U.S. Metal Powder Market Analyzing Key Players and Innovations through, 2026-2034

REPORT DETAILS

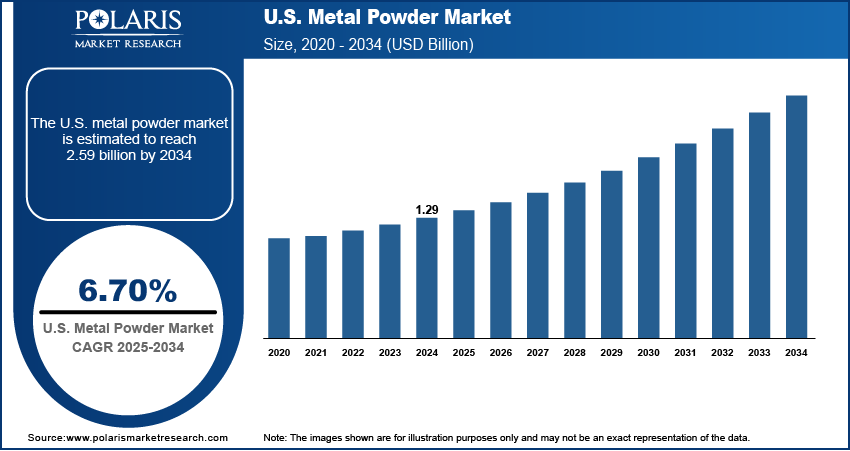

U.S. Metal Powder Market Summary

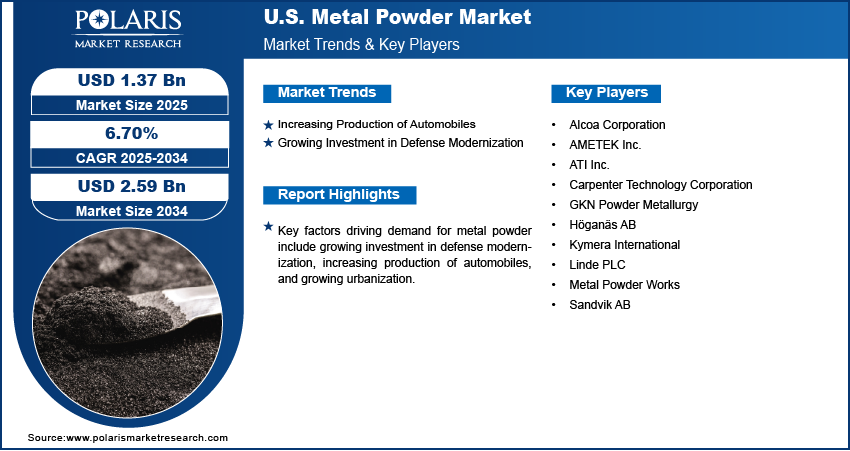

The U.S. metal powder market size was valued at USD 1.37 billion in 2025, growing at a CAGR of 6.70% from 2026 to 2034. Key factors driving demand for metal powder include growing investment in defense modernization, increasing production of automobiles, and growing urbanization

Market Statistics

Key Takeaways

- The chemical segment accounted for 60.55% of the revenue share in 2025 due to its ability to produce powders with uniform particle size.

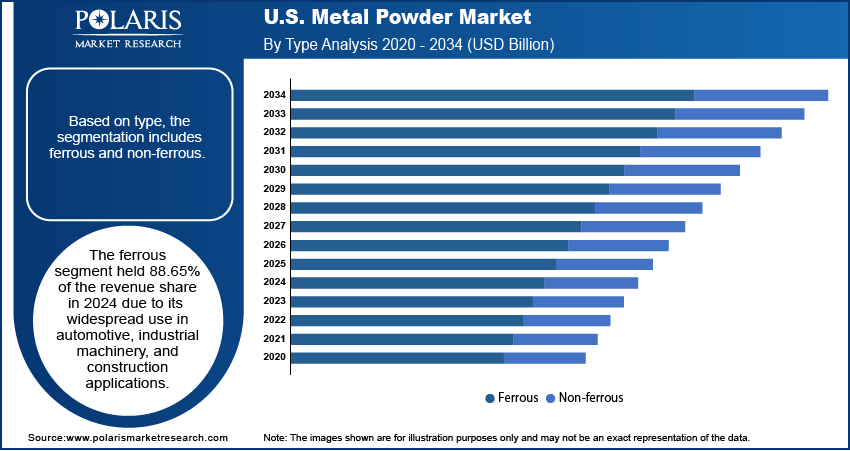

- The ferrous segment held 88.65% of the revenue share in 2025 due to its widespread use in industrial machinery.

