Small Molecule CDMO Market Size, Trends & Forecast 2025-2034

REPORT DETAILS

Market Statistics

Overview

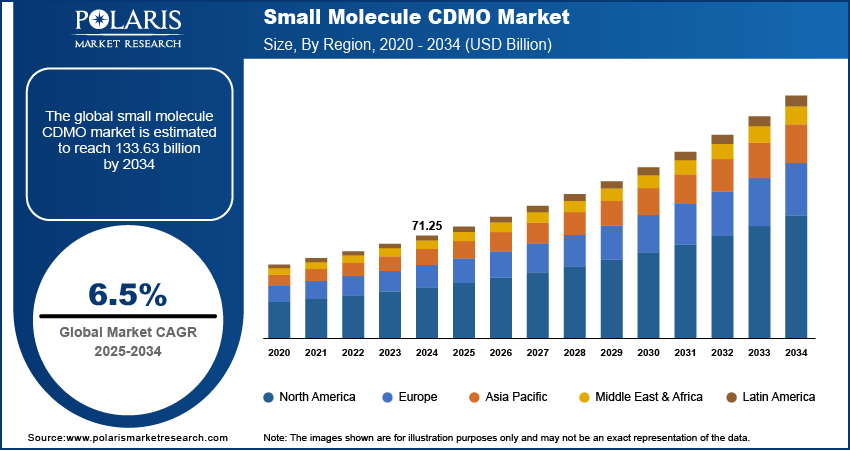

The global small molecule CDMO market size was valued at USD 71.25 billion in 2024, growing at a CAGR of 6.5% from 2025 to 2034. Pharmaceutical companies increasingly outsource small molecule drug development and manufacturing to CDMOs to reduce capital investment, improve operational efficiency, and leverage specialized expertise, driving consistent market expansion.

Key Insights

- The active pharmaceutical ingredients (API) segment led in 2024, driven by rising outsourcing of complex synthesis to specialized small molecule CDMOs.

- The innovators segment held the largest share in 2024, due to high outsourcing demand for novel small molecule drug development.

- North America dominated the small molecule CDMO market in 2024, supported by advanced manufacturing infrastructure and strong regulatory frameworks.

- The U.S. led the regional market in 2025, driven by its concentration of pharmaceutical giants, biotech firms, and global contract service providers.

- The market in Asia Pacific is projected to register the highest CAGR from 2025 to 2034, fueled by expanding manufacturing capacity and investments in advanced facilities.

- China led the region due to large-scale production capabilities, rapid adoption of advanced technologies, and strong government support for pharma modernization.

Industry Dynamics

- Rising demand for complex small molecule therapies in oncology and CNS disorders is increasing reliance on specialized CDMO partners.

- Growing pressure to reduce drug development timelines and costs is accelerating outsourcing across clinical and commercial manufacturing stages.

- Expansion into integrated end-to-end service models enables CDMOs to offer seamless development, scale-up, and regulatory support for global clients.

- Stringent regulatory requirements and quality compliance standards increase operational complexity and delay project timelines in global manufacturing networks.

Market Statistics

- 2024 Market Size: USD 71.25 billion

- 2034 Projected Market Size: USD 133.63 billion

- CAGR (2025–2034): 6.5%

- North America: Largest market in 2024

Source: Polaris Market Research Analysis

The small molecule contract development and manufacturing organization (CDMO) market refers to service providers that support pharmaceutical companies in the development, manufacturing, and commercialization of small molecule drugs. These organizations offer end-to-end solutions, including process development, active pharmaceutical ingredient production, formulation, and packaging. The solutions enable pharmaceutical firms to optimize costs, scale production, ensure regulatory compliance, and accelerate time-to-market for new therapeutics. The steady approval of new small molecule therapeutics fuels demand for CDMO services, as drug developers require scalable, compliant, and cost-efficient manufacturing capabilities.

Adoption of continuous manufacturing, advanced analytical tools, and automation enhances production efficiency, quality control, and flexibility in small molecule drug manufacturing. Moreover, increasing demand for highly potent active pharmaceutical ingredients (HPAPIs) and complex formulations boosts the need for CDMOs with specialized containment and handling capabilities.

