AI in K-12 Education Market Growth scenario, Industry Report, 2026-2034

REPORT DETAILS

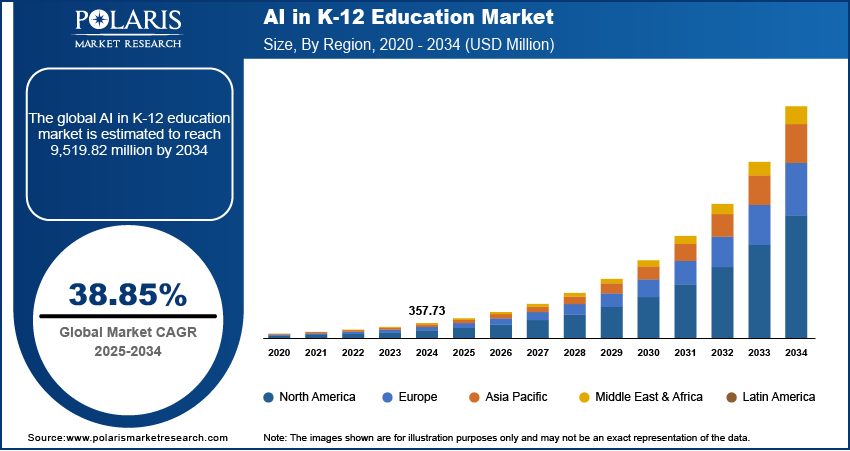

AI in K-12 Education Market summary

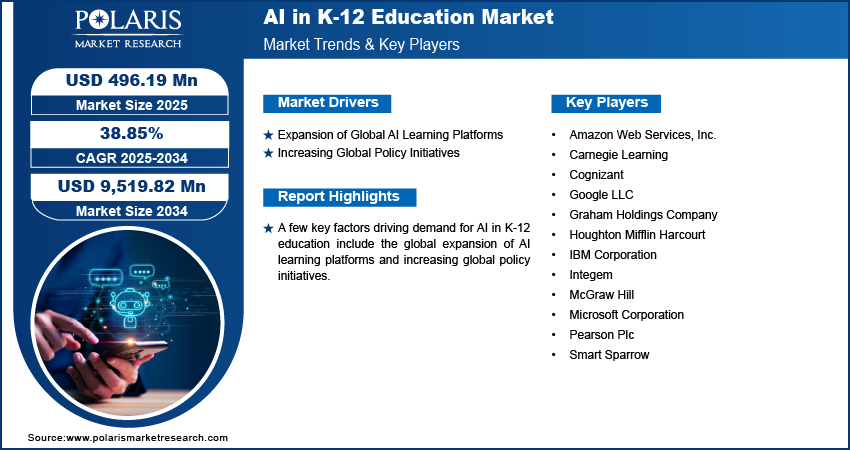

The AI in K-12 Education market size was valued at USD 496.19 million in 2025, growing at a CAGR of 38.85% from 2026 to 2034. Key factors driving demand for AI in K-12 education include the global expansion of AI learning platforms coupled with increasing policy initiatives worldwide.

Market Statistics

Key Takeaways

- The North America AI in K-12 education market dominated the market with 38.9% share in 2025.

- The U.S. AI in K-12 education market captured 89.8% share of NA in 2025, due to strong investments in EdTech, and increasing emphasis on digital transformation in schools.

- The market in Asia Pacific is projected to grow at a 38.9% from 2026-2034, propelled by government-backed digital education initiatives, and the widespread integration of smart classrooms.

- Countries such as China and Japan are playing a key role in regional growth at a CAGR of 35.8%, due to significant EdTech innovation and large-scale deployment of AI-enabled learning platforms.

