U.S. Distributed Antenna Systems Market Trends, Forecasts, and Key Players, 2025-2034

REPORT DETAILS

U.S. Distributed Antenna Systems Market Summery

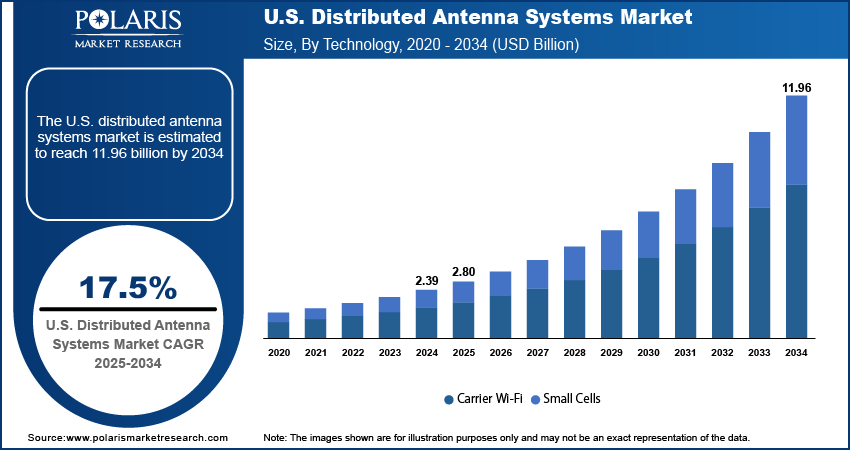

The global U.S. distributed antenna systems market size was valued at USD 2.39 billion in 2024, growing at a CAGR of 17.5% from 2025 to 2034. Growing mobile data traffic and rising 5G infrastructure are fueling the use of advanced distributed antenna systems for indoor coverage reliability.

Market Statistics

Key Takeaways

- Hardware segment led the U.S. distributed antenna systems market in 2024.

- The public safety segment is expected to record the fastest growth driven by increasing deployment of emergency communication and connectivity solutions.

Industry Dynamics

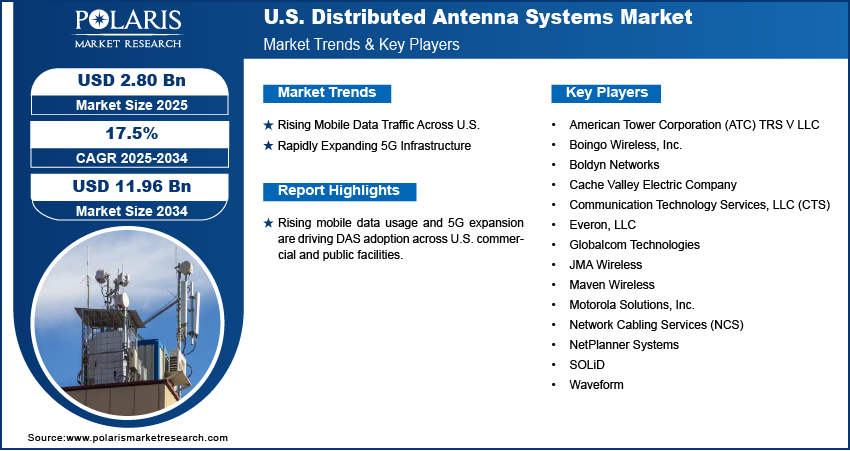

- Surging mobile data use and 5G rollout boost DAS adoption across commercial and public sites.

- Growing need for seamless indoor coverage drives deployments in enterprises, hospitals, and transport hubs.

- Fiber-based and hybrid DAS innovations improve network performance.

- High setup and maintenance costs restrict use in smaller facilities.

What is distributed antenna systems (DAS) market?

The U.S. distributed antenna systems (DAS) market features network infrastructure solutions aimed at improving wireless coverage and signal quality in indoor and outdoor settings. These systems divide cellular and data signals among multiple antennas to provide uniform connectivity in large buildings, stadiums, hospitals, airports, and campuses.

