Rigid Food Packaging Market Business Overview, and Strategic Insights, 2025-2034

REPORT DETAILS

REPORT DETAILS

Market Statistics

Overview

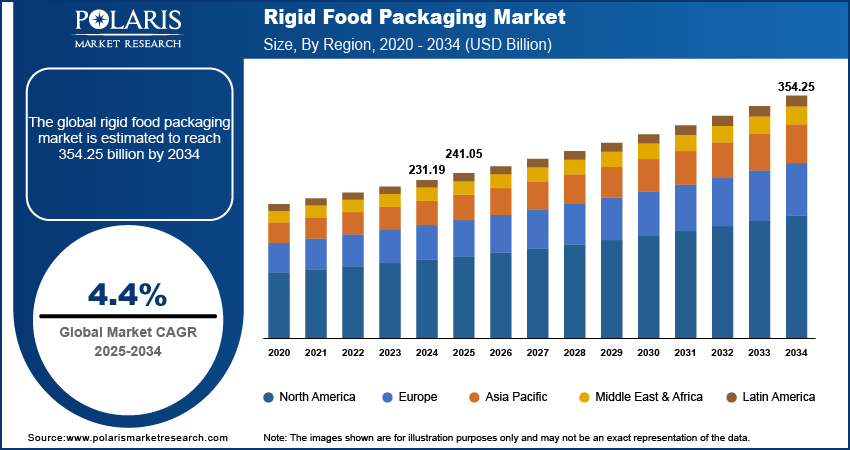

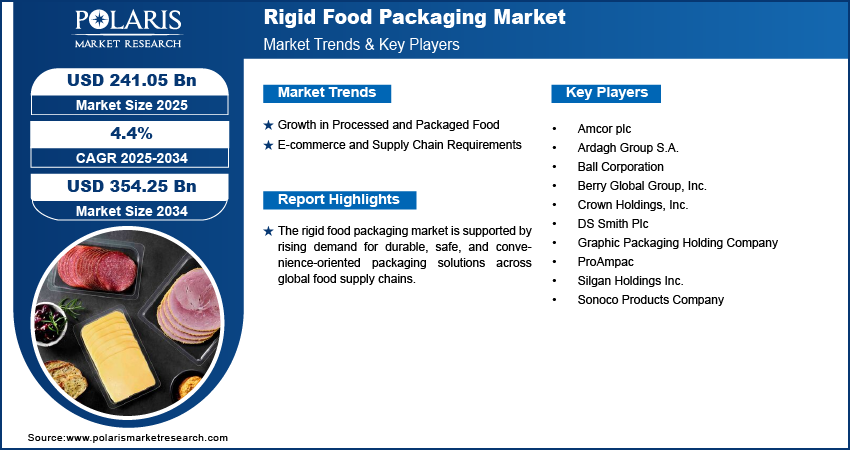

The global rigid food packaging market size was valued at USD 231.19 billion in 2024, growing at a CAGR of 4.4% from 2025–2034. Key factors driving demand for rigid food packaging include extended shelf life and food safety, demand for convenience and portability, the rise in consumption of processed food and packaged food, and e-commerce and supply chain demands.

Key Insights

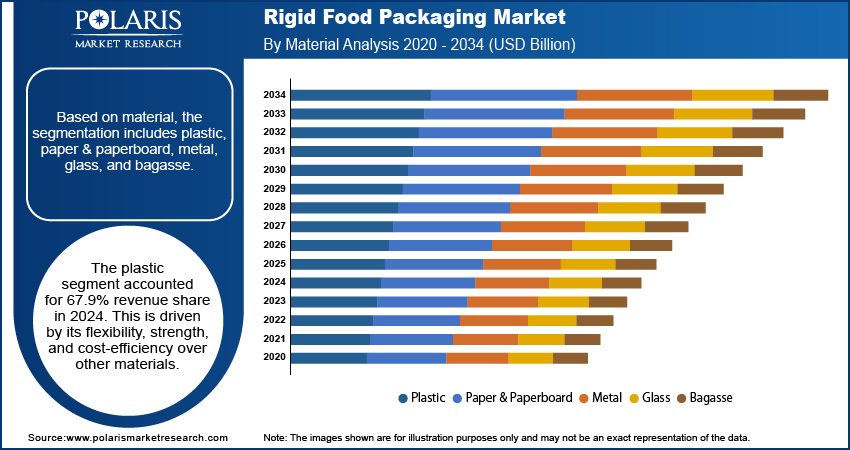

- The plastic accounted for 67.9% of the revenue in 2024. This is because they are lightweight, which decreases the cost of transportation, and it can be injected, blown, compressed, transferred, molded, and extruded.

