Security Posture Management Market Size, Growth, Global Industry Report 2026-2034

REPORT DETAILS

Security Posture Management Market Summery

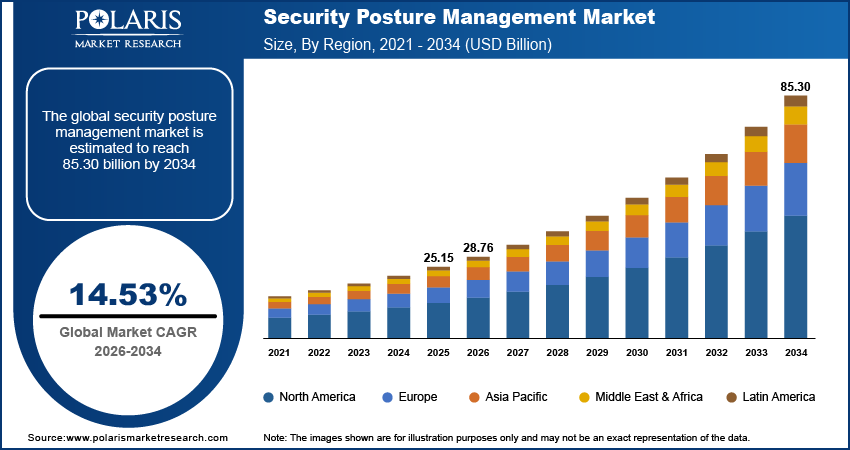

The global security posture management market is estimated around USD 25.15 billion in 2025,?with consistent growth anticipated during 2026–2034. Growth is supported by rising cyber threat frequency, rapid cloud and hybrid infrastructure adoption, and increasing regulatory compliance requirements. The market is projected to grow at a CAGR of 14.53% during the forecast period.

Market Statistics

Key Takeaways

- North America accounted for the largest regional share of around 39.4% in 2025, driven by widespread cloud adoption, strong cybersecurity regulatory frameworks, and increasing enterprise investments in zero-trust and multi-cloud security infrastructure.

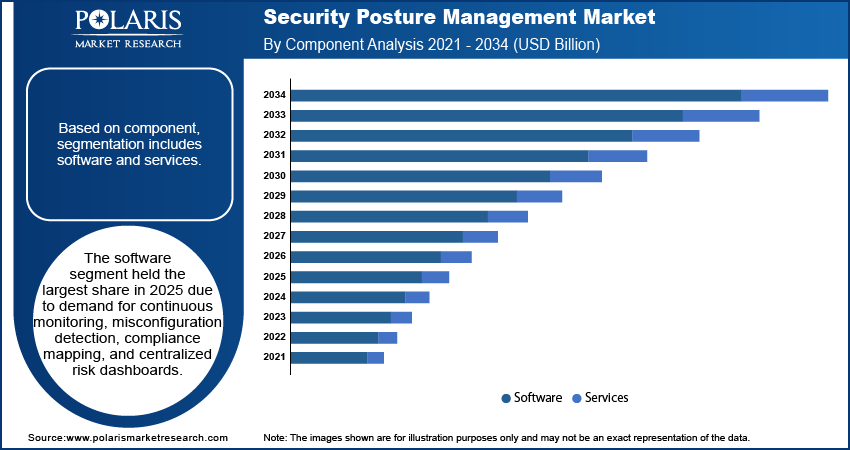

- By Component, Software segment accounted for the largest share of approximately 63.2% in 2025, supported by rising demand for automated configuration monitoring, real-time risk visibility, compliance mapping, and continuous misconfiguration detection.

- By Deployment, Cloud segment accounted for the largest share of around 66.7% in 2025, driven by growing adoption of SaaS-based platforms providing centralized visibility and protection across multi-cloud environments.

- By Enterprise Size, Large Enterprises segment accounted for the largest share of nearly 69.1% in 2025, supported by complex IT infrastructures, strict regulatory requirements, and the need for centralized security posture visibility.

- By Industry Vertical, BFSI segment accounted for the largest share of around 28.6% in 2025, driven by stringent compliance requirements, protection of high-value financial data, and rising cyberattack risks targeting financial institutions.

