Pressure Transmitter Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Pressure Transmitter Market Overview and Key Insights

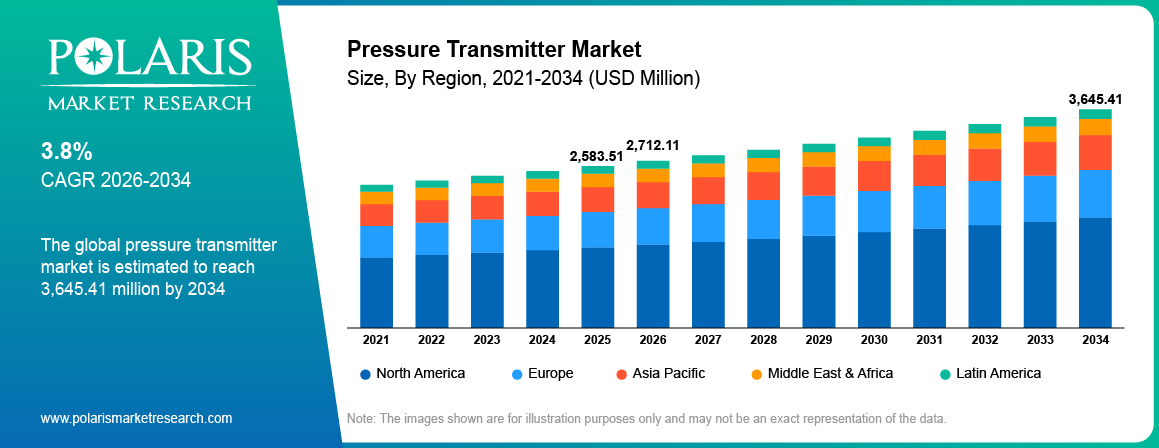

The pressure transmitter market size was valued at USD 2,583.51 million in 2025 and is projected to exhibit a CAGR of 3.8% during 2026–2034. The pressure transmitter market is driving due to rising demand for industrial automation and process instrumentation, growth in oil & gas and chemical sectors, the need for accurate pressure monitoring, and stringent safety and compliance standards.

Market Statistics

Pressure Transmitter Market Key Takeaways

- North America held the largest share of 35.3% in 2025. Well-established industrial base and the presence of key players fuel North America's dominance.

- The Asia Pacific pressure transmitter market is projected to report the highest CAGR of 5.1% during the forecast period. Rising investments in manufacturing and rapid infrastructure development fuel the growth.

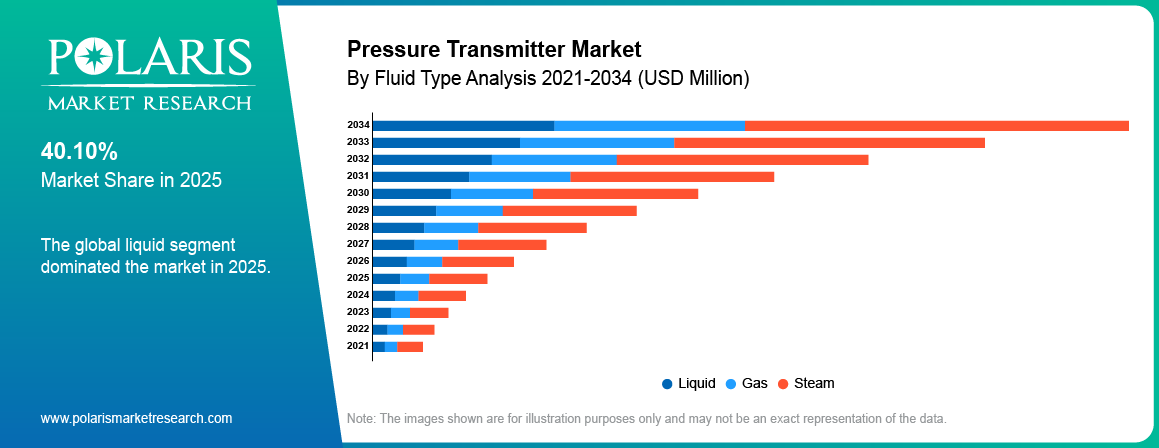

- The liquid segment dominated with 40.10% revenue share in 2025. The growth is driven by the extensive use of pressure transmitters in various industries for measuring and controlling the pressure of liquids in different applications.

- The pressure measurement application segment led the market with 43.04% share in 2025. This is due to the fundamental role of pressure transmitters in a wide spectrum of industrial processes.