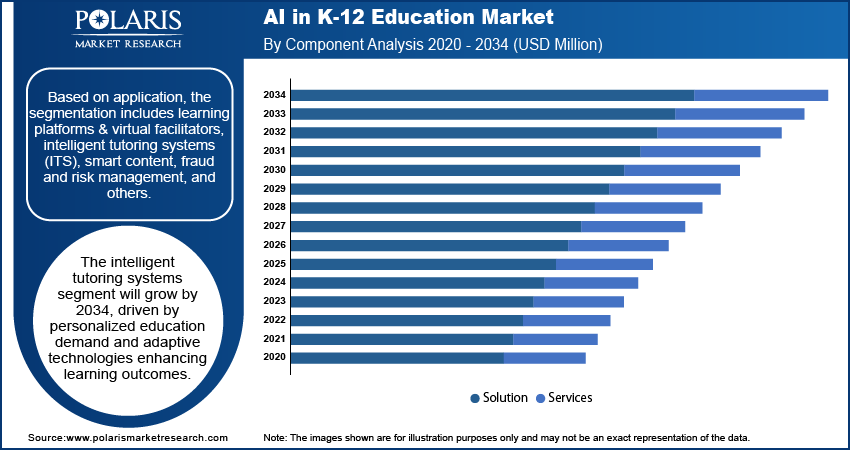

- The solutions segment dominated the market with 70.7% share in 2025.

- The services segment is projected to grow at a CAGR of 38.8% in the coming years, driven by increasing demand for AI integration, training, and maintenance support in schools.

*Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Expansion of global AI learning platforms worldwide is fueling the market growth due to rising demand for adaptive education tools, enhanced accessibility, and the ability to bridge learning gaps across diverse student groups.

- Rising policy initiatives worldwide is fueling the market growth due to increased government support for digital learning infrastructure and mandates to improve student performance through technology integration.

- The immersive learning via AI, AR, and VR integration is expected to create lucrative opportunities during the forecast period.

- The limited digital infrastructure in rural or developing regions hinders the market growth.

What is AI in K-12 Education?

AI in K-12 education refers to the integration of intelligent technologies that enhance teaching, learning, and administrative processes across primary and secondary schools. The solutions include intelligent tutoring systems, personalized learning platforms, smart content, and automated grading tools that adapt to student needs and improve academic outcomes. Schools and educational institutions are adopting AI-driven tools to streamline administrative workflows, manage data, and enhance student engagement through interactive digital learning environments. The continuous advancements in natural language processing, machine learning platform, and adaptive algorithms are further shaping the future of personalized and inclusive K-12 education worldwide.

Advancements in AI-powered decision-making tools are fueling the AI in K-12 education market by enabling schools and districts to improve efficiency, transparency, and resource allocation. For example, in June 2025, Domo and Burbio, a K-12 education data intelligence platform provider introduced an AI-driven platform that analyzes K-12 district data, providing actionable insights on spending, initiatives, and policy changes while delivering real-time alerts to stakeholders. Such innovations boost data-driven decision-making in education, enhancing operational effectiveness and helping in the broader adoption of AI solutions in the global K-12 sector.

To Understand More About this Research: Download Sample Report

Source: Polaris Market Research Analysis

The global push for digital transformation in education is driving the AI in K-12 education market, fueled by initiatives that integrate advanced technologies into classrooms to enhance learning outcomes and operational efficiency. Governments and institutions are prioritizing smart classrooms, adaptive learning platforms, and AI-driven analytics to bridge learning gaps and modernize traditional education systems. These measures modernize traditional education models and equip students with future-ready skills, positioning AI as a cornerstone of global education reforms.

How AI Works in K-12 Education

AI in K-12 education collects student data from digital platforms, assignments, and assessments. Learning patterns, progress, strengths, and weaknesses are studied through intelligent algorithms. The system creates customized educational content and study recommendations. AI tools provide real-time feedback and automated assessments. Regular performance tracking improves student performance, engagement, and learning outcomes.

AI Learning vs Traditional Learning

| Factors | AI Learning | Traditional Learning |

| Personalization | Adaptive learning based on student needs | Same teaching method for all students |

| Efficiency | Faster assessments and automated support | More manual teaching processes |

| Scalability | Supports large numbers of students online | Limited by classroom capacity |

| Teacher Workload Reduction | Reduces repetitive and administrative tasks | Teachers manage tasks manually |

| Student Engagement | Interactive tools and gamified learning | Mostly classroom-based interaction |

| Learning Outcomes | Tracks progress using real-time data | Depends on traditional assessments |

Source: Polaris Market Research Analysis

Drivers & Opportunities

Expansion of Global AI Learning Platforms: The growth of global AI learning platforms is driving the AI in K-12 Education market, fueled by increasing access to free digital resources that enhance AI awareness among students and educators. For instance, in April 2025, OpenAI recently introduced a free online AI resource hub offering courses and workshops worldwide, covering topics from foundational AI concepts to advanced applications. The platform features modules such as prompt engineering, ChatGPT on campus, and AI for K-12 students, making AI education accessible to diverse audiences, including learners, educators, and developers. These initiatives are broadening exposure to AI technologies globally, boosting their integration into K-12 education systems.

