiding interventional procedures at the point of care, from emergency rooms to outpatient clinics and even during patient transport. Their ability to provide immediate insights into heart function and blood flow dynamics is crucial for timely diagnosis and intervention, which can significantly improve patient outcomes. As the focus on preventative care and remote monitoring for heart conditions grows, the demand for portable ultrasound in cardiovascular applications is expected to see substantial further increase.

Source: Polaris Market Research Analysis

End Use Analysis

Based on end use, the segmentation includes hospitals & specialty clinics, ambulatory surgical centers, and others. The hospitals & specialty clinics segment held the largest share in 2024. This substantial share is primarily attributed to the high patient volume, broad range of medical specialties, and the established infrastructure within these settings. Portable ultrasound devices are extensively used in various departments, including emergency rooms, intensive care units, cardiology, obstetrics, and general surgery, for rapid diagnostics, guiding procedures, and patient monitoring. The ability to bring diagnostic imaging directly to the patient's bedside within a hospital environment enhances efficiency, reduces patient transport, and improves clinical workflows, making these facilities major consumers of portable ultrasound technology for diverse clinical needs.

The home care and telehealth settings segment is anticipated to register the highest growth rate during the forecast period. This rapid expansion is driven by the global shift toward decentralized healthcare, where services are increasingly delivered outside traditional clinical environments. As remote patient monitoring and virtual consultations become more prevalent, portable ultrasound devices enable healthcare professionals to conduct essential diagnostic scans in a patient's home, reducing hospital visits and improving access to care, especially for those with limited mobility or in remote areas. The convenience and real-time diagnostic capabilities offered by these devices are crucial for managing chronic conditions, post-operative care, and providing general health assessments in a patient-centric model, thus fueling significant demand and growth in this evolving end-use area.

Regional Analysis

The North America portable ultrasound devices market accounted for the largest share in 2024, primarily driven by advanced healthcare infrastructure, high healthcare spending, and the early adoption of new medical technologies. The region benefits from a strong focus on point-of-care diagnostics, which aligns well with the capabilities of portable ultrasound. The increasing prevalence of chronic diseases and an aging population also contribute to the consistent demand for accessible and efficient diagnostic tools. Additionally, supportive regulatory frameworks and favorable reimbursement policies for ultrasound procedures further encourage growth and product innovation across the region.

U.S. Portable Ultrasound Devices Market Insights

The U.S. is a key contributor In North America. The country's advanced healthcare system, coupled with substantial investments in medical technology research and development, underpins its strong presence. The rising demand for quick and precise diagnostic imaging in emergency settings, critical care, and primary care clinics drives the adoption of portable ultrasound devices. The ongoing shift toward value-based care and outpatient services also promotes the adoption of portable ultrasound systems, as they help reduce costs and improve patient access to diagnostic services outside of traditional hospital environments.

Europe Portable Ultrasound Devices Market Trends

Europe represents a substantial segment in the global industry, characterized by well-established healthcare systems and a high incidence of chronic illnesses among its aging population. The region shows a strong trend toward integrating point-of-care diagnostics into various clinical practices, which favors the use of portable ultrasound. Furthermore, government initiatives aimed at enhancing healthcare accessibility and improving diagnostic capabilities, especially in remote areas or during emergency situations, play a crucial role in driving the demand for these versatile devices across European countries.

The Germany portable ultrasound devices market is a prominent country in Europe. Its robust healthcare system, high technological adoption rate, and strong emphasis on preventative medicine contribute to a steady demand for advanced diagnostic tools. There is a notable focus on integrating artificial intelligence into medical imaging, which is enhancing the functionality and appeal of portable ultrasound devices. The rising burden of chronic diseases and a significant elderly population also necessitate efficient and accessible diagnostic methods, ensuring consistent growth in the use of portable ultrasound systems for various medical applications across the country.

Asia Pacific Portable Ultrasound Devices Market Overview

The Asia Pacific market is experiencing substantial growth, driven by improvements in healthcare infrastructure, increasing healthcare expenditure, and a large patient base. Countries in the region are increasingly focusing on expanding access to healthcare services, particularly in rural and underserved areas, where portable ultrasound offers a cost-effective and efficient diagnostic solution. The growing awareness about early disease detection and the increasing prevalence of various health conditions also contribute to the escalating demand for these flexible diagnostic tools across the diverse economies of Asia Pacific.