Escalating mobile data usage, increasing 5G network rollout, and rising need for smooth indoor connectivity are fueling DAS adoption in commercial and public buildings. For instance, in October 2025, SOLiD unveiled an in-building approved DAS solution for AT&T, T Mobile and Verizon, supporting easy multi-carrier indoor coverage for businesses. Surging investments in smart building initiatives and public safety comms networks are contributing further to market expansion.

Source: Polaris Market Research Analysis

Despite these advantages, expensive installation costs, complex integration needs, and regulatory hurdles constrain adoption for small and medium-sized businesses. Improved fiber-based and hybrid DAS technologies, coupled with the development of neutral-host and shared infrastructure concepts offer opportunities for compact network growth and enterprise-class connectivity in the American market.

Drivers & Opportunities

Which are the factors driving U.S. distributed antenna systems market growth?

Rising Mobile Data Traffic Across U.S.: The accelerated development of mobile data consumption throughout enterprises and public areas is fueling demand for consistent indoor network coverage. CTIA's 2024 survey stated that wireless networks supported 100.1 trillion megabytes of data in 2023, an 89% increase from 2021 and the highest-ever annual increase. Strong data usage due to video streaming, IoT, and business use cases is pressurizing operators and proprietors of commercial buildings to install distributed antenna systems to reinforce signal quality and ensure seamless connectivity.

Rapidly Expanding 5G Infrastructure: The continuing rollout of 5G networks in the U.S. is speeding up the installation of innovative distributed antenna systems. As 5G requires higher frequency bands and denser network infrastructure, DAS solutions are being adopted to extend coverage, support high-speed data transmission, and improve user experience across large commercial and industrial environments. 5G Americas reported that North America drove the world in 5G adoption during Q2 2025 with 339 million subscriptions and the greatest data consumption, averaging 111 GB per customer per month.

Source: Polaris Market Research Analysis

Segmental Insights

Offering Analysis

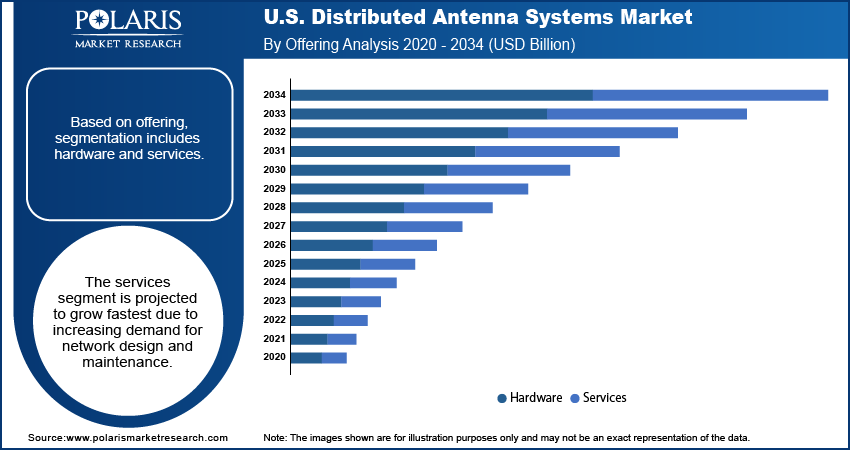

By offering, the market is divided into hardware and services. Hardware segment led in the U.S. distributed antenna systems market in 2024, fueled by enterprise-level demand for antennas, cables, and signal boosters. In addition, consistent updates in network infrastructure are driving steady hardware replacement and growth.

The services segment is projected to grow at the fastest CAGR during the forecast period, supported by rising demand for network design, installation, and maintenance services. In addition, growing outsourcing by enterprises is fueling service-based DAS deployment models.

