Radiopharmaceuticals Third-Party Logistics Market Research Report - Forecast to 2034

REPORT DETAILS

Radiopharmaceuticals Third-Party Logistics Market Summary

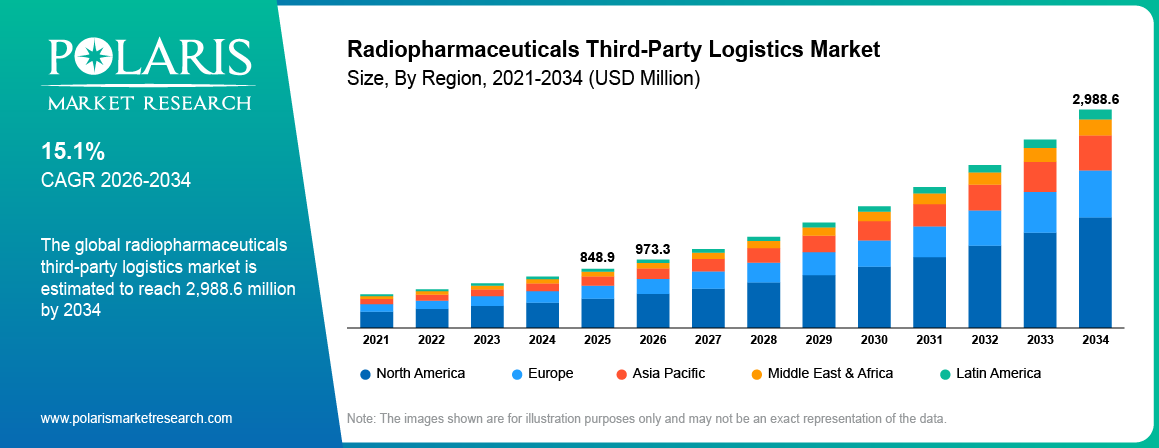

The global radiopharmaceuticals third-party logistics market is estimated around USD 848.9 million in 2025,with consistent growth anticipated during 2026–2034. Growth is driven by increasing adoption of nuclear medicine in oncology diagnostics and therapeutics, rising demand for radiopharmaceutical cold chain logistics, and expanding healthcare 3PL outsourcing services. The market is projected to grow at a CAGR of 15.1% during the forecast period.

Market Statistics

Key Takeaways

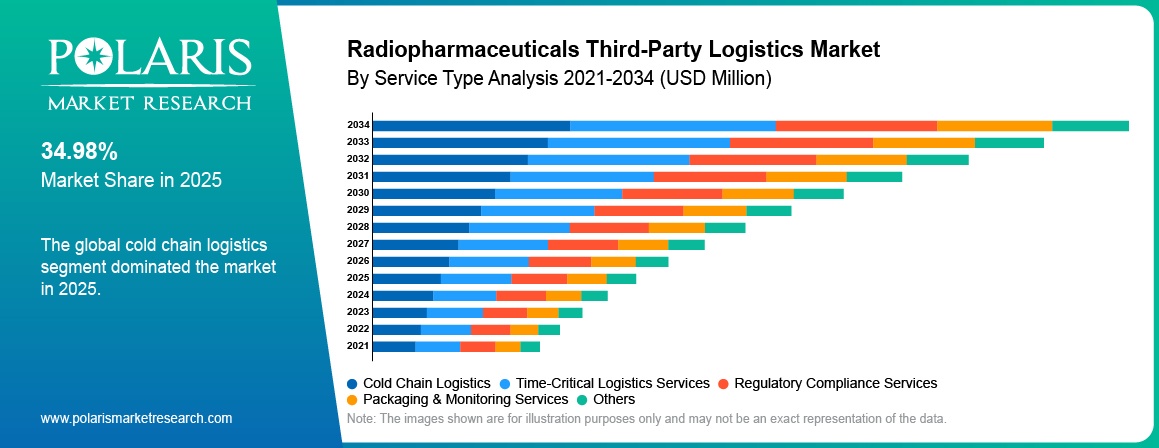

- Cold chain logistics dominated the market in 2025 by 34.98% revenue, due to increasing demand for temperature-controlled nuclear medicine transport and radiopharmaceutical stability management.

