U.S. Sterilization Container Systems Market Growth Trends, Industry Size, 2025-2034

REPORT DETAILS

REPORT DETAILS

Market Statistics

Overview

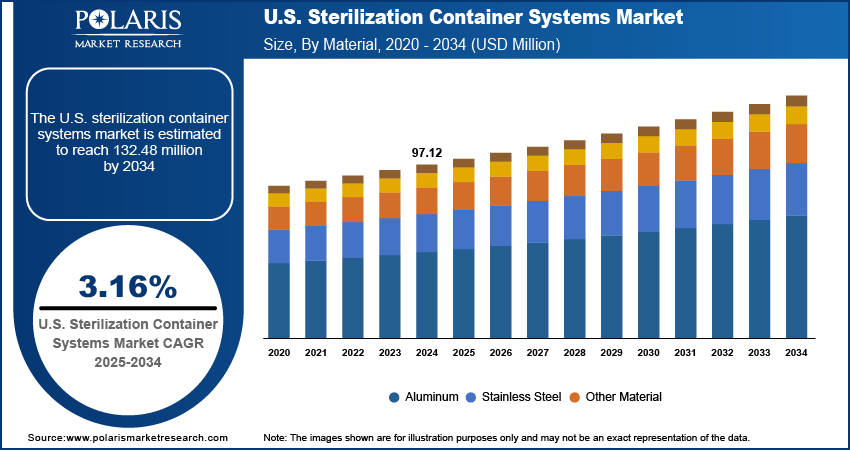

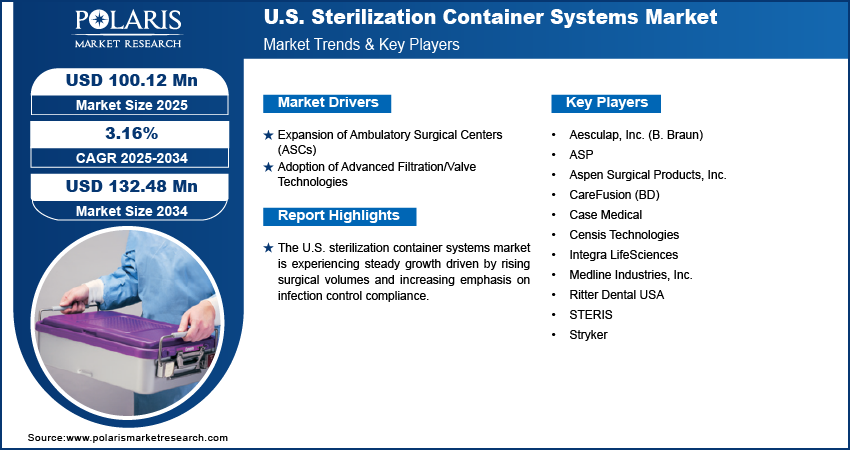

The U.S. sterilization container systems market size was valued at USD 97.12 million in 2024, growing at a CAGR of 3.16% from 2025 to 2034. Key factors driving market demand include rising surgical volumes, strict CDC & FDA sterilization guidelines, expansion of ambulatory surgical centers (ASCs), and the adoption of advanced filtration and valve technologies within sterilization container systems.

Key Insights

- The sterilization containers segment led the market revenue in 2024, owing to their durability, cost-efficiency, and contamination protection in healthcare settings.

- The non-perforated containers segment shows strong growth potential, meeting demand for enhanced protection in high-risk surgical environments.

- The filter-based systems segment dominated sales in 2024 due to their proven reliability and superior microbial barrier performance.

- The stainless steel segment emerges as the fastest-growing segment, valued for its exceptional durability, corrosion resistance, and longevity through repeated sterilization cycles.

Industry Dynamics

- Growing ASC volumes boost sterilization container needs, requiring fast instrument turnover and reliable infection control in cost-focused outpatient environment.

- Advanced filters/valves improve sterilization precision, optimizing airflow and microbial protection in steam/gas processes for better outcomes.

- High upfront costs of advanced sterilization containers limit adoption in budget-constrained hospitals, especially in emerging markets, slowing market penetration despite long-term savings.

- Rising ASC growth and outpatient surgeries create strong demand for cost-efficient, reusable containers, offering manufacturers a revenue opportunity by 2027.

Market Statistics

- 2024 Market Size: USD 97.12 million

- 2034 Projected Market Size: USD 132.48 million

- CAGR (2025–2034): 3.16%

AI Impact on U.S. Sterilization Container Systems Market

- AI-powered RFID tags automate instrument tracking in U.S. hospitals, reducing lost items and improving sterilization compliance with Joint Commission standards.

- AI analyzes usage data to forecast container wear, preventing failures and extending lifespan in high-volume ASCs and surgical centers.

- AI sensors detect moisture/contamination risks during cycles, alerting staff to reprocess loads, critical for meeting CDC and AAMI ST79 guidelines.