Increasing Global Policy Initiatives: The global policy initiatives motivating inclusive AI adoption are driving growth in the AI in K-12 education market, as governments and international organizations emphasize equity and accessibility. UNESCO, for instance, is actively aiding member states in leveraging AI for education through initiatives such as the Beijing Consensus, which provides guidance and competency frameworks for policymakers, teachers, and students. These efforts ensure AI integration boost inclusion while preparing education systems worldwide for the demands of the AI era.

Challenges in AI in K-12 Education Market

- Data privacy and cybersecurity concerns are increasing in digital learning platforms.

- High implementation costs are limiting AI adoption in budget-constrained schools.

- Limited digital infrastructure and internet access remain major market challenges.

- Lack of teacher training is affecting the use of AI-based learning tools.

- Ethical concerns related to AI bias and student monitoring are increasing globally.

To Understand More About this Research: Download Sample Report

Source: Polaris Market Research Analysis

Segmental Insights

Component Analysis

Based on component, the market is segmented into solutions and services. The solutions segment accounted for the largest market share of 70.7% in 2025, driven by the adoption of AI-powered learning platforms, intelligent tutoring systems, and smart content across K-12 institutions. These solutions facilitate personalized learning, real-time performance assessment, and adaptive content delivery, enhancing overall learning outcomes. The rising demand for digital classrooms and AI-assisted curriculum design is contributing to the widespread integration of AI solutions in education systems.

The services segment is projected to record the fastest growth at a CAGR of 38.8% through 2034 due to the rising demand for AI deployment, integration, maintenance, and training across K-12 institutions. These services enable schools to implement AI solutions effectively while reducing operational complexities and ensuring seamless functionality. Professional support allows educators to adopt personalized learning tools, intelligent tutoring systems, and smart content without extensive technical expertise. Expansion of consulting and managed services is helping institutions optimize AI-driven educational outcomes while maintaining compliance with data privacy and security requirements.

Deployment Analysis

By deployment, the market is segmented into cloud and on-premises. The cloud segment accounted for the largest share of 60.5% in 2025, since it allows schools to access AI-powered applications and learning platforms without extensive local infrastructure. Cloud deployment provides scalability, remote accessibility, and centralized management of student data and analytics, enhancing flexible and adaptive learning environments.

The on-premises segment is expected to grow fastest at a CAGR of 38.8% through 2034, driven by institutions that require enhanced control over sensitive student data, customized AI integrations, and secure offline functionality. Schools with strict regulatory requirements or limited internet connectivity are adopting on-premises solutions to maintain operational continuity while implementing AI systems.

Technology Analysis

Based on technology, the market is categorized into natural language processing (NLP) and machine learning. The machine learning segment accounted for the largest share of 65.2% in 2025, owing to its ability to deliver personalized learning experiences, predictive analytics for student performance, and automated assessment tools. Integration of machine learning algorithms allows educational platforms to adapt content dynamically, improving engagement and outcomes across diverse learning environments.

The natural language processing (NLP) segment is expected to witness the fastest growth at a CAGR of 37.6% over the forecast period, due to increasing adoption of AI-powered language applications in K-12 education. NLP solutions enable automated essay grading, real-time feedback, and interactive chatbots that assist students with queries, improving learning efficiency and comprehension. Schools are integrating NLP tools to support multilingual classrooms and personalized learning experiences, allowing educators to focus on conceptual teaching while AI handles routine assessment and communication tasks. Continuous advancements in speech recognition and language modeling technologies are expanding the range and accuracy of NLP applications, driving widespread implementation across public and private tutoring institutions.

Application Analysis

By application, the market is segmented into learning platforms & virtual facilitators, intelligent tutoring systems (ITS), smart content, fraud and risk management, and others. The learning platforms & virtual facilitators segment accounted for the largest share of 44.0% in 2025, owing to widespread adoption of AI-enabled platforms for lesson delivery, progress tracking, and virtual classroom management. These platforms help schools streamline administrative tasks while providing personalized learning experiences for students.

The intelligent tutoring systems (ITS) segment is expected to grow fastest at a CAGR of 38.9% through 2034, due to its ability to deliver individualized instruction, provide instant feedback, and adapt to each student’s learning pace. The integration of ITS in classrooms allows teachers to focus on conceptual understanding while AI systems handle repetitive assessment and content customization tasks. For instance, in April 2025, Varsity Tutors, a subsidiary of Nerdy Inc., launched Live + AI, an advanced AI-powered tutoring and teacher support platform designed to accelerate learning and close achievement gaps in schools nationwide.