Industry Dynamics

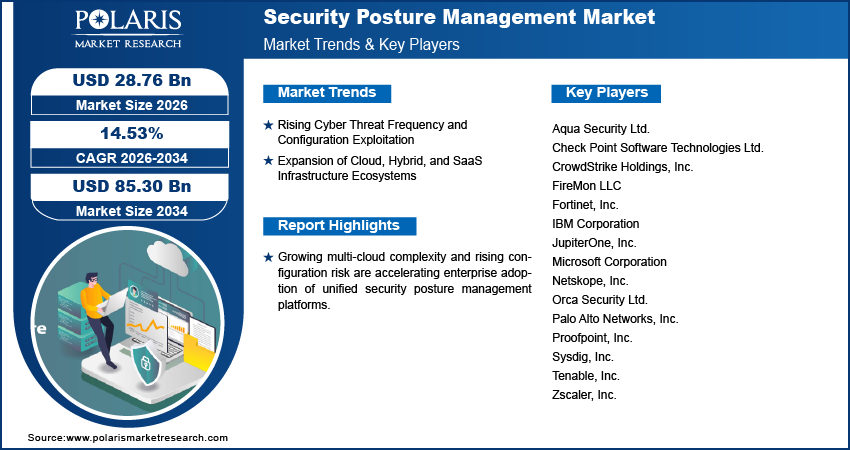

- Escalating ransomware, credential abuse, and cloud misconfiguration incidents are increasing demand for continuous posture monitoring platforms.

- Expansion of multi-cloud and vSaaS ecosystems is strengthening adoption of unified security posture management frameworks.

- Budget prioritization toward detection and response tools can delay posture platform procurement among mid-sized enterprises.

- Automation in cybersecurity and predictive maintenance risk analytics are creating long-term scalability opportunities across the SPM ecosystem.

Why Security Posture Management Matters in the Circular Economy

The security posture management market comprises platforms that deliver continuous visibility, risk assessment, and remediation oversight across security controls, configurations, identities, assets, and compliance frameworks. It spans multiple posture domains introduced at the outset: cloud security posture management (CSPM), SaaS security posture management (SSPM), data security posture management (DSPM), identity security posture management (ISPM), and broader cybersecurity posture management market structures. The global security posture management industry centers on risk quantification, misconfiguration detection, and policy validation across hybrid and multi-cloud environments.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Drivers & Opportunities

Increase in Cyber Threats: The increase in phishing, ransomware, and identity attacks is driving the vulnerability to misconfiguration and privilege risk management. In Q1 2025, the Anti-Phishing Working Group (APWG) recorded 1,003,924 phishing attacks, which is the highest recorded in a quarter since the end of 2023, indicating the severity of the threat that is credential-focused. With attackers targeting misconfigured cloud resources and unnecessary access privileges, organizations need constant visibility into endpoints, SaaS applications, identities, and cloud workloads. This trend is fueling C-level interest in monitoring, risk assessment, and compliance alignment, which is directly fueling the adoption of the security posture management market.

Acceleration of Cloud and Hybrid Infrastructure Adoption: The adoption of the cloud is accelerating the attack surface of the business. According to the United Nations Department of Economic and Social Affairs E-Government Survey 2024, 44% of the nations in the world have adopted cloud computing to facilitate digital infrastructure. The adoption of the cloud, multi-cloud, and hybrid models is unmanaged. The lack of managed security posture tends to increase the risk of misconfiguration. As enterprises aim to manage the environment, the demand in the security posture management market gets strengthened.

Restraints & Challenges

Budget Constraints and Security Spending Prioritization: Budgets for security will always be limited, and this is particularly true for mid-sized firms that must balance their digital transformation budget. While posture management is a long-term risk reducer, it can be difficult to quantify the immediate ROI in relation to threat detection and response tools. Budget constraints, therefore, temper growth in the security posture management market for certain segments.

Opportunity

Automation in Security Posture Management: The increasing complexity of configurations drives the need for remediation and enforcement by automation. Human resources security audits cannot keep up with the ever-changing nature of cloud infrastructure. Automation in SPM enables continuous scanning, auto-remediation, and real-time compliance reporting. This makes human intervention unnecessary and allows for faster remediation of misconfigurations. As infrastructure continues to become more transient, posture management by automation is ready to be a major growth driver.

Predictive Risk Analytics and Proactive Security Modeling: Enterprises are moving from reactive compliance verification to predictive risk forecasting. Predictive risk analytics relies on behavioral patterns, threat intelligence, and historical incident data to identify high-probability exposure points before they are exploited. The incorporation of predictive models into SPM solutions improves the accuracy of prioritization and executive reporting. This development will transform posture management from a visibility solution to a predictive risk forecasting engine, unlocking new market potential.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the security posture management market by component, deployment model, enterprise size, industry vertical to help readers identify the fastest expanding and most attractive demand segments.