- The bottles & jars segment is anticipated to maintain a significant share during the forecast period. This is because of high strength to avoid leaking and protect the products both in handling and shipping.

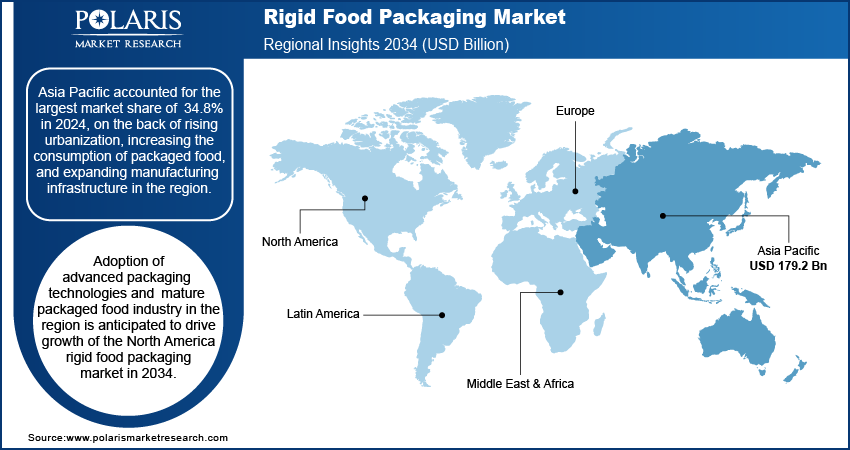

- Asia Pacific held the largest market share of 34.8% in 2024. It is driven by high investment in food processing & packaging industry and material production.

- Increasing use of sophisticated packaging solutions, and presence of well-developed packaged food industry in the region are the key factors expected to contribute to the growth of North America rigid food packaging market in 2034.

Industry Dynamics

- Growing usage of processed and packaged food fuels the growth of the market.

- The growing e-commerce and supply chain demands enhance the growth opportunities.

- Multi-material laminate recycling complexity, challenges the circular economy advancement.

- Lightweight, high-barrier mono-material solutions that fulfill sustainability requirements and are under regulatory scrutiny pave the way for growth.

Market Statistics

- 2024 Market Size: USD 231.19 billion

- 2034 Projected Market Size: USD 354.25 billion

- CAGR (2025-2034): 4.4%

- Asia Pacific: Largest market in 2024

AI Impact on the Industry

- Streamlining design, evaluation of quality and production can accelerate pace as well as lower costs.

- Down-time and material scrap are reduced by predictive maintenance and real-time production optimization.

- Allows for agile short-run packaging solutions to address niche markets or trends.

- AI-based forecasting and logistics enhance inventory management and response to disruptions.

Rigid food packaging includes all packaging forms for which a high level of protection is provided owing to its strength and inflexibility such as bottles, jars, trays, tubs, cartons, cans, and pails. The development of rigid food packaging is steadily advancing with the increasing attention on enhancement of barrier property, food preservatives and performance of packaging. The increased focus on longer shelf life and food safety drives the growth due to the nature of their material. Rigid packaging provides better protection from moisture, oxygen, contamination and physical damage. This allows food products to stay fresh for longer period. They also have the ability to feature advanced sealing, tamper-evident options and high-barrier materials, so manufacturers looking for enduring product quality often turn to them. Thus, with increasing regulatory scrutiny on hygiene and food standards, the need for safe, contamination resistant packaging to address all of these factors reinforce rigid solutions as the package of choice across all segments.

The growing consumer lifestyle, which favors easy-to-use, portable products, is also driving demand. Rigid packaging formats are made to be handled, stored and transported easily, making them perfect for a wide range of applications such as ready meals, snacks on the go, drinks, and single-serve food. Stackable and durable design, as well as compatibility with automation filler lines ensures efficiency in operation and consumer appeal. This industry continues to respond with innovative features that meet consumer needs, such as resealable closures, ergonomic shapes and microwave safe containers, with meal-conscious consumers on the go and seek convenience. These attributes make rigid food packaging a viable option for excellence in performance and convenience in modern food consumption.

