Synthetic Paper Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

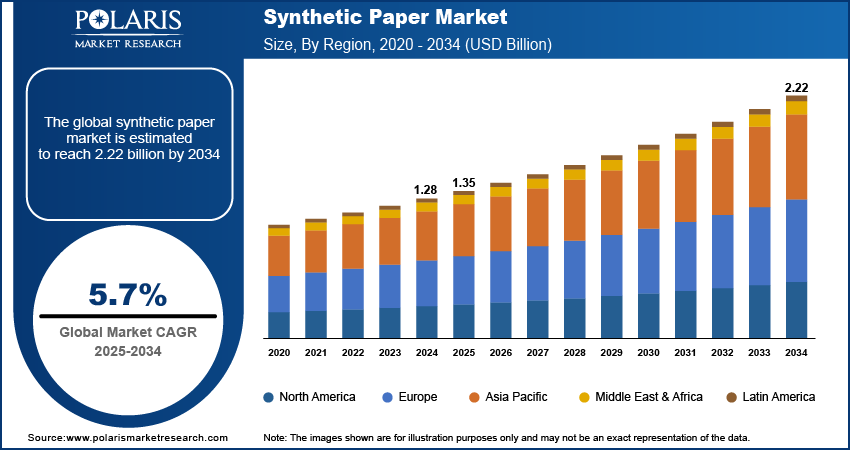

Synthetic Paper Market Summary

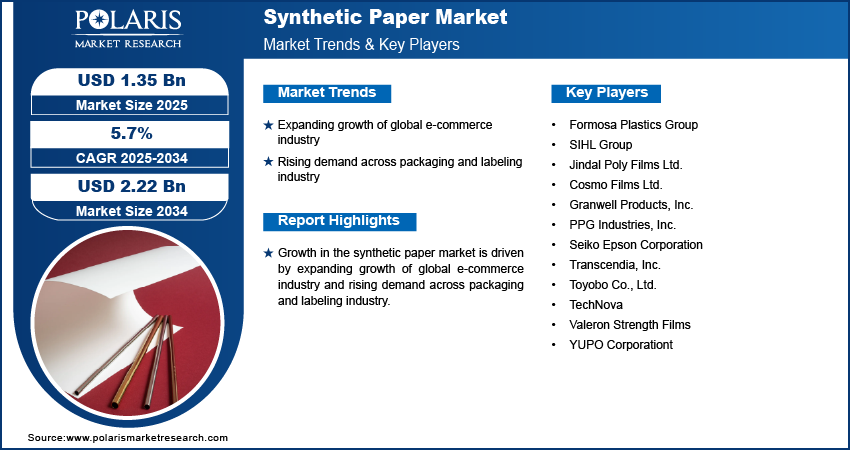

The global synthetic paper market size was valued at USD 1.35 billion in 2025, growing at a CAGR of 5.7% from 2026–2034. Expanding growth of global e-commerce industry and rising demand across packaging & labeling industry are driving the growth of synthetic paper industry.

Market Statistics

Key Takeaways

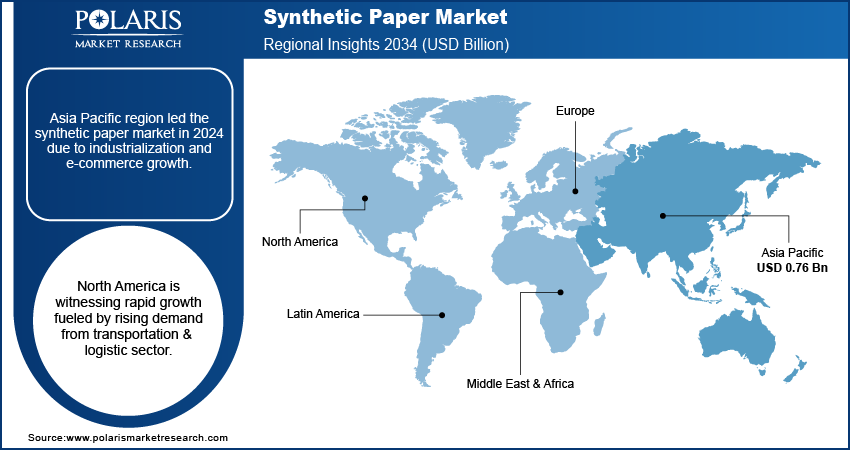

- Asia Pacific dominated the global market with 40.25% revenue share in 2025. The increasing penetration of online shopping platforms and rapid industrialization propel the regional market growth.