By Component

-

Software

The security posture management software market accounts for the largest revenue share. Organizations are engaged in continuous configuration monitoring, automated misconfiguration detection, compliance mapping, and risk management dashboards. Software tools enable real-time visibility into cloud workloads, identities, endpoints, and infrastructure resources.

-

Service

The SPM services market is growing at the quickest rate, driven by talent shortages and increasing threat complexity. Managed SPM services enable organizations to offload monitoring, remediation, and policy tuning.

By Deployment Model

-

Cloud-Based Deployment

The cloud security posture management market is the largest and fastest-growing deployment type. This is due to organizations are focusing on SaaS-based SPM solutions to manage their cloud-native environments. The multi-cloud security posture management feature is becoming a basic necessity because organizations are operating in the AWS, Azure, and Google Cloud environments.

-

On-Premise Deployment

The on-premise SPM market is still applicable in the highly regulated sectors and legacy IT environments. Organizations with strict data sovereignty or defense-grade infrastructure needs continue to use localized posture management solutions.

-

Hybrid Deployment

The hybrid deployment SPM solutions are used in scenarios where legacy systems and cloud workloads co-exist. The solutions offer a single point of visibility for the distributed assets. The adoption rate is steady but in a transition phase, which in most cases precedes a full cloud migration strategy.

By Enterprise Size

-

Large Enterprise

Large enterprise SPM adoption is at the forefront of the market due to the complexity of IT environments and increasing exposure to regulations. These enterprises need enterprise risk visibility platform market solutions that have the ability to correlate posture information for thousands of assets.

-

SMEs

SME cybersecurity posture management adoption is increasing at a rapid pace as SMEs are increasingly targeted by ransomware attacks and supply chain attacks. The cloud-first business model of SMEs is promoting the adoption of SaaS-based SPM solutions.

By Industry Vertical

-

BFSI

The BFSI industry vertical has the highest adoption of SPM solutions. The BFSI industry is under constant regulatory oversight, with stringent data protection regulations and high financial risk exposure.

-

Healthcare

The demand for SPM in the healthcare industry is increasing owing to the protection of sensitive patient data and the growing number of ransomware attacks on hospitals. Posture management solutions help protect electronic health records and medical devices.

-

Government & Defense

Cybersecurity posture management for the government is growing rapidly as part of the country’s cybersecurity modernization efforts. There is a constant need to monitor classified and sovereign data systems for defense and public infrastructure networks. Momentum in zero-trust investment continues to fuel growth.

-

IT & Telecom

SPM in the IT & telecom industry is driven by distributed network architecture, 5G networks, and cloud-native service platforms. The industry uses SPM solutions to mitigate risks in virtualized infrastructure.

-

Manufacturing

The SPM industry in manufacturing is focused on industrial control system security and protected production environments. With the growing adoption of Industry 4.0, there is a need for posture visibility in operational technology networks.