- Hospitals segment dominated the market by 36.5% share in 2025, driven by rising diagnostic imaging procedures and increasing radiopharmaceutical demand across oncology centers.

- Time-critical logistics services projected to grow at the fastest CAGR of 15.7% during the forecast period, owing to increasing demand for rapid isotope transport and just-in-time delivery systems.

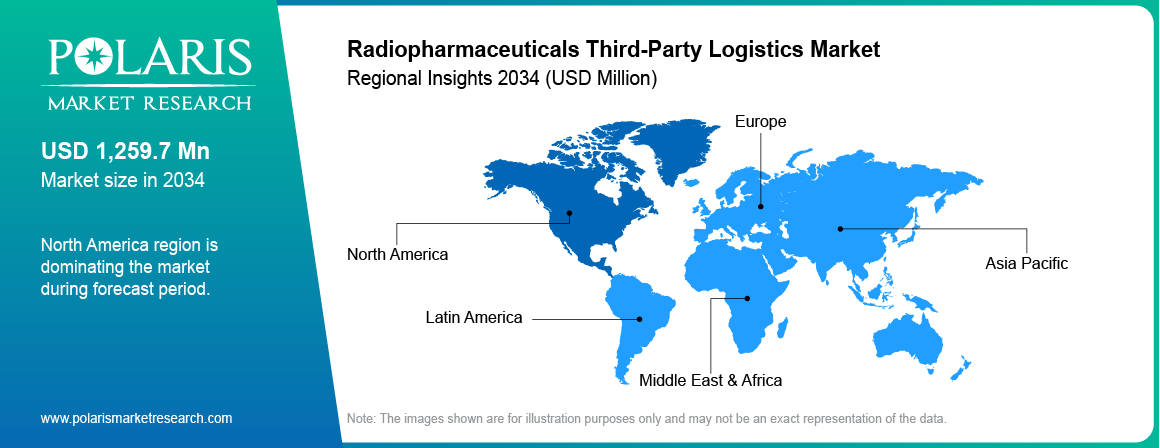

- North America dominated the market with 41.6% revenue share driven by advanced healthcare infrastructure and strong PET imaging adoption across the US.

- Asia Pacific radiopharmaceutical supply chain growth is projected to grow at the fastest CAGR of 15.6% during the forecast period, owing to increasing healthcare investments.

Industry Dynamics

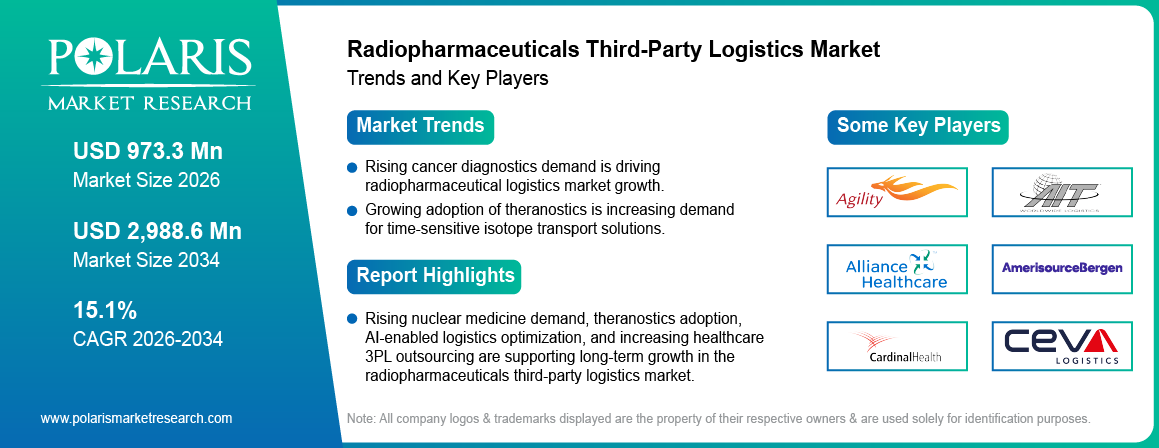

- Rising cancer diagnostics demand is driving radiopharmaceutical logistics market growth.

- Growing theranostics adoption is increasing demand for time-sensitive pharma logistics services.

- Strict radioactive transport regulations are restraining market expansion.

