Shock Sensor Market Size, Share, Analysis Report, 2023-2032

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

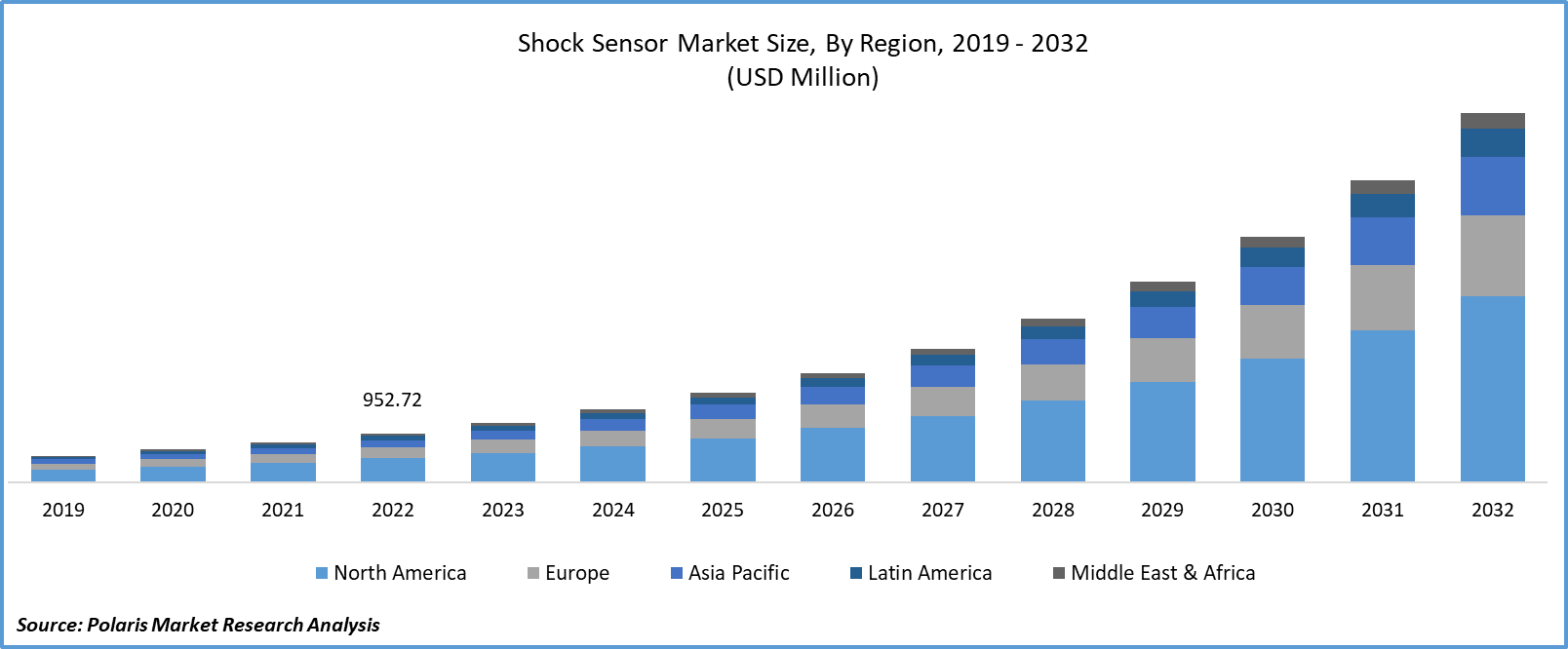

The global shock sensor market was valued at USD 952.72 million in 2022 and is expected to grow at a CAGR of 22.4% during the forecast period.

Shock sensors have revolutionized safety and security protocols across various sectors. They provide real-time monitoring of impacts, enabling rapid response to potential threats or accidents. In industries like transportation, healthcare, and defense, this technology is paramount in preventing damage to critical assets and ensuring personnel safety.

To Understand More About this Research: Download Sample Report

The integration of shock sensors in logistics and transportation has significantly reduced losses due to mishandling or accidents during transit. By alerting operators to any excessive force or impact, these sensors mitigate potential damage to fragile or high-value goods, ultimately saving businesses substantial financial losses.

Moreover, in manufacturing and electronics industries, shock sensors are instrumental in quality control. By identifying excessive shocks or vibrations during production, manufacturers can rectify potential defects before products reach the market. This results in higher product reliability and customer satisfaction.

- For instance, in November 2023, SICK introduced the MPB10 Multi-Physics Box, an innovative and robust bolt-on sensor for condition monitoring. This cutting-edge device is engineered to provide uninterrupted, real-time service data from various industrial machines, such as electric motors, pumps, fans, and conveyor systems, even in the most challenging industrial settings.

