Scar Treatment Market Demand, Trends, Industry Analysis Report, 2025 - 2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Scar Treatment Market Summary

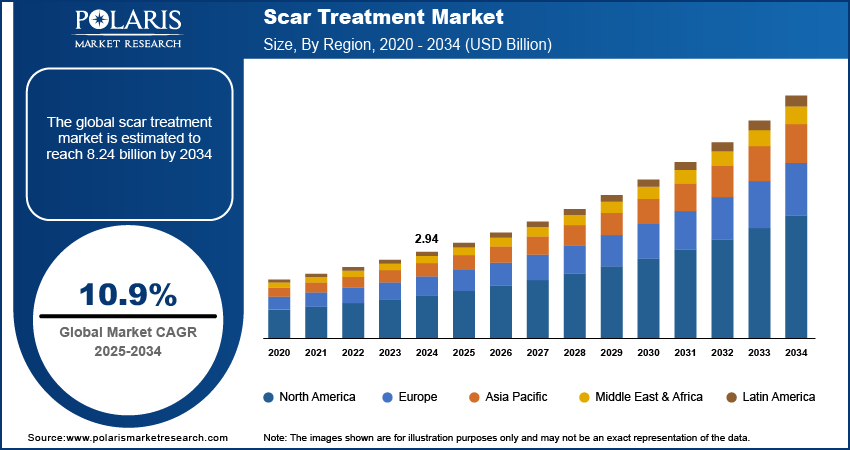

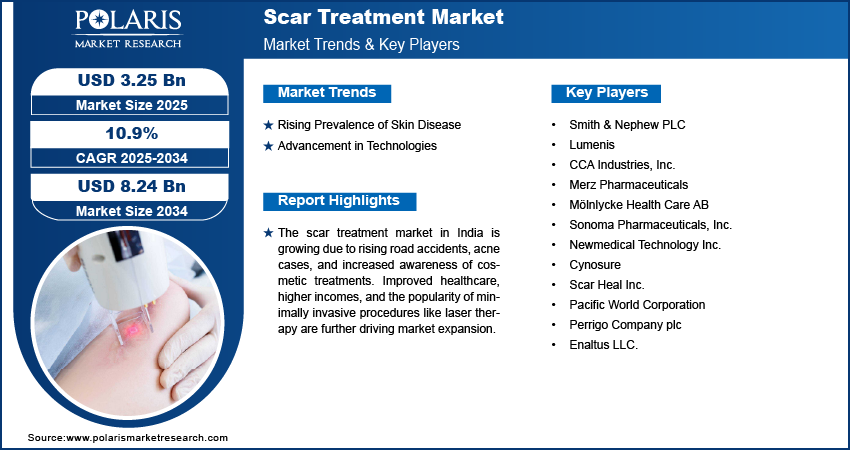

Scar treatment market size was valued at USD 2.94 billion in 2024. It is projected to grow from USD 3.25 billion in 2025 to USD 8.24 billion by 2034, exhibiting a CAGR of 10.9% during the forecast period.

Market Statistics

Scar treatment is a medical procedure aimed at improving the appearance of scars. It involves techniques designed to minimize the visibility of scars, reduce discomfort, and restore normal skin texture to enhance their appearance and improve overall quality of life significantly.

The scar treatment market growth is driven by the rising incidence of road accidents, burn injuries, and various skin-related issues. These issues include post-surgical scars, acne, stretch marks from pregnancy or weight fluctuations, and burn marks, all of which contribute to the formation of scars. Acne, a prevalent dermatological condition, significantly affects many individuals, leading to scar formation. Addressing these conditions drives the adoption of scar treatment, supporting market growth.

To Understand More About this Research: Download Sample Report

The market is growing due to technological advancements that make treatments more effective and affordable. New technologies, such as microdermabrasion and silicone-based products, are improving the results of scar treatments while reducing costs. These innovations help to improve healing, reduce scarring, and offer faster recovery times, making treatments more cost-effective. Additionally, the development of over-the-counter scar treatment products allows for at-home care, further driving scar treatment market value.