- In 2025, China held the largest share of 78.2% in the Asia Pacific market. The dominance is attributed to its leadership in the largest production and consumption of plastic films and packaging.

- The North America market is projected to register the highest CAGR of 5.8% during 2026–2034. The expansion of the e-commerce and logistics sectors would propel demand for synthetic papers.

- The biaxially oriented polypropylene (BOPP) segment dominated the market with 58.6% share in 2025. The leading position is attributed to its exceptional printability, moisture resistance, and strength.

- The labels & tags segment is projected to exhibit the highest CAGR of 6.5% during the forecast period. The growth is driven by the expansion of the e-commerce industry.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Expanding growth of global e-commerce industry is driving the growth of synthetic paper market.

- The global market is experiencing growth, driven by the rising demand across packaging and labeling industry for premium packaging solutions.

- Development of bio-based and carbon-neutral synthetic resins for paper production creates opportunity for the market.

- Volatility in raw material price restrains the growth of market.

What is synthetic paper market encompasses of?

The synthetic paper encompasses a diverse range of non-tearable, water-resistant, and durable paper-like materials primarily produced from synthetic resins such as polypropylene (PP) and polyethylene (PE). It is engineered to combine the printability and look of regular paper and the higher strength and durability of plastic films. Synthetic paper is used in printing, labeling, packaging, tags, maps, and menus in industries like food & beverages, cosmetics, pharmaceuticals, and logistics.

Generally, synthetic paper is used extensively across various industries owing to its durability and water resistance ability. Within the packaging industry, it provides tear-resistant and environmentally-friendly substitutes for conventional paper. The printing and advertising sectors utilize it for banners, posters, and maps that need long-lasting quality. It is also used in tags, ID cards, and manuals in the industrial and retail industries.

Comparison Matrix: Synthetic Paper Vs. Traditional Paper

| Parameter | Synthetic Paper | Traditional Paper |

| Raw Material | Made from synthetic polymers such as polypropylene (PP) or HDPE | Made from natural cellulose fibers (wood pulp) |

| Durability | Highly durable, tear-resistant, and long-lasting | Low durability; prone to tearing and wear |

| Water Resistance | Waterproof and moisture-resistant | Absorbs water, leading to damage and deformation |

| Chemical Resistance | Resistant to oils, chemicals, and solvents | Low resistance; can degrade when exposed to chemicals |

| Temperature Stability | Performs well under extreme temperatures | Sensitive to heat and cold; may warp or become brittle |

| Print Quality | Sharp, vibrant prints due to non-porous surface | Moderate print quality due to ink absorption |

| Ink Absorption | Non-absorbent; ink sits on surface | Absorbent; ink penetrates fibers |

| Longevity | Long lifespan; resistant to fading and degradation | Shorter lifespan; may yellow or degrade over time |

| Environmental Impact | Not easily biodegradable; recyclable in limited cases | Biodegradable and widely recyclable |

| Cost | Higher initial cost but cost-effective for long-term use | Lower upfront cost but higher replacement frequency |

| Applications | Labels, maps, ID cards, outdoor signage, packaging | Books, newspapers, office printing, packaging |

| Performance in Harsh Conditions | Excellent performance in outdoor/industrial environments | Poor performance in harsh environments |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

The market is primarily driven by innovations in film-forming and coating technologies, which improve print quality, ink adhesion, and recyclability. Global manufacturers are more often incorporating environmentally friendly resins and promoting sustainable manufacturing to conform to environmental regulations as well as circular economy objectives. For example, in November 2024, Huge Paper introduced SuperYupo and PaperTyger, robust synthetic papers with two-sided printability and resistance against water and tears.

Drivers & Opportunity

Which are the driving factors for synthetic paper market growth?