For Specific Research Requirements: Request for Customized Report

However, for smaller businesses or applications with budget limitations, the initial investment in shock sensor technology may pose a challenge. The cost of high-quality sensors and the required infrastructure may deter some potential adopters. Also, integrating shock sensors into existing systems can be complex, especially in industries with well-established protocols and equipment. This process may require substantial time, resources, and expertise, potentially acting as a deterrent for some businesses. The above factors are hampering the growth of the market.

Industry Dynamics

Growth Drivers

- Increased focus on IoT and Industry 4.0 is projected to spur product demand.

The emergence of the Internet of Things (IoT) and the advent of Industry 4.0 have hastened the adoption of shock sensors. They constitute an integral component of smart systems that necessitate instantaneous feedback on impacts, as seen in autonomous vehicles, industrial automation, and projects related to intelligent infrastructure.

Also, the proliferation of smartphones, tablets, and wearable devices has led to an unprecedented surge in the need for shock sensors within the consumer electronics sector. These sensors are pivotal in safeguarding fragile electronic components from potential impact-induced damage, thereby augmenting the overall longevity and performance of consumer devices.

In an era marked by heightened security concerns, the imperative for robust surveillance and security measures cannot be overstated. Shock sensors assume a pivotal role in such applications, furnishing an additional layer of protection by promptly alerting them to any unauthorized access attempts or physical breaches.

Moreover, rigorous safety regulations within the automotive industry are steering the integration of advanced safety features, among which shock sensors feature prominently. These sensors are indispensable for facilitating airbag deployment and optimizing the performance of other safety systems during collisions or accidents.

Report Segmentation

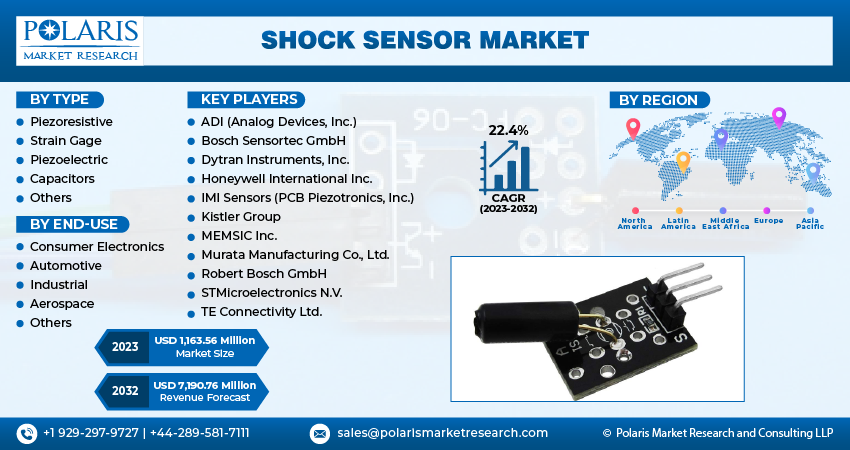

The market is primarily segmented based on type, end-use, and region.

| By Type | By End-Use | By Region |

|

|

|

To Understand the Scope of this Report: Request Customization

By Type Analysis

- The piezoresistive segment is expected to witness the fastest growth during the forecast period.

The piezoresistive segment is expected to witness the fastest growth during the forecast period. Piezoresistive sensors are crucial components that rely on changes in electrical resistance due to applied mechanical stress. This technology is highly sought after for its accuracy and sensitivity in detecting even the slightest of shocks or vibrations.

One of the key drivers behind the growth of the piezoresistive segment is its widespread application in various industries. These sensors find extensive use in automotive safety systems, aerospace applications, industrial machinery, and consumer electronics. In automotive contexts, piezoresistive shock sensors play a critical role in airbag deployment, ensuring timely and effective protection during collisions.

Furthermore, the expanding adoption of Industry 4.0 and the Internet of Things (IoT) is augmenting the demand for piezoresistive sensors. They are integral to smart systems that require real-time monitoring of impacts, such as in autonomous vehicles and industrial automation.

The healthcare sector is also witnessing a surge in demand for piezoresistive sensors. They are employed in medical devices to monitor patient movement, ensuring the effectiveness of treatment and rehabilitation programs.

Moreover, ongoing advancements in sensor technology are further enhancing the performance and capabilities of piezoresistive sensors, making them even more attractive to industries requiring precise and reliable shock detection.

