Robo Taxi Market Demand, Industry Share, Global Report, 2026-2034

REPORT DETAILS

What is the Current Market Size?

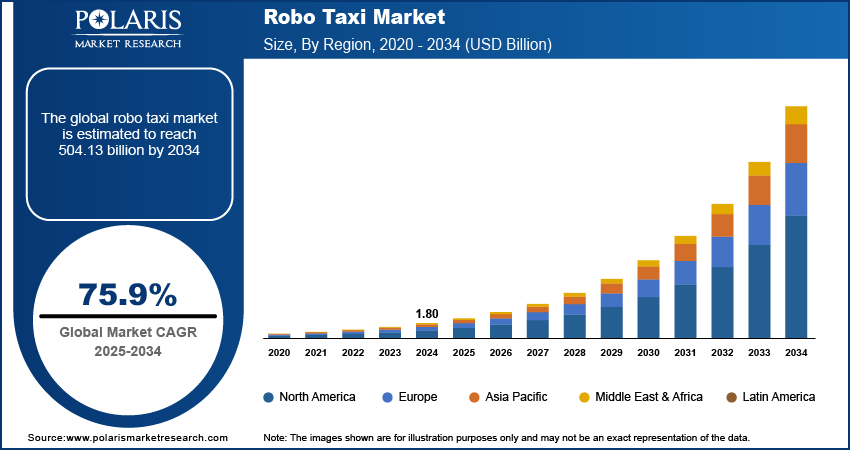

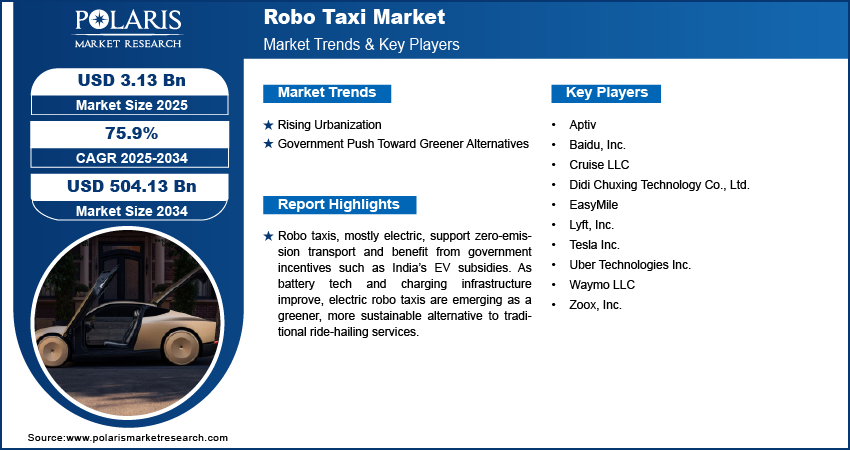

The global robo taxi market size was valued at USD 486.75 million in 2025, growing at a CAGR of 92.8% from 2026–2034. Key factors driving demand include rising urbanization, government push towards greener alternatives.

Market Statistics

Key Takeaways

- North America led the global market in 2025, holding a 72.2% revenue share. This is driven by a strong technological?base and relatively early market introduction

- The robo taxi landscape in Asia Pacific is projected to witness the fastest growth during the forecast period at a CAGR of 93.1% driven by growing urbanization, developing digital infrastructure, and high technological penetration.

- Based on propulsion type, the segmentation includes electric vehicles, hybrid electric vehicles, fuel cell vehicle. The electric vehicle segment accounted for 69.4% revenue share in 2025.

- Based on component type, the segmentation LiDAR, radar, camera, sensor. The camera segment is expected to witness the fastest growth during the forecast period at a CAGR of 94.7%

Note- Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Rising urbanization intensifies in traffic density, traffic congestion, and parking shortage driving the demand.

- Government push towards greener alternatives is due to autonomous mobility platforms which are being developed based on electric vehicle driving the growth.

