Semiconductor & IC Packaging Materials Market Overview 2024-2032

REPORT DETAILS

Semiconductor & IC Packaging Materials Market Summary

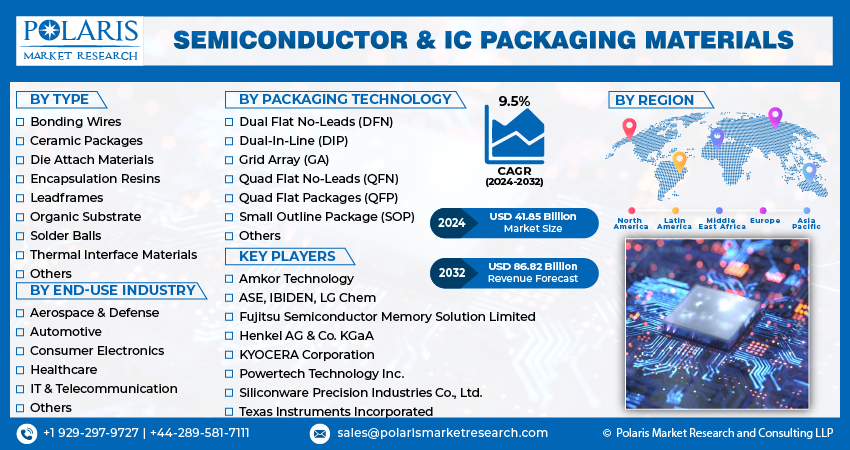

Global semiconductor & IC packaging materials market size was valued at USD 38.27 billion in 2023. The market is anticipated to grow from USD 41.85 billion in 2024 to USD 86.82 billion by 2032, exhibiting the CAGR of 9.5% during the forecast period

Market Statistics

Key Takeaways

- Asia Pacific dominated the market and contributed over 40% of the semiconductor & IC packaging materials market share in 2023

- By type, the organic substrate segment dominated the global semiconductor & IC packaging materials market size in 2023

- By end-use industry category, the consumer electronics segment accounted for the largest semiconductor & IC packaging materials market share

Industry Trends

Semiconductor and IC (Integrated Circuit) packaging materials are essential components used in the assembly and packaging of semiconductor devices, such as microchips and integrated circuits. These materials serve multiple purposes, including protecting the delicate semiconductor components from environmental factors such as moisture, dust, and physical damage, as well as providing electrical insulation and thermal management.

The Semiconductor & IC Packaging Materials Market encompasses a wide range of materials used in the assembly and packaging of semiconductor devices, playing a crucial role in ensuring their reliability, performance, and longevity. The market is driven by the rapid proliferation of semiconductor devices in various applications such as consumer electronics, automotive, telecommunications, and industrial automation. With the continuous evolution of semiconductor technology and the increasing demand for smaller, faster, and more powerful electronic devices, the need for advanced packaging materials with superior properties such as thermal conductivity, electrical insulation, and reliability is on the rise.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The market trends toward the growing demand for miniaturization and integration of semiconductor devices are leading to the development of advanced packaging solutions that offer higher performance and functionality in smaller form factors. Also, the increasing adoption of heterogeneous integration, which involves combining different semiconductor materials and technologies in a single package, is driving the need for versatile packaging materials capable of accommodating diverse device architectures.

The increasing demand for semiconductor devices across diverse end-use industries, including consumer electronics, automotive, healthcare, and telecommunications, is fueling demand for packaging materials to support the production of these devices. Similarly, technological advancements in semiconductor packaging techniques, such as flip-chip, wafer-level packaging, and through-silicon vias (TSVs), are driving the need for specialized packaging materials optimized for these advanced packaging processes. However, the market is hindered by the increasing cost and complexity of developing and manufacturing advanced packaging materials with superior properties and performance characteristics.

What are the market drivers driving the demand for the market?

The increasing demand for semiconductor devices is driving semiconductor & IC packaging materials market growth.