- The gauge pressure transmitter segment held the largest share of 32.60% in 2025. The extensive utilization of gauge pressure transmitters across various industrial applications drives the segment growth.

- The gas & oil segment accounted for the largest share of 25.34% in 2025. It is driven by the increasing use of pressure transmitters in various upstream, midstream, and downstream operations within the oil & gas industry.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Pressure Transmitter Market Dynamics

- Rising industrial automation and smart factory adoption propel the demand for accurate pressure monitoring systems. It drives the pressure transmitters industry growth.

- Expanding oil & gas, chemical, water treatment, and power industries fuel the deployment of pressure transmitters.

- High costs of installation, calibration, and maintenance restrict adoption among small-scale industries.

- Increasing adoption of IIoT and wireless monitoring solutions would create lucrative market opportunities during the forecast period.

- Increasing use of digital and multivariable pressure transmitters improves industrial process efficiency, fueling the market expansion.

AI, IIoT and Predictive Diagnostics in Pressure Transmitters

- Artificial intelligence (AI) facilitates predictive maintenance and real-time diagnostics in pressure transmitter systems.

- Smart AI-enabled transmitters improve pressure measurement accuracy and operational efficiency.

- Integration of AI technology supports remote monitoring and cloud-based industrial automation platforms.

- Machine learning (ML) algorithms are used to detect equipment failures and process abnormalities early.

- AI-based analytics reduce downtime, maintenance costs, and energy consumption in industries

What Is a Pressure Transmitter and How Does It Work?

Pressure transmitters are industrial sensing devices designed to measure the pressure of gases, liquids, steam, and other fluids and convert the readings into electrical signals for monitoring and control systems. They are widely used in oil & gas, chemicals, water treatment, manufacturing, power generation, pharmaceuticals, and industrial automation applications to ensure operational efficiency, safety, and process accuracy.

Pressure Transmitters vs. Pressure Sensors: Key Differences

| Parameter | Pressure Transmitters | Pressure Sensors |

| Signal Transmission Capability | Convert pressure readings into standardized electrical output signals for control systems | Primarily detect pressure changes and generate raw sensing data |

| Industrial Process Integration | Widely integrated with PLCs, SCADA, and distributed control systems | Mainly used for localized measurement and device-level sensing |

| Automation Compatibility | Highly suitable for industrial automation and continuous process monitoring | Commonly used in standalone or embedded electronic applications |

| Monitoring Accuracy | Provide stable, calibrated, and high-accuracy measurements for industrial operations | Accuracy may vary depending on sensor type and application environment |

| Real-Time Communication | Support analog and digital communication protocols for real-time data transmission | Limited communication functionality without additional transmitters or controllers |

| End-Use Industry | Extensively used in oil & gas, chemicals, power generation, water treatment, pharmaceuticals, and manufacturing industries | Widely used in automotive, consumer electronics, medical devices, HVAC, and industrial equipment applications |

Source: Polaris Market Research Analysis

The pressure transmitter market revolves around devices designed to measure pressure, typically of gases or liquids, and convert it into an electrical signal. This signal is then used for monitoring, control, or data analysis in various industrial applications. Pressure transmitters are essential components in numerous sectors, including oil and gas, chemical processing, water treatment chemicals, power generation, and even healthcare. They ensure operational efficiency and safety by providing accurate and reliable pressure measurements. The market is driven by the increasing demand for automation and process control across industries, as these systems rely heavily on accurate pressure measurements for optimal operation.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Industries are increasingly using advanced technologies to streamline processes, reduce waste, and improve productivity. The expansion of the renewable energy sector, particularly wind and solar power including solar panels, also significantly shapes the demand for pressure transmitters, which are crucial for efficient energy management and system performance. Furthermore, the increasing use of pressure transmitters in consumer electronics and the healthcare sector contributes to the growth.

Industry Dynamics

Increasing Adoption of Industrial Automation

The escalating adoption of industrial automation across various sectors serves as a significant driver for pressure transmitters. Industries are progressively integrating automated systems to enhance operational efficiency, improve product quality, and reduce labor costs. Pressure transmitters are fundamental components in these automated processes, providing crucial real-time pressure data for monitoring and control loops. For instance, a study published on NCBI in 2023 highlighted the growing integration of automation in the pharmaceutical industry to ensure precise control over manufacturing processes, where pressure monitoring is critical for maintaining product integrity. This increasing reliance on automated systems across diverse industries directly fuels the demand trends for pressure transmitters, as these devices are indispensable for the seamless and efficient operation of automated machinery and processes, thereby driving the growth.