Drivers & Opportunities

Growth in Processed and Packaged Food: The demand for the market is increasing owing to the rise in consumption of processed food and packaged food as consumers prefer ready-to-cook, ready-to-eat and long-shelf food products to have fast food amid their busy schedules. This shift is pushing up the need for packaging formats that ensure product freshness, maintain product stability while handling, and during storage and transportation. A UN Trade& Development report from March 2024 states that trade in foods had expanded by 350% to reach USD 1.7 trillion, highlighting a demand for dependable, rigid and innovative packaging solutions. In addition, high temperature processable rigid packaging provides excellent barrier to protect the product from contamination. This is for the packed meal, dairy, bakery, and frozen food industries. Its shape stability, branding, and portion-controlling attributes make it the ideal packaging for food manufacturing on a large-scale. Therefore, once rigid packaging provides the reliable strength and integrity to process and protect the product to longer shelf life, as food manufacturers are increasingly able to add additional types of products to their portfolio.

E-commerce and Supply Chain Requirements: Growing e-commerce and supply chain demands drive the need for rigid food packaging. According to ITA the Global B2C ecommerce revenue is expected to grow to USD 5.5 trillion by 2027 at a steady 14.4%. The packaging needs to be durable to transportation, temperature changes and to be handled at least 3 times due to online food retail, home delivery, and omnichannel distribution. Impact resistance of rigid packaging utilizes the natural strength of the container material and shape to an extent that food products are safely protected from external forces during distribution. Their standardized size increases palletization and logistics efficiency and additional features like tamper-evident closures foster trust in direct-to-home deliveries. Therefore, rigid packaging protect goods, facilitate transit, and minimize product damage and is an essential part of today's food distribution system.

Premium Insights- Emerging Technological Advancements

| Technology/Advancement | Description |

| Recycled-ready packaging & PCR materials | Packaging solutions with high recyclability incorporating post-consumer recycled (PCR) content to improve sustainability and circularity. |

| High-performance polyethylene film with VO+ technology | Films with micro-scale air pockets reducing plastic density, enhancing strength and recyclability, suitable for food contact packaging. |

| DairySeal and ClearCor PET barrier | PET packaging with ClearCor barrier providing recyclability up to 80% of materials used, maintaining taste and performance for beverages. |

| NextGen Furnace for glass packaging | Hybrid electric furnace technology reducing CO2 emissions by over 60% during glass container manufacturing. |

| ClipCombo modular machinery system | Machinery allowing flexible multipack styles on one system, reducing plastic rings and shrink wrap use, enhancing sustainability and throughput. |

| Fiberization of packaging | Transition from rigid to flexible or fiber-based materials to reduce carbon footprint, focus on mono-material recyclable films and foil replacements. |

| Z-Flute advanced paperboard | Sustainable paperboard packaging reducing fiber usage but maintaining strength to support circular economy principles. |

| Digital direct-to-shape decoration | High-speed digital printing technology with photorealistic quality and sustainable benefits for metal beverage cans. |

| AI applications in packaging design | Use of artificial intelligence to accelerate packaging development, enhance creativity, reduce time and cost in producing sustainable packaging. |

Segmental Insights

Material Analysis

Based on material, the segmentation includes plastic, paper & paperboard, metal, glass, and bagasse. The plastic segment accounted for 67.9% revenue share in 2024. This is driven by its flexibility, strength, and cost-efficiency over other materials. Its barrier properties are used to pack many types of perishable and processed food. Its light weight also reduces transportation costs, and since it can be injected, blown, compressed, transferred, molded and extruded, it is possible to produce a wide range of different shapes and sizes. Plastic also lends itself to large-scale production, making it possible to efficiently package at scale to keep up with growing consumer appetites for packaged fuel. The growing application of recyclable light weight polymer grades further boosts the demand for the product in the rigid packaging market.

Packaging Type Analysis

In terms of packaging type, the segmentation includes boxes & cartons, trays & clamshell, bottles & jars, cans, cups & tubs, and others. The bottles & jars segment is expected to hold substantial share during the forecast period. This is due to its heavy application in beverages, sauces and condiments, dairy, and shelf-stable food products. These forms have high strength to avoid leaking and protect the products during both handling and shipping. Their transparency and flexibility for labeling also help brands’ visibility, and the ability to reseal gives consumers a more convenient experience and better portion control. In addition, bottles and jars can be used with automated filling lines and high-speed production equipment, therefore they are the most popular choice for producers. The aptitude to ensure extended shelf life and freshness of the contents benefits them increasingly in the rigid packaging industry.