Hence, the piezoresistive segment is poised for substantial growth in the these shock sensor market, driven by its versatile applications, increasing integration with advanced technologies, and continuous improvements in sensor capabilities. These sensors are set to play a pivotal role in ensuring safety and reliability across a diverse range of industries.

By End-User Analysis

- Automotive segment held the largest market share in 2022

The automotive segment held the largest market share in 2022. Stringent automotive safety regulations worldwide are pushing manufacturers to integrate advanced safety features, including shock sensors. These sensors are pivotal in airbag deployment systems, ensuring precise and timely inflation during collisions or accidents, ultimately enhancing passenger safety.

Moreover, the growing popularity of electric and autonomous vehicles is bolstering the demand for shock sensors. As electric vehicles gain traction, the need for advanced safety features remains paramount. These sensors contribute to the overall safety and performance of electric and autonomous vehicles, making them an essential component in these cutting-edge automotive technologies.

Furthermore, automakers are increasingly adopting sensor-driven driver assistance systems and collision avoidance technologies. Shock sensors play a vital role in these systems by accurately detecting sudden impacts and triggering appropriate responses, such as emergency braking or steering assistance.

Thus, the automotive segment's growth within the shock sensor market is propelled by evolving safety standards, the rise of electric and autonomous vehicles, and the increasing integration of sensor-driven technologies in modern automobiles. These factors underscore the critical role shock sensors play in enhancing automotive safety and performance.

Regional Insights

- North America region held the largest market in 2022

In 2022, the North American region held the largest market share due to technologically advanced automotive and aerospace industries fueling the demand for high-performance shock sensors. These sensors are instrumental in ensuring the safety and reliability of critical components in vehicles and aircraft.

Furthermore, the stringent regulatory environment and a strong emphasis on safety standards in North America are compelling industries to adopt advanced shock sensor technologies. It is particularly evident in sectors like automotive manufacturing, where compliance with safety regulations is paramount.

The burgeoning adoption of Industry 4.0 practices and the Internet of Things (IoT) is also amplifying the demand for shock sensors in the region. They are integral to smart systems that require real-time monitoring of impacts, driving further growth in the market.

Overall, the North American shock sensor market is poised for sustained expansion, underpinned by technological advancements, regulatory compliance, and the growing integration of advanced safety features across industries.

Asia-Pacific region is expected to witness the fastest growth during the forecast period. In China, the flourishing electronics manufacturing sector and the rapid expansion of industries like automotive and aerospace are driving the demand for advanced shock sensors. These sensors are pivotal in ensuring the integrity of electronic components and critical systems. Moreover, the surge in smart manufacturing and IoT adoption further accelerates market growth. Similarly, in India, a burgeoning automotive sector and a growing emphasis on safety standards are propelling the demand for shock sensors. These sensors play a critical role in enhancing safety features in vehicles. It, coupled with increasing industrial automation, fuels market expansion in the country.

Key Market Players & Competitive Insights

The market is anticipated to witness competition due to the existence of several players. Major service providers in the market are continuously upgrading their technologies to stay ahead of the competition and to ensure integrity, efficiency, and safety. These players focus on partnership, product upgrades, and collaboration to gain a competitive advantage over their peers and capture a significant market share.

Some of the major players operating in the global market include:

- ADI (Analog Devices, Inc.)

- Bosch Sensortec GmbH

- Dytran Instruments, Inc.

- Honeywell International Inc.

- IMI Sensors (PCB Piezotronics, Inc.)

- Kistler Group

- MEMSIC Inc.

- Murata Manufacturing Co., Ltd.

- Robert Bosch GmbH

- STMicroelectronics N.V.

- TE Connectivity Ltd.

Recent Developments

- In April 2023, GT Bicycles introduced an entirely revamped Sensor, boldly declaring it as "the most proficient trail bike we've ever crafted." Boasting a fresh, lightweight construction, meticulously honed geometry, and impeccably matched specifications, this bike is primed for unyielding performance across all terrains at any given moment.

Shock Sensor Market Report Scope

| Report Attributes | Details |

| Market size value in 2023 | USD 1,163.56 million |

| Revenue forecast in 2032 | USD 7,190.76 million |

| CAGR | 22.4% from 2023 – 2032 |

| Base year | 2022 |

| Historical data | 2019 – 2021 |

| Forecast period | 2023 – 2032 |

| Quantitative units | Revenue in USD million and CAGR from 2023 to 2032 |

| Segments covered | By Type, By End-Use, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

| Customization | Report customization as per your requirements with respect to countries, region and segmentation. |

Download Sample Report of Shock Sensor Market Size, Share, Analysis Report, 2023-2032

Please fill out the form to request a customized copy of the research report.