Expansion of the Renewable Energy Sector

The significant expansion of the renewable energy sector, particularly wind and solar power, is a vital driver for pressure transmitters. These technologies require sophisticated monitoring and control systems to optimize energy generation and ensure operational safety. Pressure transmitters play a crucial role in applications such as hydraulic systems in wind turbines and coolant pressure monitoring in solar power plants. According to data from the Department of Energy in 2024, the United States witnessed a substantial increase in renewable energy capacity, necessitating advanced monitoring and control infrastructure. As the global focus on sustainable energy sources intensifies and investments in renewable energy projects continue to rise, the demand for reliable pressure transmitters in these applications will also witness significant growth, contributing substantially to the overall development.

Growing Applications in Healthcare

The healthcare sector presents a growing potential for pressure transmitters, driven by the increasing need for precise pressure monitoring in various medical devices and applications. These devices are used in infusion pumps to control fluid delivery, in respiratory equipment for monitoring air pressure, and in blood pressure monitoring systems, among others. A research article published on PubMed in 2022 discussed the critical role of accurate pressure sensors in medical devices to ensure patient safety and treatment efficacy. The rising demand for advanced medical devices, coupled with the increasing emphasis on patient monitoring and diagnostics, is expanding the applications of pressure transmitters in the healthcare industry. This growing utilization in the medical field is a notable growth factor.

Source: Polaris Market Research Analysis

Pressure Transmitter Market Segment Analysis

Pressure Transmitter Market, by Fluid Type

The liquid segment holds the largest share 40.10% in 2025. This dominance is primarily attributed to the extensive use of pressure transmitters in various industries for measuring and controlling the pressure of liquids in a wide range of applications. These include monitoring liquid levels in storage tanks, controlling flow rates in pipelines carrying liquid substances, and ensuring optimal pressure in hydraulic systems across diverse sectors such as chemical processing, water treatment, and food and beverage. The broad applicability of pressure transmitters in managing liquid-based processes contributes significantly to the substantial share of this segment.

The gas segment is anticipated to exhibit the highest growth rate over anticipated years. This growth is driven by the increasing demand for accurate and reliable pressure measurement in various gas-related applications across industries like oil and gas, power generation, and chemical manufacturing. The expanding use of natural gas as a cleaner energy source, the growing focus on industrial gas processing and transportation, and the rising adoption of advanced monitoring systems for gas-based processes are fueling the demand for pressure transmitters designed for gaseous media. This increasing utilization in diverse gas-handling industries positions the gas segment for the highest growth.

Pressure Transmitter Market, by Measurement Application

The pressure measurement application accounts for the largest share of 43.04% in 2025. This significant share is primarily due to the fundamental role of pressure transmitters in a wide spectrum of industrial processes. Accurate pressure monitoring is essential for ensuring the safe and efficient operation of equipment across diverse sectors, including chemical processing, oil and gas, power generation, and many others. The ubiquitous need for pressure measurement in various stages of production and control solidifies its leading position.

The level measurement application segment is projected to experience the highest growth rate. This increasing growth is driven by the rising demand for precise liquid level monitoring and control in industries such as water and wastewater treatment equipment, food and beverage, and pharmaceuticals. Accurate level measurement is critical for inventory management, process optimization, and regulatory compliance in these sectors. The growing adoption of advanced automation technologies and the increasing focus on efficient resource management are fueling the demand for pressure transmitters used in level measurement applications, positioning this segment for the highest growth.

Pressure Transmitter Market, by Type

The gauge pressure transmitter segment holds the largest share of 32.60% in 2025. This dominance is from the extensive utilization of gauge pressure transmitters across a broad range of industrial applications. Their ability to measure pressure relative to the ambient atmospheric pressure makes them a versatile choice for numerous processes, including tank level monitoring, general pressure indication, and control systems within industries like refining, chemical manufacturing, and utilities. The widespread applicability and cost-effectiveness of gauge pressure transmitters contribute significantly to their leading position.

The differential pressure transmitter segment is anticipated to register the highest growth rate. This accelerated growth is fueled by the increasing need for precise flow and level measurements in complex industrial environments. Differential pressure transmitters are essential for determining flow rates in pipelines, measuring liquid levels in closed tanks, and monitoring pressure drops across filters and other equipment, which are critical for process optimization and efficiency in sectors such as oil and gas, pharmaceuticals, and wastewater treatment. The growing emphasis on advanced process automation and stringent accuracy requirements are driving the heightened demand for differential pressure transmitters, positioning this segment for the most significant growth.