- Large scale commercial profitability and fleet expansion is delayed by high capital and R&D costs and by uncertain regulatory regimes end to end in different cities and countries.

- Increasing collaborations among autonomous vehicle makers, ride-hailing platforms, and city authorities allow for real-world testing, data exchange, and staged deployment that speeds up consumer adoption and learning.

What Does Robo Taxi Market Includes?

A robo taxi is a robot vehicle which is made available via on demand ride hailing applications, where it employs a complex suite of digital systems that enable it to see, understand, and navigate the road environment. Growth of the global robo taxi market is highly attributed to the evolving technology in artificial intelligence and sensor technologies including LiDAR, radar, high-resolution cameras, and edge computing platforms. In March 2026, RoboSense released its thousand-beam-level digital LiDAR EM4 and solid-state E1 to be adopted in the Robotaxi GXR, co-developed by WeRide and Farizon. Production of 2,000 units starts in the third quarter of 2026. These innovations allow self-driving cars to more accurately interpret their environment, better object detection, path planning, vehicle behavior and real-time driving decision making. An array of complex AI techniques analyzes massive amounts of sensor data to learn traffic flow, road infrastructure, and pedestrian movements. Additionally, progress in edge computing allows for data to be processed on board the vehicle, which may reduce lag and enable quicker responses to dynamic road environments. Significant reliability and safety enhancements will be enabled in autonomous mobility solutions as these integrated sensing and computing systems mature. Hence, this technological innovation is increasing the operation cost efficiency of the robo taxi service.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Cost of components for autonomous vehicles is slowly decreasing, which is another important driver for the robo taxi market growth. During early development of autonomous mobility, high-end hardware including refined sensors, and synthetic hardware components had dramatic influence on the cost for the implementation of AVs. Nevertheless, advances in technology, higher production volumes and improvements in semiconductor efficiency are the factors for component prices. The costs of lidar, automotive radar, and computing modules are trending downward with standardization of manufacturing processes and maturation of supply chains. Furthermore, reduced component costs are allowing mobility service providers and technology developers to more cost-effectively scale autonomous fleets. This optimization of costs also improves the economics of autonomous ride-hailing models in vehicle deployment and operation costs. Therefore, these factors reduce part cost is enabling the conditions for wider commercialization and sustained energy for a robo taxi service.

Drivers & Opportunities

What are the Factors Driving the Market Growth?

Rising Urbanization: The emergence of new urban and sub-urban areas poses a challenge to the transportation systems, driving the demand. Increase in urban population intensifies in traffic density, traffic congestion, and parking shortage, making it difficult for conventional transportation model to cope. According to World Bank data, urban population reached 4.69 million in 2024. The emergence of new urban and sub-urban areas poses a challenge to the transportation systems, driving the demand for robo taxi market. Increase in urban population intensifies in traffic density, traffic congestion, and parking shortage, making it difficult for conventional transportation model to cope. Robo taxi services provide a flexible and shared mobility solution that can contribute to enhancing vehicle utilization and decreasing number of public and privately-owned vehicles circulating on roads. Autonomous ride-hailing services are well suited particularly in dense urban areas with high demand for frequent, short-distance trips. 6 Robo taxis can bring about improved transportation efficiency in general, by allowing for efficient route planning, dynamic fleet management, and 24/7 operation with no driver limitations. Moreover, urban dwellers have an increasing preference for MàS solutions which reduce carownership. Therefore, with city growth prioritizing smart mobility solutions, robo taxis are becoming a key element of tomorrow’s urban transport systems.