- AI-enabled logistics optimization and predictive monitoring are creating new opportunities in nuclear medicine logistics market.

What is the Radiopharmaceuticals Third-Party Logistics Market?

Radiopharmaceuticals third-party logistics market refers to specialized outsourced logistics services used for the transportation, storage, packaging, and monitoring of radioactive pharmaceutical products. These logistics services support nuclear medicine delivery systems used in PET imaging, SPECT imaging, oncology diagnostics, and targeted radiotherapy procedures. Transportation of radiopharmaceuticals calls for stringent temperature control, speeded up delivery, and temperature-controlled transportations due to time constraints due to isotope decaying.

The radiopharmaceuticals logistical chain works based on the value chain model, where isotope production plants, cyclotrons, radiochemical firms, packaging firms, logistics companies, distributors, and end users all come together. The third-party logistics companies handle the logistic management of radioactive substances, air cargo transportation, customs clearing, and delivery of the products to the end users.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

The market is witnessing an expansion owing to increased cancer incidence, growing usage of nuclear imaging tests, and significant investments in theragnostic and precision medicine. Rising demands for pharma cold chain validation, digital monitoring of nuclear medicines shipments, and healthcare logistics ecosystems are driving sustainable growth for the market.

Drivers & Opportunities

Rising Global Cancer Burden Increasing Nuclear Medicine Demand: Growing prevalence of cancer globally is resulting in increasing adoption of radiopharmaceuticals for diagnostic imaging and therapeutic applications. World Health Organization stated that about 35 million new cases of cancers is expected to arise globally by 2050, marking a rise by 77% compared to 2022 figures. There is rising reliance on dedicated pharma 3PL companies for delivering radiopharmaceuticals owing to their ability to ensure timely and compliance-based supply of isotopes at different healthcare facilities.

Expansion of Theranostics and Personalized Medicine: The increasing use of theranostics is due to rising demand for personalized drug delivery systems that addresses the requirement of radioactive substances such as Lu-177 and Ga-68. In September 2025, Memorial Sloan Kettering Cancer Center highlighted the improvements that have been achieved in the field of targeted imaging and radiotherapy treatments using radiopharmaceuticals for cancer patients. With the increasing popularity of personalization, the demand for logistics services associated with short half-life radioactive isotopes has also risen significantly.

Restraints & Challenges

Strict Regulatory Compliance and Operational Complexity: Regulations on transportation through IAEA and FDA have remained a difficult aspect for logistics companies to deal with. It is crucial to ensure that packaging technology, radiation protection, and cold chain logistics are available to help with the transportation of radioisotopes. This means that airport delays and customs clearance is expected to continue to affect costs and risks associated with logistics.

Opportunity

AI-Driven Logistics Optimization and Predictive Monitoring: AI usage in pharmaceutical logistic optimization has made improvements in areas such as visibility of shipments, routing plans, and accurate deliveries through radiopharmaceutical transportation networks. Predictive analytics algorithms have assisted the logistics companies in minimizing the wastage of isotopes and ensuring effective deliveries for nuclear medicines. In March 2026, Aptamer Group entered into an agreement with Radiopharmium Ltd to develop radiopharmaceuticals for cancer treatment purposes.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Segmental Insights

The report provides a comprehensive analysis of the radiopharmaceuticals third-party logistics market by service type and by end user to identify key revenue generating and high-growth segments.

By Service Type

-

Cold Chain Logistics

Cold chain logistics dominated the market in 2025 by 34.98% revenue, accounting for a major share due to strict temperature requirements associated with radiopharmaceutical stability and isotope transport logistics. Radiopharmaceutical cold chain logistics systems maintain controlled conditions between 2°C and 8°C or lower depending on isotope specifications. Increasing use of PET isotopes delivery and nuclear medicine transport solutions is supporting segment growth.

-

Time-Critical Logistics Services

Time-critical logistics services projected to grow at the fastest CAGR of 15.7% during the forecast period, owing to increasing demand for rapid isotope transportation and real-time nuclear medicine delivery systems. Delivery windows for several radiopharmaceuticals remain limited to only a few hours due to isotope decay. Increasing use of express courier services, rapid tracking systems, and multimodal pharma logistics networks is accelerating growth in this segment.