Drivers & Opportunities

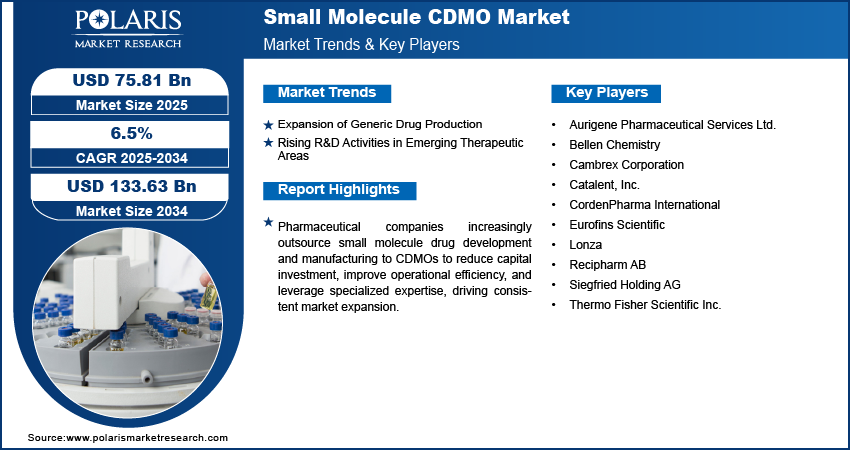

Expansion of Generic Drug Production: The increasing wave of patent expirations for bestseller drugs is creating a surge in demand for generic alternatives. According to India’s Ministry of Commerce and Industry, in 2023, India exported USD 25.8 billion worth of pharmaceuticals, with generic drugs accounting for over 70%. Pharmaceutical companies are actively seeking to introduce cost-effective versions of these drugs to meet growing patient needs, especially in price-sensitive markets. This shift is opening significant opportunities for small molecule CDMOs, as they can provide the technical expertise, infrastructure, and scalable production capabilities required for efficient generic manufacturing. Their ability to manage complex formulations, ensure regulatory compliance, and deliver high-quality products at competitive costs makes them valuable partners in the rapidly expanding generic drug landscape.

Rising R&D Activities in Emerging Therapeutic Areas: Pharmaceutical innovation in areas such as oncology, rare diseases, and central nervous system (CNS) disorders is accelerating, driven by unmet medical needs and advancements in drug discovery. According to the National Institutes of Health (NIH), the U.S. government invested USD 47.5 billion in biomedical R&D in 2024, with significant funding directed toward gene therapies, oncology, and rare disease research. These fields often require specialized development processes, complex formulations, and tailored manufacturing solutions, leading companies to collaborate with CDMOs early in the drug development cycle. Small molecule CDMOs play a critical role in supporting preclinical research, process optimization, and clinical trial material supply. Their flexibility, technical know-how, and regulatory expertise enable pharmaceutical firms to reduce timelines and costs while ensuring high-quality outcomes in these high-growth therapeutic segments.