Government Push Towards Greener Alternatives: This is due to several autonomous mobility platforms which are being developed based on electric vehicle designs in recognition of broader policy objectives with reducing greenhouse gases and urban air pollution. Authorities are providing more backing for low emission transport via legislative frameworks, urban mobility plans, and environmental targets. Electric powertrain-based and shared service-integrated remote-operated and driverless taxi systems may have a strong impact on reducing per-passenger emissions and energy consumption in urban transport. For example, in February 2026, Waymo raised USD 16 million, a valuation of USD 126 million. The company reported the reduction in serious injury crashes compared to human drivers was 90% with 127 million autonomous miles under its belt. Moreover, autonomous fleet management also enables, optimized driving styles, and routes, which significantly reduces fuel or energy consumption. Autonomous ride-hailing services are becoming the technology solution to contribute to longer term environmental and transportation goals This is due to legislators starting to focus more on these clean mobility systems lawmakers, and now with how these solutions are clean and sustainable looking forward.

Source: Polaris Market Research Analysis

Segmental Insights

Which Segments Contributed to the Market Expansion?

Propulsion Type Analysis

Based on propulsion type, the segmentation includes electric vehicles, hybrid electric vehicles, fuel cell vehicle. The electric vehicle segment accounted for 69.4% revenue share in 2025. This is owing to the operational aspects of an autonomous mobility service model which are much better suited to the electric vehicle than the other types of vehicles. Robo taxi fleets take advantage of electric vehicles because of their lower operating costs, simpler drive train architecture, and decreased maintenance needs comparative to traditional vehicles. Electric platforms are also well-suited for autonomous driving due to their support for sophisticated electronic control and centralized computing. Furthermore, increasing focus on sustainable mobility and green transportation is positioning electric vehicles as an attractive option for autonomous fleet providers. With the ability to support high-utilization vehicles, and also with improvements in battery efficiency and charging technology, electric vehicles are increasingly well suited to high-tempo robo taxi operation in urban mobility systems.

Component Type Analysis

In terms of component type, the segmentation LiDAR, radar, camera, sensor. The camera segment is expected to witness the fastest growth during the forecast period at a CAGR of 94.7%. This is essential to facilitate visual appearance and environmental knowledge in self-driving automobiles. High resolution images taken by cameras enable robo taxi to recognize lane markings, traffic signals, pedestrians, and other vehicles on the road with high precision. In contrast to many other sensing modalities, cameras are cost effective and can be conveniently embedded into vehicle architectures at various locations to capture a holistic field of view. Advances in computer vision and deep learning software have dramatically increased the complexity of driving scenes that can be understood by camera systems. With the increasing reliance of autonomous systems on data-driven perception models, camera-based sensing is emerging as a key technology to improve the navigation accuracy and safety of robo taxis systems.

Level of Autonomy Analysis

Based on level of autonomy, the segmentation includes level 4 and level 5. The level 4 segment held the largest market value of USD 360.93 million in 2025. This is due to this level of autonomous which is driving a more technology focus and business feasible stage. Level 4 vehicles also operate without the need for a human or human backup driver whereas Level 3 vehicles require a human driver to be present and able to take control of the vehicle. This regulated autonomy regime enables developers to roll out robo taxi services in select markets while maintaining high levels of safety and reliability. The technology needed for Level 4 systems is closer at least in part due to recent improvements in sensors, artificial intelligence, and mapping. Hence, quite a few autonomous mobility platforms focus on the Level 4 deployment models, as they permit immediate real-world operations and at the same time develop a full autonomous solution for broader use in the future.

Source: Polaris Market Research Analysis

Regional Analysis

How Regions Affected the Overall Market Revenue?