By End User

-

Hospitals

Hospitals segment dominated the market by 36.5% share in 2025 due to high numbers of PET imaging tests, cancer diagnosis, and radionuclides therapy procedures performed in the year 2025. Hospitals in large healthcare organizations require outsourced nuclear medicine logistics solutions for efficient distribution of radiopharmaceutical products to sustain their clinical processes.

-

Diagnostic Centers

Diagnostic centers projected to grow at the fastest CAGR during the forecast period, due to increasing demand for molecular imaging services and expansion of outpatient nuclear medicine facilities. Independent diagnostic centers are adopting specialized pharma logistics outsourcing solutions to improve operational efficiency and reduce isotope wastage. Growing demand for early-stage cancer detection and precision diagnostics is contributing to segment growth.

Source: Polaris Market Research Analysis

To Understand More About this Research: Request Customization

Regional Analysis

North America Radiopharmaceuticals Third-Party Logistics Market Assessment

North America dominated the market with 41.6% revenue share in 2025, driven by advanced healthcare infrastructure, strong PET scan adoption, and high investment in nuclear medicine delivery systems. The US leads regional demand due to increasing utilization of oncology imaging and theranostics. In May 2026, Bayer reported favorable outcomes from its Phase III trials of the PET tracer, I-124 Evuzamitide, for cardiac amyloidosis detection at several sites in the US. Increasing investment in precision molecular imaging technologies is supporting regional market expansion.

Europe Radiopharmaceuticals Third-Party Logistics Market Overview

Europe radiopharmaceutical logistics market held the second-largest share of approximately 28% market, driven by strict nuclear medicine compliance logistics standards and established healthcare infrastructure across Germany, France, and the UK. According to the European Nuclear Society, nuclear medicine supports diagnosis and treatment for more than 10 million patients annually across Europe. Increasing adoption of radiopharmaceutical transport regulations and advanced isotope handling systems is sustaining market growth.

Asia Pacific Radiopharmaceuticals Third-Party Logistics Market Insights

Asia Pacific radiopharmaceutical supply chain growth is projected to grow at the fastest CAGR of 15.6% during the forecast period, owing to increasing healthcare investments and expanding isotope production capabilities across China, India, and Japan. In December 2024, China announced successful development of a commercial reactor-based isotope production device for continuous production of Lu-177, Strontium-89, and Yttrium-90. Rising nuclear medicine adoption and expanding healthcare access are accelerating regional market expansion.

LATAM & MEA Emerging Markets

The radiopharmaceutical logistics industry in Latin America and the Middle East and Africa region is growing at a constant pace due to the advancements made in the medical sector and the acceptance of nuclear medicine. Countries like Brazil, Saudi Arabia, and the UAE are spending a lot in establishing facilities for the treatment of cancer diseases and for transporting radiopharmaceuticals.

Source: Polaris Market Research Analysis

To Understand More About this Research: Request Customization

Competitive Landscape

Key Players & Competitive Strategies

The market for radiopharmaceutical third party logistics services is moderately fragmented due to the presence of global health care logistics firms as well as firms specializing in the transport of nuclear medicine products. Competition is based on delivery speed, regulatory compliance, cold chain capability, geographic coverage, and digital shipment monitoring technologies. Market players are focusing on partnerships, acquisitions, AI-enabled logistics optimization, and expansion of temperature-controlled transportation networks to strengthen market position.

Major companies operating in the market include Agility Public Warehousing Company K.S.C., AIT Worldwide Logistics, Inc., Alliance Healthcare, AmerisourceBergen Corporation, BioMérieux SA, Cardinal Health, Inc., CEVA Logistics, Curium Pharma LLC, Deutsche Post DHL Group, FedEx Corporation, Kuehne + Nagel International AG, McKesson Corporation, SF Express Co., Ltd., UPS Supply Chain Solutions, Inc., and United Parcel Service of America, Inc.

Premium Insights

- Radiotheranostics is driving high-margin logistics demand due to increasing adoption of targeted radionuclide therapies and precision oncology applications across healthcare systems.

- The market is witnessing a shift toward integrated logistics platforms combining transportation, packaging, monitoring, and compliance management within a unified healthcare logistics ecosystem.