DAS Type Analysis

Based on DAS type, the market is segmented into passive, active, and hybrid. Active segment led the market in 2024 due to its capability to enable high-capacity and long-distance signal transmission. In addition, growing adoption in large venues and public facilities is driving its market share.

The hybrid segment is poised to witness the highest growth CAGR over the forecast period, led by its programmable architecture with active and passive components. In September 2025, Wilson Connectivity launched a hybrid DAS that provides cost-effective, multi-carrier indoor coverage for small to medium enterprises. Besides, its cost-effectiveness and scalability are compelling enterprise investments.

Coverage Analysis

Based on coverage, the market is segmented into indoor and outdoor. The indoor segment led the market in 2024 due to increasing demand for reliable indoor connectivity in offices, hospitals, and commercial properties. Additionally, the speedy growth of smart building initiatives is propelling the use of indoor DAS solutions.

The outdoor segment is anticipated to grow at the fastest CAGR during the forecast period, owing to the increasing development of connected transportation infrastructure. In addition, rising public safety communication requirements are boosting outdoor DAS installations across urban areas.

Ownership Analysis

Based on ownership, the market is segmented into neutral host, carrier, and enterprise. The carrier segment led the market in 2024 due to massive investments by telecom operators in expanding network coverage. Moreover, carrier-owned DAS networks provide improved service reliability and streamlined maintenance operations across facilities.

The neutral host segment is projected to grow at the fastest CAGR during the forecast period, supported by the shared infrastructure model that lowers capital expenditure. In addition, the rising need for multi-operator connectivity in public spaces is driving adoption.

Technology Analysis

Based on technology, the market is segmented into carrier Wi-Fi and small cells. The small cells segment led the market in 2024 due to its capacity to increase network capacity in high-density urban areas. Additionally, its integration with the current infrastructure is pushing effective indoor and outdoor network development.

The carrier Wi-Fi segment is anticipated to witness the highest CAGR throughout the forecast period owing to rising enterprise demand for wireless high-speed connectivity. In addition, the rise in data-intensive applications is pushing Wi-Fi-enabled DAS deployments.

User Facility Analysis

Based on user facility, the market is segmented into >500K FT2, 200 K–500k FT2, and <200 K FT2. The >500K FT2 segment dominated the market in 2024, driven by extensive installations in large buildings, stadiums, and airports. In addition, the increasing demand for multi-carrier coverage in expansive areas is fueling the growth of large-scale DAS networks

The 200K–500K FT2 segment is anticipated to grow at the fastest CAGR during the forecast period, supported by the rising adoption of DAS solutions across mid-sized office complexes and healthcare facilities. In addition, flexible deployment models are encouraging adoption in this segment.

Vertical Analysis

Based on vertical, the market is segmented into commercial, industrial, public safety, transportation, and residential. The commercial segment led the market in 2024, propelled by rising demand for continuous wireless connectivity in offices, malls, and hospitality establishments. Furthermore, extending enterprise communication networks is enhancing commercial DAS installations throughout the country.

Public safety segment is expected to advance at the highest CAGR over the forecast period, driven by rigorous regulations for emergency communication systems. Furthermore, increasing application of DAS in hospitals and government buildings is boosting market penetration.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The U.S. distributed antenna systems market is competitive, with network integrators and manufacturers competing to develop advanced fiber-based and hybrid DAS solutions to enhance signal reliability and coverage efficiency. In addition, partnerships between telecom operators and infrastructure providers are accelerating technology adoption across commercial, industrial, and public facilities.

Who are the major players in U.S. distributed antenna systems market?

Some of the major firms in the U.S. distributed antenna systems sector are Waveform, SOLiD, Boldyn Networks, American Tower Corporation (ATC) TRS V LLC, Network Cabling Services (NCS), Boingo Wireless, Inc., Globalcom Technologies, Cache Valley Electric Company, JMA Wireless, Everon, LLC, Maven Wireless, NetPlanner Systems, Communication Technology Services, LLC (CTS), and Motorola Solutions, Inc.