To Understand More About this Research: Request Customization

Source: Polaris Market Research Analysis

Real-World Examples of AI in K-12 Education

| Application | Examples | Usage |

| AI Tutors | AI tutoring tools | Help students with homework and learning support |

| Automated Grading Systems | AI grading software | Check assignments and tests automatically |

| Adaptive Learning Platforms | Personalized learning platforms | Customize lessons based on student progress |

| AI Chatbots | Student support chatbots | Answer student questions instantly |

| Performance Analytics Dashboards | Teacher analytics tools | Track student performance and engagement |

| Virtual Classrooms | Online learning platforms | Support digital and remote learning |

Source: Polaris Market Research Analysis

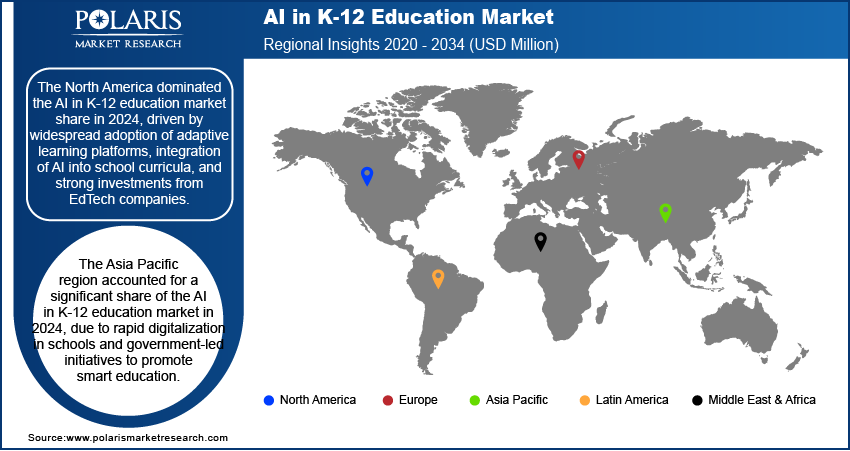

Regional Analysis

The market in North America accounted for the largest share of the AI in K-12 education market accounting for 44.3% in 2025, due to strong focus on digital learning, rising adoption of EdTech platforms, and widespread integration of AI-powered learning tools across schools. Significant funding for modernizing classrooms, coupled with active participation of technology companies in developing personalized learning solutions, continues to fortify the region’s market leadership.

The U.S. AI in K-12 Education Market Overview

Rising investment in teacher training and professional development is fueling the AI in K-12 Education market, driven by the need to equip educators with the skills required for AI-integrated learning. For instance, in July 2025, OpenAI and the American Federation of Teachers (AFT) launched the National Academy for AI Instruction, a five-year initiative aimed at preparing 400,000 K-12 educators across the U.S. with AI fluency by 2030. Backed by USD10 million in funding and resources, the program will deliver workshops, training modules, and curriculum development focused on responsible AI use in classrooms. Such large-scale investments are building teacher readiness, which is essential for accelerating AI adoption in the education sector.

Europe AI in K-12 Education Market Trends

Europe is projected to hold a substantial revenue share of 29.0% in 2025, fueled by well-established education systems, widespread digital transformation initiatives, and strict regulatory frameworks helping equitable access to AI-driven learning. Countries such as the U.K., France, and Germany are prioritizing AI in education to enhance student engagement, support multilingual learning, and boost teacher support systems. Moreover, collaboration between academic institutions, policymakers, and EdTech developers is also enabling the development of responsible AI frameworks that line up with regional values on privacy and inclusivity.

Asia Pacific AI in K-12 Education Market Assessments

Asia Pacific is projected to witness the fastest growth at a CAGR of 38.9% over the forecast period driven by the rising government investment in digital education infrastructure, and the rapid shift toward e-learning in countries such as China, Japan, and South Korea. Growing emphasis on bridging rural-urban education gaps and improving accessibility through affordable AI-powered platforms is further stimulating adoption across the region. The combination of demographic pressures and ambitious national digital education agendas positions Asia Pacific as an important growth hub in the coming years.