Scar Treatment Market Dynamics

Rising Prevalence of Skin Disease

The increasing prevalence of skin diseases is driving the market growth. Pollution, exposure to radiation, and other factors are driving this prevalence of skin diseases. For instance, according to the National Library of Medicine, skin conditions affect around 85% of individuals aged 12 to 24, showcasing an increase in prevalence. Common conditions such as photoaging, psoriasis, vitiligo, and eczema are often caused by excessive UV exposure and pollution, leading to reduced skin elasticity and various skin issues. These conditions can result in persistent scars, thereby boosting the scar treatment market demand.

Growing Adoption of Minimally Invasive Surgeries

The growing adoption of minimally invasive surgeries is driving the scar treatment market expansion. Minimally invasive procedures, which include techniques such as laser treatments, have become increasingly popular due to their numerous benefits over traditional surgical methods. These benefits include smaller incisions, reduced risk of infection, less post-operative pain, and faster recovery times. Consequently, more patients are opting for these advanced treatments, leading to an increase in surgical procedures overall.

For instance, according to the American Society of Plastic Surgeons, cosmetic procedures through minimally invasive techniques increased by 19% in 2022 from 2019, showcasing an increase in the adoption of minimally invasive surgeries.

Scar Treatment Market Segment Analysis

Scar Treatment Market Assessment by Product Outlook

The scar treatment market segmentation, based on product, includes topical products, laser products, injectables, and others. In 2024, the topical products segment held the largest market share globally due to the over-the-counter (OTC) availability of topical creams, gels, and silicone sheets, which provide accessible options for scar treatment. These products, offer a non-invasive approach and can be applied directly to the skin. They eliminate the need for physician visits, making them a convenient choice, which is boosting the demand for topical products, thereby driving segmental growth in the global market

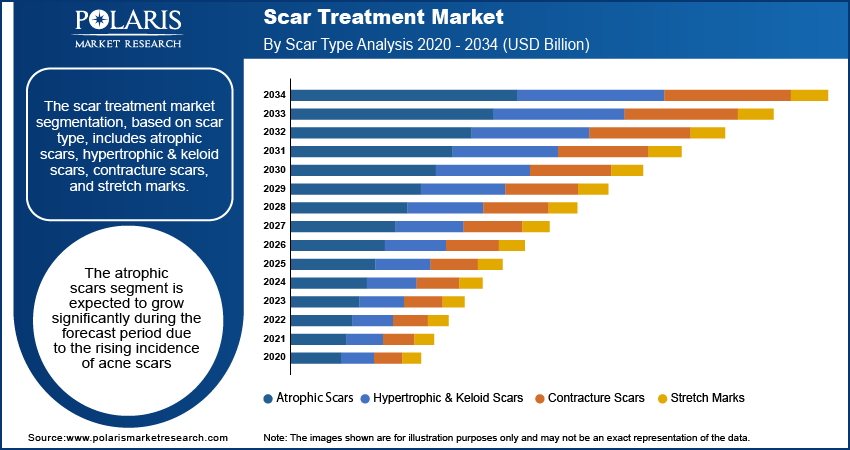

Scar Treatment Market Evaluation by Scar Type Outlook

The scar treatment market segmentation, based on scar type, includes atrophic scars, hypertrophic & keloid scars, contracture scars, and stretch marks. The atrophic scars segment is expected to grow significantly during the forecast period due to the rising incidence of acne scars. Atrophic scars, which appear as depressions or indentations on the skin, are a common result of severe acne. Incidents of acne continue to affect a large portion of the global population, especially among teenagers and young adults, and the demand for treatments to reduce or eliminate these scars is increasing. This growing need for effective solutions to treat atrophic scars is fueling the segmental growth in the global market.

The hypertrophic and keloid scar segment is also expected to grow during the forecast period. This growth is driven by an increase in traumatic wounds, surgical procedures, burn injuries, and rising road accident cases, which in turn is driving the demand for scar treatment for hypertrophic and keloid scars.

