Ready-To-Drink Packaging Market Insights, Industry Outlook, 2026-2034

REPORT DETAILS

Ready-To-Drink Packaging Market Summary

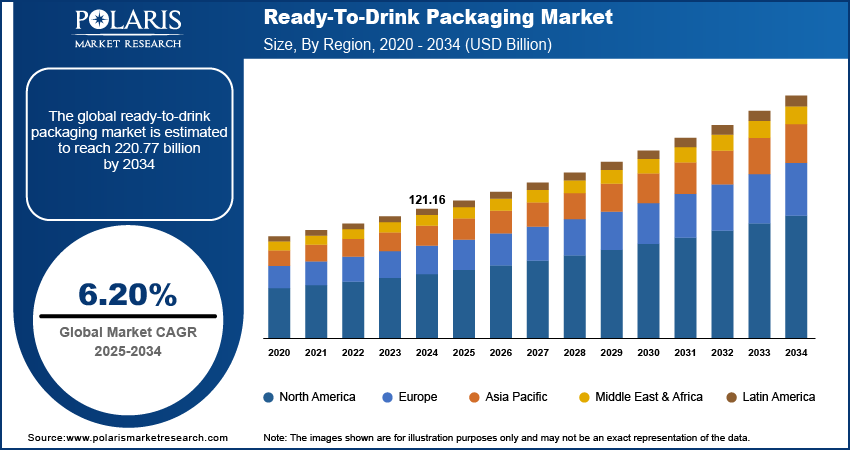

The global ready-to-drink packaging market size was valued at USD 128.51 billion in 2025. The market is projected to grow at a CAGR of 6.2% from 2026 to 2034. Rising global population and urbanization are driving packaged beverage consumption. The expansion of e-commerce platforms is driving higher distribution of RTD beverages.

Market Statistics

Key Takeaways

- North America dominated the global market with a 32.29% share in 2025. The regional market is driven by high ready-to-drink beverage consumption and advanced retail and e-commerce infrastructure.

- Asia Pacific is projected to grow at a 6.46% CAGR during the forecast period. This is due to urban population growth and the expansion of modern retail and online channels .

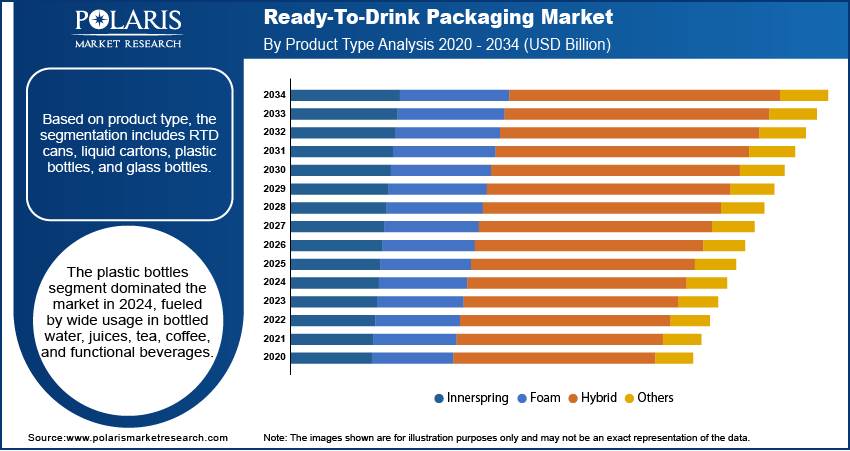

- The plastic bottles segment dominated the market with a 56.21% share in 2025. This is owing to their cost-effectiveness and lightweight nature .

- The PET material segment is projected to grow at a 5.6% CAGR during the forecast period due to its recyclability and environmental advantages .

- The bottled water segment led with a 39.25% share in 2025. The segment’s dominance is driven by rising consumption due to urbanization and health awareness.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Rising global population and urbanization are driving higher consumption of packaged beverages, creating demand for efficient RTD packaging solutions.