Source: Polaris Market Research Analysis

Segmental Insights

Product Analysis

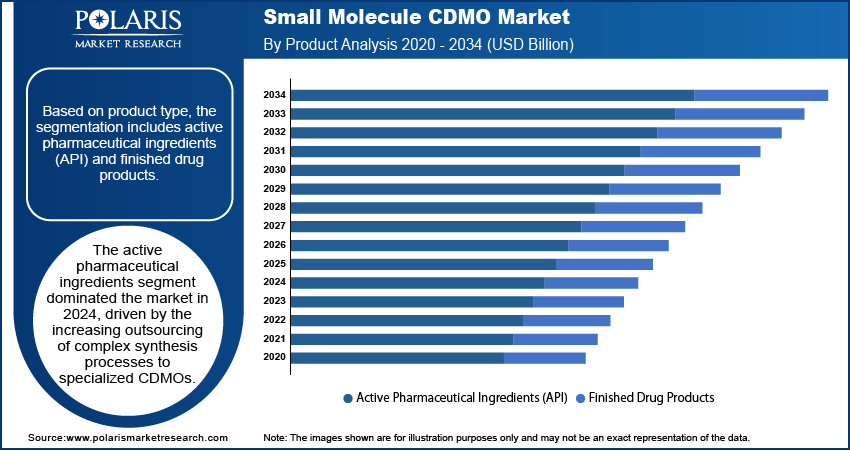

Based on product type, the segmentation includes active pharmaceutical ingredients (API) and finished drug products. The active pharmaceutical ingredients segment dominated the market in 2024, driven by the increasing outsourcing of complex synthesis processes to specialized CDMOs. The growing demand for high-potency APIs, particularly in oncology and specialty therapeutics, is pushing pharmaceutical companies to rely on CDMOs with advanced manufacturing capabilities and containment facilities. Rising cost pressures and the need for efficient scale-up from clinical to commercial production are also encouraging partnerships. Additionally, the globalization of supply chains and stricter quality standards have strengthened the role of CDMOs in delivering consistent, compliant API production for both innovators and generics.

The finished drug products segment is expected to register a significant CAGR from 2025 to 2034, supported by increasing demand for end-to-end manufacturing solutions. Pharmaceutical companies are increasingly seeking CDMOs that can handle formulation development, packaging, and final product release in one integrated process. This trend is especially prominent in oral solid dosage forms and complex delivery systems, where expertise in stability, bioavailability enhancement, and patient-friendly formats is essential. The shift toward outsourcing commercial-scale manufacturing to reduce capital investment and streamline supply chains is positioning CDMOs as key partners in delivering ready-to-market finished products.

Drug Type Analysis

In terms of drug type, the segmentation includes innovators and generics. The innovators segment held the largest revenue share in 2024 due to the high level of outsourced manufacturing for novel small molecule therapies. The growing complexity of drug molecules, coupled with the need for specialized analytical methods, makes CDMO partnerships vital during both development and commercialization. Pharmaceutical innovators often engage CDMOs to accelerate timelines, manage scale-up challenges, and maintain flexibility across global markets. Increasing investments in niche therapeutic areas and personalized medicine are boosting reliance on CDMOs with advanced technical expertise and regulatory compliance capabilities for high-value innovative drugs.

The generics segment is expected to register the highest CAGR from 2025 to 2034, fueled by a surge in patent expirations and the entry of cost-competitive products in multiple therapeutic categories. Generic drug manufacturers are turning to CDMOs to optimize production costs, ensure consistent quality, and meet stringent global regulatory requirements. CDMOs with experience in process optimization and efficient large-scale manufacturing are well-positioned to support rapid market launches. Additionally, the expansion of generics into emerging markets is creating opportunities for CDMOs to provide localized manufacturing solutions and supply chain support, further accelerating growth in this segment.

Application Analysis

In terms of application, the segmentation includes oncology, cardiovascular disease, central nervous system conditions, autoimmune/inflammation, and others. The oncology segment held the largest revenue share in 2024, driven by the rapid growth of targeted therapies, combination treatments, and high-potency oncology drugs. The complexity of manufacturing cytotoxic and highly potent compounds requires specialized containment facilities and technical expertise, making CDMO partnerships essential. Pharmaceutical companies are outsourcing both API and finished dosage production to CDMOs to streamline timelines for oncology drug launches, particularly in fast-track regulatory pathways. The increasing number of oncology clinical trials and global demand for innovative cancer treatments are keeping CDMOs at the forefront of manufacturing in this segment.

The autoimmune/inflammation segment is expected to grow significantly from 2025 to 2034, supported by advances in understanding immune system pathways and the rise of precision medicine approaches. Small molecule therapies targeting chronic inflammatory conditions are expanding, creating demand for flexible manufacturing solutions. CDMOs are becoming key partners in developing formulations that improve patient adherence and reduce side effects. The growing prevalence of autoimmune disorders, coupled with pipeline expansion in niche indications, is leading to increased outsourcing for both clinical trial material supply and commercial-scale production in this therapeutic area.