- AI optimizes container inventory for U.S. health systems, cutting costs via just-in-time replenishment and reduced overstock.

Sterilization container systems are rigid, reusable boxes designed to maintain the sterility of surgical instruments during storage and transport. In the U.S. market, the increasing volume of surgical procedures across hospitals and ambulatory surgical centers is boosting the demand for these systems. Healthcare facilities are placing greater focus on efficient, reusable, and cost-effective sterilization methods as surgical volumes grow due to an aging population and higher rates of chronic conditions requiring surgical intervention. A June 2024 CDC report highlighted that nearly 25% of the U.S. population will be over 65 by 2060, increasing risks for chronic conditions such as dementia, heart disease, diabetes, arthritis, and cancer, significantly boosting the need for these systems. Sterilization container systems offer a robust alternative to single-use wraps, providing enhanced protection and reducing the risk of contamination, which aligns well with the operational needs of high-throughput surgical environments.

Strict sterilization guidelines set by regulatory bodies such as the centers for disease control and prevention (CDC) and the food and drug administration (FDA) fuel the adoption of these systems in the U.S. These regulations enforce strict protocols on infection prevention, sterilization validation, and instrument reprocessing standards, thereby creating a highly regulated environment that favors the use of validated, compliant systems. Sterilization containers, with their consistent performance and traceability features, meet these compliance requirements more effectively than traditional wraps or pouches. Therefore, as regulatory scrutiny continues to increase, healthcare providers are increasingly shifting toward containerized sterilization systems to ensure safety, maintain accreditation, and reduce infection-related risks.

Drivers & Opportunities

Expansion of Ambulatory Surgical Centers (ASCs): The expansion of ambulatory surgical centers (ASCs) is contributing to the growth opportunities as these facilities continue to grow in number and procedural volume. A March 2025 Medicare report revealed that 6,300 ASCs performed procedures for 3.4 million FFS Medicare patients in 2023, with surgical volumes per beneficiary increasing 5.7% year-over-year. ASCs focus on providing same-day surgical care in a cost-effective, efficient environment, which necessitates rapid instrument turnaround and dependable sterilization practices. Sterilization container systems offer a reliable and reusable solution that ensures instrument sterility while streamlining workflow and reducing reliance on disposable wraps. Their durability and ease of handling make them well-suited for the high-frequency, fast-paced operations typical of ASCs, thereby aligning with the operational priorities of these centers.

Adoption of Advanced Filtration/Valve Technologies: The adoption of advanced filtration and valve technologies within sterilization container systems is also contributing to market growth. Healthcare facilities seek more precise and reliable sterilization outcomes. In July 2024, SteriTite launched a universal sterilization container system featuring 2D barcode scanning for traceability. The system is FDA-cleared and CE-marked. It supports all sterilization methods, eliminates wrapping, and offers durability with MediTray inserts, reducing long-term costs for healthcare facilities. These technological enhancements improve air exchange efficiency and microbial barrier protection during steam or gas sterilization processes. Advanced valves and filters enable better moisture regulation and airflow control, reducing the likelihood of contamination while optimizing drying and cooling phases. Therefore, as regulatory standards become more rigid and infection control remains a top priority, such innovations in container design offer both functional and compliance advantages, making them increasingly attractive to healthcare providers across the U.S.

Segmental Insights

Product Analysis

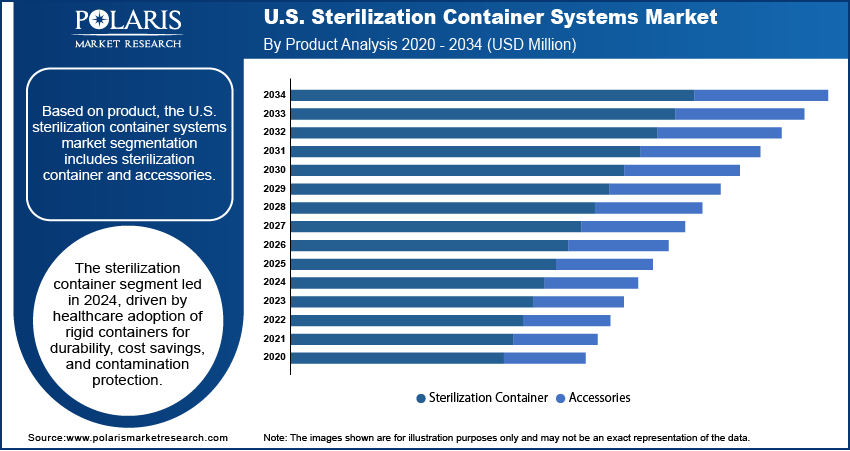

Based on product, the segmentation includes sterilization container and accessories. The sterilization container segment accounted for the largest revenue share in 2024. It is attributed to the widespread adoption of rigid containers in healthcare environments due to their durability, cost-effectiveness, and superior protection against contamination. Unlike disposable wraps, sterilization containers offer long-term usability and enhanced sterility maintenance during the storage and transport of surgical instruments. Their growing preference across hospitals and surgical centers, especially in high-volume environments, reinforces their strong position.