- Expansion of e-commerce platforms is supporting wider distribution of RTD beverages, increasing the need for durable and portable packaging formats.

- Technological advancements such as biodegradable, plant-based and compostable packaging solutions creates opportunity for the RTD packaging market.

- High production costs associated with sustainable and biodegradable packaging materials is hindering the growth of the market.

The ready-to-drink (RTD) packaging industry focuses on solutions that preserve quality, extend shelf life, and enhance convenience for beverages such as juices, tea, coffee, dairy-based drinks, energy drinks, and alcoholic beverages. It spans applications across retail, foodservice, and e-commerce channels. Growth is driven by packaging formats including bottles, cans, cartons, and pouches, along with closures and labeling solutions. These formats improve product safety, ensure regulatory compliance, and address consumer demand for convenience, portability, and sustainable options across developed and emerging economies.

Source: Polaris Market Research Analysis

In operational practice, advanced packaging materials such as PET, aluminum, paperboard, and biodegradable polymers provide durability, barrier protection, and recyclability. Manufacturers are integrating green packaging features including QR codes and freshness indicators to improve traceability and consumer engagement. Automation and robotics in filling and sealing processes enhance efficiency, reduce contamination risks, and lower production costs. For instance, beverage producers are increasingly adopting lightweight bottles and recyclable cartons to reduce environmental impact and align with sustainability targets.

The RTD packaging market is expanding as food and beverage companies respond to stricter sustainability regulations and rising consumer preference for eco-friendly solutions. In April 2025, Yoplait introduced clear, recyclable bottles made with 35% recycled PET (rPET) for its Yop yoghurt drink. The new design features an attached cap and a micro-perforated sleeve, enhancing sustainability and user convenience. Investment in circular economy practices and the adoption of plant-based or compostable packaging materials are creating new opportunities. Public–private initiatives and brand-led sustainability programs are supporting large-scale adoption of recyclable and low-carbon packaging. The industry is advancing through innovations in digital printing, smart labeling, and refillable formats, which are expected to drive long-term growth.

Cans vs Bottles vs Cartons in RTD Packaging

| Factors | Cans | Bottles | Cartons |

| Material | Made of aluminum or metal | Made of plastic/PET/glass | Made of paperboard layers |

| Portability | Easily portable | Convenient and resealable | Portable and space-saving |

| Shelf Life | Excellent shelf-life protection | Adequate shelf-life protection | Extremely long shelf-life protection |

| Recyclability | Very high recycle rate | Low recycle rate | Increasingly high recycle rate |

| Common Applications | Energy drinks, soft drinks, alcoholic beverages | Water, fruit juices, dairy beverages | Milk and fruit juices |

Source: Polaris Market Research Analysis

Drivers & Opportunities

Rising global population and urbanization driving packaged beverage consumption: The rapid growth of the global population and accelerated urbanization are increasing the demand for packaged beverages, which directly drives the adoption of RTD packaging solutions. A United Nations report projects that urban areas will gain 2.5 billion more people by 2050 due to the ongoing global shift from rural to urban living. Urban lifestyles are characterized by limited time, higher disposable incomes, and a preference for on-the-go consumption, creating strong reliance on ready-to-drink products such as tea, coffee, juices, and functional beverages. Rising health awareness and demand for convenient nutrition are further expanding packaged beverage consumption. This trend is pushing beverage producers to adopt advanced packaging formats that ensure portability, extended shelf life, and regulatory compliance across developed and emerging economies.

Expansion of global e-commerce platforms supporting higher RTD beverage distribution: The growth of global e-commerce platforms is reshaping beverage distribution by providing wider access to RTD products across diverse consumer bases. Online retail channels enable efficient delivery of packaged beverages to urban and semi-urban markets, increasing reliance on durable, lightweight, and spill-proof packaging formats. Subscription models and direct-to-consumer strategies are fueling higher sales of RTD beverages through digital platforms. As per the International Trade Administration (ITA), the global B2C e-commerce revenue is projected to reach USD 5.5 trillion by 2027, growing at a steady 14.4% annual rate. The convenience of doorstep delivery, coupled with promotional pricing, is expanding consumer preference for buying beverages online. This shift is compelling manufacturers to invest in packaging innovations that enhance product protection, improve shelf presentation, and reduce logistics costs.