Expanding Growth Global of E-commerce Industry: The burgeoning growth of online business is fueling demand for synthetic paper as it is tear-resistant and moisture-proof, printable, and durable, which makes it best suited for use in packaging and labeling. Synthetic paper is used extensively by online sellers for tags, shipping labels, and product information inserts. Its ability to maintain print quality during transport enhances brand presentation and readability. As per Internation Trade Administration (ITA), the worldwide B2B e-commerce increasing from USD 17.88 trillion in 2021 to USD 36.16 trillion by 2030.

Rising Demand Across Packaging and Labeling Industry: Synthetic paper industry is experiencing growth due to increasing demand in the packaging and label industry. It is owing to its strength, tear resistance, and high-quality prints. According to the Packaging Industry Association of India (PIAI), India's paper packaging market was USD 18.6 billion in 2024 and expected to reach USD 28.3 billion by 2033 with a growth rate of 4.56% from 2025-2033. This highlights a strong growth potential for market in the coming future.

Source: Polaris Market Research Analysis

Segmental Insights

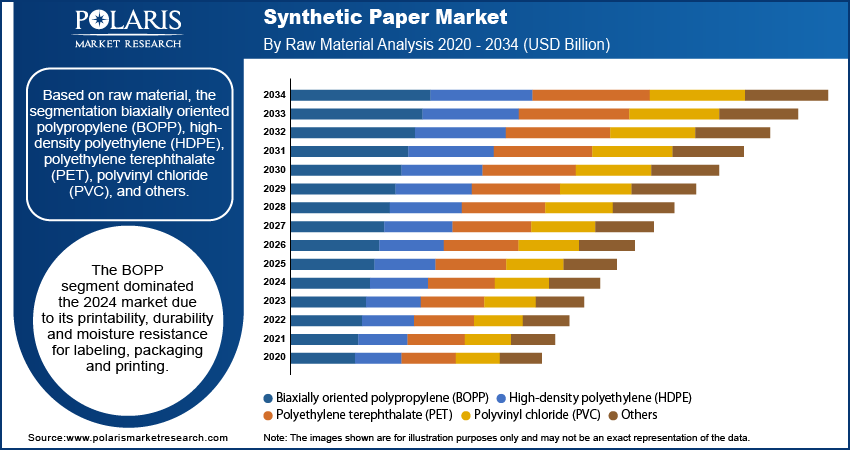

By Raw Material

Based on raw material type, the segmentation includes biaxially oriented polypropylene (BOPP), high-density polyethylene (HDPE), polyethylene terephthalate (PET), and polyvinyl chloride (PVC), and others. The biaxially oriented polypropylene (BOPP) segment dominated the market with 58.6% share in 2025, due to its exceptional printability, strength, and moisture resistance ability, which are the most suitable for labelling, packaging, and printing applications.

The HDPE segment is expected to register the highest CAGR over the forecast period, driven by mounting demand for weatherproof and tear-resistant materials used in industrial labels, signs, and maps. Synthetic papers based on HDPE provide superior strength, chemical resistance, and recyclability and hence find use as a material of choice in eco-conscious markets.

| Parameter | BOPP Synthetic Paper (Biaxially Oriented Polypropylene) | HDPE Synthetic Paper (High-Density Polyethylene) |

| Material Structure | Biaxially stretched polypropylene film for enhanced strength and clarity | High-density polyethylene with a fibrous or film-like structure |

| Surface Finish | Smooth, glossy or matte surface with premium feel | Matte, paper-like texture with a softer feel |

| Printability | Excellent print quality with sharp images and vibrant colors | Good printability but slightly lower image sharpness |

| Durability | High tensile strength and tear resistance | Very high tear resistance with flexibility |

| Water Resistance | Fully waterproof and moisture-resistant | Fully waterproof and moisture-resistant |

| Chemical Resistance | Strong resistance to oils and chemicals | Excellent chemical resistance, especially in harsh environments |

| Temperature Resistance | Performs well under moderate temperature variations | Better performance in extreme temperatures (both high and low) |

| Flexibility | Less flexible compared to HDPE | Highly flexible and fold-resistant |

| Opacity | High opacity with bright white appearance | Moderate opacity with natural paper-like look |

| Weight | Lightweight | Slightly heavier than BOPP |

| Environmental Profile | Recyclable (polypropylene-based), but limited biodegradability | Recyclable (polyethylene-based), non-biodegradable |

| Cost | Generally more cost-effective for high-volume printing | Slightly higher cost due to enhanced durability |

| Key Applications | Labels, packaging, tags, commercial printing, magazines | Maps, ID cards, outdoor signage, industrial tags, durable documents |

| Performance in Harsh Conditions | Suitable for moderate outdoor use | Superior performance in extreme outdoor and industrial environments |