Pressure Transmitter Market, by End-use Industry

The gas & oil end-use segment accounts for the largest share of 25.34% in 2025. This significant share is primarily driven by the extensive use of pressure transmitters in various upstream, midstream, and downstream operations within the oil and gas industry. Pressure transmitters are critical for monitoring and controlling pressure in pipelines, storage tanks, refineries, and offshore platforms, ensuring operational safety and efficiency in this large and well-established sector, thus contributing to its dominant position.

The pharmaceuticals end-use segment is anticipated to exhibit the highest growth rate over anticipated period. This rapid growth is fueled by the increasing stringency of regulations, the growing demand for high-quality pharmaceutical products, and the rising adoption of advanced automation in pharmaceutical manufacturing processes. Pressure transmitters play a vital role in ensuring precise pressure control in reactors, clean rooms, and various other critical applications within the pharmaceutical industry. The increasing investments in research and development and the expansion of the pharmaceutical sector globally are expected to drive significant demand for pressure transmitters, positioning this end-use segment for the highest growth.

Source: Polaris Market Research Analysis

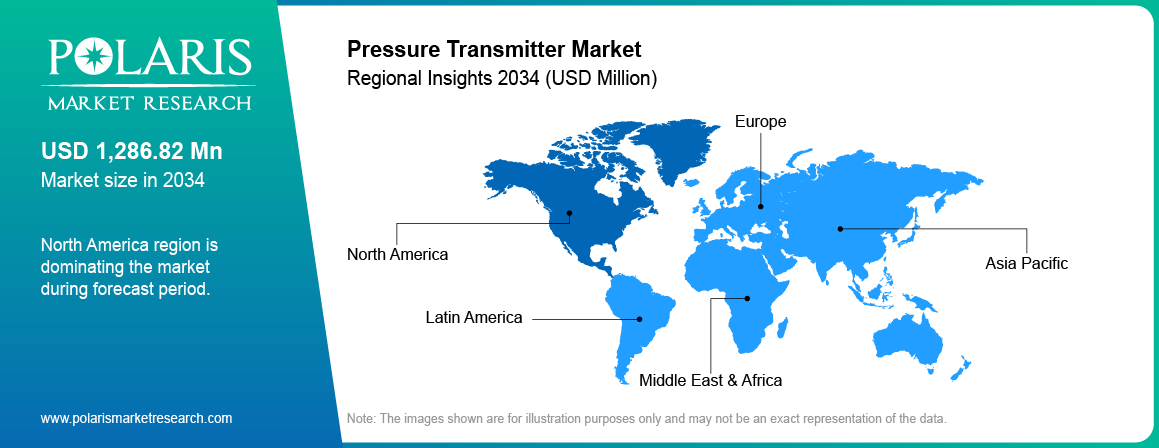

Pressure Transmitter Market Regional Analysis

North America pressure transmitter market holds the largest share of 35.3% in 2025. This can be attributed to the region's well-established industrial base, particularly in sectors such as oil and gas, chemicals, and power generation, all of which are significant consumers of pressure transmitters. Furthermore, the high adoption rate of advanced automation technologies and stringent regulatory standards in North America contribute to the substantial demand and the leading position of this region. The presence of key players and continuous technological advancements further solidify North America's dominance.

The Asia Pacific pressure transmitter market is projected to experience the highest growth rate of CAGR 5.1%. This rapid expansion is driven by the robust industrial growth across countries like China, India, and Southeast Asian nations. Increasing investments in manufacturing, infrastructure development, and the expansion of key end-use industries such as chemicals, oil and gas, water treatment, and power generation are fueling the demand trends for pressure transmitters in this region. Moreover, the rising adoption of automation technologies and favorable government initiatives promoting industrial development are significant growth factors contributing to the Asia Pacific region's position as the fastest-growing for pressure transmitters.

Source: Polaris Market Research Analysis

Pressure Transmitter Market Competitive Landscape

Some of the major players in the pressure transmitter market include Emerson Electric Co., ABB Ltd, Endress+Hauser Group Services AG, Yokogawa Electric Corporation, Honeywell International Inc., Siemens AG, Schneider Electric, VEGA Grieshaber KG, WIKA Alexander Wiegand SE & Co. KG, and Dwyer Instruments Inc.