Scar Treatment Market Regional Insights

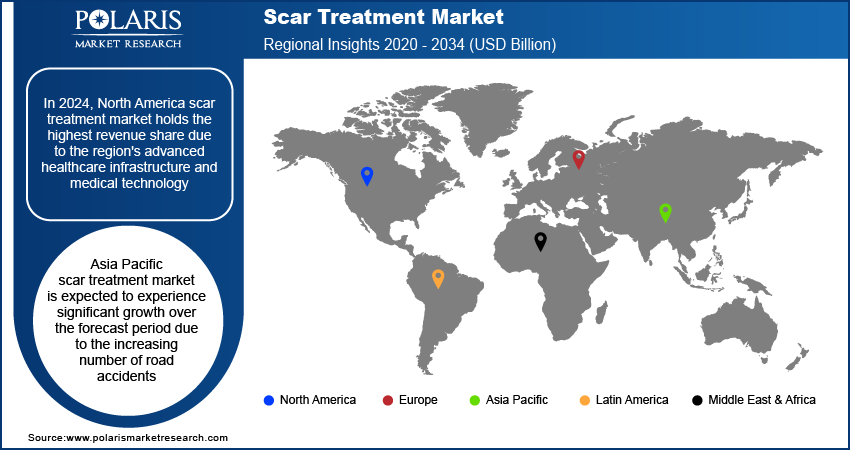

By region, the study provides the scar treatment market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2024, North America dominated the market due to the region's advanced healthcare infrastructure and medical technology. This improves access to innovative wound care and primary treatments. Additionally, the high incidence of skin conditions, traumatic injuries, and cosmetic concerns is fueling the demand for scar treatment. For instance, according to the American Burn Association, the US alone records 450,000 serious burn injuries annually, showcasing a large volume of skin incidents. Growing awareness of scar management and cosmetic improvements further boosts market growth in North America.

The scar treatment market in Asia Pacific is expected to experience significant growth over the forecast period due to the increasing number of road accidents, leading to a higher incidence of traumatic injuries that result in scars. In countries such as India, China, and Southeast Asia, where road traffic accidents are prevalent, the demand for scar treatments is rising. For instance, according to the Indian Ministry of Road Transport and Highways, in India alone, injuries due to road accidents rose by 15% in 2022 compared to 2021, showcasing an increase in the number of fatal injuries. People are increasingly seeking effective solutions to manage and reduce scars caused by accidents, thus boosting the market for scar treatment products and services in this region.

The scar treatment market in India is growing significantly due to a combination of factors, including the rising number of road accidents, increasing cases of skin conditions such as acne, and a greater awareness of cosmetic surgery. Expanding healthcare infrastructure and rising disposable incomes have led people to advanced solutions for scar removal and skin repair. Additionally, the growing popularity of minimally invasive procedures and treatments, such as laser therapy and silicone gels, is contributing to the market expansion in the country.

Scar Treatment Market Key Market Players & Competitive Analysis Report

The scar treatment industry is constantly evolving, with numerous companies striving to innovate and distinguish themselves. Leading global corporations dominate the market by leveraging extensive research and development, and advanced techniques. These companies pursue strategic initiatives such as mergers, acquisitions, partnerships, and collaborations to enhance their product offerings and expand into new markets.

New companies are impacting the industry by introducing innovative products to meet the demand of specific market sectors. Continuous progress in product offerings amplifies this competitive environment. Major players in the market include Smith & Nephew PLC; Lumenis; CCA Industries, Inc.; Merz Pharmaceuticals; Mölnlycke Health Care AB; Sonoma Pharmaceuticals, Inc.; Newmedical Technology Inc.; Cynosure; Scar Heal Inc.; Pacific World Corporation; Perrigo Company plc; and Enaltus LLC.

Smith & Nephew PLC is a British medical technology company headquartered in Watford, England. Established in 1856, it specializes in the development, manufacturing, and marketing of medical devices and services that focus on the repair, regeneration, and replacement of soft and hard tissues. The company operates through three primary segments, which include orthopedics, sports medicine & ENT, and advanced wound management. In the orthopedics segment, Smith & Nephew offers a wide range of hip and knee implants designed to replace diseased or damaged joints alongside robotics-assisted technologies for surgical precision during procedures. The sports medicine & ENT segment provides products and instruments for minimally invasive surgeries, particularly for sports medicine specialists and ENT professionals. Meanwhile, the advanced wound management segment contains products aimed at addressing complex wound care needs. Smith & Nephew’s operations span globally, with a presence in over 100 countries. Its key markets include North America, which is crucial for its orthopedic products; Europe, where it has a stronghold in advanced wound management; and Asia Pacific, which is an expanding market for all its segments.