Sustainable & Eco-Friendly Packaging Trends

Sustainability is emerging as a key focus area in the ready-to-drink packaging industry. Businesses are using recyclable PET materials, biodegradable packaging, lighter bottles, and less plastic to support sustainable development. Companies in the beverages sector are focusing on adopting environmentally friendly packaging methods to cater to their customers' needs and comply with environmental laws. In addition, companies have adopted the use of recycled materials in packaging and effective recycling practices. Growing consumer awareness about environmental concerns has led firms to develop packaging systems that would provide safety, convenience, and lower carbon emissions.

Source: Polaris Market Research Analysis

Segmental Insights

Product Type Analysis

Based on product type, the segmentation includes RTD cans, liquid cartons, plastic bottles, and glass bottles. The plastic bottles segment dominated the RTD packaging market in 2025 with 56.21% share driven by its cost-effectiveness, lightweight nature, and wide compatibility with different beverages. Plastic bottles provide durability, spill-proof sealing, and extended shelf life, making them suitable for retail, e-commerce, and on-the-go consumption. Manufacturers favor plastic bottles for mass production due to their low transportation costs and ease of customization with labels, caps, and shapes. Rising consumer preference for convenient packaging formats and high adoption in developing and urban markets further strengthens the dominance of plastic bottles in the overall RTD packaging market.

The RTD cans segment is projected to grow at the fastest CAGR during the forecast period due to rising demand for portability and enhanced product protection. Cans offer superior barrier properties against light and oxygen, ensuring beverage freshness for longer durations. Increasing adoption in energy drinks, alcoholic RTDs, and functional beverages is driving growth, fueled by lightweight designs that reduce logistics costs. Innovative designs and digital labeling are improving brand visibility, while consumer preference for recyclable aluminum materials to meet sustainability goals, boosting the adoption of RTD cans across developed and emerging regions.

Material Analysis

Based on material, the segmentation includes metal, glass, plastic, pet, and cartons. The plastic dominated the RTD packaging market in 2025 due to its affordability, lightweight properties, and versatility. It is widely used in bottles, pouches, and closures for multiple beverages, providing durability and ease of transport. Plastic packaging allows mass customization, supports efficient production processes, and ensures compliance with safety and hygiene standards. Its extensive adoption in urban and semi-urban regions, along with compatibility with automation and filling systems, pushes its dominance. Rising demand for on-the-go beverages and e-commerce distribution channels further strengthens the role of plastic materials in RTD packaging.

The PET material segment is projected to grow at the fastest CAGR of 5.6% during the forecast period due to its recyclability and environmental advantages. PET provides high clarity, strength, and chemical resistance, making it suitable for beverages such as water, juices, and functional drinks. In May 2025, Faerch launched a hot drink lid made from up to 85% recycled PET, fully recyclable and designed for a secure, sustainable, and leak-resistant fit. Increasing consumer awareness of sustainability and brand commitments to reduce carbon footprint are driving PET adoption. Lightweight and durable PET bottles reduce transportation costs and improve logistics efficiency. Manufacturers are increasingly integrating PET into innovative packaging formats, including single-serve and multi-pack solutions, to meet evolving market demand and regulatory sustainability requirements.

Application Analysis

Based on application, the segmentation includes alcoholic beverages, tea & coffee, bottled water, fruit juices, milk and milk products, and carbonated drinks. The bottled water dominated the RTD packaging market in 2025 with 39.25% share, driven by rising consumption due to urbanization, health awareness, and convenient lifestyle trends. Bottled water requires durable, lightweight, and spill-proof packaging, making it compatible with plastic and PET materials. High demand across retail and e-commerce channels, coupled with frequent consumption patterns, ensures steady market revenue. Manufacturers prioritize innovative packaging designs and labeling to improve brand visibility. Adoption of recyclable materials and portion-controlled formats further strengthens bottled water’s position, driven its dominance in the RTD packaging industry across developed and emerging markets.