- The press & sinter segment accounted for 74.00% from 2026 to 2034, owing to its role in producing high-volume components for the automotive industry.

- The aerospace & defense segment is estimated to grow at a CAGR of 8.95% from 2026 to 2034, owing to the increasing use of additive manufacturing.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Increasing production of automobiles is propelling the demand for metal powder, as automakers are using these powders extensively to create complex, lightweight, and high-strength components.

- Growing investment in defense modernization is fueling the demand for metal powder as modern defense equipment requires high-performance materials that offer superior strength, durability, and lightweight properties.

- The increasing industrialization is creating a lucrative market opportunity.

- The high production and handling costs of metal powder may hamper the market growth.

AI Impact on U.S. Metal Powder Market

- AI enhances production efficiency by optimizing metal powder manufacturing processes.

- Predictive maintenance reduces downtime in powder production facilities.

- AI accelerates R&D, enabling faster development of advanced alloy powders in the U.S. market

What is Metal Powder?

Metal powder refers to finely divided particles of metals such as aluminum, copper, iron, nickel, and titanium that are produced through processes like atomization, reduction, or electrolysis. These powders serve as essential raw materials in powder metallurgy, additive manufacturing, and thermal spraying. They enable the production of lightweight, durable, and complex components with high precision. Industries such as automotive, aerospace, electronics, and construction rely on these powders to create parts with improved strength, wear resistance, and performance.

Powder Metallurgy vs Traditional Metal Manufacturing

Powder metallurgy (PM) process offers superior material efficiency, precision, and sustainability than conventional metal manufacturing methods, including casting, forging, and machining. The process involves compacting metal powders into desired shapes and sintering them to create high-performance components. It leads to minimal waste and excellent dimensional accuracy. Traditional manufacturing methods are used for large-scale and heavy-duty applications. They involve higher material loss, extensive machining, and greater energy consumption.

| Parameter | Powder Metallurgy | Traditional Metal Manufacturing |

| Material Efficiency | Near-net-shape production enables very high material utilization with minimal scrap generation | Significant material loss occurs during machining, cutting, and finishing processes |

| Production Cost | Cost-effective for high-volume manufacturing due to reduced machining and lower waste | Higher operational and material costs due to extensive machining and processing |

| Precision & Accuracy | Provides excellent dimensional control and repeatability for complex parts | Requires additional finishing and machining to achieve tight tolerances |

| Waste Reduction | Generates very low waste and allows recycling of unused powders | Produces higher scrap and excess material during fabrication |

| Design Flexibility | Supports intricate geometries, porous structures, and complex internal features | Complex designs increase tooling complexity and machining costs |

| Scalability | Highly suitable for automated mass production and consistent output | Better suited for low-volume or customized manufacturing applications |

| Energy Consumption | Lower energy usage as metals are sintered rather than fully melted | Higher energy demand due to melting, casting, and extensive processing |

| Sustainability | Environmentally friendly with reduced waste and improved resource utilization | Higher environmental impact from scrap generation and energy-intensive operations |

| Typical End-Use Industries | Automotive, aerospace, medical devices, electronics, industrial machinery, additive manufacturing, defense | Construction, shipbuilding, heavy machinery, oil & gas, infrastructure, railways, and large-scale industrial manufacturing |

| Common Applications | Gears, bearings, filters, structural parts, cutting tools, EV components | Beams, pipes, forged components, castings, industrial equipment, structural assemblies |

Source: Polaris Market Research Analysis

The U.S. metal powder market continues to expand due to the nation’s strong industrial base, advanced manufacturing capabilities, and rising adoption of additive manufacturing technologies. Growing demand for lightweight materials in the automotive and aerospace sectors is driving the consumption of powders such as aluminum and titanium. The country’s focus on electric vehicle production, defense innovation, and sustainable manufacturing further supports market growth. Additionally, the presence of major powder producers, technological advancements, and government investments in research and development strengthen the U.S. position as a global metal powder industry.

Source: Polaris Market Research Analysis

The demand for metal powders in the U.S. is driven by the growing urbanization. According to the World Bank Group, the urban population in the U.S. reached 84% in 2024 from 83% in 2022. This increased the construction of high-rise buildings, bridges, and infrastructure projects that required advanced materials, and metal powders played a crucial role in producing high-strength, lightweight materials through processes like additive manufacturing (3D printing) and powder metallurgy. Urbanization in the country is also increasing the development of consumer electronics, medical devices, and industrial machinery, all of which rely on metal powder components. Additionally, the push for sustainable and energy-efficient solutions in urban areas is boosting the adoption of metal powders in renewable energy technologies, such as wind turbines and solar panels. Therefore, the growing urbanization in the U.S. is fueling the demand for metal powders.