North America Robo Taxi Market

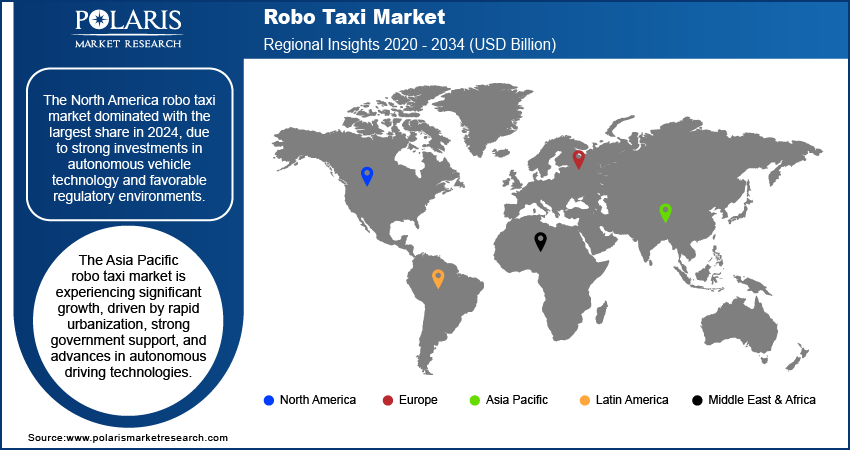

North America led the global market in 2025, holding a 72.2% revenue share. This is driven by a strong technological base and relatively early market introduction for solutions based on autonomy in the region. The existence of advanced research centres in AI, autonomous driving software, and vehicle-sensing technology has enabled an unprecedented pace of development and testing of the robo taxi concept. In addition, advanced digital infrastructure and high smart mobility scheme investments also contribute to enabling AV uptake within urban transport systems. The region also has a mature ride-hailing business and consumers who are highly receptive to mobility services provided through apps, both of which are positive signs for the region’s offerings in autonomous ride-hailing. Progress in development of autonomous vehicle software and abundant capital in mobility technologies in the U.S. will also further build the foundation for robo taxi in the near future. According to an April 2024 World Economic Forum report, the U.S. is expected to be the largest market for autonomous trucks, with up to 30% of new trucks sold in the U.S. by 2035. It is also a center for research, demonstration projects, and technology development for autonomous vehicles and next-generation transportation systems.

Asia Pacific Robo Taxi Market

The robo taxi landscape in Asia Pacific is projected to witness the fastest growth during the forecast period at a CAGR of 93.1%. This is due to the growing urbanization, developing digital infrastructure, and high technological penetration in the region including major economies. The growing urbanization and population pressure in meta cities is giving rise to space for high yielding transportation, generating demand for autonomous ride-hailing. The emergence of smart transportation ecosystems, based on connected vehicles that interact with intelligent traffic management systems, and other advanced mobility systems, is also being witnessed in the region. In 2023, World Economic Situation and Prospects stated a company in Liuzhou, China merged 5G, C-V2X, cloud computing, and roadside perception to achieve unmanned logistics on public roads in June 2021. Ten test vehicles covered more than 16,000 kilometers. Furthermore, the rapid development of AI, robotics and smart mobility in China is driving the formation of technologies for autonomous vehicles. The country also has the advantage of large urban areas and rapid digital transformation, allowing for the testing of autonomous mobility solutions and the scaling for use in metro transportation networks.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

Some of the major corporations participating in the robo taxi industry include: Aptiv; Baidu, Inc.; Didi Chuxing Technology Co., Ltd.; Lyft, Inc.; Pony AI; Tesla Inc.; Uber Technologies Inc.; Waymo LLC; WeRide.ai; Zoox, Inc. The competing companies in the robo-taxi industry are technological giants, car manufacturers and ride-hailing companies. While Waymo is ahead in terms of operational experience and fully driverless miles, Tesla is trying to get volume with its vision-only approach and existing fleet of EVs. Baidu’s Apollo Go dominates China, followed by Pony.ai, WeRide, and Didi, each with local partnerships and regulatory access. Zoox (Amazon) and Aptiv (via Motional) concentrate on tailored, bidirectional ones. Uber and Lyft capitalize on their ride-share networks, but depend on third-party AV technology (Uber with Waymo and Motional). Important differentiators: safety record, unit cost, geography expansion, and regulatory approach. Competition will also likely come from partnerships e.g., Lyft with Mobileye and vertical integration. The market is still pre-profit with 2025-2027 considered as the commercialization tipping point.

Key Players

- Aptiv

- Baidu, Inc.

- Didi Chuxing Technology Co., Ltd.

- Lyft, Inc.

- Pony AI

- Tesla Inc.