Key Players

- American Tower Corporation (ATC) TRS V LLC

- Boingo Wireless, Inc.

- Boldyn Networks

- Cache Valley Electric Company

- Communication Technology Services, LLC (CTS)

- Everon, LLC

- Globalcom Technologies

- JMA Wireless

- Maven Wireless

- Motorola Solutions, Inc.

- Network Cabling Services (NCS)

- NetPlanner Systems

- SOLiD

- Waveform

U.S. Distributed Antenna Systems Industry Developments

- October 2025: SOLiD introduced the BARS system, a cost-effective Distributed Antenna System (DAS) solution designed to enhance multi-carrier indoor connectivity for underserved mid-sized buildings.

- May 2025: Verizon announced to deploy and manage a neutral-host DAS at the new Highmark Stadium to deliver high-speed 5G connectivity for fans and venue operations.

- November 2024: Verizon deployed the first interoperable multi-vendor O-RAN-based DAS in commercial venues, enabling open-vendor connectivity and improved efficiency.

U.S. Distributed Antenna Systems Market Segmentation

By Offering Outlook (Revenue, USD Billion, 2020–2034)

- Hardware

- Services

By DAS Type Outlook (Revenue, USD Billion, 2020–2034)

- Passive

- Active

- Hybrid

By Coverage Outlook (Revenue, USD Billion, 2020–2034)

- Indoor

- Active DAS

- Amplifiers (Remote Units)

- Master Units

- Cables

- Others

- Passive DAS

- Antennas

- Signal Boosters

- Splitters and Combiners

- Cables

- Others

- Hybrid DAS

- Active DAS

- Outdoor

By Ownership Outlook (Revenue, USD Billion, 2020–2034)

- Neutral Host

- Carrier

- Enterprise

By Technology Outlook (Revenue, USD Billion, 2020–2034)

- Carrier Wi-Fi

- Small Cells

By User Facility Outlook (Revenue, USD Billion, 2020–2034)

- >500K FT2

- 200K–500K FT2

- <200K FT2

By Vertical Outlook (Revenue, USD Billion, 2020–2034)

- Commercial

- Offices

- Shopping Malls & Retail Stores

- Hotels & Hospitality

- Educational Institutions

- Healthcare Facilities

- Industrial

- Manufacturing Plants & Warehouses

- Oil & Gas

- Mining

- Power Generation & Utility Plants

- Public Safety

- Government & Administrative Offices

- Military & Defense

- Public Safety & Emergency Response Centers

- Transportation

- Airports & Seaports

- Railway Stations & Metro Line

- Highways & Tunnels

- Parking Complexes

- Residential

U.S. Distributed Antenna Systems Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 2.39 Billion |

| Market Size in 2025 | USD 2.80 Billion |

| Revenue Forecast by 2034 | USD 11.96 Billion |

| CAGR | 17.5% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

U.S. Distributed Antenna Systems Market FAQ's

The global market size was valued at USD 2.39 billion in 2024 and is projected to grow to USD 11.96 billion by 2034.

The global market is projected to register a CAGR of 17.5% during the forecast period.

A few of the key players in the market are Waveform, SOLiD, Boldyn Networks, American Tower Corporation (ATC) TRS V LLC, Network Cabling Services (NCS), Boingo Wireless, Inc., Globalcom Technologies, Cache Valley Electric Company, JMA Wireless, Everon, LLC, Maven Wireless, NetPlanner Systems, Communication Technology Services, LLC (CTS), and Motorola Solutions, Inc.

The hardware segment dominated in 2024 due to high demand for antennas, cables, and signal boosters.

The public safety segment is projected to grow fastest due to rising deployment of emergency communication networks.

Download Sample Report of U.S. Distributed Antenna Systems Market

Please fill out the form to request a customized copy of the research report.