Regional Analysis

Asia Pacific Rigid Food Packaging Market Assessment

Asia Pacific accounted for the largest market share of 34.8% in 2024, on the back of rising urbanization, increasing the consumption of packaged food, and expanding manufacturing infrastructure in the region. A 2025 United Nations Industrial Development Organization (UNIDO) report declared that industrial development in Asia-Pacific attained 57%. Furthermore, growth in the middle-class demographic and changing diets have influenced greater reliance on processed and convenience foods. This leads to increased demand for rigid pack materials. The region’s competitiveness is attributed to high investment in food processing and packaging industry, and material production. It also benefits from a strong domestic packaging industry that provides a broad range of rigid packaging solutions adapted to regional demands in volume. These trends are anticipated to consolidate the position of the Asia Pacific region in the global market for rigid food packaging.

North America Rigid Food Packaging Market Insights

Adoption of advanced packaging technologies and mature packaged food industry in the region is anticipated to drive growth of the North America rigid food packaging market in 2034. Rigid packaging formats continue to be popular among consumers, as the demand for convenience, portion control and high-quality packed products keeps increasing. The region is also driven with strong material and recycling system innovation, and design optimization to support sustainable packaging transitions. In addition, developed retail and e-commerce systems demand packaging that stand the test of time, protect products during distribution. These contribute towards making rigid food packaging solutions in North America a vital market to the future development of this industry.

Key Players & Competitive Analysis Report

Competition within the rigid packaging industry is intense, due to technological advancement and sustainability considerations. Leading industry competitive intelligence reveals key players differentiating through strategic investments in light-weight, mono-material based solutions to create resilient, sustainable value chains. The first growth potential is represented by developing countries, due to increasing consumption that creates the demand, while developed countries are getting circular models. For SMEs, the ability to quickly adapt to new materials and digital printing gives them a competitive edge over large incumbents. Success depends on adapting to supply chain disruptions, and economic and geopolitical shifts, with strategies for future development focused on innovation and regional customization to drive revenue growth.

Major companies operating in the rigid food packaging industry include Amcor plc; Ardagh Group S.A.; Ball Corporation; Crown Holdings, Inc.; DS Smith Plc; Graphic Packaging Holding Company; ProAmpac; Silgan Holdings Inc.; Sonoco Products Company; and WestRock Company.

Key Players

- Amcor plc

- Ardagh Group S.A.

- Ball Corporation

- Crown Holdings, Inc.

- DS Smith Plc

- Graphic Packaging Holding Company

- ProAmpac

- Silgan Holdings Inc.

- Sonoco Products Company

- WestRock Company

Industry Developments

-

In March 2025, LyondellBasell launched Pro-fax EP649U, a polypropylene impact copolymer for the rigid packaging market, designed for thin-walled injection molding and well suited for food packaging applications.

-

In February 2025, Avantium N.V., a renewable and circular polymer materials company, collaborated with Amcor Rigid Packaging USA, LLC a responsible packaging solutions company. This partnership aims to use Avantium's plant-based polymer PEF releaf for various products.

-

In September 2024, Marigold Health Foods collaborated with Sonoco, to launch a fully recyclable packaging solution for plant-based food products, such as stock cubes, sauces, and meat and fish alternatives.

Rigid Food Packaging Market Segmentation

By Material Outlook (Revenue, USD Billion, 2020–2034)

- Plastic

- Paper & Paperboard

- Metal

- Glass

- Bagasse

By Packaging Type Outlook (Revenue, USD Billion, 2020–2034)

- Boxes & Cartons

- Trays & Clamshell

- Bottles & Jars

- Cans

- Cups & Tubs

- Others

By Application Outlook (Revenue, USD Billion, 2020–2034)

- Meat, Poultry & Seafood

- Dairy Products

- Bakery & Confectionary

- Ready-to-eat Food

- Baby Food

- Produce Food

- Other Foods

By Regional Outlook (Revenue, USD Billion, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Rigid Food Packaging Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 231.19 Billion |

| Market Size in 2025 | USD 241.05 Billion |

| Revenue Forecast by 2034 | USD 354.25 Billion |

| CAGR | 4.4% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 231.19 billion in 2024 and is projected to grow to USD 354.25 billion by 2034.

The global market is projected to register a CAGR of 4.4% during the forecast period.

The Asia Pacific dominated the market in 2024, accounting for 34.8%.

A few of the key players in the market are Amcor plc; Ardagh Group S.A.; Ball Corporation; Crown Holdings, Inc.; DS Smith Plc; Graphic Packaging Holding Company; ProAmpac; Silgan Holdings Inc.; Sonoco Products Company; and WestRock Company.

The plastic segment accounted for 67.9% revenue share in 2024.

The bottles & jars segment is expected to hold substantial share during the forecast period.

Download Sample Report of Rigid Food Packaging Market

Please fill out the form to request a customized copy of the research report.