Drivers & Opportunities/Trends

Increasing Production of Automobiles: Automakers are using metal powders extensively in powder metallurgy and additive manufacturing (3D printing) to create complex, lightweight, and high-strength components such as gears, engine parts, and structural elements. Therefore, the growing production of automobiles is driving the demand for metal powder. United States Motor Vehicle Production was reported at 10,611,555.000 units in Dec 2023. This records an increase from the previous number of 10,052,958.000 units for Dec 2022. The rise of electric vehicles (EVs) is further accelerating the demand for metal powder, since EVs require specialized parts such as battery components, electric motor cores, and heat exchangers that rely on metal powders for precision and performance. Mass production of cars is also driving the need for cost-effective, scalable manufacturing processes, and metal powders enable efficient, high-volume production with minimal material waste. Additionally, the push for fuel efficiency and reduced emissions in vehicles is compelling manufacturers to adopt lighter materials, and metal powders help achieve these goals by allowing the creation of intricate, optimized designs that traditional methods cannot match.

Growing Investment in Defense Modernization: Modern defense equipment, such as advanced aircraft, armored vehicles, missiles, and drones, requires high-performance materials that offer superior strength, durability, and lightweight properties, all of which metal powders provide through processes like additive manufacturing and powder metallurgy. The production of complex, precision-engineered components for stealth technology, ballistic protection, and high-temperature applications relies heavily on metal powders, which enable the creation of parts with complex geometries and enhanced mechanical properties. Additionally, the push for rapid prototyping and on-demand production in defense industries favors metal powder-based technologies, allowing for faster development and customization of critical components. Therefore, as the country allocates more resources to defense innovation and self-reliance, the need for advanced materials such as metal powders continues to surge.

Source: Polaris Market Research Analysis

Segmental Insights

Production Method Analysis

Based on production method, the segmentation includes chemical, mechanical, and physical. The chemical segment accounted for 60.55% of the revenue share in 2025 due to its ability to produce powders with high purity, uniform particle size distribution, and superior quality, which industries such as automotive, aerospace, and healthcare highly demand. Manufacturers favored this method as it ensured consistent performance in applications like additive manufacturing, powder metallurgy, and specialized coatings. The growing adoption of advanced manufacturing technologies, particularly in defense and biomedical applications, also supported the expansion of this method, as it enables the creation of powders with precise compositions and enhanced functionality.

Type Analysis

Based on type, the segmentation includes ferrous and non-ferrous. The ferrous segment held 88.65% of the revenue share in 2025 due to its widespread use in automotive, industrial machinery, and construction applications. Manufacturers preferred these powders as they offer excellent strength, durability, and cost-effectiveness, making them suitable for producing gears, bearings, and structural components through powder metallurgy. The strong demand for stainless steel and iron powders in heavy-duty applications further strengthened the segment’s position. Expanding infrastructure projects and the continued need for robust machinery parts also created consistent growth opportunities for ferrous-based material.

The non-ferrous segment is expected to grow at a CAGR of 7.62% from 2026 to 2034, owing to the rising adoption of lightweight and high-performance materials in aerospace, defense, and electric vehicle production. Industries favor non-ferrous powders such as aluminum, titanium, and copper as they combine strength with reduced weight, which supports fuel efficiency and energy savings. Growing investment in 3D printing and additive manufacturing is projected to further accelerate demand, since non-ferrous alloys allow the precise fabrication of complex parts with superior corrosion resistance.

Comparison Matrix: Ferrous vs Non-Ferrous Metal Powders

| Parameter | Ferrous Powders | Non-Ferrous Powders |

| Composition | Primarily iron-based metals and alloys | Metals excluding iron, such as aluminum, copper, titanium, nickel, and cobalt |

| Key Properties | High strength, durability, magnetic properties, cost-effectiveness | Lightweight, corrosion resistance, high conductivity, non-magnetic properties |

| Cost | Generally lower cost | Relatively higher cost due to specialized metals |

| Corrosion Resistance | Moderate; often requires coatings or alloying | Excellent natural corrosion resistance |

| Common Applications | Automotive parts, gears, bearings, industrial machinery, structural components | Aerospace components, electronics, medical implants, batteries, additive manufacturing |

| Manufacturing Usage | Widely used in powder metallurgy and mass production | Preferred for high-performance and lightweight applications |

| End-Use Industries | Automotive, industrial manufacturing, construction, machinery | Aerospace, electronics, healthcare, energy, defense |

Source: Polaris Market Research Analysis

Application Analysis

In terms of application, the segmentation includes additive manufacturing, press & sinter, metal injection molding, and others. The press & sinter segment accounted for 74.00% from 2026 to 2034, owing to its role in producing high-volume components for automotive, industrial, and consumer goods. Manufacturers relied on this method as it delivers cost efficiency, design flexibility, and strong mechanical properties, which are essential for parts such as gears, bearings, and bushings. The continued demand for reliable and durable metal components in heavy-duty applications further contributed to the dominance of the segment.