Source: Polaris Market Research Analysis

Regional Analysis

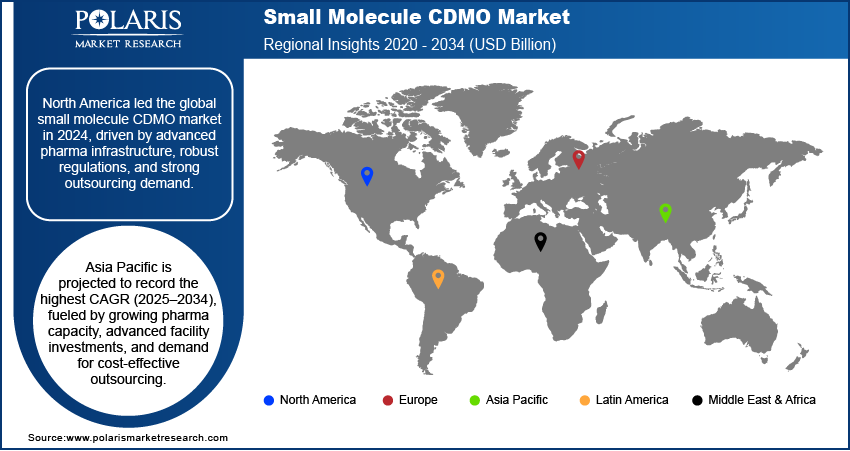

The North America small molecule CDMO market dominated revenue share in 2024 due to a strong presence of advanced pharmaceutical manufacturing infrastructure, well-established regulatory frameworks, and high demand for outsourcing from large-scale drug developers. Robust investment in technology-driven production capabilities, combined with expertise in handling complex small molecule APIs, has strengthened the region’s position. The concentration of experienced CDMOs with end-to-end capabilities, including development, scale-up, and commercial manufacturing, has further attracted both domestic and international clients. Additionally, strong funding for drug discovery programs and high adoption of innovative manufacturing techniques have ensured consistent demand for contract services across multiple therapeutic areas.

U.S. Small Molecule CDMO Market Insights

The U.S. dominated the North America market in 2024 due to its concentration of leading pharmaceutical companies, biotech innovators, and contract service providers operating at a global scale. The country’s strong intellectual property protection, advanced manufacturing technologies, and regulatory expertise have fostered confidence among drug developers for outsourcing. The presence of specialized CDMOs with capabilities in high-potency API production, continuous manufacturing, and complex formulation development has driven significant market share. High levels of R&D investment, combined with an increasing number of clinical trials, have driven sustained demand for outsourcing. The U.S. also benefits from strong supply chain integration and access to a skilled scientific workforce.

Asia Pacific Small Molecule CDMO Market Trends

The industry market in Asia Pacific is expected to register the highest CAGR from 2025 to 2034 due to expanding pharmaceutical manufacturing capacity, increasing investments in advanced production facilities, and rising demand for cost-effective outsourcing solutions. Governments across the region are supporting industry growth through favorable policies, tax incentives, and regulatory streamlining to attract global clients. Rapid growth of domestic pharmaceutical companies, coupled with increasing collaborations with multinational drug developers, is fueling market expansion. Additionally, the growing clinical trial activity in emerging economies and the availability of skilled chemists and engineers at competitive costs are positioning the region as a preferred outsourcing destination.

China Small Molecule CDMO Market Overview

China led the Asia Pacific market in 2024 due to large-scale pharmaceutical manufacturing capacity, rapid adoption of advanced production technologies, and significant government support for industry modernization. According to China’s Ministry of Industry and Information Technology, in 2024, China expanded its pharmaceutical manufacturing capacity by 22% year-on-year, with over 1,200 new GMP-certified facilities adopting AI-driven process control and continuous manufacturing technologies. The country has become a global hub for cost-effective API manufacturing while advancing capabilities in high-value small molecule drug development. Rising domestic demand for innovative and specialty generic drugs, combined with strong export potential, has accelerated CDMO growth. Strategic collaborations with international pharmaceutical companies, expansion into regulated markets, and investments in quality compliance have further strengthened China’s leadership. Additionally, the country’s growing expertise in handling complex synthesis processes has attracted more high-value outsourcing contracts.