- There has been a recent pattern of acquisition and mergers in the health logistics firms, which has contributed to enhanced logistics distribution and creation of customized transport paths for radiopharmaceuticals.

- With artificial intelligence-driven supply chain management tools, logistics services have become more innovative, providing effective routing, accurate deliveries, inventory visibility, and efficient use of isotopes.

Isotope Supply Imbalance

| Region | Production Capacity | Demand Level | Supply Gap Status |

| North America | High | High | Balanced supply-demand environment |

| Europe | Moderate | High | Supply constrained due to reactor dependency |

| Asia Pacific | Low to Moderate | High | Significant isotope demand deficit |

Source: Polaris Market Research Analysis

Pricing Intelligence

Radiopharma Logistics Cost Structure

| Cost Component | Share of Total Logistics Cost |

| Transportation | 40% |

| Specialized Packaging | 20% |

| Regulatory Compliance | 15% |

| Monitoring & Tracking | 10% |

| Insurance & Risk Coverage | 15% |

Source: Polaris Market Research Analysis

Cost of Delay Model

- 1-hour delivery delay can result in approximately 10–20% isotope value loss due to radioactive decay.

- 4-hour shipment delay can lead to nearly 40–60% value erosion for short half-life radiopharmaceutical products.

| Shipment Type | Average Pricing Range |

| Domestic Shipment | USD 500–2,000 per delivery |

| International Shipment | USD 2,000–10,000+ per delivery |

Source: Polaris Market Research Analysis

Key Players

- Agility Public Warehousing Company K.S.C.

- AIT Worldwide Logistics, Inc.

- Alliance Healthcare

- AmerisourceBergen Corporation

- Cardinal Health, Inc.

- CEVA Logistics

- Curium Pharma LLC

- Deutsche Post DHL Group

- FedEx Corporation

- Kuehne + Nagel International AG

- McKesson Corporation

- SF Express Co., Ltd.

- UPS Supply Chain Solutions, Inc.

- United Parcel Service of America, Inc.

Industry Developments

- April 2026: Telix Pharmaceuticals and Regeneron Pharmaceuticals announced a strategic radiopharma collaboration to co-develop and commercialize next-generation radiopharmaceutical therapies for solid tumors. [source: telixpharma.com]

- October 2024: Nucleus RadioPharma announced the expansion of its radiopharmaceutical research, development, and manufacturing capacity through two new facilities in Arizona and Pennsylvania totaling more than 100,000 square feet. [source: businesswire.com]

Radiopharmaceuticals Third-Party Logistics Market Segmentation

By Service Type Outlook (Revenue, USD Million, 2021-2034)

- Cold Chain Logistics

- Time-Critical Logistics Services

- Regulatory Compliance Services

- Packaging & Monitoring Services

- Others

By End User Outlook (Revenue, USD Million, 2021-2034)

- Hospitals

- Diagnostic Centers

- Pharmaceutical & Biotechnology Companies

- Research Institutes

- Others

By Regional Outlook (Revenue, USD Million, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Radiopharmaceuticals Third-Party Logistics Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 848.9 Million |

| Market Size in 2026 | USD 973.3 Million |

| Revenue Forecast by 2034 | USD 2,988.6 Million |

| CAGR | 15.1% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The global market size was valued at USD 848.9 Million in 2025 and is projected to reach USD 2,988.6 Million by 2034 at a CAGR of 15.1%.

North America dominated the market with 41.6% revenue share due to advanced healthcare infrastructure and high PET imaging adoption across the US.

Key players include Deutsche Post DHL Group, FedEx Corporation, Kuehne + Nagel International AG, Cardinal Health, Inc., CEVA Logistics, and McKesson Corporation.

Key drivers include increasing cancer diagnostics demand, rising theranostics adoption, and growing outsourcing of nuclear medicine logistics services.

Major demand comes from hospitals, diagnostic centers, pharmaceutical companies, and research institutes.

The market outlook remains strong due to increasing investment in AI-enabled logistics optimization, decentralized isotope production, and smart cold chain systems.

Cold chain systems maintain radiopharmaceutical stability and reduce isotope degradation during transportation and storage operations.

Download Sample Report of Radiopharmaceuticals Third-Party Logistics Market

Please fill out the form to request a customized copy of the research report.