The increasing demand for semiconductor devices is significantly driving the market as industries such as consumer electronics, automotive, telecommunications, and industrial automation continue to integrate semiconductor technology into their products. The demand for packaging materials to support the production of these devices rises correspondingly. Semiconductor packaging materials play a crucial role in ensuring the performance and longevity of semiconductor devices by protecting them from environmental factors, providing electrical insulation, and managing thermal properties.

Also, as the demand for electronic devices with higher performance, increased functionality, and smaller form factors continues to grow, there is a parallel need for advanced packaging materials capable of meeting these evolving requirements. This market trend is expected to drive sustained semiconductor & IC packaging materials market growth as semiconductor manufacturers strive to meet the increasing demand for semiconductor devices across various industries.

Source: Polaris Market Research Analysis

Which factor is restraining the demand for Semiconductor & IC Packaging Materials?

The cost and complexity of advanced materials are hindering the semiconductor & IC packaging materials market growth.

Developing and manufacturing advanced packaging materials with superior properties and performance characteristics incur significant costs and require intricate processes. The complexity of these materials often translates into higher production expenses, making them less accessible to semiconductor manufacturers, particularly smaller players or those operating in cost-sensitive markets. Also, the intricacies of advanced materials require specialized equipment, expertise, and quality control measures, further adding to the overall complexity and cost of production. These factors act as barriers to adoption, limiting the widespread use of advanced packaging materials and hindering semiconductor & IC packaging materials market growth.

Report Segmentation

The market is primarily segmented based on type, packaging technology, end-use industry, and region.

| By Type | By Packaging Technology | By End-Use Industry | By Region |

|

|

|

|

Source: Polaris Market Research Analysis

To Understand the Scope of this Report:Request Customization

Category Wise Insights

By Type Insights

Based on type analysis, the market has been segmented on the basis of bonding wires, ceramic packages, die-attach materials, encapsulation resins, lead frames, organic substrate, solder balls, thermal interface materials, and others. In 2023, the organic substrate segment asserted its dominance in the market since they are made from materials such as laminate or fiberglass-reinforced epoxy resin, which are widely used in semiconductor packaging due to their excellent electrical insulation properties, thermal performance, and cost-effectiveness. These substrates serve as the foundation for mounting and interconnecting semiconductor chips, providing mechanical support and electrical connectivity within electronic devices.

Organic substrates also offer advantages such as lightweight, flexibility, and compatibility with high-density interconnect (HDI) technologies, making them well-suited for miniaturized and high-performance electronic applications. The increasing demand for compact and lightweight electronic devices, coupled with the growing adoption of advanced packaging techniques such as FOWLP and system-in-package, further drives the demand for organic substrates in the global market.

By Application Insights

Based on application category analysis, the market has been segmented on the basis of aerospace & defense, automotive, consumer electronics, healthcare, IT & telecommunication, and others. The consumer electronics segment accounted for the highest Semiconductor & IC Packaging Materials market share since consumer electronics, including smartphones, tablets, laptops, wearable devices, and home appliances, have witnessed exponential growth in demand. As consumer electronics become more sophisticated, compact, and feature-rich, the demand for semiconductor devices with higher performance, reliability, and miniaturization increases correspondingly.

Semiconductor packaging materials play a critical role in enabling the production of advanced semiconductor devices used in consumer electronics, providing essential functions such as electrical insulation, thermal management, and mechanical support. Also, the rapid pace of innovation and product development in the consumer electronics industry necessitates continuous advancements in semiconductor packaging materials to meet evolving performance requirements and cost considerations. As a result, the consumer electronics segment emerges as a dominant segment of the global market.

Source: Polaris Market Research Analysis

Regional Insights

Asia Pacific

The dominance of the Asia Pacific region is attributed to various factors that highlight the region's industry leadership. With countries like Japan, China, Taiwan, South Korea, and Singapore, the region boasts of several electronics manufacturing hubs that have a comprehensive presence of foundries, packaging facilities, equipment suppliers, and research institutions, creating an integrated and highly competitive market environment that fosters continuous innovation and technological advancement. This integration is particularly evident in countries like South Korea and Japan, which are renowned for their leadership in semiconductor research and manufacturing.