Europe Small Molecule CDMO Market Assessment

The market in Europe is growing significantly due to strong regulatory compliance standards, a concentration of specialized CDMOs, and growing collaborations with global pharmaceutical companies. The region benefits from expertise in niche manufacturing capabilities such as high-potency APIs, advanced formulations, and continuous processing technologies. Demand is being supported by a steady pipeline of innovative drugs from European biotech firms, alongside increasing outsourcing by established pharma companies to optimize efficiency. Strategic mergers and acquisitions are consolidating capabilities, enabling service providers to offer comprehensive solutions from early development to commercial production. Additionally, supportive government funding for R&D and manufacturing innovation is fueling the region’s growth.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The competitive landscape of the small molecule CDMO market is shaped by dynamic industry analysis, where players focus on market expansion strategies to strengthen their global footprint. Strategic alliances and joint ventures are being leveraged to access new capabilities, enhance production capacity, and expand service portfolios across the drug development cycle. Mergers and acquisitions remain a critical growth approach, enabling companies to integrate specialized expertise and expand geographic reach, while post-merger integration focuses on streamlining operations and maximizing synergies. Technology advancements in continuous manufacturing, process optimization, and automation are driving competitive differentiation, allowing service providers to deliver higher efficiency, reduced costs, and faster time-to-market. Continuous investments in R&D, regulatory compliance, and flexible manufacturing models further enhance competitiveness, while collaborations with pharmaceutical innovators and generic manufacturers ensure a strong project pipeline and sustained market growth. This evolving competitive environment rewards innovation, operational excellence, and strategic global positioning.

Key Players

- Aurigene Pharmaceutical Services Ltd.

- Bellen Chemistry

- Cambrex Corporation

- Catalent, Inc.

- CordenPharma International

- Eurofins Scientific

- Lonza

- Recipharm AB

- Siegfried Holding AG

- Thermo Fisher Scientific Inc.

Small Molecule CDMO Industry Developments

January 2025: BioCina and NovaCina, two global contract development and manufacturing organizations (CDMOs), announced a strategic merger that would create a strong brand in small molecule and biopharmaceutical contract manufacturing.

October 2024: Thermo Fisher launched its Accelerator Drug Development suite, offering end-to-end services in manufacturing, clinical research, and supply chain for small molecules, biologics, and cell and gene therapies.

June 2024: Siegfried announced plans to acquire an early-phase CDMO facility in Wisconsin, U.S., focused on highly potent APIs, to enhance its early-stage development and manufacturing capabilities in North America.

Small Molecule CDMO Market Segmentation

By Product Outlook (Revenue, USD Billion, 2020–2034)

- Active Pharmaceutical Ingredients (API)

- Finished Drug Products

By Drug Type Outlook (Revenue, USD Billion, 2020–2034)

- Innovators

- Generics

By Application Outlook (Revenue, USD Billion, 2020–2034)

- Oncology

- Cardiovascular Disease

- Central Nervous System (CNS) Conditions

- Autoimmune/Inflammation

- Others

By Regional Outlook (Revenue, USD Billion, 2020–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Small Molecule CDMO Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 71.25 billion |

| Market Size in 2025 | USD 75.81 billion |

| Revenue Forecast by 2034 | USD 133.63 billion |

| CAGR | 6.5% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Small Molecule CDMO Market FAQ's

The global market size was valued at USD 71.25 billion in 2024 and is projected to grow to USD 133.63 billion by 2034.

The global market is projected to register a CAGR of 6.5% during the forecast period.

North America dominated the small molecule CDMO market in 2024 due to a strong presence of advanced pharmaceutical manufacturing infrastructure, well-established regulatory frameworks, and high demand for outsourcing from large-scale drug developers.

A few of the key players in the market are Aurigene Pharmaceutical Services Ltd.; Bellen Chemistry; Cambrex Corporation; Catalent, Inc.; CordenPharma International; Eurofins Scientific; Lonza; Recipharm AB; Siegfried Holding AG; and Thermo Fisher Scientific Inc.

The active pharmaceutical ingredients segment dominated the market in 2024, driven by the increasing outsourcing of complex synthesis processes to specialized CDMOs

The innovators segment held the largest revenue share in 2024 due to the high level of outsourced manufacturing for novel small molecule therapies.

Download Sample Report of Small Molecule CDMO Market

Please fill out the form to request a customized copy of the research report.