The tea and coffee segment is projected to grow at the fastest CAGR during the forecast period due to rising demand for ready-to-drink functional beverages. Increasing preference for convenient, on-the-go consumption and flavored beverages is driving growth. Innovative packaging solutions such as cans, cartons, and PET bottles preserve taste, aroma, and freshness while enabling easy portability. Adoption of sustainable materials, smart labeling, and portion-controlled packaging supports brand differentiation. Growth is further accelerated by e-commerce platforms and cold-brew coffee trends, enabling wider distribution and catering to health-conscious and busy urban consumers globally.

Source: Polaris Market Research Analysis

Regional Analysis

North America ready-to-drink packaging market dominated the global market in 2025 with 32.29% share. This is due to the high consumption of ready-to-drink beverages and strong retail and e-commerce infrastructure. Moreover, increasing consumers preference towards convenience-based packaging formats such as plastic bottles and cans to support on-the-go lifestyles is driving the industry. In addition, stringent regulatory standards regarding food safety and packaging recyclability are driving manufacturers to adopt advanced packaging solutions, ensuring compliance and sustainability. Furthermore, growing investments in automation and smart labeling technologies by beverage companies are improving operational efficiency and product traceability.

The U.S. Ready-To-Drink Packaging Market Insight

The U.S. held a dominating market share in the North America ready-to-drink packaging landscape in 2025, due to high per capita consumption of ready-to-drink beverages and a preference for convenient on-the-go packaging formats. For instance, in July 2025, Avient launched ColorMatrix Amosorb Oxyloop-1, an oxygen-scavenging additive that improves PET packaging recyclability. It works with up to 100% recycled PET, maintains clarity, and meets global food contact regulations. Moreover, extensive retail and e-commerce infrastructure is supporting wider product distribution and faster market penetration. In addition, growing consumer awareness about recyclable and lightweight packaging materials is driving adoption of PET bottles, plastic bottles, and cans. Furthermore, investments in automation, smart labeling, and digital tracking by beverage manufacturers are improving operational efficiency and traceability.

Europe Ready-To-Drink Packaging Market

The ready-to-drink packaging landscape in Europe is projected to hold a substantial share in 2034. This is owing to the rising demand for sustainable and recyclable packaging materials is driving growth in plastic and aluminum cans. As an example, in December 2024, the European Union (EU) adopted the Packaging and Packaging Waste Regulation (PPWR - Regulation (EU) 2025/40) to promote a circular and competitive economy for packaging and packaging waste. Moreover, growing consumer preference for premium ready-to-drink beverages such as cold-brew coffee and flavored teas is supporting market expansion. In addition, stringent government regulations on environmental sustainability are pushing manufacturers to adopt innovative packaging formats that minimize waste and carbon footprint.

Asia Pacific Ready-To-Drink Packaging Market

The market in Asia Pacific is projected to grow at the fastest CAGR of 6.46% during the forecast period. This growth is expanding due to the rapid urban populations and increasing disposable incomes are boosting the demand for packaged beverages, driving adoption of PET bottles and cartons. Moreover, rapid growth of e-commerce and modern retail channels in urban centers is supporting wider distribution of RTD products. In addition, the focus on eco-friendly and lightweight packaging solutions is fueling beverage manufacturers to innovate, enhancing consumer acceptance.