Source: Polaris Market Research Analysis

By Application

Based on application type, the segmentation includes printing, labels & tags, packaging, and others. The packaging segment is the leading segment of synthetic paper market in 2025 by 32.5% share due to its widespread adoption across food & beverage, personal care, and pharmaceuticals. Its high strength, resistance to moisture, and improved print quality make it best suited for high-performance and premium packaging.

The labels & tags segment is projected to exhibit the highest CAGR of 6.5% during the forecast period, driven by increasing demand from retail, logistic, and e-commerce industries. The segment is fueled by the tear resistance, weatherability, and suitability with a number of printing methods of synthetic paper, resulting in long-lasting and high-quality labelling solutions.

By End User

Based on end user, the segmentation includes industrial, institutional, and commercial & retail. Commercial & retail segment is expected to expand at the highest CAGR over the forecast period, fueled by growing use of synthetic paper in promotional content, point-of-sale displays, and premium packaging.

The commercial & retail segment is projected to grow at the fastest CAGR during the forecast period, driven by increasing adoption of synthetic paper in promotional materials, point-of-sale displays, and high-quality packaging.

Source: Polaris Market Research Analysis

Regional Analysis

Asia Pacific dominated the global market with 40.25% revenue share in 2025 due to high-speed industrialization and the growing e-commerce growth in key economies like China, India, and Japan. The growth in online shopping boosted demand for long-lasting and superior quality packaging and label materials.

China Synthetic Paper Market Insights

In 2025, China held the largest share of 78.2% in the Asia Pacific market, fueled by strong demand from packaging, labeling, and printing sectors. Growth in e-commerce, retail, and industrial sectors further increasing the adoption of durable and high-quality synthetic paper. According to International Trade Administration (ITA), the China e-commerce industry grew by 9.9% and projected to hit USD 3.6 trillion by 2028 from USD 2.20 trillion in 2023, highlighting a strong growth in the synthetic paper industry.

Europe Synthetic Paper Market Insights

The Europe held substantial share in market, driven by increasing adoption of durable, weather-resistant, and recyclable synthetic paper aligns with Europe’s stringent environmental and regulatory standards. According to Environmental Paper Network, the Europe Deforestation Regulation (EUDR) is set to ensure that products entering or leaving the Europe do not contribute to forest destruction.

North America Synthetic Paper Market Insights

The North America market is projected to register the highest CAGR of 5.8% during 2026–2034 due to increasing applications of synthetic paper in labeling and point-of-sale printing. Moreover, the expansion of the e-commerce and logistics industries is increasing consumption of durable shipping labels. According to the U.S. Department of Commerce, the U.S. logistics industry recorded USD 2.3 trillion in costs and USD 155.4 billion in foreign investment in 2023.

The U.S. Synthetic Paper Market Insights

The U.S. market for synthetic paper dominated the market due to high demand for packaging converters and advanced printing service providers requiring moisture-resistant and long-lasting substrates. Furthermore, increasing usage of eco-friendly synthetic polymers is helping drive sustainability efforts in labelling and publishing.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The synthetic paper industry is moderately fragmented and it faces competition through innovation in material performance, printability, and sustainability. The top players are targeting high-quality BOPP, HDPE, and PET-based papers for packaging, labelling, and industrial uses. Ongoing R&D investment is facilitating the creation of recyclable, sustainable, and high-durability synthetic paper solutions. These efforts aid long-term competitiveness and enable companies to comply with changing regulation and environment mandates.

Who are the major key players in synthetic paper market?

Key players operating in the market are Formosa Plastics Group, SIHL Group, Jindal Poly Films Ltd., Cosmo Films Ltd., Granwell Products, Inc., PPG Industries, Inc., Seiko Epson Corporation, Transcendia, Inc., Valeron Strength Films, Toyobo Co., Ltd., TechNova, and YUPO Corporation.