End Use Analysis

In terms of end use, the segmentation includes automotive, industrial, aerospace & defense, construction, healthcare, and others. The aerospace & defense segment is estimated to grow at a CAGR of 8.95% from 2026 to 2034, owing to the increasing use of additive manufacturing to produce lightweight, high-strength components with precise geometries. Aircraft and defense system manufacturers prefer powders such as titanium, aluminum, and nickel alloys as they offer superior strength-to-weight ratios and resistance to extreme operating conditions. The rising demand for fuel-efficient aircraft, combined with stringent regulatory requirements for safety and performance, is projected to accelerate the adoption of advanced powder-based production. Expanding investments in defense modernization programs and next-generation aircraft platforms are further strengthening the segment’s dominance.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The U.S. metal powder market features a competitive landscape shaped by established players and specialized producers serving aerospace, automotive, industrial, and additive manufacturing sectors. Key companies such as Carpenter Technology Corporation, ATI Inc., and GKN Powder Metallurgy dominate through advanced material innovation and vertical integration. Global firms like Höganäs AB and Sandvik AB maintain strong U.S. operations, leveraging technical expertise in iron, steel, and specialty alloy powders. Industrial gas and material suppliers like Linde PLC contribute through powder production and recycling technologies. Alcoa Corporation and AMETEK Inc. focus on high-performance aluminum and specialty metal powders, respectively. Emerging demand from additive manufacturing is driving consolidation and R&D investments. Competition is focused on purity, consistency, customization, and cost-efficiency, with companies expanding capabilities to meet stringent industry standards and evolving customer requirements across defense, energy, and medical applications.

Major companies operating in the U.S. metal powder industry include Alcoa Corporation, AMETEK Inc., ATI Inc., Carpenter Technology Corporation, GKN Powder Metallurgy, Höganäs AB, Kymera International, Linde PLC, Metal Powder Works, and Sandvik AB.

Key Companies

- Alcoa Corporation

- AMETEK Inc.

- ATI Inc.

- Carpenter Technology Corporation

- GKN Powder Metallurgy

- Höganäs AB

- Kymera International

- Linde PLC

- Metal Powder Works

- Sandvik AB

Industry Developments

April 2026: EOS acquired 100% of Metalpine GmbH, a specialist in high-quality metal powders. Metalpine will operate as an independent company within EOS. The company will serve its global customer base with its high-quality metal powders. (Source: eos.info)

U.S. Metal Powder Market Segmentation

By Production Method Outlook (Revenue, USD Billion, 2021–2034)

- Chemical

- Mechanical

- Physical

By Type Outlook (Revenue, USD Billion, 2021–2034)

- Ferrous

- Non-ferrous

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Additive Manufacturing

- Press & Sinter

- Metal Injection Molding

- Others

By End Use Outlook (Revenue, USD Billion, 2021–2034)

- Automotive

- Industrial

- Aerospace & Defense

- Construction

- Healthcare

- Others

U.S. Metal Powder Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 1.37 Billion |

| Market Size in 2026 | USD 1.51 Billion |

| Revenue Forecast by 2034 | USD 2.59 Billion |

| CAGR | 6.70% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

U.S. Metal Powder Market FAQ's

The market size was valued at USD 1.37 billion in 2025 and is projected to grow to USD 2.59 billion by 2034.

The market is projected to register a CAGR of 6.70% during the forecast period.

A few of the key players in the market are Alcoa Corporation, AMETEK Inc., ATI Inc., Carpenter Technology Corporation, GKN Powder Metallurgy, Höganäs AB, Kymera International, Linde PLC, Metal Powder Works, and Sandvik AB.

The chemical segment dominated the market revenue with 60.55% share in 2025.

The aerospace & defense segment is projected to witness the fastest growth of CAGR 8.95% during the forecast period.

Download Sample Report of U.S. Metal Powder Market

Please fill out the form to request a customized copy of the research report.