- Uber Technologies Inc.

- Waymo LLC

- WeRide.ai.

- Zoox, Inc.

Industry Developments

- February 2026: Baidu, Uber and Dubai’s RTA collaborated to bring Baidu’s Apollo Go autonomous ride-hailing service to the Uber platform in Dubai. Beginning in Jumeirah, fully driverless vehicles will be accessible via the Uber app, helping Dubai achieve its target of 25% driverless journeys by 2030. (Source: Uber Investor)

- January 2026: Aptiv introduced intelligent edge solutions that bring real-time sensing, thinking, and acting to devices, featuring an AI-based ADAS platform for L2++ hands-free driving. The full stack system enhances perception and behavior planning based on real-world driving data for use in transport and robotics applications. (Source: Aptiv)

Robo Taxi Market Segmentation

By Propulsion Type Outlook (Revenue, USD Million, 2021–2034)

- Electric Vehicles

- Hybrid Electric Vehicles

- Fuel Cell Vehicle

By Component Type Outlook (Revenue, USD Million, 2021–2034)

- LiDAR

- Radar

- Camera

- Sensor

By Level of Autonomy Outlook (Revenue, USD Million, 2021–2034)

- Level 4

- Level 5

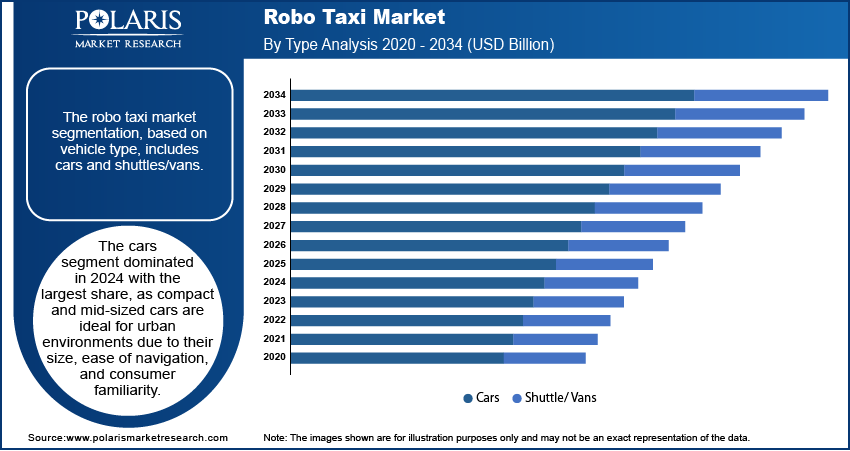

By Vehicle Type Outlook (Revenue, USD Million, 2021–2034)

- Cars

- Shuttles/Vans

By Service Type Outlook (Revenue, USD Million, 2021–2034)

- Car Rental

- Station-Based

By Application Outlook (Revenue, USD Million, 2021–2034)

- Passenger

- Goods

By Regional Outlook (Revenue, USD Million, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Robo Taxi Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 486.75 million |

| Market Size in 2026 | USD 938.20 million |

| Revenue Forecast by 2034 | USD 179, 420.81 million |

| CAGR | 92.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Robo Taxi Market FAQ's

The global market size was valued at USD 468.75 million in 2025 and is projected to grow to USD 179,420.81 million by 2034.

The global market is projected to register a CAGR of 92.8% during the forecast period.

North America led the global market in 2025, holding a 72.2% revenue share.

A few of the key players in the market are Aptiv; Baidu, Inc.; Didi Chuxing Technology Co., Ltd.; Lyft, Inc.; Pony AI; Tesla Inc.; Uber Technologies Inc.; Waymo LLC; WeRide.ai; Zoox, Inc.

The electric vehicle segment accounted for 69.4% revenue share in 2025.

The camera segment is expected to witness the fastest growth during the forecast period at a CAGR of 94.7%.

Download Sample Report of Robo Taxi Market

Please fill out the form to request a customized copy of the research report.