Key Players

- Formosa Plastics Group

- SIHL Group

- Jindal Poly Films Ltd.

- Cosmo Films Ltd.

- Granwell Products, Inc.

- PPG Industries, Inc.

- Seiko Epson Corporation

- Transcendia, Inc.

- Toyobo Co., Ltd.

- TechNova

- Valeron Strength Films

- YUPO Corporation

Industry Development

- January 2026: Kernow North America, a supplier of digitally printable synthetic papers, introduced KernowPrint Unlimited synthetic paper range. This range comprises three products, including KernowPrint FG (PET), KernowPrint FLEX Lite (PP), and KernowPrint X (PET)(Source:kernowcoatings.com).

- September 2025: Cosmo Films launched CSP-Dualcoat Synthetic Paper offering double-sided printability and high durability for labels, tags, and outdoor applications(Source:cosmofilms.com).

- July 2025: Midland Paper introduced Digital Edge Environmental Polyester, a fully recyclable synthetic paper made from 100% post-consumer recycled polyester with 31.8% lower CO₂ emissions. (Source: midlandco.com)

- June 2025: Cosmo First Limited commissioned a new BOPP film production line at its manufacturing facility in Aurangabad, India. The project, involving an investment of over INR 400 crore, added an annual capacity of 81,200 metric tonnes and increased the company’s total BOPP capacity by about 40% to 277,000 metric tonnes(Source:indiatimes.com).

- November 2024: Huge Paper, in collaboration with Yupo, launched SuperYupo synthetic paper in Canada. The new product allows double-sided printing with standard paper inks while maintaining the durability, water resistance, and UV stability characteristic of traditional synthetic paper. This innovation simplifies printing workflows and expands the use of synthetic paper for high-quality printing and labeling applications(Source:signmedia.ca).

Market Segmentation

By Raw Material

- Biaxially oriented polypropylene (BOPP)

- High-density polyethylene (HDPE)

- Polyethylene terephthalate (PET)

- Polyvinyl chloride (PVC)

- Others

By Application

- Printing

- Labels & tags

- Packaging

- Others

By End User

- Industrial

- Packaging and Labeling

- Construction and Chemical Processing

- Automotive and Transportation

- Electronics and Electrical

- Institutional

- Education and Research

- Government and Public Sector Printing

- Healthcare and Pharmaceuticals

- Commercial & Retail

- Advertising and Media

- Retail Branding

- Hospitality and Food Service

By Region

- Asia Pacific

- India

- China

- Japan

- Rest of Asia Pacific

- Europe

- Germany

- UK

- France

- Italy

- Rest of Europe

- North America

- The U.S.

- Canada

- Rest of North America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of Middle East & Africa

Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 1.35 Billion |

| Market Size in 2026 | USD 1.42 Billion |

| Revenue Forecast by 2034 | USD 2.22 Billion |

| CAGR | 5.7% from 2026–2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026–2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Techniqueat |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Synthetic Paper Market FAQ's

The global market size was valued at USD 1.35 billion in 2025 and is projected to grow to USD 2.22 billion by 2034.

The global market is projected to register a CAGR of 5.7% during the forecast period.

Asia Pacific dominated the global market with 40.25% revenue share in 2025, driven by rapid industrialization and expanding e-commerce demand for durable packaging and labeling.

A few of the key players in the market are Formosa Plastics Group, SIHL Group, Jindal Poly Films Ltd., Cosmo Films Ltd., Granwell Products, Inc., PPG Industries, Inc., Seiko Epson Corporation, Transcendia, Inc., Valeron Strength Films, Toyobo Co., Ltd., TechNova, and YUPO Corporation.

The biaxially oriented polypropylene (BOPP) segment dominated the market with 58.6% share in 2025, due to its excellent printability, durability and moisture resistance.

The labels & tags segment is projected to exhibit the highest CAGR of 6.5% during the forecast period, owing to rising demand from retail, logistics and e-commerce sectors.

North America, Europe, Asia Pacific, Latin America, Middle East & Africa.

Download Sample Report of Synthetic Paper Market

Please fill out the form to request a customized copy of the research report.