China Ready-To-Drink Packaging Market Overview

The market in China is expanding due to rising urbanization and increasing disposable incomes, which are boosting packaged beverage consumption. According to the U.S. Energy Information Administration (EIA), China's per capita disposable income is projected to increase from USD 12,236 in 2025 to USD 19,156 in 2035. This represents a growth of approximately 56.5% over the 10-year period. Moreover, rapid growth of e-commerce and modern retail channels in urban centers is enabling wider distribution of RTD beverages. In addition, government initiatives promoting sustainable and recyclable packaging materials are driving manufacturers to invest in PET bottles, cartons, and cans.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The ready-to-drink packaging market is moderately fragmented, with leading players focusing on innovative packaging solutions, automation, and smart labeling to enhance operational efficiency and product traceability. Companies are expanding their portfolios with recyclable PET bottles, aluminum cans, cartons, and biodegradable materials to meet sustainability goals and growing consumer demand. Moreover, collaborations between beverage manufacturers, packaging providers, and technology companies are enabling product innovation and supporting the adoption of region-specific packaging formats, strengthening long-term competitiveness across retail, e-commerce and foodservice channels worldwide.

Major companies operating in the ready-to-drink packaging industry include Tetra Laval Group, Crown Holdings, Inc., Amcor Limited, Ball Corporation, Ardagh Metal Packaging, Smurfit Kappa, SIG Combibloc, Elopak, Vetropack Group, Graphic Packaging International, Graham Packaging Company, and WestRock Company.

Key Players

- Amcor Limited

- Ardagh Metal Packaging

- Ball Corporation

- Crown Holdings, Inc.

- Elopak

- Graham Packaging Company

- Graphic Packaging International

- SIG Combibloc

- Smurfit Kappa

- Tetra Laval Group

- Vetropack Group

- WestRock Company

Future Outlook

The ready-to-drink packaging market is forecast to grow, driven by rising consumer preference for convenience beverages and sustainable packaging innovations. The rise in beverage sales through online channels is another factor contributing to market growth. Innovations in packaging technology, along with other factors such as urbanization and lifestyle changes, are likely to be key drivers in demand growth in the coming years.

Industry Developments

- April 2026: INNORHINO announced the official expansion of its orth American footprint. The company stated that the strategic expansion will connect its Los Angeles headquarters with an established manufacturing network in Shenzhen and Taipei. It will help companies move from digital concept to factory reality without any structural failures. (source: innorhino.com)

Ready-To-Drink Packaging Market Segmentation

By Product Type Outlook (Revenue, USD Billion, 2021–2034)

- RTD Cans

- Liquid Cartons

- Plastic Bottles

- Glass Bottles

By Material Outlook (Revenue, USD Billion, 2021–2034)

- Metal

- Glass

- Plastic

- PET

- Cartons

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Alcoholic Beverages

- Tea & Coffee

- Bottled Water

- Fruit Juices

- Milk and Milk Products

- Carbonated Drinks

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Ready-To-Drink Packaging Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 128.51 Billion |

| Market Size in 2026 | USD 139.24 Billion |

| Revenue Forecast by 2034 | USD 220.77 Billion |

| CAGR | 6.20% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Techniqueat |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Ready-To-Drink Packaging Market FAQ's

The global market size was valued at USD 128.51 billion in 2025 and is projected to grow to USD 220.77 billion by 2034.

The global market is projected to register a CAGR of 6.20% during the forecast period.

North America dominated the RTD packaging market with 32.29% share in 2025, driven by high consumption of ready-to-drink beverages and e-commerce infrastructure.

A few of the key players in the market are Tetra Laval Group, Crown Holdings, Inc., Amcor Limited, Ball Corporation, Ardagh Metal Packaging, Smurfit Kappa, SIG Combibloc, Elopak, Vetropack Group, Graphic Packaging International, Graham Packaging Company, and WestRock Company.

The plastic bottles segment dominated the market in 2025 with 56.21% share, fueled by cost-effectiveness, durability and compatibility with various beverages across retail and on-the-go consumption channels.

The plastic segment dominated the RTD packaging market in 2025, driven by affordability, lightweight properties, versatility and wide adoption in urban and semi-urban regions.

Download Sample Report of Ready-To-Drink Packaging Market

Please fill out the form to request a customized copy of the research report.