China Portable Ultrasound Devices Market Outlook

China is a major country experiencing the rising adoption of portable ultrasound devices in Asia Pacific. The country's vast population, coupled with rapid advancements in its healthcare sector and significant investments in medical technology, creates a robust demand for these devices. There is a strong push toward digital healthcare and telemedicine, which highly favors the adoption of portable and handheld ultrasound systems for remote diagnostics and monitoring. Additionally, the increasing prevalence of chronic diseases and an aging demographic further underscore the need for accessible and efficient imaging solutions, propelling the growth forward in China.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

The competitive landscape of the portable ultrasound devices market is characterized by the presence of both large, established medical technology companies and a growing number of specialized firms. These companies compete on various fronts, including product innovation, image quality, device portability, software integration, and pricing strategies. There's a strong emphasis on developing user-friendly interfaces and enhancing connectivity features to enable seamless data transfer and remote consultation. The sector also sees competition in specific application areas, with some companies excelling in cardiovascular or OB/GYN solutions, while others focus on point-of-care or emergency medicine.

A few key players in the industry include Koninklijke Philips N.V.; GE HealthCare; FUJIFILM SonoSite; Siemens Healthineers AG; Canon Medical Systems Corporation; Samsung Electronics Co., Ltd.; Mindray Medical International Limited; Hitachi, Ltd.; Konica Minolta, Inc.; Butterfly Network, Inc.; Clarius Mobile Health Corp.; and BK Medical.

Key Players

- BK Medical

- Butterfly Network, Inc.

- Canon Medical Systems Corporation

- Clarius Mobile Health Corp.

- FUJIFILM SonoSite

- GE HealthCare

- Hitachi, Ltd.

- Konica Minolta, Inc.

- Koninklijke Philips N.V.

- Mindray Medical International Limited

- Samsung Medison Co., Ltd.

- Siemens Healthineers AG

Industry Developments

March 2025: Philips unveiled AI-powered enhancements for its Compact Ultrasound 5500CV system. These updates expand cardiac imaging capabilities with advanced transducer compatibility and AI-driven efficiency, aiming to streamline workflows and improve diagnostic confidence in portable cardiac ultrasound.

September 2023: Mindray launched its TE Air Wireless Handheld Ultrasound. This device offers multi-device connectivity, allowing it to connect to a mobile device or a full ultrasound system, enhancing accessibility and utility in various clinical scenarios, particularly for point-of-care applications.

Market Segmentation

By Type Outlook (Revenue – USD Billion, 2020–2034)

- Handheld

- Compact

- Cart/Trolley

By Technology Outlook (Revenue – USD Billion, 2020–2034)

- 2D Ultrasound

- 3D & 4D Ultrasound

- Doppler Ultrasound

- High-intensity Focused Ultrasound

By Application Outlook (Revenue – USD Billion, 2020–2034)

- Obstetrics/Gynecology

- Cardiovascular

- Urology

- Gastric

- Musculoskeletal

- Others

By End Use Outlook (Revenue – USD Billion, 2020–2034)

- Hospitals & Specialty Clinics

- Ambulatory Surgical Centers

- Others

By Regional Outlook (Revenue – USD Billion, 2020–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- Suth Korea

- Indnesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- Suth Africa

- Rest of Middle East & Africa

- Latin America

- Mexic

- Brazil

- Argentina

- Rest of Latin America

Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 5.81 billion |

| Market Size in 2025 | USD 6.04 billion |

| Revenue Forecast by 2034 | USD 8.75 billion |

| CAGR | 4.2% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Insights |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Portable Ultrasound Devices Market FAQ's

The global market size was valued at USD 5.81 billion in 2024 and is projected to grow to USD 8.75 billion by 2034.

The global market is projected to register a CAGR of 4.2% during the forecast period.

North America dominated the market share in 2024.

A few key players include Koninklijke Philips N.V.; GE HealthCare; FUJIFILM SonoSite; Siemens Healthineers AG; Canon Medical Systems Corporation; Samsung Electronics Co., Ltd.; Mindray Medical International Limited; Hitachi, Ltd.; Konica Minolta, Inc.; Butterfly Network, Inc.; Clarius Mobile Health Corp.; and BK Medical.

The cart/trolley segment accounted for the largest share in 2024.

The 3D and 4D ultrasound segment is expected to witness the fastest growth during the forecast period.

Download Sample Report of Portable Ultrasound Devices Market

Please fill out the form to request a customized copy of the research report.