The competitive landscape is characterized by a mix of well-established global corporations and smaller, specialized manufacturers. These players compete on factors such as product innovation, accuracy, reliability, range of offerings, application-specific solutions, and geographical presence. The market witnesses continuous technological advancements, including the integration of digital communication protocols, wireless capabilities, and smart features for enhanced diagnostics and predictive maintenance. Strategic collaborations, partnerships, and product development focused on meeting the evolving needs of various end-use industries shape the competitive dynamics.

List of Key Companies

- ABB Ltd

- Dwyer Instruments Inc.

- Emerson Electric Co.

- Endress+Hauser Group Services AG

- Honeywell International Inc.

- Schneider Electric

- Siemens AG

- VEGA Grieshaber KG

- WIKA Alexander Wiegand SE & Co. KG

- Yokogawa Electric Corporation

Pressure Transmitter Market Recent Developments

- February 2026: Yokogawa Electric Corporation announced the launch of the OpreX™ Pressure Transmitter EJX S Series. The company claims that EJX S Series offers enhancements in accuracy, long-term stability, and durability. It will ensure stable plant operations and improve maintenance efficiency. (Source: yokogawa.com).

Pressure Transmitter Market Segmentation and Forecast

By Fluid Type Outlook (Revenue – USD Million, 2021–2034)

- Liquid

- Gas

- Steam

By Measurement Application Outlook (Revenue – USD Million, 2021–2034)

- Level

- Pressure

- Flow

By Type Outlook (Revenue – USD Million, 2021–2034)

- Differential Pressure

- Absolute

- Gauge

- Multivariable

By End-Use Outlook (Revenue – USD Million, 2021–2034)

- Gas & Oil

- Chemical

- Treatment of Water & Wastewater

- Power

- Pharmaceuticals

- Paper & Pulp

- Mining & Metals

- Food & Beverage

- Others

By Regional Outlook (Revenue – USD Million, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Malaysia

- Suth Korea

- Indnesia

- Australia

- Vietnam

- Rest of Asia-Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- Suth Africa

- Rest of Middle East & Africa

- Latin America

- Mexic

- Brazil

- Argentina

- Rest of Latin America

Pressure Transmitter Market Report Scope and Methodology

| Report Attributes | Details |

| Market Size Value in 2025 | USD 2,583.51 million |

| Market Size Value in 2026 | USD 2,712.11 million |

| Revenue Forecast by 2034 | USD 3,645.41 million |

| CAGR | 3.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Insights |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Pressure Transmitter Market Frequently Asked Questions

The global market size was valued at USD 2,583.51 million in 2025 and is projected to grow to USD 3,645.41 million by 2034.

The market is projected to register a CAGR of 3.8% during the forecast period, 2026-2034.

North America had the largest share of 35.3% in 2025.

Some of the major players include Emerson Electric Co., ABB Ltd, Endress+Hauser Group Services AG, Yokogawa Electric Corporation, Honeywell International Inc., Siemens AG, Schneider Electric, VEGA Grieshaber KG, WIKA Alexander Wiegand SE & Co. KG, and Dwyer Instruments Inc.

The liquid segment accounted for the larger share of 40.10% in 2025.

Following are some of the trends: ? Increasing Adoption of Industrial Automation: The continuous drive to optimize resources, enhance efficiency, and improve product quality across various industries is increasing the demand for pressure transmitters as integral components of automated systems. ? Integration of Smart Technologies: The incorporation of digital communication protocols, wireless capabilities (like Wi-Fi and Bluetooth), and IoT features in pressure transmitters enables real-time data monitoring, remote diagnostics, and predictive maintenance, leading to improved operational efficiency and reduced downtime. ? Rising Demand for Multivariable Transmitters: These transmitters, capable of measuring multiple parameters like pressure, temperature, and flow simultaneously, are gaining traction due to their ability to reduce the number of devices required and lower the total cost of ownership.

A pressure transmitter is a device that measures the pressure of a fluid (liquid or gas) and converts this measurement into an electrical signal. This electrical signal, typically an analog current signal (like 4-20 mA) or a digital signal, can then be transmitted to a control system, display, or data acquisition system for monitoring and control purposes. Essentially, it acts as a translator, taking a physical pressure value and making it understandable for electronic systems.

Download Sample Report of Pressure Transmitter Market

Please fill out the form to request a customized copy of the research report.