Source: Polaris Market Research Analysis

Regional Analysis

North America Security Posture Management Market Assessment

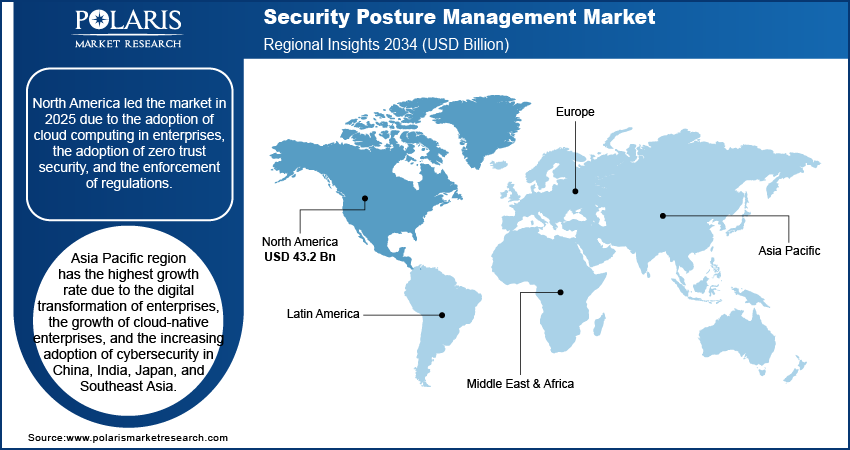

North America security posture management market maintained the largest market share due to the extensive enterprise integration of posture visibility solutions and the mandated zero trust strategy. Enterprises adopted SPM solutions to monitor misconfigurations, maintain policy baselines, and protect growing multi-cloud environments. In the US, the increasing adoption of cloud infrastructure and the rising interest in cybersecurity regulations accelerated procurement cycles in the financial services, healthcare, and government industries. In October 2025, Tempo Software introduced modular SPM Collections in its Adaptive SPM solution, enabling enterprises to incrementally enhance posture management. This further reinforced the market size for security posture management solutions.

Asia Pacific Security Posture Management Market Insight

The growth in the management of Asia Pacific security posture outpaced other regions due to the accelerated digital transformation and the increase in cloud-native enterprises in China, India, Japan, and Southeast Asia. The trend towards hybrid and multi-cloud environments increasing vulnerability to configuration drift, thereby increasing the need for automated compliance monitoring and risk orchestration. Digitization and AI-driven service expansion by governments improved the security budgets of enterprises. According to the Data Security Council of India, India had more than 400 cybersecurity product companies in 2025, generating USD 4.46 billion in combined revenue. The maturity of the ecosystem above reflected the improving trends in cybersecurity investments in the region and helped fuel the accelerated deployment of SPM.

Europe Security Posture Management Market Overview

Europe SPM market is influenced by the adoption trends that are largely driven by the enforcement of GDPR regulations and the pressure of data sovereignty. Organizations use posture management solutions to maintain readiness, global compliance, and policy consistency in their cloud architecture. The regulatory focus has heightened boardroom-level concern for cybersecurity risk, thereby solidifying the procurement of automated governance platforms. The investment in the market is driven by compliance rather than expansion, aligning with the risk management framework for data protection in Europe.

Middle East Security Posture Management Market Assessment

Middle East cybersecurity market moves forward with increasing investment in financial services and government infrastructure. Large-scale smart city projects and government digitization initiatives increase vulnerability to cloud misconfigurations and policy deviations, fueling the need for posture management solutions. Investment trends in the Middle East cybersecurity market show an increasing focus on centralized visibility solutions that can handle hybrid environments. While adoption is limited to high-value segments, growth momentum increases with stricter regulatory norms and increased enterprise cloud adoption.

Heat Map Analysis

| Region | Market Position | Growth Momentum | Regulatory Strength | Recycling Infrastructure | Secondary Lead Production Base |

| North America | Dominant | High | Very High | Low | Low |

| Asia Pacific | High | Very High | Medium | Low | Low |

| Europe | Medium–High | Medium | Very High | Low | Low |

| Middle East | Emerging | High | Medium | Low | Low |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

SPM vs CSPM vs DSPM vs SSPM vs ASPM vs ISPM

| Category | Primary Focus | Key Risk Addressed |

| SPM (Security Posture Management) | Unified security posture across cloud, identity, data, apps | Enterprise-wide misconfigurations & compliance gaps |

| CSPM (Cloud Security Posture Management) | Cloud infrastructure security | Cloud misconfigurations & compliance drift |

| DSPM (Data Security Posture Management) | Sensitive data discovery & protection | Data exposure & unauthorized access |

| SSPM (SaaS Security Posture Management) | SaaS application configurations | SaaS misconfigurations & third-party app risks |

| ASPM (Application Security Posture Management) | Application security lifecycle | Code vulnerabilities & release risks |

| ISPM (Identity Security Posture Management) | Identity & access controls | Privilege misuse & credential compromise |

Source: Polaris Market Research Analysis

Difference between SPM and CSPM:

CSPM focuses specifically on cloud configuration security, while SPM provides a broader, unified view that includes cloud, identity, data, SaaS, and applications.

What is DSPM?

DSPM helps in identifying, categorizing, and tracking sensitive data in the cloud and on-prem environments to minimize risk.

AI & Automation in Security Posture Management

Cybersecurity automation helps in continuous posture analysis and quick remediation. Advanced SPM solutions employ AI-powered predictive risk analysis to assess vulnerabilities, detect configuration drift, and point out privilege escalation threats. Automated policy enforcement, identity remediation, and misconfiguration rollback minimize manual effort. Integration with DevOps pipelines helps in shift-left security validation.