North America

The North American region is anticipated to experience substantial semiconductor & IC packaging materials market growth due to the presence of major players, coupled with significant investments in research and development, innovation, and technological advancements, which positions North America as a hub for semiconductor packaging materials development and production. Also, the region's strong focus on emerging technologies such as artificial intelligence, the Internet of Things, and 5G connectivity drives demand for advanced semiconductor devices with higher performance, reliability, and efficiency, further boosting the demand for innovative packaging materials.

Source: Polaris Market Research Analysis

Competitive Landscape

The competitive landscape for the market is characterized by intense competition among key players competing for market share and technological leadership. Major players in the market include prominent materials manufacturers such as Henkel AG & Co. KGaA, LG Chem, Siliconware Precision Industries Co., Ltd., and Kyocera Corporation, among others. These companies offer a diverse portfolio of packaging materials tailored to meet the stringent requirements of semiconductor packaging applications, including substrates, encapsulants, bonding wires, and thermal interface materials. Moreover, there is a growing presence of niche players and startups specializing in innovative materials and technologies to address specific market needs and emerging trends.

Some of the major players operating in the global market include:

- Amkor Technology

- ASE

- Fujitsu Semiconductor Memory Solution Limited

- Henkel AG & Co. KGaA

- IBIDEN

- KYOCERA Corporation

- LG Chem

- Powertech Technology Inc.

- Siliconware Precision Industries Co., Ltd.

- Texas Instruments Incorporated

Recent Developments

- In February 2025, ASE Technology Holding inaugurated its largest overseas facility in Penang, Malaysia. The launch aims to expand operations in robotics and AI, support supply chain realignment, and reinforce its position as the world’s largest chip assembly and testing provider.

- In February 2025, Resonac outlined plans for acquisitions following post-restructuring measures after lowering borrowings, with the objective of strengthening its market position amid intense competition.

- In January 2025, GlobalFoundries (GF) announced an investment of USD 575 million to build an advanced microchip packaging and photonics center in Malta, New York, supported by federal and state funding.

- In June 2024, Shin-Etsu Chemical developed new equipment to manufacture semiconductor package substrates using a dual damascene process. This breakthrough removes the requirement for interposers, lowering costs and supporting further miniaturization for advanced semiconductor packaging.

- In April 2024, Sumitomo Chemical disclosed plans to invest USD 545 million in a new semiconductor materials facility in Gunma, Japan. This investment will reinforce the firm’s supply chain and address rising demand for high-purity semiconductor process chemicals.

Report Coverage

The Semiconductor & IC Packaging Materials market report emphasizes key regions across the globe to provide a better understanding of the product to the users. Also, the report provides market insights into recent developments and trends and analyzes the technologies that are gaining traction around the globe. Furthermore, the report covers an in-depth qualitative analysis pertaining to various paradigm shifts associated with the transformation of these solutions.

The report provides a detailed analysis of the market while focusing on various key aspects such as competitive analysis, type, packaging technology, end-use industry, and their futuristic growth opportunities.

Semiconductor & IC Packaging Materials Market Report Scope

| Report Attributes | Details |

| Market size value in 2024 | USD 41.85 billion |

| Revenue Forecast in 2032 | USD 86.82 billion |

| CAGR | 9.5% from 2024 – 2032 |

| Base year | 2023 |

| Historical data | 2019 – 2022 |

| Forecast period | 2024 – 2032 |

| Quantitative units | Revenue in USD billion and CAGR from 2024 to 2032 |

| Segments Covered | By Type, By Packaging Technology, By End-Use Industry, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Semiconductor & IC Packaging Materials Market FAQ's

The Semiconductor & IC Packaging Materials Market report covering key segments are type, packaging technology, end-use industry, and region.

Semiconductor & IC Packaging Materials Market Size Worth USD 86.82 Billion by 2032

Semiconductor & IC packaging materials market exhibiting the CAGR of 9.5% during the forecast period

Asia Pacific is leading the global market

key driving factors in Semiconductor & IC Packaging Materials Market are increasing demand for semiconductor devices

Download Sample Report of Semiconductor & IC Packaging Materials Market

Please fill out the form to request a customized copy of the research report.