Type Analysis

In terms of type, the segmentation includes perforated and non-perforated. The non-perforated segment is expected to witness significant growth during the forecast period, due to the increasing need for maximum protection against external contaminants in complex and high-risk surgical procedures. These containers provide a completely sealed environment, minimizing the risk of microbial intrusion during storage and transport. As infection control protocols tighten and surgical instrument sterility becomes even more critical, the demand for non-perforated systems is anticipated to rise steadily across various healthcare facilities.

Technology Analysis

The segmentation, based on technology, includes filter and valves. The filter segment dominated the market in 2024, driven by the reliability and enhanced microbial barrier efficiency that modern filter systems provide. Filters offer consistent airflow control during sterilization cycles while maintaining an effective barrier to contaminants post-sterilization. Their replaceable nature also allows for periodic maintenance without compromising container performance, making them a favored choice in facilities focused on maintaining strict sterility standards.

Material Analysis

Based on material, the segmentation includes aluminum, stainless steel, and other material. The stainless steel segment is expected to witness the fastest growth during the forecast period due to stainless steel’s superior strength, corrosion resistance, and long service life under repeated sterilization cycles. Additionally, its non-reactive surface ensures better compatibility with various sterilization methods, such as steam and gas. Stainless steel containers are emerging as a preferred material choice across the U.S. healthcare landscape as hospitals and surgical centers increasingly seek robust, low-maintenance, and hygienic solutions.

Key Players & Competitive Analysis

The U.S. sterilization container systems market is shaped by strategic investments and technological advancements, with key players such as STERIS and B. Braun leveraging sustainable value chains to meet latent demand from hospitals and ASCs. Competitive intelligence reveals a focus on revenue growth through innovations such as smart tracking and reusable designs, aligning with industry trends toward infection control. Small and medium-sized businesses compete by offering niche solutions, while larger firms dominate via regional footprint and product offerings. Supply chain disruptions pose challenges, but future development strategies emphasize resilience through automation. Expert insights highlight a total addressable market expansion, driven by aging populations and stricter regulations. Pricing insights show premium pricing for advanced containers, though cost pressures persist. Growth projections remain strong, fueled by emerging technologies such as radio-frequency identification (RFID) integration.

A few major companies operating in the U.S. sterilization container systems market include Aesculap, Inc. (B. Braun); ASP; Aspen Surgical Products, Inc.; CareFusion (BD); Case Medical; Censis Technologies; Integra LifeSciences; Medline Industries, Inc.; Ritter Dental USA; STERIS; and Stryker.

Key Players

- Aesculap, Inc. (B. Braun)

- ASP

- Aspen Surgical Products, Inc.

- CareFusion (BD)

- Case Medical

- Censis Technologies

- Integra LifeSciences

- Medline Industries, Inc.

- Ritter Dental USA

- STERIS

- Stryker

U.S. Sterilization Container Systems Industry Developments

- March 2022: Aesculap, Inc. launched the Aicon Sterile Container System, featuring synchronized containers/baskets and an Enhanced Drying System (EDS) that reduces dry time by 47% while expanding sterile aseptic area efficiency.

U.S. Sterilization Container Systems Market Segmentation

By Product Outlook (Revenue, USD Million, 2020–2034)

- Sterilization Container

- Accessories

By Type Outlook (Revenue, USD Million, 2020–2034)

- Perforated

- Non-perforated

By Technology Outlook (Revenue, USD Million, 2020–2034)

- Filter

- Valves

By Material Outlook (Revenue, USD Million, 2020–2034)

- Aluminum

- Stainless Steel

- Other Material

By End User Outlook (Revenue, USD Million, 2020–2034)

- Hospitals

- Ambulatory Surgical Centers

- Others

U.S. Sterilization Container Systems Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 97.12 Million |

| Market Size in 2025 | USD 100.12 Million |

| Revenue Forecast by 2034 | USD 132.48 Million |

| CAGR | 3.16% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The market size was valued at USD 97.12 million in 2024 and is projected to grow to USD 132.48 million by 2034.

The market is projected to register a CAGR of 3.16% during the forecast period.

A few of the key players in the market are Aesculap, Inc. (B. Braun); ASP; Aspen Surgical Products, Inc.; CareFusion (BD); Case Medical; Censis Technologies; Integra LifeSciences; Medline Industries, Inc.; Ritter Dental USA; STERIS; and Stryker.

The sterilization container segment accounted for the largest revenue share in 2024.

The stainless steel segment is expected to witness fastest growth during the forecast period.

Download Sample Report of U.S. Sterilization Container Systems Market

Please fill out the form to request a customized copy of the research report.