India AI in K-12 Education Market Insights

Government initiatives to integrate artificial intelligence in school education are fueling the AI in K-12 education market due to the growing emphasis on nurturing future-ready talent and equipping students with advanced digital skills. For example, in June 2025, India’s government unveiled the AI Policy 2025, which sets out plans to introduce AI curriculum in 35% of schools by 2029 and expand coverage to 90% by 2036. The program will gradually expose students to AI fundamentals at the primary level and progress to data science, coding, and AI ethics during secondary education. Such policies are creating strong demand for AI-driven learning platforms, intelligent tutoring systems, and smart content solutions, positioning AI as a critical enabler of next-generation education systems.

To Understand More About this Research: Request Customization

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The AI in K-12 education market is highly competitive, with key players such as Microsoft Corporation, Google LLC, IBM Corporation, Pearson plc, Smart Sparrow, and Carnegie Learning. The companies focus on developing AI-powered learning management systems, intelligent tutoring solutions, and predictive analytics tools to enhance student engagement, performance tracking, and individualized learning experiences. The competitive dynamics are further shaped by strategic partnerships with schools and educational institutions and acquisitions aimed at expanding product offerings and improving accessibility. The growing adoption of AI-driven assessment tools, virtual classrooms, and personalized learning analytics is reshaping market competition

A few major companies operating in the AI in K-12 education industry include Amazon Web Services, Inc., Cognizant, Graham Holdings Company, Microsoft Corporation, Google LLC, IBM Corporation, Pearson Plc, Integem, McGraw Hill, Houghton Mifflin Harcourt, Smart Sparrow, and Carnegie Learning.

Key Players

- Amazon Web Services, Inc.

- Carnegie Learning

- Cognizant

- Google LLC

- Graham Holdings Company

- Houghton Mifflin Harcourt

- IBM Corporation

- Integem

- McGraw Hill

- Microsoft Corporation

- Pearson Plc

- Smart Sparrow

AI in K-12 Education Industry Developments

- April 2026: Frontline Education partnered with AI for Education. The company also launched an AI K-12 Advisory Council to improve administrative and operational software. (Source: globenewswire.com)

- January 2026: Intellinetics released a new AI-driven document management platform for schools. The platform focuses on secure data management and automation. (Source: investing.com)

- June 2025: Google unveiled Gemini for Education at ISTE 2025, a cloud-based AI suite seamlessly integrated with Google Classroom, NotebookLM, and Google Forms. This innovative platform is designed to enhance learning personalization while streamlining administrative tasks for educators and students alike. (Source: blog.google)

- June 2025: Pearson partnered with Google Cloud to develop AI-powered educational tools for the K-12 sector. The collaboration aims to personalize learning experiences, provide actionable insights for teachers, and enhance digital content delivery. (Source: googlecloudpresscorner.com)

AI in K-12 Education Market Segmentation

By Component Outlook (Revenue, USD Million, 2021–2034)

- Solution

- Services

By Deployment Outlook (Revenue, USD Million, 2021–2034)

- Cloud

- On-premises

By Technology Outlook (Revenue, USD Million, 2021–2034)

- Natural Language Processing (NLP)

- Machine Learning

By Application Outlook (Revenue, USD Million, 2021–2034)

- Learning Platform & Virtual Facilitators

- Intelligent Tutoring System (ITS)

- Smart Content

- Fraud and Risk Management

- Others

By Regional Outlook (Revenue, USD Million, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

AI in K-12 Education Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 496.19 Million |

| Market Size in 2026 | USD 691.26 Million |

| Revenue Forecast by 2034 | USD 9,519.82 Million |

| CAGR | 38.85% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The AI in K-12 education market size was valued at USD 496.19 million in 2025 and is projected to grow to USD 9,519.82 million by 2034.

The AI in K-12 education market is projected to register a CAGR of 38.85% during the forecast period.

The North America AI in K-12 education market dominated the market with 38.9% share in 2025.

A few of the key players in the market are Amazon Web Services, Inc., Cognizant, Graham Holdings Company, Microsoft Corporation, Google LLC, IBM Corporation, Pearson Plc, Integem, McGraw Hill, Houghton Mifflin Harcourt, Smart Sparrow, and Carnegie Learning.

The cloud segment accounted for the largest share of 60.5% in 2025.

The natural language processing (NLP) segment is expected to witness the fastest growth at a CAGR of 37.6% over the forecast period.

Download Sample Report of AI in K-12 Education Market

Please fill out the form to request a customized copy of the research report.