Future Outlook to 2034

- Convergence of CSPM, DSPM, SSPM, ASPM, and ISPM into unified SPM platforms.

- Wider adoption of zero trust security posture models.

- Increased reliance on predictive risk analytics for proactive threat prevention.

- Expansion of automated remediation frameworks with governance controls.

Security posture management is anticipated to mature into a centralized risk orchestration layer for cloud-native, AI-driven, and multi-identity enterprise environments.

Key Players & Competitive Analysis Report

The security posture management market is moderately concentrated, driven by a combination of global cybersecurity platform vendors and cloud-native security innovators competing on the basis of automation depth, cross-environment visibility, and AI-driven risk prioritization. Competitive dynamics vary across different groups of vendors. Full-platform vendors have incorporated SPM into holistic security solutions that include network, endpoint, and cloud security, thereby improving adoption and stickiness. Cloud-native and API-first vendors focus on agentless-based deployment, multi-cloud misconfigurations, and risk scoring, which place them advantageously in rapidly growing enterprise settings.

Among the key players that are currently influencing the global security posture management market include Aqua Security Ltd., Check Point Software Technologies Ltd., CrowdStrike Holdings, Inc., FireMon LLC, Fortinet, Inc., IBM Corporation, JupiterOne, Inc., Microsoft Corporation, Netskope, Inc., Orca Security Ltd., Palo Alto Networks, Inc., Proofpoint, Inc., Sysdig, Inc., Tenable, Inc., and Zscaler, Inc.

Key Players

- Aqua Security Ltd.

- Check Point Software Technologies Ltd.

- CrowdStrike Holdings, Inc.

- FireMon LLC

- Fortinet, Inc.

- IBM Corporation

- JupiterOne, Inc.

- Microsoft Corporation

- Netskope, Inc.

- Orca Security Ltd.

- Palo Alto Networks, Inc.

- Proofpoint, Inc.

- Sysdig, Inc.

- Tenable, Inc.

- Zscaler, Inc.

Industry Developments

- January 2026: Group-IB launched its Cloud Security Posture Management (CSPM) solution as part of the Unified Risk Platform to help organizations detect cloud misconfigurations, close compliance gaps, and strengthen overall cloud security.

- August 2025: Google Cloud previewed its Data Security Posture Management (DSPM) capabilities to help enterprises identify sensitive data risks and enforce security policies across cloud environments.

- September 2024: CrowdStrike unveiled new Falcon Cloud Security innovations that included expanded cloud threat detection, risk prioritization, and posture management capabilities across multi-cloud environments.

Security Posture Management Market Segmentation

By Component Outlook (Revenue, USD Billion, 2021-2034)

- Software

- Services

By Deployment Model Outlook (Revenue, USD Billion, 2021-2034)

- Cloud-Based Deployment

- On-Premise Deployment

- Hybrid Deployment

By Enterprise Size Outlook (Revenue, USD Billion, 2021-2034)

- Large Enterprises

- SMEs

By Industry Vertical Outlook (Revenue, USD Billion, 2021-2034)

- BFSI

- Healthcare

- Government & Defense

- IT & Telecom

- Manufacturing

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Security Posture Management Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 25.15 Billion |

| Market Size in 2026 | USD 28.76 Billion |

| Revenue Forecast by 2034 | USD 85.30 Billion |

| CAGR | 14.53% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Security Posture Management Market FAQ's

The global market size was valued at USD 25.15 billion in 2025 and is projected to grow to USD 85.30 billion by 2034.

North America leads due to the widespread adoption of cloud computing in enterprises, the mandated adoption of zero trust security, and the evolving cybersecurity regulations.

Large enterprises drive the market due to their complex IT environments and exposure to regulations, while the BFSI and government segments are the largest industry verticals.

Key companies include Aqua Security Ltd., Check Point Software Technologies Ltd., CrowdStrike Holdings, Inc., FireMon LLC, Fortinet, Inc., IBM Corporation, JupiterOne, Inc., Microsoft Corporation, Netskope, Inc., Orca Security Ltd., Palo Alto Networks, Inc., Proofpoint, Inc., Sysdig, Inc., Tenable, Inc., and Zscaler, Inc.

Cyber threats are becoming more advanced, multi-cloud environments are expanding, there is pressure to comply with regulations, automation in cybersecurity is increasing, and predictive risk analytics are in demand.

Download Sample Report of Security Posture Management Market

Please fill out the form to request a customized copy of the research report.