Merz Pharmaceuticals GmbH develops pharmaceutical treatments for neurological, psychiatric, and neuromuscular conditions. The company also provides solutions for scars, acne, hair loss, and fungal diseases. Serving a global customer base, Merz Pharmaceuticals is dedicated to advancing medical aesthetic treatments. In April 2023, Merz Therapeutics finalized an asset purchase agreement with a US-based biotech firm. This investment represents Merz's second acquisition of a NASDAQ-listed company in over a decade.

Key Companies in Scar Treatment Market

- Smith & Nephew PLC

- Lumenis

- CCA Industries, Inc.

- Merz Pharmaceuticals

- Mölnlycke Health Care AB

- Sonoma Pharmaceuticals, Inc.

- Newmedical Technology Inc.

- Cynosure

- Scar Heal Inc.

- Pacific World Corporation

- Perrigo Company plc

- Enaltus LLC.

Scar Treatment Market Developments

March 2025: Mölnlycke Health Care AB unveiled a notable study during the 35th European Wound Management Association Conference in Barcelona. Findings demonstrated that transitioning chronic wound patients to Mepilex Border Flex, along with enhanced clinician training, led to fewer dressing changes, reduced treatment costs, and improved overall patient outcomes.

August 2024: Sonoma Pharmaceuticals has partnered with a global distributor to enhance wound care product distribution in the US.

Scar Treatment Market Segmentation

By Product Outlook (Revenue USD Billion, 2020–2034)

- Topical Products

- Creams

- Gels

- Silicon Sheets

- Others

- Laser Products

- CO2 Laser

- Pulse-dyed Laser

- Others

- Injectables

- Others

By Scar Type Outlook (Revenue USD Billion, 2020–2034)

- Atrophic Scars

- Hypertrophic & Keloid Scars

- Contracture Scars

- Stretch Marks

By End Use Outlook (Revenue USD Billion, 2020–2034)

- Hospitals

- Clinics

- Homecare

By Regional Outlook (Revenue USD Billion, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Scar Treatment Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2024 | USD 2.94 billion |

| Market Size Value in 2025 | USD 3.25 billion |

| Revenue Forecast in 2034 | USD 8.24 billion |

| CAGR | 10.9 % from 2025 to 2034 |

| Base Year | 2023 |

| Historical Data | 2020 – 2023 |

| Forecast period | 2025 – 2034 |

| Quantitative units | Revenue in USD billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global scar treatment market size was valued at USD 2.94 billion in 2024 and is projected to grow to USD 8.24 billion by 2034.

The global market is projected to grow at a CAGR of 10.9% during the forecast period, 2025-2034.

North America had the largest share of the global market.

The key players in the market are Smith & Nephew PLC; Lumenis; CCA Industries, Inc.; Merz Pharmaceuticals; Mölnlycke Health Care AB; Sonoma Pharmaceuticals, Inc.; Newmedical Technology Inc.; Cynosure; Scar Heal Inc.; Pacific World Corporation; Perrigo Company plc; and Enaltus LLC.

The topical Products segment held the largest market share the market in 2024, due to the availability of over-the-counter (OTC)

The atrophic scars segment is expected to grow significantly during the forecast period due to the rising incidence of acne scars.

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research & Consulting, Inc. uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

1. Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

2. Data Collection

We gather information from both public and verified sources:

3. Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

| Region | Segment | VolumeUnits | Avg PriceUSD | RevenueUSD Mn | Share % |

|---|---|---|---|---|---|

| North America | Product A | 250 | 2.5 | 500 | 15% |

| Product A | XX | XX | XX | XX | |

| Product A | XX | XX | XX | XX | |

| Consistent methodology applied across regions | |||||

4. Market Estimation

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Forecasting

Step 6:

At Polaris Market Research & Consulting, Inc., we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Validation & Triangulation

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Triangulation Framework

Estimates are cross-verified across three sources:

Company-level data

• Primary inputs from industry participants

• Secondary benchmarks and published data

Variance maintained within +5-10%

Adjustments applied to align estimates

Segment values validated against overall market structure

Data Consistency & Integrity

Segment totals validated to 100%

Regional estimates aligned with global market size

Historical trends compared against forecast outputs

Assumptions reviewed for cross-segment and regional alignment

Final Outputs

Deliverables

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements

Download Sample Report of Scar Treatment Market Demand, Trends, Industry Analysis Report, 2025 - 2034

Please fill out the form to request a customized copy of the research report.